York-Regional-Connectivity-Report.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Inverness Information Pack PDF 367Kb Download

Inverness General information Inverness, the capital of the Scottish Highlands acts as the hub for transport, administration and economic links in the north of Scotland. One of the fastest growing cities in Europe it is well provisioned with retail, healthcare and industrial sectors plus a booming tourist trade. Within minutes of leaving the city it is possible to be surrounded by wide-open spaces and stunning scenery – most notably Loch Ness, which at around 23 miles long holds more fresh water than all the lakes of England and Wales combined. The River Ness that flows out from Loch Ness winds through the heart of the city, providing tranquil riverside walks along its banks and Ness Islands. Transport links Inverness’s connections to the rest of the UK, Europe and beyond are strong, with daily flights from the airport to London Heathrow, London Gatwick, Manchester, Dublin and Amsterdam. Regular rail services serve Aberdeen, Edinburgh and Glasgow, plus the Caledonian Sleeper runs overnight to London Euston six times per week. By road it is 2.5 hours to Aberdeen, and access to the UK motorway network via Perth can be made in under 3 hours. Travel times to Highland mountain regions – and their winter ski resorts – are also brief with Aviemore and the Cairngorms under an hour to the south-east and Ben Nevis just 70 miles to the south-east. Ullapool and the West Coast can be reached in just over an hour. Inverness Airport The location of Inverness Airport 9 miles to the east of the city makes it ideally positioned for commuting in from the wider area. -

Local Authority & Airport List.Xlsx

Airport Consultative SASIG Authority Airport(s) of Interest Airport Link Airport Owner(s) and Shareholders Airport Operator C.E.O or M.D. Committee - YES/NO Majority owner: Regional & City Airports, part of Broadland District Council Norwich International Airport https://www.norwichairport.co.uk/ Norwich Airport Ltd Richard Pace, M.D. Yes the Rigby Group (80.1%). Norwich City Cncl and Norfolk Cty Cncl each own a minority interest. London Luton Airport Buckinghamshire County Council London Luton Airport http://www.london-luton.co.uk/ Luton Borough Council (100%). Operations Ltd. (Abertis Nick Barton, C.E.O. Yes 90% Aena 10%) Heathrow Airport Holdings Ltd (formerly BAA):- Ferrovial-25%; Qatar Holding-20%; Caisse de dépôt et placement du Québec-12.62%; Govt. of John Holland-Kaye, Heathrow Airport http://www.heathrow.com/ Singapore Investment Corporation-11.2%; Heathrow Airport Ltd Yes C.E.O. Alinda Capital Partners-11.18%; China Investment Corporation-10%; China Investment Corporation-10% Manchester Airports Group plc (M.A.G.):- Manchester City Council-35.5%; 9 Gtr Ken O'Toole, M.D. Cheshire East Council Manchester Airport http://www.manchesterairport.co.uk/ Manchester Airport plc Yes Manchester authorities-29%; IFM Investors- Manchester Airport 35.5% Cornwall Council Cornwall Airport Newquay http://www.newquaycornwallairport.com/ Cornwall Council (100%) Cornwall Airport Ltd Al Titterington, M.D. Yes Lands End Airport http://www.landsendairport.co.uk/ Isles of Scilly Steamship Company (100%) Lands End Airport Ltd Rob Goldsmith, CEO No http://www.scilly.gov.uk/environment- St Marys Airport, Isles of Scilly Duchy of Cornwall (100%) Theo Leisjer, C.E. -

AOA-Summer-2015.Pdf

THE AIRPORT OPERATORTHE OFFICIAL MAGAZINE OF THE AIRPORT OPERATORS ASSOCIATION DELIVERING A BETTER AIRPORT London Luton Features DELIVERING A A LEAP OF FAITH BETTER LUTON Charlotte Osborn, Chaplain, Chief Executive, Nick Barton Newcastle International SECURITY STANDARDS SMALLER AIRPORTS THE WAY AHEAD The House of Commons Transport Peter Drissell, Director of Select Committee reports SUMMER 2015 Aviation Security, CAA ED ANDERSON Introduction to the Airport Operator THE AIRPORT the proposal that APD be devolved in MARTIJN KOUDIJS PETE COLLINS PETE BARNFIELD MARK GILBERT Scotland. The Scottish Government AIRPORT NEEDS ENGINEERING SYSTEM DESIGN BAGGAGE IT OPERATOR THE OFFICIAL MAGAZINE OF THE AIRPORT OPERATORS ASSOCIATION has made it clear that it will seek GARY MCWILLIAM ALEC GILBERT COLIN MARNANE SERVICE DELIVERY CUSTOMER SOLUTIONS INSTALLATION to halve the APD rate in Scotland. AIRPORT OPERATORS ASSOCIATION Whilst we welcome reductions in the current eye watering levels of APD, Ed Anderson we absolutely insist on a reduction Chairman anywhere in the UK being matched by Darren Caplan the same reduction everywhere else. Chief Executive We will also be campaigning for the Tim Alderslade Government to incentivise the take up Public Affairs & PR Director of sustainable aviation fuels, which is Roger Koukkoullis an I welcome readers to this, an initiative being promoted by the Operations, Safety & Events Director the second of the new look Sustainable Aviation coalition. This Airport Operator magazine. I has the potential to contribute £480 Peter O’Broin C hope you approve of the new format. million to the UK economy by 2030. Policy Manager Sally Grimes Since the last edition we have of We will also be urging real reductions Events & Member Relations Executive course had a General Election. -

Travelling Made Easy…

Travelling made easy… Guidance and information on Travelling Safely in the UK and Scotland Follow government guidance on travelling safely in the UK and Scotland • Fly Safe with Loganair - Simple Steps to Healthy Flying • Dundee Airport - Information for Passengers • London City Airport - Safe, Careful, Speedy Journeys • Heathrow Airport - Fly Safe • Edinburgh Airport - Let's all Fly Safe • Glasgow Airport - Helping Each Other to Travel Safely • Aberdeen Airport - Helping Each Other to Travel Safely • Network Rail - Let's Travel Safely Fly into Dundee Dundee has a twice daily service from Dundee Airport to London City, which serves around 50 international destinations as well as a non-stop service between Dundee and Belfast City, serving 18 destinations including Amsterdam, with up to 12 flights per week and is a 5 minute drive from the city centre. A taxi rank is located just outside the airport. Discounted Flights to / from Dundee from London City or Belfast Loganair is offering up to 30% off flights to delegates travelling to/from Dundee from London City or Belfast for this conference. Please book at Loganair.co.uk before 16 April 2021, quoting promotional code 'SBNS2021' at the time of booking, for travel between 10 – 18 April 2021. Please click here to book. View airport and flight options here - http://www.hial.co.uk/dundee-airport/. To book visit Loganair International Flights are available to/from Scotland’s other major cities Fly into Aberdeen International Airport Connects with 50 international destinations and a 1 hour 30 minute drive from Dundee View airport and flight options here: https://www.aberdeenairport.com/ How to get to Dundee from the Airport TAXI/PRIVATE Discounted fares to/from Aberdeen International Airport, click here HIRE DIRECT BY TRAIN Aberdeen International Airport is about 11 kilometres from Aberdeen Railway Station, you can get there by hiring a taxi OR catching a bus in less than 30 minutes. -

Read Book Hampshire Airfields in the Second World

HAMPSHIRE AIRFIELDS IN THE SECOND WORLD WAR PDF, EPUB, EBOOK Robin J. Brooks | 192 pages | 31 Dec 1996 | COUNTRYSIDE BOOKS | 9781853064142 | English | Berks, United Kingdom Hampshire Airfields in the Second World War PDF Book Add to basket Buy Now Item Price. RAF Nefyn [40] [41]. Military attractions in Hampshire is part of Visit Hampshire the official tourism website. Count: Out of stock. Help Learn to edit Community portal Recent changes Upload file. Netherlands East Indies. Discover military attractions in Portsmouth. The runway is now buried under the M5 motorway. RAF Ulbster. RAF Broad Bay. Mexican P Thunderbolts of Squadron fly over the unforgiving terrain of central Luzon in July Archived from the original on 18 October More search options. This was a 'Q-t Built as satellite to RAF Milfield. Now Kibrit Air Base. RAF Hmawbi. The most obvious route, via the Azores, was not an option as Portugal remained staunchly neutral until August Search Military Attractions. Solent Sky Museum tells the fascinating story of this magical warplane. Use this tool to build your own journey or choose from an exciting range of specially selected tours. British Mauritius. RAF Maharajpur. RAF Half Die. RAF Fordoun. Now City of Derry Airport , Derry. RAF Jemappes. Underground bunker of contains the Group Operations Room from where the vital 11 Fighter Group was commanded during the Battle of Britain. RAF Dalby [27]. Part of the site is retained by the Ministry of Defence and leased to the Met Office. Also known as RAF Heathfield. RAF Calvo. The Aldershot Military Museum is situated on a active Army base giving visitors even more of an authentic experience. -

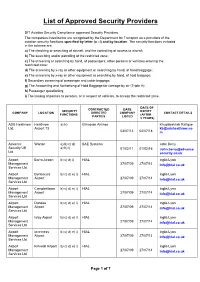

List of Approved Security Providers

List of Approved Security Providers DfT Aviation Security Compliance approved Security Providers The companies listed below are recognised by the Department for Transport as a providers of the aviation security functions specified by letter (a - i) and by location. The security functions included in the scheme are: a) The checking or searching of aircraft, and the controlling of access to aircraft; b) The searching and/or patrolling of the restricted zone ; c) The screening or searching by hand, of passengers, other persons or vehicles entering the restricted zone; d) The screening by x-ray or other equipment or searching by hand, of hand baggage; e) The screening by x-ray or other equipment or searching by hand, of hold baggage; f) Secondary screening of passenger and cabin baggage; g) The Accounting and Authorising of Hold Baggage for carriage by air (Triple A); h) Passenger questioning; i) The issuing of passes to persons, or in respect of vehicles, to access the restricted zone. DATE OF CONTRACTED DATE SECURITY EXPIRY COMPANY LOCATION DIRECTED COMPANY CONTACT DETAILS FUNCTIONS (AFTER PARTIES LISTED 5 YEARS) ADS Heathrow Heathrow a) h) Ethiopian Airlines Khudabakhsh Rafique Ltd. Airport T3 [email protected] 03/07/13 02/07/18 m Advance Warton a) b) c) d) BAE Systems John Berry Security UK e) h) i) 01/02/11 01/02/16 John.berry@advance Ltd security.co.uk Airport Barra Airport b) c) d) i) HIAL Inglis Lyon Management 27/07/09 27/07/14 [email protected] Services Ltd Airport Benbecula b) c) d) e) i) HIAL Inglis Lyon Management Airport 27/07/09 -

1 PE1804/P Petitioner Submission of 30 October 2020 In

PE1804/P Petitioner submission of 30 October 2020 In communications with HIAL managers the Benbecula Community Council (BCC) and Far North Aviation based at Wick Airport have found out that the HIAL Board have made their decision to downgrade the air traffic service provision at Benbecula and Wick airports without any supporting operational safety assessments or formal operational Safety Cases. Regardless that the Safety Cases have not yet been written, HIAL are now pressing on with implementing their decision, which have flight safety and flight regularity implications. Both Communities (Benbecula & Wick) have stakeholders, retired pilots/air traffic controllers who have the technical understanding to either comment on or review these Safety Cases when they written. Will HIAL permit any stakeholder involvement, the BCC suspect not. One of HIALs Managers has recently advised a stakeholder at Wick ‘the Flight Information Service unit would still allow most normal operations to take place'. This is a very glib statement for HIAL to make, considering that the operational Safety Cases have not been written. Using HIAL Islay airport as an example where Flight Information Service is the level of air traffic service provided, the following information is officially published under type of traffic permitted at the airport. (Instrument Flight Rules (IFR) /Visual Flight Rules (VFR)) The Aeronautical Information Publication (AIP) states VFR. Additionally, under Flight Procedures in the same document there is a warning: - Use of RNP (effectively IFR) procedures at this Aerodrome restricted to Highlands and Islands Airports Ltd - Approved Operators only. This raises the question how do IFR customers gain access to Benbecula and Wick if the airports are downgraded to the likes of Islay, and what is the HIAL the criteria required to become an HIAL 'Approved Operator'. -

EASA Aerodrome Certificates

UNITED KINGDOM A Member of the European Union CIVIL AVIATION AUTHORITY AERODROME CERTIFICATE ABERDEEN Certificate Reference: UK: EGPD - 001 Pursuant to Regulation (EC) No 216/2008 of the European Parliament and of the Council and the Commission Regulation (EU) No 139/2014 for the time being in force and subject to the conditions specified below, The United Kingdom Civil Aviation Authority hereby certifies that: Aberdeen International Airport Ltd Aberdeen Airport Dyce Aberdeen AB21 7DU is authorised to operate Aberdeen Aerodrome in accordance with the provisions of Regulation (EC) No 216/2008 and its Implementing Rules, the aerodrome certification basis, the terms of the certificate and the aerodrome manual. This certificate shall remain valid for an unlimited duration, unless it is surrendered or revoked. Date of original issue: 22 January 2015 Signed: …................................................................................................................... For the UK Civil Aviation Authority TERMS OF THE CERTIFICATE Certificate Reference UKEGPD – 001 Aerodrome Name and Aberdeen ICAO location indicator EGPD Conditions to operate Day/night, IFR, VFR Runway declared distances 16 - 1953m 2153m 1953m 1953m Runway designator, TORA 34 - 1953m 2091m 1953m 1953m TODA, ASDA, LDA, in metres 16 - 1953m 2153m 1953m 1953m Declared TORA commences at location of threshold lights. for each runway, including 34 - 1953m 2091m 1953m 1953m Declared TORA commences at location of intersection take-off if threshold lights. applicable 16 - 1829m 2029m -

EAST MIDLANDS AIRPORT Schedule of Charges and Terms & Conditions of Use

EAST MIDLANDS AIRPORT Schedule of Charges and Terms & Conditions of Use 1 April 2020 to 31 March 2021 magairports.com Part of MAG, East Midlands Airport (EMA) serves just over 4.5 million passengers and continues to be the largest dedicated cargo airport in the UK, carrying over 370,000 tonnes of freight in 2019. Our 24-hour operation enables EMA to be a key strategic gateway to the UK’s global supply chain; providing connections between UK PLC and Europe, and nearly 200 non-EU countries. It is the UK’s primary express cargo airport, hosting hub operations for DHL, FedEx, Royal Mail and UPS. Serving predominantly leisure destinations with airline partners including Jet2.com, Ryanair, TUI and more, the airport connects regional passengers to over 80 destinations across the UK, Europe and Africa. East Midlands Airport is part of MAG (which also operates London Stansted and Manchester Airports) – the UK’s largest airport group, serving a combined 62 million passengers and handling over 700,000 tonnes of cargo a year. We look forward to working with you over the coming year. East Midlands Airport 2 EAST MIDLANDS AIRPORT CHARGES FINANCIAL YEAR 2020/21 This document sets out East Midlands Airport Limited’s Terms and Conditions of Use (‘the Terms’) and the Charges that will apply from 1st April 2020 to 31st March 2021 (‘the Period’) unless the users are notified otherwise by East Midlands International Airport Limited (‘the Company’). The provisions in Sections 1 to 19 inclusive are strictly subject to the Terms contained in Section 20. Contents -

Body of Tex for Health Select Committee

meeting CROSS SERVICE AND EXTERNAL AFFAIRS SELECT COMMITTEE date 11 April 2005 agenda item number Report of the Chair of the Cross Service and External Affairs Select Committee Robin Hood Airport Study Group – Final Report Purpose of report 1 The purpose of this report is to inform the Cross Service and External Affairs Select Committee of the findings and recommendations, based on the evidence from this study, of the Committee’s Robin Hood Airport Study Group. 2 In July 2004 the Select Committee agreed to develop an evidence-based study of Robin Hood Airport – Doncaster Sheffield. The Committee decided to focus on the impact of the airport on Nottinghamshire as a whole, and to look particularly at the following issues in relation to the airport: • Highway and Transportation issues relating to the airport – including access and public transport issues. • Regeneration, economic development, job opportunities, and training issues • Impact on residents living near to the airport • Impact on Nottingham East Midlands Airport • Local investment, including impact on businesses and in-bound tourism 3 A Study Group was set up to develop and examine the findings from this study; the Members of the Study Group were Councillor Roy Barsley, Councillor Sue Bennett, Councillor Martin Brandon – Bravo OBE, Councillor Kenneth Bullivant, Councillor E Llewellyn – Jones, Councillor James Napier, and Councillor Sheila Place. Officer support was provided by Lynn Senior, Head of Scrutiny, and Trish Adams, Culture and Community Department. A number of other officers from the County Council’s Culture and Community, 1 Environment, and Education Departments, also greatly assisted the Select Committee by providing information and/or presenting information at meetings for this study. -

CH-CP-UK-Gabs Reno-Isle of Benbecula Scotland

CASE HISTORY Ref: UK / CH / CP — Rev:03, February 17 COASTAL EROSION PROTECTION AT AIRPORT ISLE OF BENBECULA, SCOTLAND, UK COASTAL PROTECTION Product: Polymeric Woven Gabions & Reno® Mattresses Problem Located in the Outer Hebrides, the Isle of Benbecula is among the most westerly places in the British Isles. It is exposed to the constant erosion and storm force winds of the Atlantic Ocean. This coastal erosion was encroaching on the South Western perimeter of Benbecula airport, a vital link with the mainland for those living on the Island. Client, Highlands and Islands Airports Ltd wanted to limit this erosion, thereby protecting their airport operations. Solution Project Consulting Engineers, Pick Everard designed a robust revetment that could withstand the exposure conditions. The 500m long revetment structure would stabilise and protect the sand dune system. 0.5m thick Reno Mattresses were selected to protect the sloped revetment and a low height crest wall constructed from gabions would retain the runway and control wave Location of the Isle of Benbecula overtopping. A similar solution had been adopted successfully at a MOD Firing Range elsewhere on Benbecula Due to the dynamic loading conditions and potential for the foundation conditions to change over the life of the structure, there was the possibility of differential settlement. Therefore, double twist woven steel wire mesh gabions were selected as their inherent flexibility would enable the structure to accommodate differential settlement without sustaining damage. Preserving the natural shoreline, the box gabions and heavy Reno Mattresses were filled with more than 8,000 tonnes of locally quarried stone. These heavy revetment mattresses, provided a natural looking solution, which would soon accrete sands and silts in which vegetation can establish. -

Kintyre Opportunities Breathe Business

A UNIQUE DISCOVER SECTOR ROOM TO YOUR LOCATION KINTYRE OPPORTUNITIES BREATHE BUSINESS KINTYRE A SPACE TO GROW ARGYLL AND BUTE, SCOTLAND Page 1 A UNIQUE DISCOVER SECTOR ROOM TO YOUR LOCATION KINTYRE OPPORTUNITIES BREATHE BUSINESS MACC BUSINESS CS WIND CAMPBELTOWN PORT AND PARK CAMPBELTOWN AIRPORT Kintyre has inherited a wealth of industrial infrastructure from past economic activity on the peninsula - a unique blend not found elsewhere in Scotland. Photo Credit: RCHAMS www.rchams.gov.uk MACHRIHANISH AIRBASE COMMUNITY COMPANY (MACC) BUSINESS PARK www.machrihanish.org/developments.php This former military airbase offers a wide range of flexible The site assets include: warehousing, work and office spaces and group on-site accommodation. ■ 1,000 acres of land and buildings available for development ■ 5 hectares of reinforced concrete hardstanding Currently around 80 tenants already located on site, over 200 people employed. ■ Workshops ranging from 52-1400 sqm ■ Office space ranging from 450-2788 sqm Page 2 A UNIQUE DISCOVER SECTOR ROOM TO YOUR LOCATION KINTYRE OPPORTUNITIES BREATHE BUSINESS MACC BUSINESS CS WIND CAMPBELTOWN PORT AND PARK CAMPBELTOWN AIRPORT CS WIND www.cswind.com CS Wind started operating from Machrihanish in 2017 supplying ■ A wealth of service businesses have developed in wind turbine towers to customers around the UK. At their peak the region to support this significant industry CSW employed over 150 skilled staff. ■ A range of flexible accommodation on the MACC business park from 1500 to 6000 sqm supports the business