Michael Findlay the VALUE of ART

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Elementary, My Dear Readers

NEW ORLEANS NOSTALGIA Remembering New Orleans History, Culture and Traditions By Ned Hémard Elementary, My Dear Readers NCIS (which stands for Naval Criminal Investigative Service) is an extremely popular “police procedural” television drama that has spun off as a New Orleans series. NCIS: New Orleans, which airs Tuesday nights on CBS, is set in the Crescent City and it would be highly unusual if you haven’t seen the show filming around town. It premiered on September 23, 2014. The episodes revolve around a fictional team of agents led by Special Agent Dwayne Cassius “King” Pride, Special Agent Christopher LaSalle, and Special Agent Meredith Brody. They handle criminal investigations involving the U.S. Navy and Marine Corps. If the NCIS team seems to be everywhere you look these days, allow yourself to travel back in literary time and imagine another famous detective team present all around you. Even if their bailiwick was late Victorian England, I seem to feel their presence all around this historic city. Perhaps you will, too. Arthur Conan Doyle penned his first Sherlock Holmes story, A Study in Scarlet, in novel form in 1886 at the age of 27. In it Holmes expounded: “Criminal cases are continually hinging upon that one point. A man is suspected of a crime months perhaps after it has been committed. His linen or clothes are examined and brownish stains discovered upon them. Are they blood stains, or mud stains, or rust stains, or fruit stains, or what are they? That is a question which has puzzled many an expert, and why? Because there was no reliable test. -

Behind the Camera

BEHIND THE CAMERA BEHIND THE CAMERA CREATIVE TECHNIQUES OF 100 GREAT PHOTOGRAPHERS PRESTEL PAUL LOWE MUNICH • LONDON • NEW YORK Previous page People worshipping during the first prayers at Begova Dzamija mosque in Sarajevo, Bosnia, after its reopening following the civil war. Prestel Verlag, Munich · London · New York 2016 A member of Verlagsgruppe Random House GmbH Neumarkter Strasse 28 · 81673 Munich Prestel Publishing Ltd. 14-17 Wells Street London W1T 3PD Prestel Publishing 900 Broadway, Suite 603 New York, NY 10003 www.prestel.com © 2016 Quintessence Editions Ltd. This book was produced by Quintessence Editions Ltd. The Old Brewery 6 Blundell Street London N7 9BH Project Editor Sophie Blackman Editor Fiona Plowman Designer Josse Pickard Picture Researcher Jo Walton Proofreader Sarah Yates Indexer Ruth Ellis Production Manager Anna Pauletti Editorial Director Ruth Patrick Publisher Philip Cooper All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the permission of the copyright holder. Library of Congress Control Number: 2016941558 ISBN: 978-3-7913-8279-1 10 9 8 7 6 5 4 3 2 1 Color reproduction by Bright Arts, Hong Kong. Printed in China by C&C Offset Printing Co., LTD. Foreword 6 Introduction 8 Key to creative tips and techniques icons 18 Contents Places 42 Spaces 68 Things 90 Faces 108 Bodies 134 Ideas 158 Moments 180 Stories 206 Documents 228 Histories 252 Bibliography 276 Glossary 278 Index 282 Picture credits 288 by Simon Norfolk by Foreword Foreword I happened to be in Paris on the night of the terrorist attacks at We were either totally wasting our time (the terrorists were the Bataclan concert hall and the Stade de France in 2015. -

Ben Heller, Pioneering Collector of Abstract Expressionism: ‘There’S Nobody Else in That League’

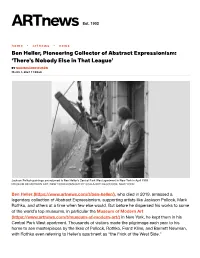

Est. 1902 home • ar tnews • news Ben Heller, Pioneering Collector of Abstract Expressionism: ‘There’s Nobody Else in That League’ BY MAXIMILÍANO DURÓN March 3, 2021 11:00am Jackson Pollock paintings are returned to Ben Heller's Central Park West apartment in New York in April 1959. MUSEUM OF MODERN ART, NEW YORK/LICENSED BY SCALA/ART RESOURCE, NEW YORK Ben Heller (https://www.artnews.com/t/ben-heller/), who died in 2019, amassed a legendary collection of Abstract Expressionism, supporting artists like Jackson Pollock, Mark Rothko, and others at a time when few else would. But before he dispersed his works to some of the world’s top museums, in particular the Museum of Modern Art (https://www.artnews.com/t/museum-of-modern-art/) in New York, he kept them in his Central Park West apartment. Thousands of visitors made the pilgrimage each year to his home to see masterpieces by the likes of Pollock, Rothko, Franz Kline, and Barnett Newman, with Rothko even referring to Heller’s apartment as “the Frick of the West Side.” When he began seriously collecting Abstract Expressionism during the ’50s, museums like MoMA largely ignored the movement. Heller rushed in headlong. “He wasn’t someone to say, ‘Let me take a gamble on this small picture so that I don’t really commit myself.’ He committed himself a thousand percent, which is what he believed the artists were doing,” Ann Temkin, chief curator of painting and sculpture at MoMA, said in an interview. Though Heller was never formally a board member at MoMA—“I was neither WASP-y enough nor wealthy enough,” he once recalled—he transformed the museum, all the while maintaining close relationships with artists and curators in its circle. -

The New American Art Lily Rothman Oct 09, 2017

The Oct. 13, 1967, cover of TIME TIME MEDIA 50 Years Ago This Week: The New American Art Lily Rothman Oct 09, 2017 Milestone moments do not a year make. Often, it’s the smaller news stories that add up, gradually, to big history. With that in mind, in 2017 TIME History will revisit the entire year of 1967, week by week, as it was reported in the pages of TIME. Catch up on last week’s installment here. Week 41: Oct. 13, 1967 Tony Smith was the "most dynamic, versatile and talented new sculptor in the U.S. art world" proclaimed this week's cover story — but that wasn't the only reason why his work was so newsworthy. The other factor worth considering was what his work at the time looked like. Smoke, the work discussed at the top of the article, was metal, crafted in a fabrication shop from his designs, and it was huge. Smith was TIME's way of looking at a major new trend in contemporary art. As American cities grew and modernized, they needed art that could hold its own. Enter the new American artist: In the year 1967, the styles and statements of America's brash, brilliant and often infuriating contemporary artists have not only become available to the man in the street, but are virtually unavoidable. And with proliferation comes confusion. Whole new schools of painting seem to charge through the art scene with the speed of an express train, causing Pop Artist Andy Warhol to predict the day "when everyone will be famous for 15 minutes." ...Tony Smith, who was thought of as primarily an architect at the time, witnessed the coming of age of the U.S. -

The Painted Word a Bantam Book / Published by Arrangement with Farrar, Straus & Giroux

This edition contains the complete text of the original hardcover edition. NOT ONE WORD HAS BEEN OMITTED. The Painted Word A Bantam Book / published by arrangement with Farrar, Straus & Giroux PUBLISHING HISTORY Farrar, Straus & Giroux hardcover edition published in June 1975 Published entirely by Harper’s Magazine in April 1975 Excerpts appeared in the Washington Star News in June 1975 The Painted Word and in the Booh Digest in September 1975 Bantam mass market edition / June 1976 Bantam trade paperback edition / October 1999 All rights reserved. Copyright © 1975 by Tom Wolfe. Cover design copyright © 1999 by Belina Huey and Susan Mitchell. Book design by Glen Edelstein. Library of Congress Catalog Card Number: 75-8978. No part o f this book may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the publisher. For information address: Farrar, Straus & Giroux, 19 Union Square West, New York, New York 10003. ISBN 0-553-38065-6 Published simultaneously in the United States and Canada Bantam Books are published by Bantam Books, a division of Random House, Inc. Its trademark, consisting of the words “Bantam Books” and the portrayal of a rooster, is Registered in U.S. Patent and Trademark Office and in other countries. Marca Registrada. Bantam Books, New York, New York. PRINTED IN THE UNITED STATES OF AMERICA BVG 10 9 I The Painted Word PEOPLE DON’T READ THE MORNING NEWSPAPER, MAR- shall McLuhan once said, they slip into it like a warm bath. -

Zeus in the Greek Mysteries) and Was Thought of As the Personification of Cyclic Law, the Causal Power of Expansion, and the Angel of Miracles

Ζεύς The Angel of Cycles and Solutions will help us get back on track. In the old schools this angel was known as Jupiter (Zeus in the Greek Mysteries) and was thought of as the personification of cyclic law, the Causal Power of expansion, and the angel of miracles. Price, John Randolph (2010-11-24). Angels Within Us: A Spiritual Guide to the Twenty-Two Angels That Govern Our Everyday Lives (p. 151). Random House Publishing Group. Kindle Edition. Zeus 1 Zeus For other uses, see Zeus (disambiguation). Zeus God of the sky, lightning, thunder, law, order, justice [1] The Jupiter de Smyrne, discovered in Smyrna in 1680 Abode Mount Olympus Symbol Thunderbolt, eagle, bull, and oak Consort Hera and various others Parents Cronus and Rhea Siblings Hestia, Hades, Hera, Poseidon, Demeter Children Aeacus, Ares, Athena, Apollo, Artemis, Aphrodite, Dardanus, Dionysus, Hebe, Hermes, Heracles, Helen of Troy, Hephaestus, Perseus, Minos, the Muses, the Graces [2] Roman equivalent Jupiter Zeus (Ancient Greek: Ζεύς, Zeús; Modern Greek: Δίας, Días; English pronunciation /ˈzjuːs/[3] or /ˈzuːs/) is the "Father of Gods and men" (πατὴρ ἀνδρῶν τε θεῶν τε, patḕr andrōn te theōn te)[4] who rules the Olympians of Mount Olympus as a father rules the family according to the ancient Greek religion. He is the god of sky and thunder in Greek mythology. Zeus is etymologically cognate with and, under Hellenic influence, became particularly closely identified with Roman Jupiter. Zeus is the child of Cronus and Rhea, and the youngest of his siblings. In most traditions he is married to Hera, although, at the oracle of Dodona, his consort is Dione: according to the Iliad, he is the father of Aphrodite by Dione.[5] He is known for his erotic escapades. -

Duke Certamen 2018 Novice Division Round 1

DUKE CERTAMEN 2018 NOVICE DIVISION ROUND 1 1. Also known as the Boreads, what twin brothers were said to have purple wings which allowed them to fly? ZETES AND CALAÏS B1: When Zetes and Calaïs chased the Harpies all the way to the Strophades Islands, either Iris or what messenger deity persuaded them to stop, promising that the Harpies would no longer hurt Phineus? HERMES B2: Which of the Argonauts killed Zetes and Calais because they had convinced the rest of the Argonauts to abandon him in Mysia? HERACLES 2. If, after listening to a Latin translation of Jay-Z’s song Encore, your friend asks you what “Vēni, vīdi, vīci” means in English, how should you respond? I CAME, I SAW, I CONQURERED B1: That same friend then googles more Julius Caesar quotes. Next, She asks you what “Alea Iacta est” means in English. What do you tell her? THE DIE IS/HAS BEEN CAST B2: An acquaintance, having overheard this conversation, comes over and tells you that they don’t see why you are speaking a “dead language.” Being the witty Classicist that you are, you respond “rident stolidi linguam Latinam.” What did you just say? FOOLS LAUGH AT THE LATIN LANGUAGE 3. For the phrase magnus agricola, give the dative singular. MAGNŌ AGRICOLAE B1: Make that phrase plural. MAGNĪS AGRICOLĪS B2: Make the phrase genitive plural. MAGNORUM AGRICOLORUM 4. What pious king of Rome advanced Roman religious tradition with such deeds as founding the Roman calendar and building the temple of Janus? NUMA POMPILIUS B1: Numa was said to be guided by what nymph? EGERIA B2: Numa originated from what tribe? SABINES 5. -

Oral History Interview with Leo Castelli

Oral history interview with Leo Castelli Archives of American Art 750 9th Street, NW Victor Building, Suite 2200 Washington, D.C. 20001 https://www.aaa.si.edu/services/questions https://www.aaa.si.edu/ Table of Contents Collection Overview ........................................................................................................ 1 Administrative Information .............................................................................................. 1 General............................................................................................................................. 2 Scope and Contents........................................................................................................ 1 Scope and Contents........................................................................................................ 1 Biographical / Historical.................................................................................................... 1 Names and Subjects ...................................................................................................... 2 Container Listing ...................................................................................................... Oral history interview with Leo Castelli AAA.castel69may Collection Overview Repository: Archives of American Art Title: Oral history interview with Leo Castelli Identifier: AAA.castel69may Date: 1969 May 14-1973 June 8 Creator: Castelli, Leo (Interviewee) Cummings, Paul (Interviewer) Extent: 194 Pages (Transcript) Language: English -

The Staff of Asclepius Or Hermes Eric Vanderhooft, M.D

aduceus Cthe staff of Asclepius or Hermes Eric Vanderhooft, M.D. The author (AΩA, University of Utah, 1988) is clinical assistant professor in the Department of Orthopedics at the University of Utah, and in private practice at the Salt Lake Orthopedic Clinic. He is also the clinical director of the University Orthopedic Rotation and Family Practice Residency Orthopedic Rotation at HCA St. Mark’s Hospital. he staff entwined by a serpent or serpents is ac- cepted as a common symbol of the medical pro- fession and health care industry. Unfortunately, twoT distinct images exist. The staff with a single snake be- longed to Asclepius, father of western medicine. The staff with two entwined snakes belonged to Hermes, the prince of thieves, and is more commonly seen. A review of 527 professional medical academies, asso- ciations, colleges, and societies revealed that 23 organiza- tions use the staff in their symbolism. The staff of Asclepius outnumbered that of Hermes nearly three-fold, 92 versus 3 organizations respectively. Introduction Hippocrates has come to be considered the father of Western medicine, and, in the United States, a modification of the Hippocratic Oath continues to be recited by graduat- ing medical students. It should therefore be no surprise that Roman statue of Asclepius. © Mimmo Jodice/CORBIS. The Pharos/Autumn 2004 our symbol for medicine, the caduceus, similarly is derived from Greek traditions. Greek healers such as Hippocrates be- lieved they were descended from Asclepius, the mythic phy- sician, and came to be known as Asklepiadai or Asclepiads, “sons of Asclepius.”1p6 Represented variously by the snake, cock, dog, and goat,1p28–32, 2, 3p258 the staff entwined by a single snake is the most recognized symbol of Asclepius. -

Design the Whole Story

DESIGN THE WHOLE STORY General Editor Elizabeth Wilhide Foreword by Jonathan Glancey DESIGN THE WHOLE STORY PRESTEL Munich • London • New York Calico printing at the Morris and Co workshop in Merton Abbey Mills, London, in 1931. Prestel Verlag, Munich · London · New York 2016 A member of Verlagsgruppe Random House GmbH Neumarkter Strasse 28 · 81673 Munich Prestel Publishing Ltd. 14-17 Wells Street London W1T 3PD Prestel Publishing 900 Broadway, Suite 603 New York, NY 10003 www.prestel.com © 2016 Quintessence Editions Ltd. This book was designed and produced by Quintessence Editions Ltd., London Senior Editor Elspeth Beidas Editors Rebecca Gee, Carol King, Frank Ritter Senior Designer Isabel Eeles Design Assistance Tom Howey, Thomas Keenes Picture Researcher Sarah Bell Production Manager Anna Pauletti Editorial Director Ruth Patrick Publisher Philip Cooper All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any other information storage and retrieval system, or otherwise without prior permission in writing from Prestel Publishing. ISBN 978-3-7913-8189-3 Library of Congress Control Number: 2016941556 A CIP catalogue record for this book is available from the British Library. Printed in China CONTENTS FOREWORD by Jonathan Glancey 6 INTRODUCTION 8 1 | the emergence of design 1700 – 1905 16 2 | the age of the machine 1905 – 45 108 3 | identity and conformity 1945 – 60 222 4 | design and the quality of life 1960 – 80 326 5 | -

Collection of Hesiod Homer and Homerica

COLLECTION OF HESIOD HOMER AND HOMERICA Hesiod, The Homeric Hymns, and Homerica This file contains translations of the following works: Hesiod: "Works and Days", "The Theogony", fragments of "The Catalogues of Women and the Eoiae", "The Shield of Heracles" (attributed to Hesiod), and fragments of various works attributed to Hesiod. Homer: "The Homeric Hymns", "The Epigrams of Homer" (both attributed to Homer). Various: Fragments of the Epic Cycle (parts of which are sometimes attributed to Homer), fragments of other epic poems attributed to Homer, "The Battle of Frogs and Mice", and "The Contest of Homer and Hesiod". This file contains only that portion of the book in English; Greek texts are excluded. Where Greek characters appear in the original English text, transcription in CAPITALS is substituted. PREPARER'S NOTE: In order to make this file more accessable to the average computer user, the preparer has found it necessary to re-arrange some of the material. The preparer takes full responsibility for his choice of arrangement. A few endnotes have been added by the preparer, and some additions have been supplied to the original endnotes of Mr. Evelyn-White's. Where this occurs I have noted the addition with my initials "DBK". Some endnotes, particularly those concerning textual variations in the ancient Greek text, are here ommitted. PREFACE This volume contains practically all that remains of the post- Homeric and pre-academic epic poetry. I have for the most part formed my own text. In the case of Hesiod I have been able to use independent collations of several MSS. by Dr. -

A N T I C H I T À

A N T I C H I T À ALBERTO DI CASTRO Late-Mannerist European sculptor Second half 16th century The Three Graces High relief in terracotta, 57.5 x 45.5 x 13.5 cm (22 5/8 x 17 7/8 x 5 3/8 in.) The artistic popularity of the Graces can be traced back to the Charities, minor Ancient Greek goddesses who centuries later in Ancient Rome became known as the Three Graces. Tasked with spreading goodwill, pleasure and mirth, Aglaea, “beauty, splendour or glory”, Euphrosyne, “good cheer or mirth”, and Thalia, “rich banquet or festivity”, were the immortal daughters of Zeus and the sea-nymph Eurynome; they attended banquets and, together with the Muses, danced for the gods. Their principal attributes, an apple, a rose and a sprig of myrtle. Although only Roman copies are to be found today, the earliest portrayals of the three Graces belong to the Hellenistic period. Antichità Alberto Di Castro S.r.l. Socio Unico Piazza di Spagna, 5 – 00187 Roma T. +39 06 6792269 – Fax +39 06 6787410 [email protected] – www.dicastro.com A N T I C H I T À ALBERTO DI CASTRO Fig. 1: The Three Graces: portrayal and sculpture, Roman age The enormous success enjoyed by the Three Graces throughout the years of the Roman Empire (fig. 1) presented itself anew with the advent of the Renaissance thanks to the production of numerous 16th century engravings by Marco Dente (?–1527), Enea Vico (1523–1567), Étienne Delaune (1518/19– 1583) (fig. 2) and other anonymous artists.