2012 Miami-Dade

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Some Pre-Boom Developers of Dade County : Tequesta

Some Pre-Boom Developers of Dade County By ADAM G. ADAMS The great land boom in Florida was centered in 1925. Since that time much has been written about the more colorful participants in developments leading to the climax. John S. Collins, the Lummus brothers and Carl Fisher at Miami Beach and George E. Merrick at Coral Gables, have had much well deserved attention. Many others whose names were household words before and during the boom are now all but forgotten. This is an effort, necessarily limited, to give a brief description of the times and to recall the names of a few of those less prominent, withal important develop- ers of Dade County. It seems strange now that South Florida was so long in being discovered. The great migration westward which went on for most of the 19th Century in the United States had done little to change the Southeast. The cities along the coast, Charleston, Savannah, Jacksonville, Pensacola, Mobile and New Orleans were very old communities. They had been settled for a hundred years or more. These old communities were still struggling to overcome the domination of an economy controlled by the North. By the turn of the century Progressives were beginning to be heard, those who were rebelling against the alleged strangle hold the Corporations had on the People. This struggle was vehement in Florida, including Dade County. Florida had almost been forgotten since the Seminole Wars. There were no roads penetrating the 350 miles to Miami. All traffic was through Jacksonville, by rail or water. There resided the big merchants, the promi- nent lawyers and the ruling politicians. -

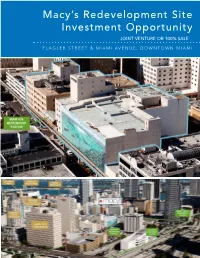

Macy's Redevelopment Site Investment Opportunity

Macy’s Redevelopment Site Investment Opportunity JOINT VENTURE OR 100% SALE FLAGLER STREET & MIAMI AVENUE, DOWNTOWN MIAMI CLAUDE PEPPER FEDERAL BUILDING TABLE OF CONTENTS EXECUTIVE SUMMARY 3 PROPERTY DESCRIPTION 13 CENTRAL BUSINESS DISTRICT OVERVIEW 24 MARKET OVERVIEW 42 ZONING AND DEVELOPMENT 57 DEVELOPMENT SCENARIO 64 FINANCIAL OVERVIEW 68 LEASE ABSTRACT 71 FOR MORE INFORMATION, CONTACT: PRIMARY CONTACT: ADDITIONAL CONTACT: JOHN F. BELL MARIANO PEREZ Managing Director Senior Associate [email protected] [email protected] Direct: 305.808.7820 Direct: 305.808.7314 Cell: 305.798.7438 Cell: 305.542.2700 100 SE 2ND STREET, SUITE 3100 MIAMI, FLORIDA 33131 305.961.2223 www.transwestern.com/miami NO WARRANTY OR REPRESENTATION, EXPRESS OR IMPLIED, IS MADE AS TO THE ACCURACY OF THE INFORMATION CONTAINED HEREIN, AND SAME IS SUBMITTED SUBJECT TO OMISSIONS, CHANGE OF PRICE, RENTAL OR OTHER CONDITION, WITHOUT NOTICE, AND TO ANY LISTING CONDITIONS, IMPOSED BY THE OWNER. EXECUTIVE SUMMARY MACY’S SITE MIAMI, FLORIDA EXECUTIVE SUMMARY Downtown Miami CBD Redevelopment Opportunity - JV or 100% Sale Residential/Office/Hotel /Retail Development Allowed POTENTIAL FOR UNIT SALES IN EXCESS OF $985 MILLION The Macy’s Site represents 1.79 acres of prime development MACY’S PROJECT land situated on two parcels located at the Main and Main Price Unpriced center of Downtown Miami, the intersection of Flagler Street 22 E. Flagler St. 332,920 SF and Miami Avenue. Macy’s currently has a store on the site, Size encompassing 522,965 square feet of commercial space at 8 W. Flagler St. 189,945 SF 8 West Flagler Street (“West Building”) and 22 East Flagler Total Project 522,865 SF Street (“Store Building”) that are collectively referred to as the 22 E. -

The Serpent's Tale V36 Issue 2

NEWS (2- 3) Heroes Come and Go, • New Year, New Laws by Ismael Contreras • Anti-Semitism in the Big Apple by Dylan Pren- tice but Legends are Forever • Two Years After Calamity: the Aftermath of By Ismael Contreras and Dylan Prentice Parkland by Tania Rojas • 2020 Catastrophes by Andrea Rodriguez and On Sunday, January 26, 2020, at 9:45 a.m. (12:45 p.m. EST), Adrian Perez a helicopter crashed into a hillside in Calabasas, California, killing all • Coronavirus in the U.S. by Steven Ponce De of its 9 passengers, including 41-year-old retired NBA player Kobe Leon and Milton Ramos Bryant and his 13 year-old daughter, Gianna. • Enterprising Educators by Sam Quincoses • A Crisis Down Under by Adriel Basulto Bryant, his daughter, and the other passengers were headed to a basketball game that Gianna was to play in and Kobe was to coach. Kobe had often taken helicopters to skip LA traffic, and this flight was SPORTS (4-5) not a particularly special one. That morning, however, there was thick, • SMSH Basketball: Bringing It Home by Ismael low-lying fog obstructing visibility. Despite regular procedures consid- Contreras and Alana Demler ering the conditions, for unknown reasons, the helicopter began an ex- • College Football Championship by Steven tremely rapid descent, crashing into the California hillside. Paramedics Ponce De Leon arrived at the scene and determined there were no survivors. The cause • Wrestling: Escaping From a Pretzel by Milton of the crash is still under investigation. Ramos • Super Bowl LIV by Ashley Fernandez Kobe Bryant is arguably one of the greatest basketball players • Dwayne Wayde’s Jersey Retirement by Milton to ever step on an NBA court. -

Downtown Kendall Charrette CHARRETTE MASTER PLAN REPORT EXECUTIVE SUMMARY

MIAMI-DADE COUNTY DEPARTMENT OF PLANNING AND ZONING • COMMUNITY PLANNING SECTION Downtown Kendall Charrette CHARRETTE MASTER PLAN REPORT EXECUTIVE SUMMARY Snapper Creek Expressway DOWNTOWN KENDALL CHARRETTE, MIAMI DADE COUNTY FLORIDA: In 1995, the Kendall Council of ChamberSOUTH originated the idea of working together with property owners, Dade County government and the neighboring community to build consensus on the future of the Dadeland-Datran area. Three years of Snapper Creek Canal SW 70 Ave meetings, phone calls and great effort from the Chamber staff accomplished the organization and fund-raising for an extensive week-long design “charrette”. Palmetto Expressway Palmetto SW 72 Ave 72 SW Held in the first week of June 1998, the Downtown SW 88 St Kendall Charrette was the combination of a South Dixie Highway town meeting with an energetic design studio. Two local town planning firms, Dover, Kohl & Partners, and Duany Plater-Zyberk and Co., were jointly commissioned with facilitating and Metrorail drawing the community’s ideas from the public design sessions. Participants from the community included property owners, neighbors, business people, developers, elected officials, county planning staff and others. Over one hundred Above: The Downtown Kendall Charrette Master Plan and fifty individuals participated. The charrette began on a Friday evening with presentations by ChamberSOUTH and the design team. The following morning, design began as 100 people from the community, armed with markers and pencils, gathered around eight tables, rolled up their sleeves, and drew their ideas on big maps of the Dadeland- Datran area. Later, a spokesperson from each table presented the main ideas from their table Above: Residential neighborhood on the north Above: Kendall Town Square at the intersection side of the canal of Kendall Boulevard and Dadeland Boulevard to the larger group. -

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna

Miami Office Space Can Be Found by Those Who Search February 7, 2017 By: Carla Vianna Businesses searching for space in Miami's urban core have more options than they might think. While vacancy rates are down across the board, significant chunks of space are available in several Class A buildings in downtown and the Brickell Avenue financial district. "There are more alternatives available for those companies that take the time to appropriately investigate the market," said Chris Lovell, a senior managing director with Savills Studley in Miami. Leasing space on an upper floor with a view may be difficult since only six buildings on Brickell have a full floor above the 20th story available for lease. For tenants that can live without the view, there is plenty of open space to choose from. Four downtown Class A buildings have at least 75,000 square feet of contiguous space available, one Class A building on Brickell has a 65,000- square-foot block — "and we don't have tenants of that size standing in line to the claim the space," Lovell said. Savills Studley has found many of the large available blocks are in older downtown buildings. "You're always going to have buildings that are going to have certain pockets available," said Tere Blanca, founder of Miami-based Blanca Commercial Real Estate Inc. She said the market is responding well to the new Miami Central project, which is under construction with 60 percent of its office component pre- leased. The mixed-use development will serve as Brightline's downtown train station and will add 286,000 square feet of office space in two buildings. -

Lobbying in Miami-Dade County

Miami-Dade County Board of County Commissioners Lobbying In Miami-Dade County 2013 Annual Report HARVEY RUVIN, Clerk of Circuit & County Courts and Ex-Officio Clerk to the Miami-Dade Board of County Commissioners Prepared by: Christopher Agrippa, Director Clerk of the Board Division Miami-Dade County Board of County Commissioners Lobbyist Registration SECTION I REGISTRATION BY LOBBYIST Printed on: 1/7/2014 Page 3 of 72 Miami-Dade County Board of County Commissioners Lobbyist Registration A ALFORD, JONATHAN 2440 RESEARCH BLVD ROCKVILLE MD 20850 ABOODY, JASON 9965 FEDERAL DRIVE OTSUKA AMERICA PHARMACEUTICALS COLORADO SPRINGS CO 80921 THE SPECTRANETICS CORPORATION ALLY, DEANNA 700 10TH AVENUE SOUTH SUITE 20 MINNEAPOLIS MI 55415 ABRAMS, MICHAEL 801 BRICKELL AVENUE STE 900 ZYGA TECHNOLOGY, INC. MIAMI FL 33131 BALLARD PARTNERS ALSCHULER, JR, JOHN H 99 HUDSON ST 3 FLOOR NEW YORK NY 10013 ACOSTA, EDWARD 100 DENNIS DRIVE BECKHAM BRAND LIMITED READING PA 19606 SURGICAL SPECIALITIES CORPORATION ALVAREZ, JORGE A 95 MERRICK WAY 7TH FLOOR CORAL GABLES FL 33134 ACOSTA, PABLO 131 MADEIRA AVE PH COMMUNITY CONSULTANTS, INC. CORAL GABLES FL 33134 CLEVER DEVICES INC AMSTER, MATTHEW G COMTECH ENGINEERING 200 S BISCAYNE BLVD Ste 850 MIAMI FL 33131 FLORIDA DEVELOPMENT GROUP, INC METRO GAS FL LLC NETZACH YISROEL TORAH CENTER, INC MIAMI DOWNTOWN DEVELOPMENT AUTHORITY SURGICAL PARK CENTER, LTD ADLER, BRIAN ANDARA, CHRISTOPHER D 1450 BRICKELL AVENUE SUITE 2300 11767 MEDICAL LLC MIAMI FL 33131 MIAMI FL 33156 19301 WEST DIXIE STORAGE, LLC ORBIS MEDICAL ANSALDOBREDA, INC ANDERSON, MELISSA P MIRON REALTY COMPANY 8555 NW 64TH STREET MODANI CAPITAL LLC DORAL FL 33166 PMG AVENTURA, LLC CROWN CASTLE USA SONNENKLAR LIMITED PARTNERSHIP THE ASSOC. -

US 1 from Kendall to I-95: Final Summary Report

STATE ROAD (SR) 5/US 1/DIXIE HIGHWAY FROM SR 94/SW 88 STREET/ KENDALL DRIVE TO SR 9/I-95 MIAMI-DADE COUNTY, FLORIDA FDOT FINANCIAL PROJECT ID: 434845-1-22-01 WWW.FDOTMIAMIDADE.COM/US1SOUTH March 2019 Final Summary Report ACKNOWLEDGMENTS Thank you to the many professionals and stakeholders who participated in and contributed to this study. From the communities along the corridor to the members of the Project Advisory Team, everyone played a crucial role in forming the results and conclusions contained in this study. 2 STATE ROAD (SR) 5/US 1/DIXIE HIGHWAY FROM SR 94/SW 88 STREET/KENDALL DRIVE TO SR 9/I-95 This report compiles the results of the State Road (SR) 5/US 1/ Dixie Highway from SR 94/SW 88 Street/Kendall Drive to SR 9/I-95 Corridor Study and includes: › Findings from the study › Recommendations for walking, bicycling, driving, and transit access needs along US 1 between Kendall Drive and I-95 › Next steps for implementing the recommendations This effort is the product of collaboration between the Florida Department of Transportation District Six and its regional and local partners. FDOT and its partners engaged the community at two critical stages of the study – during the identification of issues and during the development of recommendations. The community input helped inform the recommended strategies but the collaboration cannot stop here. Going from planning to implementation will take additional coordination and, in some instances, additional analysis. FDOT is able and ready to lead the effort but will continue seeking the support of community leaders, transportation and planning organizations, and the general public! To learn more, please read on and visit: www.fdotmiamidade.com/us1south WWW.FDOTMIAMIDADE.COM/US1SOUTH 3 CONTENTS 1. -

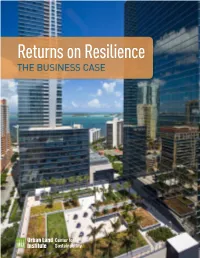

ULI: Returns on Resilience the Business Case

Returns on Resilience THE BUSINESS CASE Cover photo: A view of the green roof and main office tower at 1450 Brickell Avenue, with Biscayne Bay beyond. Robin Hill © 2015 Urban Land Institute 1025 Thomas Jefferson Street, NW Suite 500 West Washington, DC 20007-5201 All rights reserved. Reproduction or use of the whole or any part of the contents without written permission of the copyright holder is prohibited. Recommended bibliographic listing: Urban Land Institute: Returns on Resilience: The Business Case. ULI Center for Sustainability. Washington, D.C.: the Urban Land Institute, 2015. ISBN: 978-0-87420-370-7 Returns on Resilience THE BUSINESS CASE Project Director and Author Sarene Marshall Primary Author Kathleen McCormick This report was made possible through the generous support of The Kresge Foundation. Center for Sustainability About the Urban Land Institute The mission of the Urban Land Institute is to provide leadership in the responsible use of land and in creating and sustaining thriving communities worldwide. Established in 1936, the Institute today has more than 35,000 members worldwide representing the entire spectrum of the land use and development disciplines. ULI relies heavily on the experience of its members. It is through member involvement and information resources that ULI has been able to set standards of excellence in development practice. The Institute has long been recognized as one of the world’s most respected and widely quoted sources of objective information on urban planning, growth, and development. ULI SENIOR -

Miami Cbd Large Blocks of Office Space

RESEARCH MIAMI CBD AUGUST 2019 LARGE BLOCKS OF OFFICE SPACE 836 MACARTHUR CAUSEWAY 100,000+ SF Blocks 395 Southeast Financial Center Four Seasons Tower 200 S Biscayne Boulevard 1441 Brickell Avenue Ponte Gadea USA 9 Millennium Partners Management 1 1,225,000 RBA – 67.8% Leased 258,767 RBA – 98.1% Leased 133,120 SF Max Contig. 28,763 SF Max Contig. $53.25/RSF FS $60.00/RSF FS Citigroup Center 1221 Brickell 201 S Biscayne Boulevard 1221 Brickell Avenue Crocker Partners Rockpoint Group 2 809,594 RBA – 74.0% Leased 10 408,649 RBA – 86.1% Leased 95 127,634 SF Max Contig. 26,761 SF Max Contig. $48.00-$52.00/RSF FS $52.50/RSF FS Freedom PORT BLVD A1A Tower Wells Fargo Center 50,000 - 99,999 SF Blocks 333 SE 2nd Avenue AVE MetLife Real Estate Investments AVE 11 ND 752,845 RBA – 85.9% Leased ND SunTrust International Center 26,000 SF Max Contig. 1 SE 3rd Avenue BISCAYNE BLVD BISCAYNE $48.00/RSF FS N MIAMI AVE MIAMI N 2 NE NW 2 NW MiaMarina Pacific Coast Capital Partners MIAMI RIVER 3 440,299 RBA – 66.4% Leased 90,255 SF Max Contig. $38.00-$40.00/RSF FS 15,000 - 24,999 SF Blocks Brickell Office Plaza Brickell World Plaza Downtown 777 Brickell Avenue 600 Brickell Avenue 8 Padua Realty Company Elm Spring, Inc. 4 288,457 RBA – 74.8% Leased 12 631,866 RBA – 92.5% Leased 3 6 68,386 SF Max Contig. CLASS 24,138 SF Max Contig. -

1200 Brickell Avenue, Miami, Florida 33131

Jonathan C. Lay, CCIM MSIRE MSF T 305 668 0620 www.FairchildPartners.com 1200 Brickell Avenue, Miami, Florida 33131 Senior Advisor | Commercial Real Estate Specialist [email protected] Licensed Real Estate Brokers AVAILABLE FOR SALE VIA TEN-X INCOME PRODUCING OFFICE CONDOMINIUM PORTFOLIO 1200 Brickell is located in the heart of Miami’s Financial District, and offers a unique opportunity to invest in prime commercial real estate in a gloabl city. Situated in the corner of Brickell Avenue and Coral Way, just blocks from Brickell City Centre, this $1.05 billion mixed-used development heightens the area’s level of urban living and sophistication. PROPERTY HIGHLIGHTS DESCRIPTION • Common areas undergoing LED lighting retrofits LOCATION HIGHLIGHTS • 20- story, ± 231,501 SF • Upgraded fire panel • Located in Miami’s Financial District • Typical floor measures 11,730 SF • Direct access to I-95 • Parking ratio 2/1000 in adjacent parking garage AMENITIES • Within close proximity to Port Miami, American • Porte-cochere off of Brickell Avenue • Full service bank with ATM Airlines Arena, Downtown and South Beach • High-end finishes throughout the building • Morton’s Steakhouse • Closed proximity to Metromover station. • Lobby cafeteria BUILDING UPGRADES • 24/7 manned security & surveillance cameras • Renovated lobby and common areas • Remote access • New directory • On-site manager & building engineer • Upgraded elevator • Drop off lane on Brickell Avenue • Two new HVAC chillers SUITES #400 / #450 FLOOR PLAN SUITE SIZE (SF) OCCUPANCY 400 6,388 Vacant 425 2,432 Leased Month to Month 450 2,925 Leased Total 11,745 Brickell, one of Miami’s fastest-growing submarkets, ranks amongst the largest financial districts in the United States. -

FDOT Overpass Studies for Bird Rd

Non-Motorized Overpass at SR 5/US1 And SR 976/SW 40th Street (Bird Road) Executive Summary 6.0’ March 9, 2017 Prepared By: MARLIN Engineering Inc 1700 NW 66th Avenue, Ste. 106 Plantation, FL 33313 P: 305.477.7575 www.marlinengineering.com Non-Motorized Overpass at SR 5/US1 and SR 976/SW 40th Street (Bird Road) (FM No. 421053-3-12-01) EXECUTIVE SUMMARY Project Description: Concept and Feasibility Analysis for a non-motorized overpass for pedestrian and bicycles to support the Underline adjacent to US-1 at SW 40th Street (Bird Road). Purpose: The Department requested a conceptual and feasibility analysis to identify, evaluate, and recommend potential alignments for a non-motorized overpass. This conceptual analysis consisted of: Typical Section Analysis Horizontal and Vertical Geometric Analysis Traffic Control Analysis Background: The study was conducted at US 1 at 40th Street adjacent to the Underline, a proposed 10 mile signature linear park and urban trail. The Underline will serve as a gateway to the adjacent communities, by improving physical access from north to south running from underneath the Metrorail line and parallel to US1. Need: At this specific location, the traffic congestion is impacting the safety of pedestrians and bicyclists crossing SW 40th Street. Methodology: The feasibility study included the following tasks; Field review of existing conditions Analyze existing Right of Way Maps and Survey (topography) Obtain aerial images of the proposed study area Performed horizontal and vertical geometric analysis Coordination with local companies that manufacture pre-fabricated bridges to obtain preliminary cost estimates and engineering specifications Performed a conceptual Right of Way cost analysis of the adjacent properties within the study area Development of design criteria Development of concept alternatives including typical section, plan and profile. -

Download the Press Release

Florida Department of Transportation RON DESANTIS 1000 N.W. 111 Avenue KEVIN J. THIBAULT, P.E. GOVERNOR Miami, Florida 33172 SECRETARY For Immediate Release Contact: Tish Burgher April 22, 2020 (305) 470-5277 [email protected] Governor DeSantis Announces Upcoming Contract for Tamiami Trail Next Steps Phase 2 MIAMI, Fla. – Today, Governor Ron DeSantis announced the upcoming contract advertisement for the State Road (SR) 90/Tamiami Trail Next Steps Phase 2 Project. “I have worked diligently with the Florida Department of Transportation (FDOT) and the National Park Service (NPS) to accelerate this critical infrastructure project,” said Governor Ron DeSantis. “The Tamiami Trail project is a key component of the Comprehensive Everglades Restoration Plan. Elevating the trail will allow for an additional 75 to 80 billion gallons of water a year to flow south into the Everglades and Florida Bay.” In June 2019, Governor DeSantis announced that full funding had been secured to complete the project to elevate the Tamiami Trail. The U.S. Department of Transportation awarded an additional $60 million to the state’s $40 million to fully fund the project, which is critical to the Governor’s plan to preserve the environment. “This is another example of how Governor DeSantis has made preserving our environment and improving Florida’s infrastructure among his top priorities,” said Florida Department of Transportation Secretary Kevin J. Thibault, P.E. “This important project advances both and will also provide much needed jobs.” “Expediting Everglades restoration has been one of the hallmarks of the Governor’s environmental agenda,” said Florida Department of Environmental Protection Secretary Noah Valenstein.