2L Schedule for Liability Reporting by Counterparty

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Directory of the Exchange®Atm Locations in Canada

DIRECTORY OF THE EXCHANGE®ATM LOCATIONS IN CANADA Winter 2012/13 YOUR ATM NETWORK TABLE OF CONTENTS Alberta ..................................................................................................... 1 British Columbia ...................................................................................... 2 Manitoba ............................................................................................... 14 New Brunswick ...................................................................................... 15 Newfoundland ....................................................................................... 18 Nova Scotia ........................................................................................... 21 Ontario .................................................................................................. 26 Prince Edward Island ............................................................................ 46 Quebec ................................................................................................. 47 Saskatchewan ....................................................................................... 66 DIRECTORY OF ATM LOCATIONS WINTER 2012/13 ALBERTA St. Albert Canadian Western Bank HSBC Bank Canada 300 – 700 St. Albert Road 400-665 St. Albert Road Calgary Canadian Western Bank Canadian Western Bank Canadian Western Bank #300, 5222 - 130 Ave. SE 606 4th Street SW 6606 MacLeod Trail SW HSBC Bank Canada HSBC Bank Canada HSBC Bank Canada 1217 Kensington Road NW 140, 815 – 17th Avenue SW 212-111 -

Directory of the Exchange®Atm Locations in Canada

DIRECTORY OF THE EXCHANGE®ATM LOCATIONS IN CANADA SUMMER 2006 YOUR ATM NETWORK TABLE OF CONTENTS Alberta ......................................................................................................1 British Columbia .......................................................................................2 Manitoba.................................................................................................14 New Brunswick.......................................................................................15 Newfoundland.........................................................................................18 Nova Scotia ............................................................................................20 Ontario....................................................................................................24 Prince Edward Island..............................................................................37 Quebec...................................................................................................39 Saskatchewan ........................................................................................57 DIRECTORY OF ATM LOCATIONS SUMMER 2006 ALBERTA Calgary Canadian Western Bank Citizens Bank of Canada HSBC Bank Canada 6606 MacLeod Trail SW 505 Third St. SW 407-8th Avenue S.W HSBC Bank Canada HSBC Bank Canada HSBC Bank Canada 212-111 3rd Ave E 95 Crowfoot Centre NW 347 - 58th Avenue SE National Bank of Canada 301 6th Avenue Sw Edmonton Canadian Western Bank HSBC Bank Canada HSBC Bank Canada 10303 -

Rule D4 Institution Numbers and Clearing Agency/Representative Arrangements

RULE D4 INSTITUTION NUMBERS AND CLEARING AGENCY/REPRESENTATIVE ARRANGEMENTS 2021CANADIAN PAYMENTS ASSOCIATION This Rule is copyrighted by the Canadian Payments Association. All rights reserved, including the right of reproduction in whole or in part, without express written permission by the Canadian Payments Association. Payments Canada is the operating brand name of the Canadian Payments Association (CPA). For legal purposes we continue to use “Canadian Payments Association” (or the Association) in these rules and in information related to rules, by-laws, and standards. RULE D4 – INSTITUTION NUMBERS AND CLEARING AGENCY/REPRESENTATIVE ARRANGEMENTS TABLE OF CONTENTS IMPLEMENTED ............................................................................................... 3 AMENDMENTS PRE-NOVEMBER 2003 ........................................................ 3 AMENDMENTS POST-NOVEMBER 2003 ..................................................... 3 INTRODUCTION ................................................................................................................. 6 ELIGIBILITY......................................................................................................................... 6 INSTITUTION NUMBERS ................................................................................................... 6 AMALGAMATION AND ACQUISITION .............................................................................. 6 NON-MEMBER ENTITIES .................................................................................................. -

CUSTODIAL AGREEMENTS As of April 30, 2019

Contact: Samantha Duffield Manager, Financial Compliance Phone: (416) 943-4662 Email: [email protected] CUSTODIAL AGREEMENTS The following is an alphabetical listing of prescribed Custodial Agreements executed as of April 30, 2019 between the Mutual Fund Dealers Association of Canada (MFDA), as bare trustee on behalf of Members, and mutual fund companies and other financial institutions, in accordance to the Member Regulation Notice MSN-0058, Acceptable Securities Locations. Please ensure that your assets held are included in the types of products listed by the entity. Fund Manager/ Financial Institution Type of Products 1 1832 Asset Management L.P. Mutual Fund / Hedge Fund / Labour Dynamic Mutual Fund Sponsored Fund / Deposit Accounts 2 Acker Finley Asset Management Inc. Mutual Fund 3 ACM Advisors Ltd. Mortgage Investment Fund 4 Acorn Global Investments Inc. Hedge Fund 5 ADS Canadian Bank GIC’s / High Interest Savings Account 6 AGF Investments Inc. Mutual Fund / Pooled Fund - Acuity Pooled Funds - AGF Pooled Funds - AGF family of mutual funds - AGF Elements family of mutual funds - Harmony family of mutual funds 7 AIP Asset Management Inc. Mutual Fund / Hedge Fund / Limited Partnership 8 AlphaNorth Asset Management Mutual Fund 9 Arrow Capital Management Inc. Investment Products 10 ATB Investment Management Inc. Mutual Fund 11 Aurion Capital Management Inc. Pooled Fund 12 Aventine Management Group Inc. Mutual Fund 13 B2B Bank GIC’s / High Interest Investment Accounts 14 Bank of Montreal GIC’s / High Interest Savings Accounts 15 Bank of Montreal Mortgage Corporation GIC’s 16 Bank of Nova Scotia (The) GIC’s 17 Barometer Capital Management Inc. Mutual Fund / Pooled Fund Doc 110950 Page 1 of 30 Fund Manager/ Financial Institution Type of Products 18 BC Advantage Fund Management Limited Venture Capital Corporation (VCC) Funds 19 B.E.S.T. -

CBA Contact List for Matters Involving Mortgage Discharges

CBA Contact List for Matters Involving Mortgage Discharges Bank Contact Information Bank of Montreal All inquiries: Contact the office that provided the payout documentation Escalation only: For all provinces except Quebec: [email protected] Quebec: [email protected] CIBC All inquiries: Collateral Charges (CIBC brand): Contact the local branch of account Conventional Charges (CIBC brand): Mortgage Call Centre: 1-888-264-6843 Simplii Financial Mortgages: Mortgage Call Centre: 1-888-866-0866 option 3 FirstLine Mortgages: Mortgage Call Centre: 1-800-970-0700 President’s Choice Financial Mortgages registered to CIBC or CIBC Mortgages Inc: 1-888-866-0866 option 3 Escalation only: [email protected] Secondary: Lou Silva Senior Manager, Retail Mortgage Operations [email protected] Canadian Western All inquiries: Bank Contact the office that provided the payout documentation Escalation only: Lucia Bermedo 780-423-9732 [email protected] Equitable Bank All inquiries: [email protected] Escalation only: Becky Leibold Director, Mortgage Services [email protected] Bank Contact Information Home Capital / Home All Inquiries: Trust / Home Bank Home Bank Service Centre 1-855-270-3630 Escalation Only: Miki Asano VP Customer Experience [email protected] HSBC All inquiries: Contact the office that provided the payout documentation Escalation only: HSBC Bank Canada; HSBC Trust Company (Canada): June Yao Assistant Manager, Unit Operations Secured Lending West (Maintenance/Security) [email protected] [email protected] Secondary: Ruby Callahan Senior Operations Specialist Secured Lending West [email protected] HSBC Finance Mortgages; Household Realty Corporation Limited Liliana Terriaca [email protected] Laurentian Bank of All inquiries: Canada LBC Branches: Mortgage Loans Administration Fax: 514-284-4659 or 1-877-355-0055 For B2B Bank Munish Bhalla Senior Manager, Administration Lending Operations LBC Tech 199 Bay St. -

As of 10/31/2020

Annual Report | October 31, 2020 Vanguard Total International Bond Index Fund See the inside front cover for important information about access to your fund’s annual and semiannual shareholder reports. Important information about access to shareholder reports Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of your fund’s annual and semiannual shareholder reports will no longer be sent to you by mail, unless you specifically request them. Instead, you will be notified by mail each time a report is posted on the website and will be provided with a link to access the report. If you have already elected to receive shareholder reports electronically, you will not be affected by this change and do not need to take any action. You may elect to receive shareholder reports and other communications from the fund electronically by contacting your financial intermediary (such as a broker-dealer or bank) or, if you invest directly with the fund, by calling Vanguard at one of the phone numbers on the back cover of this report or by logging on to vanguard.com. You may elect to receive paper copies of all future shareholder reports free of charge. If you invest through a financial intermediary, you can contact the intermediary to request that you continue to receive paper copies. If you invest directly with the fund, you can call Vanguard at one of the phone numbers on the back cover of this report or log on to vanguard.com. Your election to receive paper copies will apply to all the funds you hold through an intermediary or directly with Vanguard. -

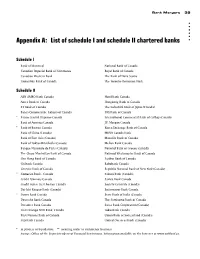

List of Schedule I and Schedule II Chartered Banks

Bank Mergers 39 Appendix A: List of schedule I and schedule II chartered banks Schedule I Bank of Montreal National Bank of Canada Canadian Imperial Bank of Commerce Royal Bank of Canada Canadian Western Bank The Bank of Nova Scotia Laurentian Bank of Canada The Toronto-Dominion Bank Schedule II ABN AMRO Bank Canada Hanil Bank Canada Amex Bank of Canada Hongkong Bank of Canada BT Bank of Canada The Industrial Bank of Japan (Canada) Banca Commerciale Italiana of Canada ING Bank of Canada * Banco Central Hispano-Canada International Commercial Bank of Cathay (Canada) Bank of America Canada J.P. Morgan Canada * Bank of Boston Canada Korea Exchange Bank of Canada Bank of China (Canada) MBNA Canada Bank Bank of East Asia (Canada) Manulife Bank of Canada Bank of Tokyo-Mitsubishi (Canada) Mellon Bank Canada Banque Nationale de Paris (Canada) National Bank of Greece (Canada) The Chase Manhattan Bank of Canada National Westminster Bank of Canada Cho Hung Bank of Canada Paribas Bank of Canada Citibank Canada Rabobank Canada Citizens Bank of Canada Republic National Bank of New York (Canada) ** Comerica Bank - Canada Sakura Bank (Canada) Crédit Lyonnais Canada Sanwa Bank Canada Credit Suisse First Boston Canada Société Générale (Canada) Dai-Ichi Kangyo Bank (Canada) Sottomayor Bank Canada * Daiwa Bank Canada State Bank of India (Canada) Deutsche Bank Canada The Sumitomo Bank of Canada Dresdner Bank Canada Swiss Bank Corporation (Canada) First Chicago NBD Bank, Canada Tokai Bank Canada First Nations Bank of Canada Union Bank of Switzerland (Canada) Fuji Bank Canada United Overseas Bank (Canada) * in process of liquidation; ** awaiting order to commence business Source: Office of the Superintendent of Financial Institutions. -

Custodial Agreement Listing As at August 31, 2016

Contact: Samantha Duffield Manager, Financial Compliance Phone: (416) 943-4662 Email: [email protected] CUSTODIAL AGREEMENTS The following is an alphabetical listing of prescribed Custodial Agreements executed as of August 31, 2016 between the Mutual Fund Dealers Association of Canada (MFDA), as bare trustee on behalf of Members, and mutual fund companies and other financial institutions, in accordance to the Member Regulation Notice MSN-0058, Acceptable Securities Locations. Please ensure that your assets held are included in the types of products listed by the entity. Fund Manager/ Financial Institution Type of Products 1 1832 Asset Management L.P. Mutual Fund / Hedge Fund / Labour - Dynamic Mutual Fund Sponsored Fund / Deposit Accounts 2 Acker Finley Asset Management Inc. Mutual Fund 3 ACM Advisors Ltd. Mortgage Investment Fund 4 Acorn Global Investments Inc. Hedge Fund 5 AGF Investments Inc. Mutual Fund / Pooled Fund - Acuity Pooled Funds - AGF Pooled Funds - AGF family of mutual funds - AGF Elements family of mutual funds - Harmony family of mutual funds 6 AlphaNorth Asset Management Mutual Fund 7 Arrow Capital Management Inc. Investment Products 8 Aston Hill Asset Management Inc. Mutual Fund / Hedge Fund / Labour Sponsored Fund / Structured Products 9 ATB Investment Management Inc. Mutual Fund 10 Aurion Capital Management Inc. Pooled Fund 11 Aventine Management Group Inc. Mutual Fund 12 B2B Bank GIC’s / High Interest Investment Accounts 13 Bank of Nova Scotia (The) GIC’s 14 Bank of Montreal GIC’s 15 Bank of Montreal Mortgage Corporation GIC’s 16 Barometer Capital Management Inc. Mutual Fund / Pooled Fund 17 BC Advantage Fund Management Limited Venture Capital Corporation (VCC) Funds Doc 110950 Page 1 of 24 Fund Manager/ Financial Institution Type of Products 18 B.E.S.T. -

1832 Asset Management LP Scotia Short Term Bond Fund

FUND FACTS 1832 Asset Management L.P. Scotia Short Term Bond Fund - Series K November 9, 2018 This document contains key information you should know about Scotia Short Term Bond Fund (the "Fund"). You can ®nd more detailed information in the Fund©s simpli®ed prospectus. Ask your representative for a copy, contact 1832 Asset Management L.P. at 1-800-268-9269, [email protected], or visit www.scotiafunds.com. Before you invest in any fund, consider how the fund would work with your other investments and your tolerance for risk. Effective November 16, 2018, the Fund's name will change to Scotia Private Short Term Bond Pool. Quick Facts Fund code(s): SWM6410 Fund Manager: 1832 Asset Management L.P. Date series started: July 12, 2016 Portfolio Manager: 1832 Asset Management L.P. Total value of Fund on September 30, 2018: $302,751,528 Minimum investment: $500 initial Management expense ratio (MER): 0.12% What does the Fund invest in? The Fund invests primarily in bonds and treasury bills issued or guaranteed by Canadian federal, provincial and municipal governments, any agency of such governments and Canadian corporations as well as money-market instruments of Canadian issuers. Up to 10% of the Fund©s assets may be invested in foreign securities. The charts below provide you with a snapshot of the Fund©s investments on September 30, 2018. The Fund's investments will change. Top 10 investments (September 30, 2018) Investment mix (September 30, 2018) 1. Canada Housing Trust No. 1 2.00% Dec 15, 2019 19.3% Sector Mix 14.5% 2. -

Bare Trustee Agreements Approved Fund Managers As of March 31, 2020 Fund Manager Region Type of Products Funds Covered by Agreement 1 1832 Asset Management L.P

Bare Trustee Agreements Approved Fund Managers as of March 31, 2020 Fund Manager Region Type of Products Funds covered by agreement 1 1832 Asset Management L.P. (Dynamic Funds) Canada Mutual Funds / Hedge Funds / LSF's Includes Deposit accounts 2 3IQ CORP. Canada Pooled Fund 3IQ Corp. 3 Aberdeen Global Services S.A. Overseas Mutual Fund Aberdeen Global II Funds Aberdeen Global Funds 4 Accilent Capital Management Inc. Canada Mutual Fund/Pooled Fund/Ltd. Partnership Capsure Hedged Oil and Gas Income & Growth Trust 5 Acker Finley Asset Management Inc. Canada Mutual Fund QSATM Funds 6 ACM Advisors Ltd. Canada Mortgage Investment Fund ACM Commercial Mortgage Fund 7 Addenda Capital Inc. Canada Pooled Fund Addenda Pooled Funds 8 ADS Canadian Bank Canada GIC's / Investment Savings Accounts 9 AGAWA Fund Management Inc. Canada Limited Partnership AGAWA Fund I Limited Partnership 10 AGF Investments Inc. Canada Mutual Fund / Pooled Fund Acuity Pooled funds Harmony family of mutual funds Acuity family of mutual funds AGF family of mutual funds AGF Pooled funds AGF Elements family of mutual funds 11 AHF Capital Partners Inc. Canada Mutual Fund/Hedge Fund/Pooled Fund AHF Credit Opportunities Fund - Series A, F and I 12 AIP Asset Management Canada Limited Partnership AIP Global Marco Fund LP 13 Aldergrove Credit Union Canada GIC's 14 Algonquin Capital Corporation Canada Limited Partnership 15 Alignvest Capital Management Inc. Canada Hedge Fund 16 Alignvest Investment Management Corporation Canada Pooled Fund 17 Alitis Investment Counsel Inc. Canada REIT Listing of Approved Fund Managers by Name Page 1 of 22 Fund Manager Region Type of Products Funds covered by agreement Alitis Private REIT Alitis Mortgage Plus Fund 18 AlphaNorth Asset Management Canada Mutual Fund 19 Altema Asset Management Inc. -

Mortgage Pre - Approval Requirements

MORTGAGE PRE - APPROVAL REQUIREMENTS In order to complete the Agreement of Purchase and Sale, all purchasers must provide a valid mortgage pre-approval. We ask that purchasers obtain a mortgage letter from one of the Schedule “I” Banks in Canada within 10 days from signing. A list of Schedule “I” Banks is attached. All mortgage pre-approvals must be on the financial institution’s letterhead, have the mortgage representative’s signature and contain the following information: Option 1 - 21% or 36% Deposit Pre-Approval (Preferred) 1. Building/Address: 11 Yorkville Condos / 11-25 Yorkville Avenue Suite No. (e.g. Suite 5502) Unit No. (e.g. Unit 02) Level no. (e.g. Level 55) 2. Purchaser(s) Name PLEASE NOTE: The name(s) on the Agreement of Purchase and Sale MUST be the same on the mortgage pre-approval.) 3. Total Purchase Price (e.g. $500,900) must include Parking and Locker if applicable 4. Mortgage Pre-Approval Amount (e.g. $395,711) PLEASE NOTE: Your mortgage pre-approval amount and your deposit MUST add up to the purchase price of the unit. e.g. $395,711 (Mortgage Amt) + $105,189 (total deposit) = $500,900 (Total Purchase Price) 5. Tentative Occupancy Date: September 2024. The pre-approval must be dated and current. 6. Contact name and phone number of Mortgage Representative at financial institution issuing the mortgage pre-approval. 7. If pre-approval is issued by a third-party mortgage lender, their license # (e.g. #M10000) must be stated in the letter. In addition, the lender institution (e.g. RBC) must be referenced. -

Strategic Analysis of a Retail Banking Firm

STRATEGIC ANALYSIS OF A RETAIL BANKING FIRM Tracy Tong Bachelor of Commerce, University of British Columbia, 1997 PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION In the Faculty of Business Administration O Tracy Tong 2005 SIMON FRASER UNIVERSITY Summer 2005 All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission of the author. APPROVAL Name: Tracy Tong Degree: Master of Business Administration Title of Project: Strategic Analysis of a Retail Banking Firm Supervisory Committee: Senior Supervisor Ed Bukszar, Associate Professor Second Reader Neil Abramson, Associate Professor Date Approved: SIMON FRASER UNIVERSITY Partial Copyright Licence The author, whose copyright is declared on the title page of this work, has granted to Simon Fraser University the right to lend this thesis, project or extended essay to users of the Simon Fraser University Library, and to make partial or single copies only for such users or in response to a request from the library of any other university, or other educational institution, on its own behalf or for one of its users. The author has further granted permission to Simon Fraser University to keep or make a digital copy for use in its circulating collection. The author has further agreed that permission for multiple copying of this work for scholarly purposes may be granted by either the author or the Dean of Graduate Studies. It is understood that copying or publication of this work for financial gain shall not be allowed without the author's written permission.