Finances and Governance of Urban Local Bodies: an Approach of Urban Development Perspective from a Developing Country (India)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Urban Population Growth in the Municipalities of North 24 Parganas, It Is Clear That North 24 Parganas Has Retained a High Level of Urbanization Since Independence

World Wide Journal of Multidisciplinary Research and Development WWJMRD 2018; 4(3): 68-73 www.wwjmrd.com International Journal Peer Reviewed Journal Urban Population Growth in the Municipalities of Refereed Journal Indexed Journal North 24 Parganas: A Spatio-Temporal Analysis UGC Approved Journal Impact Factor MJIF: 4.25 E-ISSN: 2454-6615 Mashihur Rahaman Mashihur Rahaman Abstract Research Scholar The rapid growth of urban population causes various problems in urban centres like increased P.G. Department of unemployment, economic instability, lacks of urban facilities, unhygienic environmental conditions Geography, Utkal University, Vani Vihar, Bhubaneswar, etc. People were well aware about the importance of population studies from very beginning. Odisha, India Explosively growing of urban population has attracted the attention of urban geographers and town planners. For country like India, it is very important to study the decadal variation of population growth, it helps in realizing problems. The population growth and socio-economic changes are closely related to each other. In present study North 24 Parana’s has been chosen as study area. The level of urbanization remained high in the district (57.6 % in 2011). Rapid increase in urbanization can be attributed to growth of Kolkata metropolis.Barasat is now within greater Kolkata (Kolkata 124).From 1991 onwards the real estate business in this district thrived and projects were taken which are more of residential type than business type. The aim of the present paper is to investigate the change in urban population growth rate of municipality wise during the three decades 1981-91, 1991- 2001 and 2001-2011. Due to push-pull factors the rural-urban migration is causing the process of urbanization. -

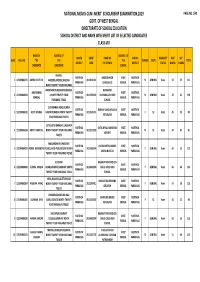

Page 1 of 8 LIST of CLINICAL ESTABLISHMENT (DIAGNOSTIC CENTRE), BARASAT SUB. DIV. NORTH 24 PARGANAS

Page 1 of 8 LIST OF CLINICAL ESTABLISHMENT (DIAGNOSTIC CENTRE), BARASAT SUB. DIV. NORTH 24 PARGANAS Last Sl Owner Facilities Name of Doctors Licence Revenue Name Address Phone No. Owners Name renewed No. Ph. No. Available on roll No. Collected upto Hospital Road, Sarkar X-Ray Clinic & Patho Lab Dr Debasish 1 Habra, North 24 253524 Sashim Sarkar, 5/56N 9.2.2008 Rs 1500 Clical Laboratory, Medium Majumder Parganas Patapatti, Kalibari, Eastern Clinical Patho Lab, 2 Habra, North 24 03216233212 Dr. R. Debnath 03216270412 Dr Ranjit Kr Debnath 12/71N 25.10.2005 Rs 500 Laboratory Medium Parganas Jessore Road, Champadali, Patho Lab 3 Gan Labarotary, 25622479 Ashim Gan 25622479 Dr K Chatterjee 36/25N 20.8.2005 Rs 500 Barasat, North 24 Medium Parganas Diagnostic Nabapally Colony Patho Lab Dr Manish 4 Laboratory & Chest More, Barasat, North 25524117 Aloka Mukherjee 25524117 115/23N 24.2.2006 Rs 250 Small Mukherjee Clinic, 24 Parganas 6, K.N.C. Raod, 1St Floor, Haritala, Dr. Ramesh Ch. 5 Health Care Centre, 25424479 25424479 Patho Lab DR G Mukherjee 101/N/130/P 16.5.2005 Rs 1750 Barasat, North 24 Saha, Parganas Barasat Cancer Banamapipur, Secretary Barasat Patho Lab 6 Research & Welfare Barasat, North 24 25622500 Cancer Research & 25522222 Dr Samir Roy 200/215/N 2.1.2006 Rs 1000 Medium Centre, Parganas Welfare Centre Chowmatha Badu Reliance Clinical Road, Patho Lab 7 25388155 Shiv Sankar Saha 25731834 Dr S R Chowdhury 249N/234 17.6.2005 Rs 500 Laboratory Madhyamgram, Small North 24 Parganas Bidhan Park, Dr A K Roy 8 Life Line Laboratory, Barasat, North 24 25521857 Chitali Mukherjee 25521930 Patho Small 258/273N 16.2.2006 Rs 375 Chowdhury Pargans Gobardanga Station Re-Life Diagonstic Patho Lab Dr A K Roy 9 Road, North 24 03216249885 Kalyan Samaddar 02316248569 299N/284 15.11.2005 Rs 500 Laboratory, Small Chowdhury Parganas Dolphin Medical 650/A/1 Ashoknagar, 03 Patho Lab Dr Kumud Ranjan 10 Smt. -

List of Municipalities Sl.No

LIST OF MUNICIPAL BODIES WHERE ELECTIONS WILL BE HELD IN THE MIDDLE OF 2010 SL.NO. DISTRICT NAME OF MUNICIPALITY 1 Cooch Behar Municipality 2 Tufanganj Municipality Cooch Behar 3 Dinhata Municipality 4 Mathabhanga Municipality 5 Jalpaiguri Jalpaiguri Municipality 6 English Bazar Municipality Malda 7 Old Malda Municipality 8 Murshidabad Municipality 9 Jiaganj-Azimganj Municipality 10 Kandi Municipality Murshidabad 11 Jangipur Municipality 12 Dhulian Municipality 13 Beldanga Municipality 14 Nabadwip Municipality 15 Santipur Municipality 16 Ranaghat Municipality 17Nadia Birnagar Municipality 18 Kalyani Municipality 19 Gayeshpur Municipality 20 Taherpur Municipality 21 Kanchrapara Municipality 22 Halishar Municipality 23 Naihati Municipality 24 Bhatpara Municipality 25North 24-Parganas Garulia Municipality 26 North Barrackkpore Municipality 27 Barrackpore Municipality 28 Titagarh Municipality 29 Khardah Municipality \\Mc-4\D\Munc. Elec-2010\LIST OF MUNICIPALITIES SL.NO. DISTRICT NAME OF MUNICIPALITY 30 Kamarhati Municipality 31 Baranagar Municipality 32 North Dum Dum Municipality 33 Bongaon Municipality 34 Gobardanga Municipality 35North 24-Parganas Barasat Municipality 36 Baduria Municipality 37 Basirhat Municipality 38 Taki Municipality 39 New Barrackpore Municipality 40 Ashokenagar-Kalyangarh Municipality 41 Bidhannagar Municipality 42 Budge Budge Municipality 43South 24-Parganas Baruipur Municipality 44 Jaynagar-Mazilpur Municipality 45 Howrah Bally Municipality 46 Hooghly-Chinsurah Municipality 47 Bansberia Municipality 48 Serampore Municipality 49 Baidyabati Municipality 50 Champadany Municipality 51 Bhadreswar Municipality Hooghly 52 Rishra Municipality 53 Konnagar Municipality 54 Arambagh Municipality 55 Uttarpara Kotrung Municipality 56 Tarakeswar Municipality 57 Chandernagar Municipal Corporation 58 Tamluk Municipality Purba Medinipur 59 Contai Municipality 60 Chandrakona Municipality 61 Ramjibanpur Municipality 62Paschim Medinipur Khirpai Municipality 63 Kharar Municipality 64 Khargapur Municipality 65 Ghatal Municipality \\Mc-4\D\Munc. -

Government of West Bengal Office of the Sub-Divisional Magistrate & Sub-Divisional Officer, Barrackpore, North 24 Parganas P

Government of West Bengal Office of the Sub-Divisional Magistrate & Sub-Divisional Officer, Barrackpore, North 24 Parganas Phone-033 2592 0616; Fax-033 2592 0814 e-mail: [email protected] ORDER In partial modification of this office Memo No. 167(9)/ConlBkp dated 04.02.2021 in connection with ensuing West Bengal Legislative Assembly General Election, 2021 the following officers are drafted as Assistant Returning Officer under 103 — Bizpur Assembly Constituency to 114-Dum Dum Assembly Constituency (copy enclosed). Sub-Divisional Magistrate & Sub-Divisional Officer Barrackpore, North 24 Parganas Memo No. /ConfBkp Date 20.02.2021 Copy forwarded for information to:- 1. The District Magistrate & District Election Officer, North 24 Parganas, Barasat 2. The Commissioner of Police, Barrackpore Police Commissionerate, Barrackpore 3. The Additional District Magistrate (General), North 24 Parganas, Barasat 4. The Returning Officer, Assembly Constituency 5. The Officer-in-Charge, Election, Barrackpore 6. The Officer-in-Charge, Training Cell, Barrackpore 7. The N.D.C., Barrackpore 8. The (Head of the Office) 9. Sri / Smt. , Assistant Returning Officer, Assembly Constituency Sub-Divisional Magistrate & Sub-Divisional Officer Barrackpore, North 24 Parganas List of AROs in connection with General Election to WBLA, 2021 AC No. & SI. Name of ARO Name No. Designation of ARO Mobile No. Senior Revenue Officer - II & Block Land & Land I AtanuDas 9903211705 Reforms Officer, Barrackpore - I Revenue Officer (1), Block Land & Land Reforms 2 SanjoyKumarDas 8582843535 Officer's Office, Barrackpore - 103 - Bijpur Revenue Officer (II), Block Land & Land Reforms 3 Subhashia Dasgupta 9851088820 Officer's Office, Barrackpore - 4 Santu Das C.D.P.O., ICDS, Kanchrapara 8927802757 8240454775 / 5 Sekh Kabir Ali Sub - Inspector of Schools, Bizpur Circle 8768788652 8336959188 I 1 Samit Sarkar, WBCS (Exe.) B.D.O., Barrackpore-1 7439311972 2 Gour Chandra Mandal 104 - Naihati it. -

Ist Cover Page-I-Ii.P65

DISTRICT HUMAN DEVELOPMENT REPORT NORTH 24 PARGANAS DEVELOPMENT & PLANNING DEPARTMENT GOVERNMENT OF WEST BENGAL District Human Development Report: North 24 Parganas © Development and Planning Department Government of West Bengal First Published February, 2010 All rights reserved. No part of this publication may be reproduced, stored or transmitted in any form or by any means without the prior permission from the Publisher. Front Cover Photograph: Women of SGSY group at work. Back Cover Photograph: Royal Bengal Tiger of the Sunderban. Published by : HDRCC Development & Planning Department Government of West Bengal Setting and Design By: Saraswaty Press Ltd. (Government of West Bengal Enterprise) 11 B.T. Road, Kolkata 700056 Printed by: Saraswaty Press Ltd. (Government of West Bengal Enterprise) 11 B.T. Road, Kolkata 700056 While every care has been taken to reproduce the accurate date, oversights/errors may occur. If found, please convey it to the Development and Planning Department, Government of West Bengal. Minister-in-Charge Department of Commerce & Industries, Industrial Reconstruction, Public Enterprises and Development & Planning GOVERNMENT OF WEST BENGAL E-mail : [email protected] Foreword It has been generally accepted since ancient times that welfare and well being of human is the ultimate goal of Human Development. An environment has to be created so that the people, who are at the centre of the churning process, are able to lead healthy and creative lives. With the publication of the West Bengal Human Development Report in 2004 and it being subsequently awarded by the UNDP for its dispassionate quality of analysis and richness in contents, we had to strive really hard to prepare the District Human Development Reports. -

Rainfall, North 24-Parganas

DISTRICT DISASTER MANAGEMENT PLAN 2016 - 17 NORTHNORTH 2424 PARGANASPARGANAS,, BARASATBARASAT MAP OF NORTH 24 PARGANAS DISTRICT DISASTER VULNERABILITY MAPS PUBLISHED BY GOVERNMENT OF INDIA SHOWING VULNERABILITY OF NORTH 24 PGS. DISTRICT TO NATURAL DISASTERS CONTENTS Sl. No. Subject Page No. 1. Foreword 2. Introduction & Objectives 3. District Profile 4. Disaster History of the District 5. Disaster vulnerability of the District 6. Why Disaster Management Plan 7. Control Room 8. Early Warnings 9. Rainfall 10. Communication Plan 11. Communication Plan at G.P. Level 12. Awareness 13. Mock Drill 14. Relief Godown 15. Flood Shelter 16. List of Flood Shelter 17. Cyclone Shelter (MPCS) 18. List of Helipad 19. List of Divers 20. List of Ambulance 21. List of Mechanized Boat 22. List of Saw Mill 23. Disaster Event-2015 24. Disaster Management Plan-Health Dept. 25. Disaster Management Plan-Food & Supply 26. Disaster Management Plan-ARD 27. Disaster Management Plan-Agriculture 28. Disaster Management Plan-Horticulture 29. Disaster Management Plan-PHE 30. Disaster Management Plan-Fisheries 31. Disaster Management Plan-Forest 32. Disaster Management Plan-W.B.S.E.D.C.L 33. Disaster Management Plan-Bidyadhari Drainage 34. Disaster Management Plan-Basirhat Irrigation FOREWORD The district, North 24-parganas, has been divided geographically into three parts, e.g. (a) vast reverine belt in the Southern part of Basirhat Sub-Divn. (Sundarban area), (b) the industrial belt of Barrackpore Sub-Division and (c) vast cultivating plain land in the Bongaon Sub-division and adjoining part of Barrackpore, Barasat & Northern part of Basirhat Sub-Divisions The drainage capabilities of the canals, rivers etc. -

BARASAT DMSION' PWD R^*O^. Rnoda Rovra Road

Public Works DePartment Government of West Bengal Notification No. 3p-37ll3l43l-R/pl- dated 11.08.2015.-ln exercise of the power conferred by Section 5 of the West as the said Act), the Governor is Bengal Highways Act, lg64 (west Ben. Act XXVIII of 1964) (hereinafter referred to of clause (d) of section 2 pleased hereby to appoint, with immediate effect, the Highway Authority within the meaning its length under under the Public of the said Act as mentioned in column (4) of Schedule below, in respect of road and (3), respectively, of the said works Department in North 24 parganas district as mentioned in column (2) and column Schedule, for the purposes of the said Act:- SCHEDULE NORTH 24 PARGANAS DISTRICT DMSION: BARASAT DMSION' PWD q0- Highway sl. Name of the Road oE Authority No. (4) I (3) 5.00 I Yol Road (0.00 40.00 2 ET Eloeirhqf I Road kmo to 40.00 km (40-00 6.40 .t Elooirhof I Rond kmn to 46.40 km pa\El 0.50 4 ith hnth side ). D.":"L"r ljosnqhed Rnad (0 00 kmn to 13.00 13.00 3.00 gasirhat Flasnabad Road (13.00 kmp to 16'00 kmp) t 18.00 7 R^*o^. Rnoda Rovra Road (0.00 kmp to 18.00 km 1 5.60 8 gonsron gugda Boyra Road (18.00 kmp to 33'60 km) 16.00 9 BonguonChakdah Ro@ l.60 0 Bonsaon Diagonal MuniciPal Road t.20 i) Executive I Bongaon Station Road Engineer, Barasat 2.07 2 Gachha to BOP Road Division r 0.00 13 C,qiohqlq Gnhnrdansn Road ii) Assistant 0.80 4 Hakimpur Bithari Road Engineers under 15.50 5 Hasnabad Hingalgani Road Barasat Division r.80 6 Hasnabad Takighat Road having t7.60 7 Helencha Sindhrani Duttafulia Road jurisdiction of the 33.60 8 Hinealeani Dulduli Hemnagar Road road. -

Seedling Morphology of Taki, North 24 Parganas, West Bengal

ISSN(Online): 2319-8753 ISSN (Print): 2347-6710 International Journal of Innovative Research in Science, Engineering and Technology (A High Impact Factor & UGC Approved Journal) Website: www.ijirset.com Vol. 6, Issue 8, August 2017 Seedling Morphology of Taki, North 24 Parganas, West Bengal S. Sanyal Department of Botany, Bethune College, Kolkata, West Bengal, India ABSTRACT: Seedling morphology was studied from different parts of Taki, North 24 Parganas, West Bengal. A total of 139 taxa was described and illustrated. Seedling morphological data are used as taxonomic markers in the systematic consideration of angiosperms. Using these characters, artificial key for the identification of taxa of different seedling groups has been developed which helps in the identification of plants at juvenile stage much earlier before flowering and fruiting stage. KEYWORDS: cotyledons, seedlings, morphology. I. INTRODUCTION Seedling characters are as important and reliable as that of floral one in the delimitation of species, genera and sometimes families. The characters of seedlings are limited in number, but their diversity is large and thus their assemblage serves the purpose of identification. Considerable works have been done on the seedling flora in tropical and temperate regions (Duke, 1965; Burger 1972; Muller, 1978; de Vogel, 1980; Ye, 1983; Hladik & Miquel, 1990; Welling, 2000), but in India, no work has been done on seedling flora, hence an attempt has been made on the proposed topic. Seedlings have mostly been classified into two main groups, based on the position of para(cotyledons) and whether or not the testa and fruit wall are shed. On germination, the majority of dicotyledons conform to two of several patterns of development. -

North 24 Parganas Merit List

NATIONAL MEANS‐CUM ‐MERIT SCHOLARSHIP EXAMINATION,2019 PAGE NO.1/49 GOVT. OF WEST BENGAL DIRECTORATE OF SCHOOL EDUCATION SCHOOL DISTRICT AND NAME WISE MERIT LIST OF SELECTED CANDIDATES CLASS‐VIII NAME OF ADDRESS OF ADDRESS OF QUOTA UDISE NAME OF SCHOOL DISABILITY MAT SAT SLNO ROLL NO. THE THE THE GENDER CASTE TOTAL DISTRICT CODE THE SCHOOL DISTRICT STATUS MARKS MARKS CANDIDATE CANDIDATE SCHOOL ASHARU‐ NORTH 24 AMDOBE HIGH WEST NORTH 24 1 123194806172 ABHRA KANTI PAL AMDOBE,AMDOBE,BAGDAH 19112011401 M GENERAL None 57 57 114 PARGANAS SCHOOL(H.S) BENGAL PARGANAS NORTH TWENTY FOUR PARGANAS NARAYANPUR,RUDRAPUR,BADURI RUDRAPUR ABU RAIHAN NORTH 24 WEST NORTH 24 2 123194804014 A NORTH TWENTY FOUR 19114700102 RADHABALLAV HIGH M GENERAL None 47 62 109 MANDAL PARGANAS BENGAL PARGANAS PARGANAS 743401 SCHOOL GOURBANGA ROAD,KUMRA NORTH 24 DAKHIN NANGLA BALIKA WEST NORTH 24 3 123194802181 ADITI BISWAS KASHIPUR,HABRA NORTH TWENTY 19110504301 F SC None 45 39 84 PARGANAS VIDYALAYA BENGAL PARGANAS FOUR PARGANAS 743271 SUTIA,SUTIA BARASAT,GAIGHATA NORTH 24 SUTIA B PALLI UNNAYAN WEST NORTH 24 4 123194806189 ADITYA MONDAL NORTH TWENTY FOUR PARGANAS 19112213503 M SC None 43 42 85 PARGANAS VIDYAPIT BENGAL PARGANAS 743273 MASLANDAPUR CHARGHAT NORTH 24 CHATRA NETAJI BALIKA WEST NORTH 24 5 123194804039 ADRIJA MAJUMDAR ROAD,GHOSHPUR,BADURIA NORTH 19111000504 F GENERAL None 60 53 113 PARGANAS SIKSHA NIKETAN BENGAL PARGANAS TWENTY FOUR PARGANAS 743289 K B DHAR BASIRHAT HARI MOHON NORTH 24 WEST NORTH 24 6 123194804040 ADRIKA SINGHA ROAD,BASIRHAT,BASIRHAT NORTH 19114600904 -

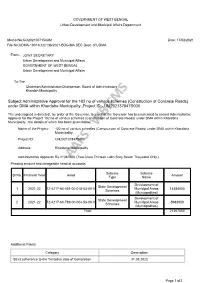

Subject:Administrative Approval for the 102 No of Various Schemes

GOVERNMENT OF WEST BENGAL Urban Development and Municipal Affairs Department Memo No:GO2021007154UM Date: 17/02/2021 File No:UDMA-13014(12)/136/2021-BDG-MA SEC-Dept. of UDMA From:- JOINT SECRETARY Urban Development and Municipal Affairs GOVERNMENT OF WEST BENGAL Urban Development and Municipal Affairs To:The Chairman/Administrator/Chairperson, Board of Administrators , Khardah Municipality Subject:Administrative Approval for the 102 no of various schemes (Construction of Concrete Roads) under DMA within Khardaha Municipality.,Project ID:- UM202137847S000 The undersigned is directed , by order of the Governor, to say that the Governor has been pleased to accord Administrative Approval for the Project 102 no of various schemes (Construction of Concrete Roads) under DMA within Khardaha Municipality. ,the details of which has been given below. Name of the Project: 102 no of various schemes (Construction of Concrete Roads) under DMA within Khardaha Municipality. Project ID: UM202137847S000 Address : Khardaha Municipality. Administrative Approval: Rs 21367000 (Two Crore Thirteen Lakh Sixty Seven Thousand Only.) Phasing amount and chargeable head of accounts Scheme Scheme Sl No. Financial Year Head Amount Type Name Development of State Development 1 2021-22 72-4217-60-051-00-018-53-00-V Municipal Areas 15384000 Schemes (Municipalities) Development of State Development 2 2021-22 72-4217-60-789-00-004-53-00-V Municipal Areas 5983000 Schemes (Municipalities) Total 21367000 Additional Points Category Description Strict adherence to the Tentative date of Completion 31.03.2022 Page 1 of 2 Additional Conditions Conditions Description 1 Strict observance of all relevant Financial Rules & Regulations including E-Tender Rules vides G.O. -

Details of Student 17-19

AL HERA COLLEGE OF EDUCATION (CODE-ERCAPP1485) Recognized by NCTE & Affiliated to WBUTTEPA Vill-Kodalia,P.O-Dakshin Bagundi,P.S-Basirhat,North 24 Parganas,West Bengal,Pin-743429 Student Details: Number of students course -wise; year -wise along with details: 2017 -19 Year of Admission Sl. Name Father’ s Address Category Year of Result Percent Contact Admission No. of the (Gen/SC/ Admission age No. / fee (Receipt student Name OBC/Others)ST/ mobile No., Date& admitte No. Amount) d 1 2 3 4 5 6 7 8 9 10 VIll -Taki P.O-Taki Ananya Dey P.S-Hasnabad 9501/30.06.17/ 1. Ananta Kr. Dey OBC-B 2017 8609417441 Dist- North 24 pgs Rs.30000.00 Pin-743429 West Bengal VIll-Patilachandra P.O-P.Madhyampur Mostafa Sardar P.S-Basirhat 9876/30.06.17/ 2. Chhurat Ali Sardar OBC-A 2017 8926716243 Dist- North 24 pgs Rs.20000.00 Pin-743429 West Bengal VIll-Patilachandra P.O-P.Madhyampur Rejaul Islam Gazi P.S-Basirhat 7101/30.06.17/ 3. Badel Gazi OBC-B 2017 8926720402 Dist- North 24 pgs Rs.40000.00 Pin- West Bengal VIll -Tokipur P.O-Tokipur Mallika Maity P.S-Hasnabad 7876/30.06.17/ 4. Asit Kr Maity GEN 2017 7602724442 Dist- North 24 pgs Rs.20000.00 Pin-743429 West Bengal VIll-Naihati P.O-Badartala Soumen Bandyopadhyay Late Gobinda P.S-Basirhat 7802/29.06.17/ 5. GEN 2017 9434686780 Bandyopadhyay Dist- North 24 pgs Rs.20000.00 Pin-743492 West Bengal VIll -Angnara P.O-South Kalibari Salma Khatun P.S-Hasnabad 8001/30.06.17/ 6. -

Khardaha Assembly West Bengal Factbook

Editor & Director Dr. R.K. Thukral Research Editor Dr. Shafeeq Rahman Compiled, Researched and Published by Datanet India Pvt. Ltd. D-100, 1st Floor, Okhla Industrial Area, Phase-I, New Delhi- 110020. Ph.: 91-11- 43580781, 26810964-65-66 Email : [email protected] Website : www.electionsinindia.com Online Book Store : www.datanetindia-ebooks.com Report No. : AFB/WB-109-0619 ISBN : 978-93-5293-708-0 First Edition : January, 2018 Third Updated Edition : June, 2019 Price : Rs. 11500/- US$ 310 © Datanet India Pvt. Ltd. All rights reserved. No part of this book may be reproduced, stored in a retrieval system or transmitted in any form or by any means, mechanical photocopying, photographing, scanning, recording or otherwise without the prior written permission of the publisher. Please refer to Disclaimer at page no. 155 for the use of this publication. Printed in India No. Particulars Page No. Introduction 1 Assembly Constituency at a Glance | Features of Assembly as per 1-2 Delimitation Commission of India (2008) Location and Political Maps 2 Location Map | Boundaries of Assembly Constituency in District | Boundaries 3-9 of Assembly Constituency under Parliamentary Constituency | Town, Ward & Village-wise Winner Parties- 2019, 2016, 2014, 2011 and 2009 Administrative Setup 3 District | Sub-district | Towns | Villages | Inhabited Villages | Uninhabited 10-12 Villages | Village Panchayat | Intermediate Panchayat Demographics 4 Population | Households | Rural/Urban Population | Towns, Ward and Villages 13-15 by Population Size |