Sioux City Economic Development Department

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Convention Center Hotel Nears Completion PAGE J2 Courtyard by Marriott in Downtown Sioux City to Feature 151 Rooms

INDUSTRY SUNDAY, MARCH 17, 2019 | siouxcityjournal.com | SECTION I Today, in its annual Progress edition, The Journal continues a series of special sections over fi ve Sundays that detail new development in the tri-state region. Sections I and J today focus on a bevy of industrial and housing projects. TIM HYNDS PHOTOS, SIOUX CITY JOURNAL Developer to restore Warrior Hotel and Davidson Building developers Renee and Lew Weinberg, left, talk with Restoration St. Louis’ Amy and Amrit Gill prior to a three historic buildings in ceremonial ribbon cutting held Tuesday, Feb. 5, 2019, in what will become the second-story lobby area of the Warrior Hotel in downtown Sioux City. The long-empty historic hotel and the adjacent Davidson Building are being remodeled into hotel, apartment and retail spaces. Sioux City. HISTORIC WARRIOR gets extensive facelift Ho-Chunk Inc.’s Flatwater DOLLY A. BUTZ Crossing in South Sioux [email protected] enters next phases. SIOUX CITY — Plans to restore the War- rior Hotel to its former glory have come and gone over the past 40 years, but this time, PAGE I5 Amy and Amrit Gill, owners of Restoration St. Louis, say rehabilitation of the historic building is a “done deal.” The humming of construction equipment echoed through the Warrior on a Monday af- ternoon in early February as the Gills toured the historic hotel. A buck hoist, a temporary elevator, was being put in place to transport materials to each fl oor of the Warrior, and demolition work was ongoing in the next- door Davidson Building. First units sold in Sioux “When you do a hotel like this with Mar- City’s Chestnut Hill riott’s blessing, it can’t look like anything People leave the former Warrior Hotel following a ceremonial ribbon cutting Feb. -

Offering Memorandum 4Th & Jackson | Of�Ce Condos 700 4Th St, Sioux City, IA 51101 for Sale Of�Ce Building 12,751 SF | $1,174,725

For Sale Ofce Building 12,751 SF | $1,174,725 Offering Memorandum 4th & Jackson | Ofce Condos 700 4th St, Sioux City, IA 51101 For Sale Ofce Building 12,751 SF | $1,174,725 Table of Contents 4 Section 1 Location Information 11 Section 2 Property Information 19 Section 3 Demographics For Sale Ofce Building 12,751 SF | $1,174,725 SALE PRICE: $1,174,725 Property Overview NUMBER OF UNITS: 4 100% leased office condo investment in the heart of Siouxland's entertainment district. The sale includes CAP RATE: 8.0% the first two floors, consisting of units 100, 200, 210 & 220. GRM: 6.8 NOI: $93,978 Featuring lots of natural light and great views down Historic Fourth, the entire building has been remodeled LOT SIZE: 2.6 Acres and converted to Class A space. The building has direct 4th floor and skywalk level accesses to the BUILDING SIZE: 12,751 SF adjacent Heritage Parking Ramp and direct skywalk access to the Sioux City Convention Center, Marriott BUILDING CLASS: A Courtyard, Mercy One, Orpheum Theatre & Historic Pearl. Also adjacent is the Promenade 14 Cinema & YEAR BUILT: 1972 RENOVATED: 2020 Marto Brewing. ZONING: DC MARKET: Sioux City, IA Building naming rights facing I-29 are available for future non-financial anchor tenant. Sale includes seller's SUB MARKET: Downtown installation of a $115,000 HVAC system on main floor prior to closing, which will reduce annual repair CROSS STREETS: 4th St & Jackson St costs. TRAFFIC COUNT: 10,400 400 Gold Circle, Suite 120 Dakota Dunes, SD 57049 712 224 2727 tel naiunited.com 4th & Jackson | Ofce Condos 700 4th -

¨§¦35 ¨§¦29 ¨§¦80

FEDERAL HISTORIC TAX CREDIT PROJECTS Iowa A total of 382 Federal Historic Tax Credit projects (certified by the National Park Service) and $325,028,326 in Federal Historic Tax Credits between fiscal year 2001 through 2020, leveraged an estimated $1,868,912,873 in total development. Data source: National Park Service, 2020 Spirit Lake 3 Decorah 2 7 Spillville Spencer Mason City Algona West Union3 Sumner Waverly 35 ¦¨§ Waterloo Sherrill 18 Fort Dodge4 28 46 Iowa Falls Cedar Falls Sioux City Independence Dubuque Eldora New 380 Bellevue Providence ¦¨§ Marion Ames 5Marshalltown Jefferson2 3 4 Maquoketa Denison 42 ¦¨§29 Story Colo State Center 2 Cedar Rapids Mount Vernon Clinton4 Dunlap Perry Woodbine5 Minburn 9 80 Iowa City West Des Newton Grinnell ¦¨§ 5Tipton Le Claire 68 Stuart Moines Davenport 39 ¦¨§680 Shelby Des Moines Bettendorf Earlham Muscatine3 Atlantic 3 Winterset Oskaloosa 11 5 Greenfield Washington Council Peru Bluffs Mount Creston Osceola Albia Pleasant Red Oak Corning Chariton 2 8 2 Clarinda Burlington Bloomfield Fort Madison3 Bedford Keokuk3 Federal Historic Tax Credit Projects 1 6 - 10 0 20 40 80 Miles R 2 - 5 11 and over Provided by the National Trust for Historic Preservation and the Historic Tax Credit Coalition For more information, contact Shaw Sprague, NTHP Vice President for Government Relations | (202) 588-6339 | [email protected] or Patrick Robertson, HTCC Executive Director | (202) 302-2957 | [email protected] Iowa Historic Tax Credit Projects, FY 2001-2020 Project Name Address City State Year Qualified Project Use Expenditures Peoples State Bank 102 S. Main Street Albia IA 2001 $1,271,000 Not Reported Algona Junior & Senior 213 & 301 South Algona IA 2017 $5,052,631 Housing High School Bldg. -

3. 1887 Corn Palace 4. Kemp Building 5. Commerce Building 9. 1888 Corn Palace 9. 1889 Corn Palace 9. 1890 Corn Palace 9. 1

3. 1887 Corn Palace 4. Kemp Building 5. Commerce Building 9. 1888 Corn Palace 9. 1889 Corn Palace 9. 1890 Corn Palace 9. 1891 Corn Palace 11. Government Corner, 1940s 12. Municipal Auditorium 1. Badgerow Building 1933 Art Deco style National Register of Historic Places Sioux City Features stylized Native American busts along cornice and elaborate geometric patterns on 2nd floor windows. Sioux City’s largest and finest office building for several decades. Named one of Iowa’s top 100 buildings in 2004. 2. Martin Department Store Annex 1902 Beaux Arts style National Register Downtown One of two remaining Beaux Arts buildings in downtown. Features terra cotta and glazed brick. Constructed as an annex to the T.S. Martin Department Store, the building later housed the Cameo Theater (movie theater) from 1969 to 1989. 3. 1887 Corn Palace October 3-8 1887 Walking Tour 20,000 bushels of grain were used to decorate this structure which was visited by 140,000 people, including President Grover Cleveland. The Goldie Roller skating rink was operated on the same site from 1884-87. Start at #1 4. Kemp Building Built in the late 1910s Retail/Commercial Style First known as the Kemp Building, later home to a variety of businesses including the Ryal Miller Chevrolet Company 4th and Jackson (622 4th Street) (later evolved to become Knoepfler Chevrolet), tire sales, bakery, café, grocery store and the Yellow Cab Company. 5. Motor Mart/Commerce Building 1912 Chicago School style National Register Originally constructed as Ralph Bennet’s Motor Mart Building, it included a freight elevator to lift automobiles. -

Rescue Ready

RESCUE READY LOCAL LANDMARKS VISIONARY VENUE SPRING - SUMMER 2019 LANDMARK READY TO WORK GET THE LEAD OUT EXPO UPDATE Partnering with the City of Sioux City, Woodbury County has become the first county in Iowa Local homeowners can receive funding to The new Siouxland Expo Center will RENOVATION to achieve ACT Work Ready Communities certification—a national initiative that matches address lead paint and other health hazards be one-of-a-kind yet offer something thanks to a grant from the U.S. Department of for everyone. Renovation of two Sioux City treasures is skilled workers with jobs in demand. Housing and Urban Development Lead-Based “This dynamic facility will be underway! The Warrior Hotel was built as a The program provides companies with evidence of a skilled workforce, as each Paint Hazard Reduction Program. Sioux City completely unique to the region and premier hotel in 1930 but closed in 1976, participating community must measure and improve the skill levels of its workforce through a standardized workforce skills credential—the is one of just 48 state and local government complement existing venues in the while the Davidson Building was the city’s Before National Career Readiness Certificate. agencies in the nation to share in $139 million community,” shares Renae Billings, business development first office building when it was constructed “This recognition provides local employers awarded through the HUD grant. coordinator for the City of Sioux City. “Major expo events can in 1913. Both appear on the National and prospective companies with credible “This special honor is given to the attract thousands of people from a wide radius and generate Register of Historical Places but have been data on the workforce in our county,” says community as a whole, yet the improvements considerable economic activity for the region.” underutilized for decades. -

Downtown Sioux City

Community Name: Downtown Sioux City Priority Dates for New Main Street Program Visits (If designated) In order to facilitate scheduling new Main Street Iowa program visits, we ask that your community prioritize the three date options listed for each new program service. Main Street Iowa will do our best to accommodate high priority dates. If a date does not work for your community please note that below. The visits listed below will only be conducted if the community is designated a new Main Street Iowa program. If your community is not designated a new Main Street Iowa program in this round, Main Street Iowa will schedule a visit to discuss Main Street Iowa Advisory Council score, recommendations, and guidance for future activities. These visits will take place in September. New Main Street Program Visits (Date Choices -- September 3, 9, or 10) This initial onsite visit after designation will be approximately 3-4 hours in length. Agenda will tentatively include: time for a local presentation of Main Street Iowa signage/press conference, a meeting with the local hiring committee, and approximately 90 minutes with the local Main Street Board of Directors and City representatives to discuss Board roles and responsibilities and planning for future Main Street Iowa visits. First Priority of Date Choices: September 3 Second Priority of Date Choices: September 9 Third Priority of Date Choices: September 10 Baseline Visits (Date Choices -- October 6-8, October 13-15, or October 27-29) The Baseline Visit will be a 2 ½ day onsite, intensive Main Street Iowa consulting team visit. The intent of the Baseline Visit is to gain an understanding of local downtown development opinion, partners, and direction. -

May 3 0 2006

MAY 3 0 2006 NPSForm 10-900 (Rev. 10-90) United States Department of the Interior National Park Service This form is for use in nominating or requesting determinations for individual properties and districts. See instructions irirteiMo oiJjflpKte the National Register of Historic Places Registration Form (National Register Bulletin 16A). Complete elch item by marking "x" m^h^propriate box or by entering the information requested. If any item does not apply to the property being documented, enter "N/A" for "not applicable:ll*For functions, architectural classification, materials, and areas of significance, enter only categories and subcategories from the instructions. Place additional entries and narrative items on continuation sheets (NPS Form 10-900a). Use a typewriter, word processor, or computer, to complete all items. 1. Name of Property historic name .Municipal Auditorium other names/site number 2. Location street & number___ 500 Gordon Drive _D not for publication N/A city or town_____ Sioux City D vicinity N/A state Iowa code IA county Wood bury zip code 51102 3. State/Federal Agency Certification As the designated authority under the National Historic Preservation Act of1986, as amended, I hereby certify that this X nomination D request for determination of eligibility meets the documentation standards for registering properties in the National Register of Historic Places and meets the procedural and professional requirements set forth in 36 CFR Part 60. In my opinion, the property X meets D does not meet the National Register Criteria. I recommend that this property be considered significant D nationally D statewide^Upcally. (D See continuation sheet for additional comments.) Signature of certifying official CTre HISTORICAL SOCIETY OF IOWA State or Federal agency and bureau In my opinion, the property D meets D does not meet the National Register criteria. -

Fall 2016 Newsletter/Annual Repor

Fall 2016 • Vol. 2, Issue 11 “Virtual Collections” website is launched “We were very pleased to The Museum’s Virtual Collec- receive a Gilchrist Founda- tions is an “online museum” tion grant to turn the vision of with something for every- having the collection more one; for both people in Sioux available to the public into City who visit the museum a reality,” said Steve Hansen, frequently and people from Museum Director. out of town who might be interested in Sioux City and The new Virtual Collections website front To showcase the Museum’s its history, but not able to visit page features rotating images of artifacts. collections online like larger the facility. ver want to see what institutions is a major under- the Sioux City Public taking requiring many hours “We wanted to have a mix EMuseum has in its exten- of staff time. Fortunately, of artifacts from the perma- sive collection? With more intern/volunteer Haley (Brees) nent gallery and from the ar- than 60,000 objects, over one Aguirre had the right experi- tifacts in storage that people million photographic images, ence; her thesis for the Uni- may never see,” said Aguirre. and 3,600 linear feet of ar- versity Honors Program at the (continued on page 2) chival materials, only a small University of South Dakota fraction of the collection is was a website exploring his- Inside: on display in the permanent tory through the use of vari- FY 2016 annual report gallery. ous objects. Sioux City is first stop for national touring exhibit he new touring exhibition, historical A Photo Album of records TIreland, emerges from may have an ongoing democratic overlooked. -

Sioux City Badgerow Building Redevelopment SOI Page 2

STATEMENT OF INTEREST FOR REDEVELOPMENT OF THE BADGEROW BUILDING AT 622 4TH STREET Sioux City, Iowa Issued: Friday April 3, 2020 Submission Deadline: May 13, 2020 Issued on Behalf of Sioux City by: Hunden Strategic Partners, Inc. 213 W Institute Place, Suite 707 Chicago, Illinois 60610 Primary Contact: Rob Hunden [email protected] Introduction to the Opportunity The City of Sioux City (“Client”) is seeking a qualified Developer or Development Team (Developer) for the purchase and redevelopment of the Badgerow Building in Sioux City, Iowa (Project). The Badgerow Building is an historic building sitting on a 0.22-acre site in downtown Sioux City, just north of the Missouri River and I-29. The building was built in 1920 and originally operated as an office building. It is located on the edge of Sioux City’s Historic 4th Street Entertainment District. The City is seeking to have the building redeveloped to accommodate a mix of uses, including, but not limited to, retail, restaurant, office, and market rate residential. Sioux City is open to helping induce a compelling redevelopment via the use of incentives if proven needed, which are detailed in their own section in this Statement of Interest (SOI). This document outlines the process by which the Client will move through the solicitation and selection process, as well as the overall intent of the development. The Client has engaged Hunden Strategic Partners, Inc. (HSP) to administer the selection process, communicate with potential Developers, and generally smooth the process for all parties under a set of guidelines for all involved. Project. -

Federal Register / Vol. 48, No. 41 / Tuesday, March 1, 1983 / Notices 8621

Federal Register / Vol. 48, No. 41 / Tuesday, March 1, 1983 / Notices 8621 UNITED STATES INFORMATION 2. The authority to redelegate the VETERANS ADMINISTRATION AGENCY authority granted herein together with the power of further redelegation. Voluntary Service National Advisory [Delegation Order No. 83-6] Texts of all such advertisements, Committee; Renewal notices, and proposals shall be This is to give notice in accordance Delegation of Authority; To the submitted to the Office of General Associate Director for Management with the Federal Advisory Committee Counsel for review and approval prior Act (Pub. L. 92-463) of October 6,1972, Pursuant to the authority vested in me to publication. that the Veterans Administration as Director of the United States Notwithstanding any other provision Voluntary Service National Advisory Information Agency by Reorganization of this Order, the Director may at any Committee has been renewed by the Plan No. 2 of 1977, section 303 of Pub. L. time exercise any function or authority Administrator of Veterans Affairs for a 97-241, and section 302 of title 5, United delegated herein. two-year period beginning February 7, States Code, there is hereby delegated This Order is effective as of February 1983 through February 7,1985. 8,1983. to the Associate Director for Dated: February 15,1983. Management the following described Dated: February 16,1983. By direction of the Administrator. authority: Charles Z. Wick, Rosa Maria Fontanez, 1. The authority vested in the Director Director, United States Information Agency. by section 3702 of title 44, United States Committee Management Officer. [FR Doc. 83-5171 Filed 2-28-83; 8:45 am] Code, to authorize the publication of [FR Doc. -

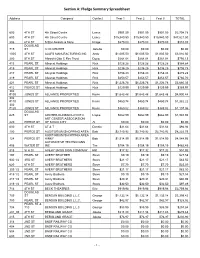

Section A: Pledge Summary Spreadsheet

Section A: Pledge Summary Spreadsheet Address Company Contact Year 1 Year 2 Year 3 TOTAL 600 4TH ST 4th Street Centre Lance $901.59 $901.59 $901.59 $2,704.78 600 4TH ST 4th Street Centre Lance $15,940.50 $15,940.50 $15,940.50 $47,821.50 206 6TH ST 5 Star Awards & More Krage $270.03 $270.03 $270.03 $810.09 DOUGLAS 715 ST A I D CENTER Jonette $0.00 $0.00 $0.00 $0.00 1005 4TH ST AALFS MANUFACTURING INC Andy $1,005.50 $1,005.50 $1,005.50 $3,016.50 200 5TH ST Albrecht Otto C Rev Trust Doug $264.04 $264.04 $264.04 $792.13 413 PEARL ST Alleycat Holdings Rick $128.28 $128.28 $128.28 $384.84 415 PEARL ST Alleycat Holdings Rick $236.25 $236.25 $236.25 $708.75 417 PEARL ST Alleycat Holdings Rick $158.43 $158.43 $158.43 $475.28 419 PEARL ST Alleycat Holdings Rick $253.57 $253.57 $253.57 $760.70 421 PEARL ST Alleycat Holdings Rick $1,226.78 $1,226.78 $1,226.78 $3,680.35 412 PIERCE ST Alleycat Holdings Rick $129.99 $129.99 $129.99 $389.97 302 #100 JONES ST ALLIANCE PROPERTIES Kevin $1,643.48 $1,643.48 $1,643.48 $4,930.44 302 #110 JONES ST ALLIANCE PROPERTIES Kevin $460.74 $460.74 $460.74 $1,382.22 302 #120 JONES ST ALLIANCE PROPERTIES Kevin $369.02 $369.02 $369.02 $1,107.06 DOUGLAS 625 ST ARCHER-DUNBAR LOYCE C Loyce $662.99 $662.99 $662.99 $1,988.98 ART CENTER ASSOCIATION 220 PIERCE ST OF SIOUX CITY Al $0.00 $0.00 $0.00 $0.00 600 4TH ST AT & T Dennis $31.64 $31.64 $31.64 $94.93 100 PIERCE ST AUDITORIUM SHOPPING AREA Bob $2,740.92 $2,740.92 $2,740.92 $8,222.75 AUDITORIUM SHOPPING AREA 124 PIERCE ST HINKY Bob $1,514.99 $1,514.99 $1,514.99 $4,544.96 AUTOMOTIVE -

NOTICE of MEETING of the CITY COUNCIL of the CITY of SIOUX CITY, IOWA City Council Agendas Are Also Available on the Internet At

NOTICE OF MEETING OF THE CITY COUNCIL OF THE CITY OF SIOUX CITY, IOWA City Council agendas are also available on the Internet at www.sioux-city.org. You are hereby notified a meeting of the City Council of the City of Sioux City, Iowa, will be held Monday, May 6, 2019, 4:00 p.m., local time, in the Council Chambers, 5th Floor, City Hall, 405 6th Street, Sioux City, Iowa, for the purpose of taking official action on the agenda items shown hereinafter and for such other business that may properly come before the Council. This is a formal meeting during which the Council may take official action on various items of business. If you wish to speak on an item, please follow the seven participation guidelines adopted by the Council for speakers: 1. Anyone may address the Council on any agenda item. 2. Speakers should approach the microphone one at a time and be recognized by the Mayor. 3. Speakers should give their name, spell their name, give their address, and then their statement. 4. Everyone should have an opportunity to speak. Therefore, please limit your remarks to three minutes on any one item. 5. At the beginning of the discussion on any item, the Mayor may request statements in favor of an action be heard first followed by statements in opposition to the action. 6. Any concerns or questions you may have which do not relate directly to a scheduled item on the agenda will also be heard under ‘Citizen Concerns’. 7. For the benefit of all in attendance, please turn off all cell phones and other communication devices while in the City Council Chambers.