The Coffee Exporter's Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Kosovo Commercial Guide

Kosovo Table of Contents Doing Business in Kosovo ____________________________ 6 Market Overview ___________________________________ 6 Market Challenges __________________________________ 7 Market Opportunities ________________________________ 8 Market Entry Strategy ________________________________ 9 Political and Economic Environment ____________________ 11 Selling US Products & Services ________________________ 11 Using an Agent to Sell US Products and Services _________________ 11 Establishing an Office ________________________________ 11 Franchising ______________________________________ 11 Direct Marketing ___________________________________ 12 Joint Ventures/Licensing ______________________________ 12 Selling to the Government ______________________________ 12 Distribution & Sales Channels____________________________ 13 Express Delivery ___________________________________ 13 Selling Factors & Techniques ____________________________ 13 eCommerce ______________________________________ 14 Overview ____________________________________________ 14 Current Market Trends ___________________________________ 14 Domestic eCommerce (B2C) ________________________________ 14 Cross-Border eCommerce __________________________________ 14 Online Payment________________________________________ 15 Major Buying Holidays ___________________________________ 15 Social Media __________________________________________ 15 Trade Promotion & Advertising ___________________________ 15 Pricing _________________________________________ 19 Sales Service/Customer -

No. 2138 BELGIUM, FRANCE, ITALY, LUXEMBOURG, NETHERLANDS

No. 2138 BELGIUM, FRANCE, ITALY, LUXEMBOURG, NETHERLANDS, NORWAY, SWEDEN and SWITZERLAND International Convention to facilitate the crossing of fron tiers for passengers and baggage carried by rail (with annex). Signed at Geneva, on 10 January 1952 Official texts: English and French. Registered ex officio on 1 April 1953. BELGIQUE, FRANCE, ITALIE, LUXEMBOURG, NORVÈGE, PAYS-BAS, SUÈDE et SUISSE Convention internationale pour faciliter le franchissement des frontières aux voyageurs et aux bagages transportés par voie ferrée (avec annexe). Signée à Genève, le 10 janvier 1952 Textes officiels anglais et français. Enregistrée d'office le l* r avril 1953. 4 United Nations — Treaty Series 1953 No. 2138. INTERNATIONAL CONVENTION1 TO FACILI TATE THE CROSSING OF FRONTIERS FOR PASSEN GERS AND BAGGAGE CARRIED BY RAIL. SIGNED AT GENEVA, ON 10 JANUARY 1952 The undersigned, duly authorized, Meeting at Geneva, under the auspices of the Economic Commission for Europe, For the purpose of facilitating the crossing of frontiers for passengers carried by rail, Have agreed as follows : CHAPTER I ESTABLISHMENT AND OPERATION OF FRONTIER STATIONS WHERE EXAMINATIONS ARE CARRIED OUT BY THE TWO ADJOINING COUNTRIES Article 1 1. On every railway line carrying a considerable volume of international traffic, which crosses the frontier between two adjoining countries, the competent authorities of those countries shall, wherever examination cannot be satisfactorily carried out while the trains are in motion, jointly examine the possibility of designating by agreement a station close to the frontier, at which shall be carried out the examinations required under the legislation of the two countries in respect of the entry and exit of passengers and their baggage. -

Hidden Cargo: a Cautionary Tale About Agroterrorism and the Safety of Imported Produce

HIDDEN CARGO: A CAUTIONARY TALE ABOUT AGROTERRORISM AND THE SAFETY OF IMPORTED PRODUCE 1. INTRODUCTION The attacks on the World Trade Center and the Pentagon on Septem ber 11, 2001 ("9/11") demonstrated to the United States ("U.S.") Gov ernment the U.S. is vulnerable to a wide range of potential terrorist at tacks. l The anthrax attacks that occurred immediately following the 9/11 attacks further demonstrated the vulnerability of the U.S. to biological attacks. 2 The U.S. Government was forced to accept its citizens were vulnerable to attacks within its own borders and the concern of almost every branch of government turned its focus toward reducing this vulner ability.3 Of the potential attacks that could occur, we should be the most concerned with biological attacks on our food supply. These attacks are relatively easy to initiate and can cause serious political and economic devastation within the victim nation. 4 Generally, acts of deliberate contamination of food with biological agents in a terrorist act are defined as "bioterrorism."5 The World Health Organization ("WHO") uses the term "food terrorism" which it defines as "an act or threat of deliberate contamination of food for human con- I Rona Hirschberg, John La Montagne & Anthony Fauci, Biomedical Research - An Integral Component of National Security, NEW ENGLAND JOURNAL OF MEDICINE (May 20,2004), at 2119, available at http://contenLnejrn.org/cgi/reprint/350/2112ll9.pdf (dis cussing the vulnerability of the U.S. to biological, chemical, nuclear, and radiological terrorist attacks). 2 Id.; Anthony Fauci, Biodefence on the Research Agenda, NATURE, Feb. -

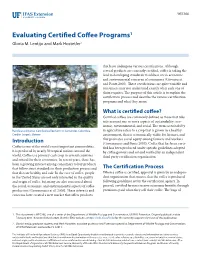

Evaluating Certified Coffee Programs1 Gloria M

WEC306 Evaluating Certified Coffee Programs1 Gloria M. Lentijo and Mark Hostetler2 that have undergone various certifications. Although several products are currently certified, coffee is taking the lead in developing standards to address socio-economic and environmental concerns of consumers (Giovanucci and Ponte 2005). These certifications are quite variable and consumers may not understand exactly what each one of them requires. The purpose of this article is to explain the certification process and describe the various certification programs and what they mean. What is certified coffee? Certified coffees are commonly defined as those that take into account one or more aspects of sustainability: eco- nomic, environmental, and social. The term sustainability Rainforest Alliance-Certified coffee farm in Santander, Colombia. in agriculture refers to a crop that is grown in a healthy Credits: Jorge E. Botero environment, that is economically viable for farmers, and Introduction that promotes social equity among farmers and workers (Giovannucci and Ponte 2005). Coffee that has been certi- Coffee is one of the world’s most important commodities. fied has been produced under specific guidelines adopted It is produced by nearly 50 tropical nations around the by coffee growers and set and verified by an independent world. Coffee is a primary cash crop in several countries third party certification organization. and critical for their economies. In recent years, there has been a growing interest among consumers to buy products that follow strict standards in their production process and The Certification Process that also are healthy and safe. In the case of coffee, people When a coffee is certified, approval is given by an indepen- in the United States are not only interested in the quality dent organization that ensures that the coffee is produced and origin of coffee, but many are also concerned about following guidelines set by the certification agency. -

The Harvest and Post-Harvest Management Practices' Impact On

Chapter The Harvest and Post-Harvest Management Practices’ Impact on Coffee Quality Mesfin Haile and Won Hee Kang Abstract Coffee is one of the most important agricultural commodities in the world. The coffee quality is associated with pre-harvest and post-harvest management activi- ties. Each step starting from selecting the best coffee variety for plantation until the final coffee drink preparation determines the cupping quality. The overall coffee quality influenced by the factors which involve in changes the physicochemical properties and sensorial attributes, including the post-harvest operations. The post- harvest processing activities contribute about 60% of the quality of green coffee beans. The post-harvest operations include pulping, processing, drying, hulling, cleaning, sorting, grading, storage, roasting, grinding, and cupping. This chapter comprises the harvest and post-harvest operations of coffee and their impacts on coffee quality. Keywords: digestive bioprocessing, coffee cherry, caramelization, Maillard reaction, speciality coffee 1. Introduction Coffee trees are widely grown in tropical and subtropical regions of Africa, Southeast Asia, and South America [1]. The world annual coffee production esti- mated 158.6 million 60-kg bags as of 2017/2018, up from 148.6 million 60-kg bags in 2014/2015. South America, Asia and Oceania, Mexico and Central America, and Africa produced as presented, respectively, 81.5, 47.7, 21.7, and 17.8 million 60-kg bags of coffee. The genus Coffea belongs to the Rubiaceae family and holds more than 90 different species. However, only Coffea arabica, Coffea canephora, and Coffea liberica are commercially important [1]. Arabica coffee accounts for about 64%, while C. -

In-Transit Cargo Crime Impacting the Retail Supply Chain

Journal of Transportation Management Volume 29 Issue 1 Article 4 7-1-2018 In-transit cargo crime impacting the retail supply chain John Tabor National Retail Systems, Inc. Follow this and additional works at: https://digitalcommons.wayne.edu/jotm Part of the Operations and Supply Chain Management Commons, and the Transportation Commons Recommended Citation Tabor, John. (2018). In-transit cargo crime impacting the retail supply chain. Journal of Transportation Management, 29(1), 27-34. doi: 10.22237/jotm/1530446580 This Article is brought to you for free and open access by the Open Access Journals at DigitalCommons@WayneState. It has been accepted for inclusion in Journal of Transportation Management by an authorized editor of DigitalCommons@WayneState. IN-TRANSIT CARGO CRIME IMPACTING THE RETAIL SUPPLY CHAIN John Tabor1 National Retail Systems, Inc. ABSTRACT Surveys of retail security directors show that almost half of those polled had been the victims of a supply- chain disruption directly related to cargo theft. This is a significant increase from just five years ago. In order to fully understand the issue of cargo theft, retailers need to know why it exists, who is perpetrating it, how risk can be reduced, and ultimately how to react to a loss. This article explores a number of dimensions of the issue, and offers several suggestions for mitigating the risk and dealing with theft after it occurs. INTRODUCTION That said, remember that virtually 100 percent of the merchandise in retail stores is delivered by truck. Surveys of retail security directors showed that In many cases the only two preventative measures almost half of those polled had been the victims of a put in place to secure that same merchandise in supply-chain disruption directly related to cargo transit is a key to the tractor and a seal on the rear theft. -

A Short History of Poland and Lithuania

A Short History of Poland and Lithuania Chapter 1. The Origin of the Polish Nation.................................3 Chapter 2. The Piast Dynasty...................................................4 Chapter 3. Lithuania until the Union with Poland.........................7 Chapter 4. The Personal Union of Poland and Lithuania under the Jagiellon Dynasty. ..................................................8 Chapter 5. The Full Union of Poland and Lithuania. ................... 11 Chapter 6. The Decline of Poland-Lithuania.............................. 13 Chapter 7. The Partitions of Poland-Lithuania : The Napoleonic Interlude............................................................. 16 Chapter 8. Divided Poland-Lithuania in the 19th Century. .......... 18 Chapter 9. The Early 20th Century : The First World War and The Revival of Poland and Lithuania. ............................. 21 Chapter 10. Independent Poland and Lithuania between the bTwo World Wars.......................................................... 25 Chapter 11. The Second World War. ......................................... 28 Appendix. Some Population Statistics..................................... 33 Map 1: Early Times ......................................................... 35 Map 2: Poland Lithuania in the 15th Century........................ 36 Map 3: The Partitions of Poland-Lithuania ........................... 38 Map 4: Modern North-east Europe ..................................... 40 1 Foreword. Poland and Lithuania have been linked together in this history because -

4.1 Potential Facilities List FY 17-18

FY 2017-2018 Annual Report Permittee Name: City of San José Appendix 4.1 FAC # SIC Code Facility Name St Num Dir St Name St Type St Sub Type St Sub Num 820 7513 Ryder Truck Rental A 2481 O'Toole Ave 825 3471 Du All Anodizing Company A 730 Chestnut St 831 2835 BD Biosciences A 2350 Qume Dr 840 4111 Santa Clara Valley Transportation Authority Chaboya Division A 2240 S 7th St 841 5093 Santa Clara Valley Transportation Authority - Cerone Division A 3990 Zanker Rd 849 5531 B & A Friction Materials, Inc. A 1164 Old Bayshore Hwy 853 3674 Universal Semiconductor A 1925 Zanker Rd 871 5511 Mercedes- Benz of Stevens Creek A 4500 Stevens Creek Blvd 877 7542 A.J. Auto Detailing, Inc. A 702 Coleman Ave 912 2038 Eggo Company A 475 Eggo Way 914 3672 Sanmina Corp Plant I A 2101 O'Toole Ave 924 2084 J. Lohr Winery A 1000 Lenzen Ave 926 3471 Applied Anodize, Inc. A 622 Charcot Ave Suite 933 3471 University Plating A 650 University Ave 945 3679 M-Pulse Microwave, Inc. A 576 Charcot Ave 959 3672 Sanmina Corp Plant II A 2068 Bering Dr 972 7549 San Jose Auto Steam Cleaning A 32 Stockton Ave 977 2819 Hill Bros. Chemical Co. A 410 Charcot Ave 991 3471 Quality Plating, Inc. A 1680 Almaden Expy Suite 1029 4231 Specialty Truck Parts Inc. A 1605 Industrial Ave 1044 2082 Gordon Biersch Brewing Company, Inc. A 357 E Taylor St 1065 2013 Mohawk Packing, Div. of John Morrell A 1660 Old Bayshore Hwy 1067 5093 GreenWaste Recovery, Inc. -

155158452006.Pdf

Revista de Administração de Empresas ISSN: 0034-7590 ISSN: 2178-938X Fundação Getulio Vargas, Escola de Administração de Empresas de S.Paulo BOAVENTURA, PATRICIA SILVA MONTEIRO; ABDALLA, CARLA CAIRES; ARAÚJO, CECILIA LOBO; ARAKELIAN, JOSÉ SARKIS VALUE CO-CREATION IN THE SPECIALTY COFFEE VALUE CHAIN: THE THIRD-WAVE COFFEE MOVEMENT Revista de Administração de Empresas, vol. 58, no. 3, 2018, May-June, pp. 254-266 Fundação Getulio Vargas, Escola de Administração de Empresas de S.Paulo DOI: https://doi.org/10.1590/S0034-759020180306 Available in: https://www.redalyc.org/articulo.oa?id=155158452006 How to cite Complete issue Scientific Information System Redalyc More information about this article Network of Scientific Journals from Latin America and the Caribbean, Spain and Journal's webpage in redalyc.org Portugal Project academic non-profit, developed under the open access initiative RAE-Revista de Administração de Empresas (Journal of Business Management) FORUM Submitted 07.31.2017. Approved 12.26.2017 Evaluated through a double-blind review process. Guest Scientific Editors: Marina Heck, Jeffrey Pilcher, Krishnendu Ray, and Eliane Brito Original version DOI: http://dx.doi.org/10.1590/S0034-759020180306 VALUE CO-CREATION IN THE SPECIALTY COFFEE VALUE CHAIN: THE THIRD-WAVE COFFEE MOVEMENT Cocriação de valor na cadeia do café especial: O movimento da terceira onda do café Cocreación de valor en la cadena del café especial: El movimiento de la tercera ola del café ABSTRACT Brazil represents approximately 29% of the world’s coffee exports, with 15% of that being “specialty coffee.” Most Brazilian coffee exports are composed of commoditized green beans, influencing the value chain to be grounded on an exchange paradigm. -

Autopsies in Norway and Czech Republic

CHARLES UNIVERSITY IN PRAGUE THIRD FACULTY OF MEDICINE Astrid Teigland Autopsies in Norway and Czech Republic: A comparison A look at international tendencies concerning autopsy rates, and whether these have had any impact regarding autopsy as a means of a retrospective diagnostic tool Diploma thesis 1 Prague, August 2010 Author of diploma thesis: astrid Teigland Master's programme of study Advisor of the thesis: : MUDr. Adamek Department of the advisor of the thesis: Forensic Dpt., FNKV Prague Date and year of defence: august 2010 2 Written Declaration I declare that I completed the submitted work individually and only used the mentioned sources and literature. Concurrently, I give my permission for this diploma/bachelor thesis to be used for study purposes. Prague, 29.03.10 Astrid Teigland 3 Contents Contents............................................................................................................................................4 Introduction ..................................................................................Chyba! Záložka není definována. DEFINITION AND DESCRIPTION..............................................................................................7 NATIONAL REGULATions concerning autopsies....................................................8 CAUSES OF DEATH - NORWAY VS. CZECH REPUBLIC...................................................11 DISCUSSION……………………………………………………………………………………..14 The value of the autopsy…………………………………………………………………………15 Are autopsies still necessary?........................................................................................................18 -

Starmaya: the First Arabica F1 Coffee Hybrid Produced Using Genetic Male Sterility

METHODS published: 22 October 2019 doi: 10.3389/fpls.2019.01344 Starmaya: The First Arabica F1 Coffee Hybrid Produced Using Genetic Male Sterility Frédéric Georget 1,2*, Lison Marie 1,2, Edgardo Alpizar 3, Philippe Courtel 3, Mélanie Bordeaux 4, Jose Martin Hidalgo 4, Pierre Marraccini 1,2, Jean-christophe Breitler 1,2, Eveline Déchamp 1,2, Clément Poncon 3, Hervé Etienne 1,2 and Benoit Bertrand 1,2 1 CIRAD, UMR IPME, Montpellier, France, 2 IPME, Université de Montpellier, IRD, CIRAD, Montpellier, France, 3 Plant material, ECOM, Exportadora Atlantic, Managua, Nicaragua, 4 FONDATION NICAFRANCE, Managua, Nicaragua In the present paper, we evaluated the implementation of a seed production system based on the exploitation of male sterility on coffee. We studied specifically the combination between CIR-SM01 and Marsellesa® (a Sarchimor line), which provides a hybrid population called Starmaya. We demonstrated that the establishment of seed garden under natural pollination is possible and produces a sufficient amount of hybrid seeds to be multiplied efficiently and economically. As expected for F1 hybrid, the performances of Starmaya are highly superior to conventional cultivars. However, we observed some heterogeneity on Starmaya cultivar Edited by: in the field. We confirmed by genetic marker analysis that the off-types were partly related to Marcelino Perez De La Vega, Universidad de León, Spain the heterozygosity of the CIR-SM01 clone and could not be modified. Regarding the level Reviewed by: of rust resistance of Starmaya cv., we saw that it could be improved if Marsellesa was more Aaron P. Davis, fully fixed genetically. If so, we should be able to decrease significantly the percentage of rust Royal Botanic Gardens, Kew, United Kingdom incidence of Starmaya from 15 to 5%, which would be quite acceptable at a commercial Eveline Teixeira Caixeta, level. -

Coffee Economic Fact Sheet# 2 July 1989

Coffee Economic Fact Sheet# 2 July 1989 Department of Agricultural and Resource Economics College of Tropical Agriculture and Human Resources University of Hawaii By ·Kevin M. Yokoyama, Stuart T. Nakamoto, and Kulavit Wanitprapha CROP PROFILE ac, respectively. Hawaii's was substantially SPECIES higher at 1166 lb/ac. Exceptional yields of 2682 lb/ac or more have been obtained in Hawaii, • Over 70% of the world coffee supply is arabica from advanced plantations in Brazil, and in the coffee (Coffea arabica), slightly more than 20% People's Democratic Republic of Yemen. is robusta coffee (C. canephora), and the rest is from C. liberica and C. excelsa and other species. • For every 100 lb of clean, dried, unroasted coffee beans, 500 to 600 lb of coffee berries are needed. • All high-quality (specialty) coffees come from C. Unroasted coffee beans can be stored up to three arabica, but quality is affected by the processing years without a noticeable loss in quality. method. Examples are Jamaican Blue Moun tain coffee and Kon a coffee, both of which are se USES AND PRODUCTS lectively picked when ripe, then processed by the wet method. Brazilian coffee also comes • Coffee beans can be roasted, ground, and brewed. from C. arabica. This coffee is mass-harvested In the Middle East, roasted coffee is ground into by strip-picking the coffee berries at various a powder, boiled several times, and sweetened stages of development and is processed by the with sugar to produce a small cup heavy with dry method, resulting in a lower quality coffee. sediment. In southern Europe and Latin Amer ica, coffee is dark-roasted, nearly burned, and • Robusta coffee does not possess the aroma or bitter.