Merger Tracker Become Challenging in Fourth Quarter

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Private Equity Holdings Disclosure 06-30-2019

The Regents of the University of California Private Equity Investments as of June 30, 2019 (1) Capital Paid-in Capital Current Market Capital Distributed Total Value Total Value Description Vintage Year (2) Net IRR (3) Committed (A) Value (B) (C) (B+C) Multiple (B+C)/A) Brentwood Associates Private Equity II 1979 3,000,000 3,000,000 - 4,253,768 4,253,768 1.42 5.5% Interwest Partners I 1979 3,000,000 3,000,000 - 6,681,033 6,681,033 2.23 18.6% Alta Co Partners 1980 3,000,000 3,000,000 - 6,655,008 6,655,008 2.22 13.6% Golder, Thoma, Cressey & Rauner Fund 1980 5,000,000 5,000,000 - 59,348,988 59,348,988 11.87 30.5% KPCB Private Equity (Legacy Funds) (4) Multiple 142,535,631 143,035,469 3,955,643 1,138,738,611 1,142,694,253 7.99 39.4% WCAS Capital Partners II 1980 4,000,000 4,000,000 - 8,669,738 8,669,738 2.17 14.0% Brentwood Associates Private Equity III 1981 3,000,000 3,000,000 - 2,943,142 2,943,142 0.98 -0.2% Mayfield IV 1981 5,000,000 5,000,000 - 13,157,658 13,157,658 2.63 26.0% Sequoia Private Equity (Legacy Funds) (4) Multiple 293,200,000 352,355,566 167,545,013 1,031,217,733 1,198,762,746 3.40 30.8% Alta II 1982 3,000,000 3,000,000 - 5,299,578 5,299,578 1.77 7.0% Interwest Partners II 1982 4,008,769 4,008,769 - 6,972,484 6,972,484 1.74 8.4% T V I Fund II 1982 4,000,000 4,000,000 - 6,744,334 6,744,334 1.69 9.3% Brentwood Associates Private Equity IV 1983 5,000,000 5,000,000 - 10,863,119 10,863,119 2.17 10.9% WCAS Capital Partners III 1983 5,000,000 5,000,000 - 9,066,954 9,066,954 1.81 8.5% Golder, Thoma, Cressey & Rauner Fund II 1984 -

2020 Annual Report

MMBB Financial Services 2020 Annual Report Answering the Call to Adapt, Evolve, Respond “ God has always called all human beings to share in the divine mission in the world—and God still does. God calls women and men to ordained ministry in the church, and God calls other followers of Christ to special ministries both in the church and outside it.” Ben Campbell Johnson1 Table of Contents Report of the Chief Executive Officer .........1 Benefit Plans ..................................................... 6 2020 Financials and Audit Report ............... 9 Administration ................................................38 Officers, Board of Managers and Investment Committee Members ......... 39 Asset Managers, Investment Custodian and Counsel ................................................ 40 1 Hearing God’s Call: Ways of Discernment for Laity and Clergy, Wm. B. Eerdmans Publishing Co., 2002 Report of the Chief Executive Officer Some describe a calling as a yearning or an intense through retirement. This vision enables our members to pull that is heard over and over. Others say it stirs and focus on their faith rather than their finances. nourishes the soul and must be satisfied for a person to With this in mind, MMBB has answered the call to adapt, feel complete and purposeful. Still others describe an urge evolve and respond to support ministers, churches and toward a particular way of life or a deep conviction about faith-based organizations in their calling through times of a path one is meant to take. But most people agree that a prosperity and times of crisis. We have been a trusted partner calling is much more than a casual pursuit. to our constituents through tremendous financial and When God calls a person into ordained ministry, they feel societal upheaval, such as the Depression, the Civil Rights compelled to heed the call. -

June 2011 Investment Return

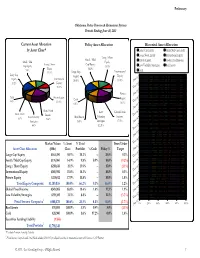

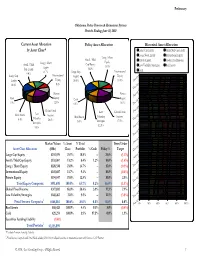

Current Asset Allocation by Asset Class* Small / Mid Oklahoma Police Pension & Retirement System Lar Cap Equity ge Cap Equity 9.8% 20.2% Periods Ending June 30, 2011 Lon g / Short Cash Equity 1.6% 13.9% Policy Asset Allocation International Small / Mid Real Assets Equity Large Cap Cap Equity 10.3% Equity 3.9% Long / Short 20.0% 10.0% Private Equity Low Volatility Equity Preliminary Strategies Global Fixed 11.8% 15.0% 8.8% Income 19.4% Cash Large CapHistorical Equity Asset Allocation International Large CapAsset Equity Class Allocation $363,290 30.5% 20.2% -- 20.0% 0.2%0.0% Long/Short Equity Small / Mid Cap Equity $176,960 14.9% 9.8% 0.9% 10.0% Equity Private Equity 10.0% Long / Short Equity $250,616 21.1% 13.9% -- 15.0% Low Volatility Strategies Real Assets Cash Small/Mid Cap Equity International Equity $185,956 15.6%Market 10.3% Values -- 10.0% 0.3% 5.0% Jun-11 International Equity Private Equity $213,012 17.9% 11.8% -- 10.0% 1.8% Private Global Fixed Income (000s) Low Dec-10 Volatility Equity Real Assets % Asset Global Fixed Income $349,065 68.6% 19.4% 1.6% 17.5% 1.9% Strategies 10.0% Jun-10 Total Equity Composite $1,189,835 100.0% 66.2%Class 0.1% 65.0% Global Fixed Low Volatility Strategies $159,105 31.3% 8.8% -- 12.5% % Total 12.5% Dec-09 Portfolio % Cash Policy % Income 17.5% Jun-09 Real AssetsFixed Income Composite $70,893 100.0% 3.9% 0.4% 5.0% Dec-08 Cash $28,900 100.0% 1.6% 97.2% 0.0% 1.6% Jun-08 Securities Lending Liability Over/Under Dec-07 1 Jun-07 *Excludes Securities Lending Liability Target 1 $508,878 100.0% 28.3% 0.8% 30.0% Fixed Income Composite and Total Fund includes $709,117 for illiquid securities in terminated account with Overseas CAP Partner Dec-06 Total Portfolio Jun-06 (0.2%) 1 (1.1%) Dec-05 ($358) © 2011 Asset Consulting Group All Rights Reserved.$1,798,148 Jun-05 Dec-04 1.2% Jun-04 Dec-03 (3.7%) Jun-03 (1.7%) (1.1%) Dec-02 Jun-02 0% 20% 40% 60% 80% 100% s. -

The 2008 Preqin Private Equity Performance Monitor - Sample Pages

Sample Pages The 2008 Preqin Private Equity Performance Monitor - Sample Pages © 2008 Private Equity Intelligence Ltd 1 Sample Pages A Guide to the Performance of Private Equity Fund Managers © 2008 Private Equity Intelligence Ltd 2 Sample Pages Contents 1. Executive Summary 7 Fund of Funds 41 - DPI, RVPI and TVPI 2. Methodology 13 - Median Net IRR and Quartile Ranking - Fund Selection Performance 3. Overall Performance of Private Equity 19 - Relationship between Successor and Predecessor Fund - Fund Universe Mezzanine 45 - DPI, RVPI and TVPI - DPI, RVPI and TVPI - Median IRRs, Money Weighted IRRs and Pooled IRRs - Median Net IRR and Quartile Ranking - Performance by Geographic Region - Quartile Ranking by Fund Number - Relationship between Predecessor and Successor Fund Quartile Real Estate 49 - Experience Effect - DPI, RVPI and TVPI - Median Net IRR and Quartile Ranking 4. Performance by Fund Type 29 - Relationship between Successor and Predecessor Fund Buyout 31 Secondaries 53 - DPI, RVPI and TVPI - DPI, RVPI and TVPI - Median Net IRR and Quartile Ranking - Median IRR - Median, Weighted and Pooled IRRs Venture 55 - North American vs. European Buyout Funds - DPI, RVPI and TVPI - Large and Mega Buyout Funds - Median Net IRR and Quartile Ranking - Buyout Cash Flow Analysis - Median, Weighted and Pooled IRRs - Buyout Net Cash Flow by Vintage Year - Performance of Early Stage Funds - Performance at Different Points in Time - Performance of Industry Focused Funds - Relationship between Successor and Predecessor Fund Quartile - Venture Cash Flow Analysis Distressed Debt & Special Situations 39 - Venture Cash Flow by Vintage - DPI, RVPI and TVPI - Performance at Different Points in Time - Median IRR - Relationship between Successor and Predecessor Fund Quartile © 2008 Private Equity Intelligence Ltd 3 Sample Pages 5. -

June 2010 Investment Return

Preliminary Oklahoma Police Pension & Retirement System Periods Ending June 30, 2010 Current Asset Allocation Policy Asset Allocation Historical Asset Allocation by Asset Class* Large Cap Equity Small/Mid Cap Equity Long/Short Equity International Equity Long / Short Small / Mid Private Equity Global Fixed Income Equity Small / Mid Long / Short Cap Equity 15.0% Low Volatility Strategies Real Assets Cap Equity Equity 10.0% Large Cap International Cash 8.4% 14.7% Large Cap International Equity Equity -10 Equity Equity 20.0% 10.0% Jun 9.4% 9 18.8% c-0 De Private Private -09 Jun Cash Equity Equity Cash 8 c-0 1.9% 12.5% 0.0% 10.0% De 8 n-0 Global Fixed Low Global Fixed Ju Low Real Assets Income 7 Real Assets Volatility Income c-0 4.4% Volatility De 20.4% 5.0% Strategies 17.5% Strategies 7 12.5% n-0 9.5% Ju 6 c-0 De 6 n-0 Market Values % Asset % Total Over/Under Ju 5 c-0 Asset Class Allocation (000s) Class Portfolio % Cash Policy % Target De Large Cap Equity $292,059 29.5% 18.8% -- 20.0% (1.2%) -05 Jun Small / Mid Cap Equity $131,067 13.2% 8.4% 1.2% 10.0% (1.6%) 4 c-0 Long / Short Equity $228,338 23.0% 14.7% -- 15.0% (0.3%) De -04 International Equity $145,687 14.7% 9.4% -- 10.0% (0.6%) Jun 3 Private Equity $194,547 19.6% 12.5% -- 10.0% 2.5% c-0 De Total Equity Composite $991,698 100.0% 63.7% 0.2% 65.0% (1.3%) -03 Global Fixed Income $317,692 68.0% 20.4% 3.9% 17.5% 2.9% Jun 2 c-0 Low Volatility Strategies $148,463 31.8% 9.5% -- 12.5% (3.0%) De 1 Fixed Income Composite -02 $466,864 100.0% 30.0% 0.8% 30.0% 0.0% Jun 0% 20% 40% 60% 80% 100% Real Assets $68,423 100.0% 4.4% 0.3% 5.0% (0.6%) Cash $29,274 100.0% 1.9% 97.5% 0.0% 1.9% Securities Lending Liability ($361) 1 Total Portfolio $1,555,899 *Excludes Securities Lending Liability 1 Fixed Income Composite and Total Fund includes $709,116 for illiquid securities in terminated account with Overseas CAP Partners. -

2020 Comprehensive Annual Financial Report Table of Contents

Comprehensive Annual Financial Report For the Fiscal Years Ended June 30, 2020 and 2019 Oklahoma Police Pension and Retirement System A Component Unit of the State of Oklahoma Oklahoma Police Pension and Retirement System MISSION To provide secure retirement benefits for members and their beneficiaries. VISION To be the best State Retirement System in Oklahoma through outstanding communication, education, customer service and financial stability. VALUES AND BEHAVIORS The Oklahoma Police Pension and Retirement System values its members, both active and retired, and the important contributions they make protecting the citizens of Oklahoma. Expect the OPPRS staff to exhibit integrity, ethical conduct, professionalism and a commitment to superior performance through teamwork, communication, mutual respect and cooperation driven to produce results. Effectively communicate new statute and rule changes to municipalities, members and staff. Use technology, such as the OPPRS website, to provide information in a timely manner. Use every opportunity to continually educate members, municipalities, the OPPRS board and staff. Utilize the most current technology to manage and operate the OPPRS. Provide every member a forum for timely and fair due process regarding applications and appeals. Strive to maintain financial stability by actively managing a broadly diversified investment portfolio designed to cover the current and future cost of benefits. GOALS Provide exceptional communication and education to our membership. Adopt new technology that can -

Nber Working Paper Series Borrow Cheap, Buy High?

NBER WORKING PAPER SERIES BORROW CHEAP, BUY HIGH? THE DETERMINANTS OF LEVERAGE AND PRICING IN BUYOUTS Ulf Axelson Tim Jenkinson Per Strömberg Michael S. Weisbach Working Paper 15952 http://www.nber.org/papers/w15952 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 April 2010 Earlier versions of this paper were circulated under the title “Leverage and pricing in buyouts: An empirical analysis.” We are very grateful to Steve Kaplan for sharing his data on 1980’s LBOs, and to Joakim Bång, Ji-Woong Chung, and Reimo Juks for excellent research assistance. We would also like to thank Viral Acharya, Malcolm Baker, Laura Bottazzi, Phil Canfield, Chris Collins, Marco DaRin, Francois Derrien, Chris James, Steve Kaplan, Steven Ongena, Morten Sorensen, David Sraer, Ayako Yasuda, as well as participants in numerous seminar presentations for valuable comments. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer- reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2010 by Ulf Axelson, Tim Jenkinson, Per Strömberg, and Michael S. Weisbach. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Borrow Cheap, Buy High? The Determinants of Leverage and Pricing in Buyouts Ulf Axelson, Tim Jenkinson, Per Strömberg, and Michael S. Weisbach NBER Working Paper No. -

Q3 in Review Frothy Markets Side-By-Side

www.buyoutsnews.com October 9, 2017 • Issue 21 BUYOUTS Vol. 30, No. 21, October 9, 2017 Building through the peak CONSISTENT Firms pursue buy-and-build EXECUTION TAKES strategies to navigate YOU HIGHER. Q3 in Review frothy markets Side-by-side. That’s where we start and where we remain throughout the lifecycle of a transaction. For more than two decades, our innovative financing solutions, reliable deal execution and sophisticated perspective on the middle market have made all the difference. 28 View our completed transactions at Antares.com Consistency by design. Q3 IN REVIEW Tax-reform plan raises questions about interest deductibility 6 GPs navigate high prices through relationships, buy-and-build 28 KKR’s sale of Capsugel headlines M&A exits in booming Q3 50 U.S. PE fundraising may reach post-crisis record 58 5 Questions: Sun Capital’s Edwards on storm-disaster planning 98 It’s budget planning season... luckily, help is on its way! Are your compensation practices competitive? Eliminate the guesswork by ordering the seventh edition of the 2017-2018 Featuring VCJ Texas and Buyouts Texas Holt-MM&K-Buyouts Insider PE/VC Compensation Report. December 4-6, 2017 • Hotel Van Zandt • Austin, TX The 2017-2018 edition is the largest, most comprehensive compensation study For the first time since its launch available, based on surveys from a large and diverse population of GPs in private 10 years ago, PartnerConnect equity and venture capital. The report is Southwest is moving from Dallas developed by the leading authorities in PE/ to Austin. This event will bring VC organizational management, employee you the same great content and remuneration, and PE/VC market intelligence. -

07.09 Asap Opprs

*Current Asset Allocation by Asset Class Lar Small / Mid Oklahoma Police Pension & Retirement System ge Cap Equity Cap Equity 19.4% 7.9% Long / Periods Ending July 31, 2009 Short Equity Cash 15.1% 1.5% Policy Asset Allocation International Equity Small / Mid Real Assets Large Cap 10.0% Cap Equity Equity 4.8% 20.0% 10.0% Long / Short Private Preliminary Low Equity Equity Volatility Global Fixed 15.0% Strategies 11.2% Income Cash Historical Asset Allocation 9.3% International Large Cap Equity 20.8% 0.0% Large CapAsset Equity Class Allocation $288,243 30.5% 19.4% -- 20.0% Equity Long/Short Equity Small / Mid Cap Equity $116,973 12.4% 7.9% 1.0% 10.0% 10.0% Private Equity Low Volatility Strategies Long / Short Equity $224,104 23.7% 15.1% -- 15.0% 0.1%Real Assets International Equity $149,020 15.8% 10.0% -- 10.0% 0.0% Cash Small/Mid Cap Equity Market Values 5.0% Private Equity Jul-09 International Equity Private Equity $166,283 17.6% 11.2% -- 10.0% 1.2% Low Volatility (000)'s 10.0% Apr-09 Global Fixed Income % Asset Strategies Jan-09 Real Assets Global Fixed Income 12.5% Oct-08 Total Equity Composite $944,623 100.0% 63.7%Class 0.1% 65.0% Global Fixed Low Volatility Strategies Jul-08 % Total Income Apr-08 Fund % Cash Policy % 17.5% Jan-08 Real AssetsFixed Income Composite $446,614 100.0% 30.1% 1.1% 30.0% Oct-07 Cash Jul-07 Apr-07 Securities Lending Liability Jan-07 $307,972 69.0% 20.8% 1.5% 17.5% 3.3% Over/Under Oct-06 $137,934 30.9% 9.3% -- 12.5% Jul-06 *Excludes Securities Lending Liability Target Apr-06 1 Total Fund includes $709,116 for illiquid securities in terminated account with Overseas CAP Partners. -

Global Liquidity and Settlement System (GLASS)

Global Liquidity And Settlement System (GLASS) GLASS White Paper | glassnet.io 03 Important Legal Notices and Disclaimers 04 Executive Summary 04 The Blockchain Revolution at Risk 04 The SharesPost Solution 06 Market Overview 06 The ICO and Token Markets are Growing Rapidly 06 Trading Platforms Struggle to Generate Liquidity 07 Regulators Force Token Platforms to Evolve 09 Competitive Landscape is Undeveloped 11 Sharespost Global Liquidity and Settlement System 11 Settlement Network 13 Liquidity Pooling 14 Technology Summary 15 Governance 15 SharesPost Marketplace 17 Token Uses And Utilities 17 Token Use: Global Liquidity and Settlement System 18 Token Use: SharesPost Marketplace 19 Technology Roadmap 20 The Company 20 The SharesPost Marketplace 21 SharesPost Management Team 21 SharesPost Investors 22 External Advisors For more information, email 23 Partners and Service Providers [email protected] 24 Sources glassnet.io Important Legal Notices And Disclaimers The purpose of this white paper is for information purposes only and may be subject to change or update without notice. This white paper is a preliminary concept release intended solely for review and discussion by the blockchain and cryptocurrency communities regarding the technological merits of the potential system outlined herein. This white paper may contain references to third party data and industry publications. As far as we are aware, the information reproduced in this white paper is accurate and the estimates and assumptions contained herein are reasonable. However, we offer no assurances as to the accuracy or completeness of this data. GLASS glassnet.io | 3 Executive Summary The Blockchain Revolution at Risk The emergence of cryptocurrencies and blockchain tokens promises to fundamentally remake the private capital market. -

Investor Update May 2017 Financial Information As of 31 March 2017 Unless Otherwise Noted

NB PRIVATE EQUITY PARTNERS: INVESTOR UPDATE MAY 2017 FINANCIAL INFORMATION AS OF 31 MARCH 2017 UNLESS OTHERWISE NOTED FOR PROFESSIONAL CLIENT USE ONLY NB PRIVATE EQUITY PARTNERS INVESTOR UPDATE OVERVIEW NBPE invests in private equity backed companies KEY HIGHLIGHTS INVESTMENT TYPE BY FAIR VALUE Listing Date: 2007 EQUITY INVESTMENTS Market Capitalisation (5/5/17): £511.3m 60% Net Asset Value (NAV): $766.3m NAV per Share: $15.70 (£12.11) NAV Total Return – 1 year / 3 year (USD): 16.0% / 34.1% Share Price Total Return – 1 year / 3 year (GBP): 50.9% / 88.6% INCOME INVESTMENTS 2017 Avg. Daily Trading Volume: ~76k shares per day 20% Current share price (5/5/17): £10.48 (~14% discount) Dividend Yield (on Share Price): 3.8% FUND INVESTMENTS 20% Note: NBPE data as of 31 March 2017; GBP share price returns converted at daily GBP/USD close FX rates. GBP/USD 5/5/17 rate of $1.296. Numbers may not sum due to rounding. All performance figures assume re-investment of dividends at NAV or closing share price on the ex-dividend date and reflect cumulative returns over the relevant time periods shown and are not annualised returns; share price return data based on the London Stock Exchange. Average trading volume represents daily average across London Stock Exchange, Euronext Amsterdam and over-the-counter trading platforms. FOR PROFESSIONAL CLIENT USE ONLY 2 NB PRIVATE EQUITY PARTNERS INVESTOR UPDATE VOTING RIGHTS AND PREMIUM LISTING The Company’s Class A Shares have been admitted to trading on the premium segment of the London Stock Exchange Recent NBPE -

Private Equity Deskbook Mid-Year Update 2008

Private Equity Deskbook Mid-Year Update 2008 2008 © Probitas Partners Contents Introduction ......................................................................... 1 The Perfect Storm: The Credit Cycle & Private Equity .................................................................... 2 The Market for Buying Companies .................................. 2 Defaults & Bankruptcies ..................................................... 4 Fundraising & Distressed Investing ............................... 9 “The Best & the Brightest” .............................................. 11 The Venture Capital Market: No Exit .......................... 13 The Secondary Market ..................................................... 14 Conclusion ........................................................................... 18 Funds in or Coming to Market ....................................... 20 Introduction Probitas Partners is a leading independent knowledge, innovation and solutions provider to private markets clients. It has three integrated global practices that include placement of alternative investment products, portfolio management and liquidity management. These services are offered by a team of employee owners dedicated to leveraging the firm’s vast knowledge and technical resources to provide the best results for its clients. probity ¯¯˘ n. [from Latin probitas: good, proper, honest.] adherence to the highest principles, ideals and character. On an ongoing basis, Probitas Partners offers research and investment tools on the alternative investment