Amended Prospectus

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2016 Annual Report

SULONG 2016 ANNUAL REPORT PHOENIX PETROLEUM PHILIPPINES, INC. INSIDE THIS REPORT 02 About Us 04 Financial Highlights 05 Industry Highlights 06 Philippine Highlights 08 Message to Shareholders 14 Q&A with the Chief Operating Officer 16 Operational Highlights 22 Subsidiaries 26 Corporate Social Responsibility 30 Board of Directors 34 Management Team 37 Corporate Governance 41 Statement of Management’s Responsibility for Financial Statements 42 Report of Independent Auditors 46 Consolidated Financial Statements 51 Management’s Discussion and Analysis of Financial Conditions 55 Our Products 56 Corporate Offices 2016 ANNUAL REPORT “Sulong” is a Filipino term that serves as a rallying cry: “Charge! Move! Onward!” That is also the team’s call to ABOUT action as we unite and work together towards our goal THE COVER to become a bigger player in the industry. In the midst of changes in the political and economic landscape, to be able to quickly act on opportunities is essential. Sulong Phoenix! We’re ready to soar. SULONG PHOENIX VISION To be an indispensable partner in the journey of everyone ABOUT whose life we touch US MISSION • We deliver the best value in products and services to our business partners • We conduct our business with respect, integrity, and excellence • We provide maximum returns to our shareholders and investors • We create opportunities for learning, growth, and recognition to the Phoenix Family • We build programs to nurture the environment and welfare of the communities we serve 02 | 2016 ANNUAL REPORT PHOENIX PETROLEUM PHILIPPINES, INC. Phoenix Petroleum Philippines, Inc. (PNX) is the leading independent and fastest-growing oil company in the Philippines. -

World Ex U.S. Value Portfolio

World Ex U.S. Value Portfolio As of July 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. This fund operates as a fund-of-funds and generally allocates its assets among other mutual funds, but has the ability to invest in securities and derivatives directly. The holdings listed below contain both the investment holdings of the corresponding underlying funds as well as any direct investments of the fund. -

(SEC Form 20-IS) of Our Company for Your Consideration and Approval

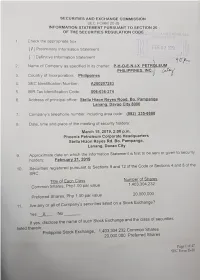

26 February 2019 Securities & Exchange Commission Secretariat Building, PICC Complex Roxas Blvd, Metro Manila Philippine Stock Exchange Disclosure Department 3/F PSE Plaza, Ayala Triangle Plaza Makati City, Metro Manila Philippine Dealing & Exchange Corporation 37th Floor, Tower 1, The Enterprise Center 6766 Ayala Ave. corner Paseo de Roxas Makati, 1226 Metro Manila, Philippines Attention: Hon. Vicente Graciano P. Felizmenio, Jr. Director, Market and Securities Regulation Department Securities & Exchange Commission Ms. Janet Encarnacion Head - Disclosure Department Philippine Stock Exchange Atty. Joseph B. Evangelista Head - Issuer Compliance and Disclosure Department (ICDD) Ladies and Gentlemen: We are herewith submitting the attached Definitive Information Statement (SEC Form 20-IS) of our company for your consideration and approval. Thank you and warm regards. Very truly yours, Atty. Socorro Ermac Cabreros Corporate Secretary SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: [ ] Preliminary Information Statement [ / ] Definitive Information Statement 2. Name of Company as specified in its charter: P-H-O-E-N-I-X PETROLEUM PHILIPPINES, INC. 3. Country of Incorporation: Philippines 4. SEC Identification Number:A200207283 5. BIR Tax Identification Code:006-036-274 6. Address of principal office: Stella Hizon Reyes Road, Bo. Pampanga Lanang, Davao City 8000 7. Company’s telephone number, including area code: (082) 235-8888 8. Date, time and place of the meeting of security holders: March 15, 2019, 2:00 p.m. Phoenix Petroleum Corporate Headquarters Stella Hizon Reyes Rd. Bo. Pampanga, Lanang, Davao City 9. Approximate date on which the Information Statement is first to be sent or given to security holders: February 21, 2019 10. -

Page 2 of 47 SEC Form IS-20

Page 2 of 47 SEC Form IS-20 Page 3 of 47 SEC Form IS-20 PART I. INFORMATION REQUIRED IN INFORMATION STATEMENT A. GENERAL INFORMATION Item 1. Date, time and place of meeting of security holders (a) Date : March 15, 2019 Time : 2:00 p.m. Place : Phoenix Petroleum Corporate Headquarters Stella Hizon Reyes Rd. Davao City Mailing P-H-O-E-N-I-X PETROLEUM PHILIPPINES, INC. Address: Office of the Corporate Secretary Phoenix Petroleum Corporate Headquarters Stella Hizon Reyes Road, Bo. Pampanga Lanang, Davao City 8000 (b) Approximate date on which the Information Statement is first to be sent or given to security holders: February 21, 2019. Item 2. Dissenter’s Right of Appraisal Procedure for the exercise of Appraisal Right Pursuant to Section 81 of the Corporation Code of the Philippines, a stockholder has the right to dissent and demand payment of the fair value of his shares in case of any amendment to the articles of incorporation that, (1) in case of amendment to the articles of incorporation, has the effect of changing or restricting the rights of any stockholder or class of shares, or of authorizing preferences in any respect superior to those of outstanding shares of any class, or of extending or shortening the term of corporate existence; (2) in case of lease, exchange, transfer, mortgage, pledge or other disposition of all or substantially all of the corporate property and assets as provided in the Corporation Code, and (3) in case of merger or consolidation. Such appraisal right may be exercised by any stockholder who shall have voted against the proposed corporate action by making a written demand on the Company within thirty (30) days after the date on which the vote was taken for payment of the fair value of his shares. -

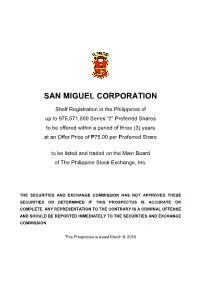

Shelf Registration in the Philippines Of

SAN MIGUEL CORPORATION Shelf Registration in the Philippines of up to 975,571,800 Series “2” Preferred Shares to be offered within a period of three (3) years at an Offer Price of ₱75.00 per Preferred Share to be listed and traded on the Main Board of The Philippine Stock Exchange, Inc. THE SECURITIES AND EXCHANGE COMMISSION HAS NOT APPROVED THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS ACCURATE OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE AND SHOULD BE REPORTED IMMEDIATELY TO THE SECURITIES AND EXCHANGE COMMISSION. This Prospectus is dated March 9, 2016 SAN MIGUEL CORPORATION 40 San Miguel Avenue Mandaluyong City 1550 Philippines Telephone number (632) 632-3000 http://www.sanmiguel.com.ph This Prospectus relates to the shelf registration and continuous offer by way of sale in the Philippines (the “Offer”) of up to 975,571,800 cumulative, non-voting, non-participating, non-convertible Peso-denominated Series “2” Preferred Shares (the “Offer Shares”) of San Miguel Corporation (“SMC”, the “Company”, the “Parent Company” or the “Issuer”), a corporation duly organized and existing under Philippine law, subject to the registration requirements of the Securities and Exchange Commission of the Philippines (the “SEC”). The Offer Shares will be sold at a subscription price of ₱75.00 per share (the “Offer Price”), or for a total offer size of up to Seventy-Three Billion One Hundred Sixty-Seven Million Eight Hundred Eighty-Five Thousand Pesos (₱73,167,885,000.00). The Offer Shares shall be issued in tranches within a period of three (3) years (the “Shelf Period”), at an offer price of ₱75.00 per share. -

Preliminary Prospectus Dated August 22, 2016

BEEN YET Subject to Completion PRELIMINARY PROSPECTUS Petron Corporation (a company incorporated under the laws of the Republic of the Philippines) SHALL NOT CONSTITUTE AN OFFER TO SELL OR A Shelf Registration in the Philippines of Fixed Rate Bonds in the aggregate principal amount of up to P40,000,000,000 to be offered within a period of three (3) years at an Issue Price of 100% of Face Value to be listed and traded through The Philippine Dealing & Exchange Corp. (AND THE RELEVANT OFFER SUPPLEMENT) THE SECURITIES AND EXCHANGE COMMISSION HAS NOT APPROVED THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS ACCURATE OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE AND SHOULD BE REPORTED IMMEDIATELY TO THE SECURITIES AND EXCHANGE COMMISSION. F AN OFFER TOBUY. ANOFFER F The date of this Preliminary Prospectus is August 22, 2016. EFFECTIVE. THESE SECURITIES MAY NOT BE SOLD NOR OFFERS TO BUY THE SAME BE ACCEPTED PRIOR TO THE TIME THE REGISTRATION i A REGISTRATION STATEMENT RELATING TO THESE SECURITIES HAS BEEN FILED WITH THE SECURITIES AND EXCHANGE COMMISSION BUT HAS NOT DECLARED STATEMENT BECOMES EFFECTIVE. THIS O SOLICITATION PROSPECTUS Petron Corporation SMC Head Office Complex 40 San Miguel Avenue Mandaluyong City, Philippines Telephone number: (632) 886 3888 Corporate website: www.petron.com This prospectus (“this Prospectus” and, as the context may require, the term includes the relevant Offer Supplement) relates to the shelf registration and offer by Petron Corporation (“Petron”, the “Company” or the “Issuer”), a corporation duly organized and existing under Philippine law, through a sale in the Philippines of fixed rate bonds (the “Bonds”) in the aggregate principal amount of up to P40,000,000,000. -

Download (PCC-Issues-Paper-2021-05

PCC Issues Paper No. 05 Series of 2021 PAPER ISSUES Market Study on the Refined Petroleum Industry Peter L. U, Ph.D. Romeo Balanquit, Ph.D. Gilbert Garchitorena Allan Francisco Jesalva Perry Fernand Reyes Market Study on the Refined Petroleum Industry The Center for Research and Communication Foundation, Inc. Research Team Principal/Lead Researcher: Peter L. U, Ph.D. Members: Romeo Balanquit, Ph.D. | Gilbert Garchitorena Allan Francisco Jesalva | Perry Fernand Reyes Published by: Philippine Competition Commission 25/F Vertis North Corporate Center 1 North Avenue, Quezon City 1105 PCC Issues Papers aim to examine the structure, conduct, and performance of select industries to better inform and guide PCC’s advocacy and enforcement initiatives. The opinions, findings, conclusions, and recommendations expressed in these studies are those of the author(s) and do not necessarily reflect the views of the Commission. This work is protected by copyright and should be cited accordingly. The views reflected in this paper shall not in any way restrict or confine the ability of the PCC to carry out its duties and functions, as set out in the Philippine Competition Act. PCC reserves the right, when examining any alleged anti-competitive activity that may come to its attention, to carry out its own market definition exercise and/or competition assessment, in a manner which may deviate or differ from the views expressed in this paper. [email protected] | www.facebook.com/CompetitionPH | www.twitter.com/CompetitionPH | www.phcc.gov.ph EXECUTIVE SUMMARY The pricing of retail petroleum remains a prominent public issue. Price adjustments evolved to a weekly practice wherein firms announce on Mondays the price adjustments that take effect the next day.