Cfao (Ghana) Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2017 Annual Report and Financial Statements

2017 ANNUAL REPORT AND FINANCIAL STATEMENTS 2017 ANNUAL REPORT AND FINANCIAL STATEMENTS SAS FORTUNE FUND LIMITED 3 SAS FORTUNE FUND LIMITED CORPORATE INFORMATION The Manager: SAS Investment Management Ltd. (SAS-IM) 14th Floor WTCA Building, Indep. Avenue, Accra Tel: +233-302-661770/2/008/880 +233-302-661900 Fax: +233-302-663999 E-mail: [email protected] Website: www.sasghana.com Directors of the Fund: Maxwell Logan (Chairman) Togbe Afede XIV Apiigy Afenu (Removed on 6th July 2017) Nana Soglo Alloh (Removed on 6th July 2017) Paul Hammond The Custodian: Standard Chartered Securities Services Head Office P. O. Box 768 Accra Independent Auditors: Nexia Debrah & Co. (Chartered Accountants) BCB Legacy House # 1 Nii Amugi Avenue East Adabraka, Accra P. O. Box CT 1552 Cantonments, Accra Solicitors: R. S. Agbenoto and Associates 4th Floor Total House 25 Liberia Road Secretary: Accra Nominees Cedar House No. 13 Samora Machel Road Asylum Down, Accra 4 CONTENTS Corporate Information 4 Chairman’s Report 8-9 Fund Manager’s Report 10-15 Report of the Directors 16-17 Report of the Auditors 18-21 Statement of Investment Assets 22-23 Statement of Comprehensive Income 24 Statement of Financial Position 25 Statement of Cash Flows 26 Portfolio Summary 28 SAS Notes to the Financial Statements 29-37 FORTUNE FUND REPORT Report of the Custodian 38-40 Information on Directors 41 AND FINANCIAL STATEMENTS 5 SAS FORTUNE FUND LIMITED NOTICE OF MEETING NOTICE is hereby given that the 13th Annual General Meeting of the Members of the SAS Fortune Fund will be held on Thursday July 26, 2018 at the British Council Hall, Liberia Road, Accra at 12.30 p.m. -

Has Gse Played Its Role in the Economic Development of Ghana?

CAPITAL MARKET 23 YEARS AND COUNTING: HAS GSE PLAYED ITS ROLE IN THE ECONOMIC DEVELOPMENT OF GHANA? 1st CAPITAL MARKET CONFERENCE BY EKOW AFEDZIE, DEPUTY MANAGING DIRECTOR MAY 10, 2013 INTRODUCTION Ghana Stock Exchange (GSE) was established with a Vision: -To be a relevant, significant, effective and efficient instrument in mobilizing and allocating long-term capital for Ghana’s economic development and growth. INTRODUCTION OBJECTIVES - To facilitate the Mobilization of long term capital by Corporate Bodies/Business and Government through the issuance of securities (shares, bonds, etc). - To provide a Platform for the trading of issued securities. MEMBERSHIP OF GHANA STOCK EXCHANGE GSE as a public company limited by Guarantee has No OWNERS OR SHAREHOLDERS. GSE has Members who are either corporate or individuals. There are two categories of members:- - Licensed Dealing Members - 20 - Associate Members - 34 HISTORICAL BACKGROUND 1968 - Pearl report by Commonwealth Development Finance Co. Ltd. recommended the establishment of a Stock Exchange in Ghana within two years and suggested ways of achieving it. 1970 – 1989 - Various committees established by different governments to explore ways of bringing into being a Stock Exchange in the country. HISTORICAL BACKGROUND 1971 - The Stock Exchange Act was enacted. - The Accra Stock Exchange Company incorporated but never operated. Feb, 1989 - PNDC government set up a 10-member National Committee on the establishment of Stock Exchange under the chairmanship of Dr. G.K. Agama, the then Governor of the Bank of Ghana. HISTORICAL BACKGROUND July, 1989 - Ghana Stock Exchange was incorporated as a private company limited by guarantee under the Companies Code, 1963. HISTORICAL BACKGROUND Nov. -

Aluworks Annual Report

ALUWORKS LIMITED ANNUAL REPORT AND FINANCIAL STATEMENTS 31ST DECEMBER 2018 ALUWORKS LIMITED CONTENTS. Notice of Annual General Meeting 3 Corporate Information 4 Directors Gallery and Profiles 5 Corporate Governance 8 Chairman’s Statement 9 Quality Assurance Policy 13 Management Gallery 14 Financial Highlights 15 Report of the Directors 16 Independent Auditor’s Report 23 Statement of Financial Position 27 Statement of Comprehensive Income 28 Statement of Changes in Equity 29 Statement of Cash Flows 30 Notes to the Financial Statements 31 Shareholders Information Appendix 72 Corporate Social Responsibility Appendix 73 Proxy Form 79 Page 2 2018 Aluworks Limited Annual Report ALUWORKSALUWORKS LIMITEDLIMITED CONTENTS. Notice of Annual General Meeting 3 Corporate Information 4 Directors Gallery and Profiles 5 Corporate Governance 8 Chairman‟s Statement 9 Quality Assurance Policy 12 Management Gallery 13 Financial Highlights 14 Report of the Directors 15 Independent Auditor‟s Report 20 By Order Of the Board Statement of Financial Position 24 Statement of Comprehensive Income 25 Statement of Changes in Equity 26 Statement of Cash Flows 27 Notes to the Financial Statements ACCRA28 NOMINEES LIMITED COMPANY SECRETARIES Note:Shareholders Information Appendix 58 A member of the company entitled to attend and vote may appoint a proxy to attend and vote in his/her stead. A proxy need not be a member of the company. Completed proxy forms should beCorporate deposited atSocial the offices Responsibility of the Registrars Appendix Universal Merchant Bank 59Limited, 123 Kwame Nkrumah Avenue, Sethi Plaza, Adabraka, Accra, P. O. Box GP401, Accra not less than 48 hours beforeProxy the Form appointed time of the meeting. -

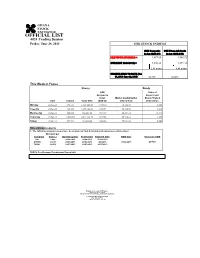

OFFICIAL LIST 4024 Trading Session Friday, June 28, 2013 GSE STOCK INDICES

OFFICIAL LIST 4024 Trading Session Friday, June 28, 2013 GSE STOCK INDICES GSE Composite GSE Financial Stocks Index (GSE-CI) Index (GSE-FSI) PREVIOUS 27/06/2013) = 1,877.65 1,585.72 CURRENT 28/06/2013) = 1,880.26 1,591.18 2.61 points 5.46 points CHANGE-YEAR TO DATE (Jan 01, 2013- June 28, 2013) 56.72% 53.02% This Week in Focus Shares Bonds GSE Value of Composite Government Index Market Capitalization Bonds Traded Date Volume Value GH¢ (GSE-CI) GH¢ million GH¢ million Monday 24-Jun-13 493,511 1,581,041.68 1,900.10 56,154.80 0.000 Tuesday 25-Jun-13 426,550 1,196,438.69 1,891.94 56,110.32 1.240 Wednesday 26-Jun-13 880,088 966,256.30 1,874.67 55,894.32 15.743 Thursday 27-Jun-13 1,553,869 2,844,118.70 1,877.65 55,910.61 4.295 Friday 28-Jun-13 251,546 482,820.80 1,880.26 55,924.82 0.000 Notes/Announcements 1. The following announcements have been made on final dividends and annual general meetings: Dividend per Company Share ¢ Qualifying Date Ex-Div Date Payment Date AGM Date Venue for AGM CAL 0.006 26/06/2013 24/06/2013 30/08/2013 AYRTN 0.0013 25/06/2013 21/06/2013 8/8/2013 27/06/2013 OEPCH TOTAL 0.6900 18/07/2013 16/07/2013 26/07/2013 GCPS:GhanaAICC: Accra International College of Physicians Conference and Centre Surgeons OEPCH:Osu Ebenezer Presbyterian Church HalL Enquiries to: General Manager Ghana Stock Exchange 5th & 6th Floors Cedi House, Liberia Road, Accra Tel: 021 669908, 669914, 669935 Fax: 021 669913 e-mail: [email protected] OFFICIAL LIST 4024 Trading Session ODD LOT Friday, June 28, 2013 ISIN Share Code Total Shares No. -

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 8th January, 2015 STOCK MARKET ACCRA BOURSE MAKES PROMISING START INDICATORS WEEK OPEN WEEK END CHANGE The year 2014 has begun living up to expectations as bullish runs in equities from the petroleum, finance and consumer Market Capitalization (GH¢ goods sectors saw the annual returns of the broader market 'million) 64,352.42 64,229.12 -0.19% Market Capitalization (US$' inch up to 0.42% last Thursday. Though, most equities gave million) 20,109.50 20,014.06 -0.47% up their opening prices, rise in the market value of Ghana Oil Petroleum Company Limited (GOIL), Societe Generale Ghana Volume traded (shares) 783,118.00 573,274.00 -26.80% Table 1: Market Summary Limited (GOIL) and Fan Milk Limited (FML) were enough to close the week’s activities on a positive note. Key benchmark indices closed the week better despite slight volatilities during inter-day trading. The GSE Composite INDEX ANALYSIS index closed at a year-to-date return of 0.42% whiles the GSE Financial Stocks Index settled at 0.67% returns. INDICATORS Closing Week YTD Level Change CHANGE Total market capitalization of the Ghana Stock Exchange was GH¢64.23 billion, an equivalent to USD20.00 billion. GSE Composite Index 2,270.57 0.42% 0.42% GSE Financial Stocks Index 2,258.77 0.67% 0.67% Table 2: Key Stock Market Indices LIQUIDITY The absence of block trades over the period saw liquidity comparatively down last week. All in all, an approximate figure of 573,274 shares exchanged hands within the first trading week of the year, and was also valued about GH¢2.48 million. -

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 14th September, 2017 Address: No. 67A & B Switchback Road, Email: [email protected] Website: www.sic-fsl.com Phone: +233-302-767-051 +233-302-767-123 STOCK MARKET PROFIT-TAKING SLOWS MARKET PERFORMANCE Intense profit-taking on the Ghana Stock Exchange (GSE) INDICATORS WEEK OPEN WEEK END CHANGE saw key performance indicators dip for the first time in Market Capitalization several weeks. Among the nine (9) price movers, five (5) (GH¢'million) 58,810.32 58,022.89 -1.34% equities were ticked-down while the rest gained. Among the Market Capitalization (US$'million) 13,359.91 13,171.45 -1.41% laggards, shares of Standard Chartered Bank Limited (SCB), GCB Bank Limited (GCB), Enterprise Group Limited (EGL) Volume traded (shares) 1,090,896.00 3,860,498.00 253.88% and Trust Bank Gambia Limited (TBL) were the hardest hit on Value Traded (GH¢) 7,134,447.86 9,038,209.20 26.68% the bourse last week. Value Traded (US$) 1,620,728.73 2,051,713.70 26.59% At the close of activities last Thursday yields on the GSE- Table 1: Market Summary Composite Index (GSE-CI), the GSE Financial Stocks Index (GSE-FSI) and the SIC-FSL Top 15 liquid Index (T-15 Index) declined from their previous week year-to-date gains of INDEX ANALYSIS 44.73%, 42.91% and 52.92% to settle at annual returns of 37.08%, 31.38% and 45.33% respectively. INDICATORS Closing Week YTD Level Change CHANGE Total market capitalization dipped from the previous week’s GSE Composite Index 2,315.48 -5.28% 37.08% figure of GH¢58.81 billion to GH¢58.02 billion. -

5Th Ghana CEO Summit Magazine

ADVERT 1 Programme 09:30 – 11:00AM. SESSION ONE – KEYNOTE SPEECHES The 5th Ghana CEO Summit - Programme Outline – MONDAY 17TH –TEUSDAY 18TH MAY 2021 09:30 – 11:00AM. SESSION ONE – KEYNOTE SPEECHES Day 1 - MONDAY 17TH 09:30 – 11:00AM. SESSION ONE – KEYNOTE SPEECHES Expert Insight: Dr. Bright C. Mawudor PHD, Practice Lead, Managed Security Services & Consulting (MEA), Intelligent Security, Dimension Data. Topic - C-Level Engagement in Building Organizational Cyber Resilience in the Covid-19 Era Keynote Speaker I: Dr. K. K. Sarpong, CEO, GNPC. Topic: Digital Transformation: Resetting the Corporate Governance Agenda for a Post-Pandemic Economic Resilience Keynote Speaker II: Mr. Emmanuel Antwi-Darkwa, Chief Executive, Volta River Authority (VRA). Topic – “Powering Ghana’s Digital Agenda with Clean & Sustainable Energy”. SIGA Statement: Hon. Stephen Asamoah Boateng, Director General, State interests and Governance Authority (SIGA). Speech – Mr. Kofi Adomakoh, CEO, GCB Bank. Presentation - Mr. Enoch Entsua-Mansah, CEO, Eris Properties. Keynote Speaker III: Mr. Moses Baiden Jnr, CEO, Margins Group. Topic - The Power of Digital Identities in Resetting Ghana’s Economy. PFABG Keynote Speaker IV: Dr. Maxwell Opoku-Afari, First Deputy Governor, Bank of Ghana. Topic - Resetting Ghana’s Economy: Policy response & Strategies for building a resilient Economy Post-Covid pandemic. Sponsor Presentations and Videos Co ee Break & Networking. 11:00AM – 12 NOON. SESSION TWO – SUMMIT OPENING & PRESIDENTIAL DIALOGUE 5TH GHANA CEO SUMMIT SPEECH: Mr. Ernest De-Graft Egyir CEO, Chief Executives Network Ghana. PRESIDENTIAL SPEECH BY H. E. PRESIDENT NANA AKUFO-ADDO. The President Of The Republic Of Ghana. The Special Guest Of Honour. OFFICIAL OPENING OF THE 5TH GHANA CEO SUMMIT, CORPORATE EXHIBITION, GROUP PHOTOGRAPH & DIALOGUE WITH THE PRESIDENT OF THE REPUBLIC OF GHANA. -

The Republic of Ghana the Africa Country Series

2016 The Africa Country Series The Republic Of Ghana The Africa Country Series The Republic Of Ghana May 2016 Acknowledgements Team Leader: Samir S. Amir Lead Researcher: Falak Hadi Disclaimer The findings, interpretations and conclusions expressed herein do not necessarily reflect the views of the Board of Directors and Members of the Pakistan Business Council or the companies they represent. Any conclusions of analysis based on ITC, IDB, CTS, UNCTSD and WTO data are the responsibility of the author(s) and do not necessarily reflect the opinion of the WTO, IMF or UN. Although every effort has been made to cross-check and verify the authenticity of the data, the Pakistan Business Council, or the author(s) do not guarantee the data included in this work. All data and statistics used are correct as of 28th February 2016, and may be subject to change. Unless otherwise stated, all monetary amounts are given in USD (millions). For any queries or feedback regarding this report, please contact [email protected] or falak@ pbc.org.pk ii The Republic of Ghana The Pakistan Business Council: An Overview The Pakistan Business Council (PBC) is a business policy advocacy forum, representing private- sector businesses that have substantial investments in Pakistan’s economy. It was formed in 2005 by 14 (now 52) of Pakistan’s largest enterprises, including multinationals, to allow businesses to meaningfully interact with government and other stakeholders. The Pakistan Business Council is a pan-industry advocacy group. It is not a trade body nor does it advocate for any specific business sector. -

Registration Document 2014

EQUIPMENT HEALTHCARE CONSUMER GOODS Registration Document 2014 Société anonyme (French Joint-stock company) with a Supervisory Board and a Management Board With share capital of €10,459,512 Head office: 18, Rue Troyon, 92316 Sèvres, France Registered in the Nanterre Trade and Companies Registry Under number 552 056 152 REGISTRATION DOCUMENT including the annual financial report 2014 This document is a free translation into English of CFAO’s original Document de Référence (hereinafter referred to as the “Registration Document”), which was prepared in French and filed with the French financial markets authority (Autorité des marchés financiers – AMF) on April 20 , 2015 , in accordance with Article 212-13 of the AMF’s General Regulations. Only the French version of this Registration Document is legally binding. The French Registration Document may be used in the context of a financial transaction only if it is accompanied by a securities Note approved by the AMF. It was prepared by the issuer and its signatories therefore assume responsibility for its content. Copies of this English translation of the French Registration Document are available at CFAO’s registered office: 18, Rue Troyon, 92316 Sèvres, France. This document may also be consulted on the website of the AMF (www.amf-france.org) and on the website of CFAO (www.cfaogroup.com). REGISTRATION DOCUMENT 2014 - CFAO 1 General General This Registration Document also includes: ■ the annual management report of the Company’s Management Board, which must be submitted to the shareholders’ Meeting ■ the annual financial report that must be prepared and published called to approve the financial statements for each fiscal by all listed companies within four months following the end of year, pursuant to Articles L. -

CONFERENCE PROCEEDINGS Editors: Dr

UNIVERSITY OF GHANA BUSINESS SCHOOL CONFERENCE PROCEEDINGS editors: Dr. Richard Boateng, Dr. Mohammed A. Sanda, Dr. Godfred A. Bokpin, Dr. Adelaide Kastner and Mr. Francis Adzei UNIVERSITY OF GHANA BUSINESS SCHOOL UGBS CONFERENCE ON BUSINESS AND DEVELOPMENT 2013 This book of proceedings features a mix of conceptual and empirical research papers which set the agenda for discussion on key themes in accounting; finance, banking & insurance; marketing and customer management; operations and management information systems; organisation and human resource management; and public administration and health services management. Published 2013 in Ghana by University of Ghana Business School (UGBS) Copyright © 2013 UGBS. All Rights Reserved. ISBN: xxx-xxxx-x-xxxx-x All rights reserved. Published by University of Ghana Business School (UGBS) P. O. Box LG 78 Legon, Accra, Ghana Tel: +233 302 501008 Email: [email protected] Printed in Ghana by UGBS in collaboration with Craft Concepts Limited P. O. Box NB 649, Nii Boiman, Accra, Ghana Tel: +233-302-925-762 Email: [email protected] Copyright©2013 Internet Version (30 April 2013) The Internet version of this document can be accessed at: http://ugbs.ug.edu.gh/ UGBS Conference on Business and Development – Conference Proceedings Contents Contents ................................................................................................................................................................. 1 Conference Welcome ............................................................................................................................................ -

WEEKLY MARKET REVIEW 25 June 2018

DATABANK RESEARCH WEEKLY MARKET REVIEW 25 June 2018 ANALYST CERTIFICATE & REQUIRED DISCLOSURE BEGINS ON PAGE 4 GSE MARKET STATISTICS SUMMARY Current Previous % Change Weekly Market Update Databank Stock Index 36,989.82 37,829.75 -2.22% The equities market ended the week with reducing year to date GSE-CI Level 2,918.27 2,989.68 -2.39% returns of 13.12% for the GSE’s Composite Index and 12.49% for Market Cap (GH¢ m) 58,718.96 62,501.44 -6.05% the Databank Stock Index. YTD Return DSI 12.49% 15.04% YTD Return GSE-CI 13.12% 15.89% The gainers this week were ACCESS (+17.65% GH¢4.00), ETI Weekly Volume Traded (Shares) 7,111,051 3,728,037 90.75% (+5.00%, 21Gp) and GOIL (+1.27% GH¢4.00). Weekly Turnover (GH¢) 10,906,829 1,946,907 460.21% The laggards were CAL (-2.40% GH¢1.22), EGH (-11.76% Avg. Daily Volume Traded 878,468 854,409 2.82% (Shares) GH¢9.00), GCB (-0.39% GH¢5.15), SCB (-0.66% GH¢27.15), TLW Avg. Daily Value Traded (GH¢) 3,788,144 3,859,240 -1.84% (-15.00% GH¢14.56), SOGEGH (-17.58%, GH¢1.36) and Total (- No. of Counters Traded 20 20 1.23%, GH¢4.00). No. of Gainers 3 5 A total of ~7.11 million shares valued at ~GH¢10.9 million were No. of Laggards 7 11 traded on the Ghana Stock Exchange this week. Outlook KEY ECONOMIC INDICATORS Fixed Income Market Current Previous Change We anticipate lackluster activity on the Ghana Stock Exchange 91-Day Treasury Bill 13.34% 13.30% +4bps next week with a price gain in Unilever Ghana. -

Ms. Dinah Glover (GM, Management Control - Toyota Ghana Company Limited) HR Metrics; Staying Accountable

HUMAN RESOURCE MAGAZINE Free Quarterly Magazine Q4 2016 Ms. Dinah Glover (GM, Management Control - Toyota Ghana Company Limited) HR Metrics; Staying Accountable Theme Story Personality Spotlight HR Metrics; Ms. Dinah Glover Staying Accountable (GM, Management Control - Toyota Ghana Company Limited) Article How Not to Go Broke Event Spotlight after Christmas HR Focus Conference 2016 We live for HR Solutions Ask L’AINE FOR STREAMLINED TRAINING SOLUTIONS Recruitment L’AINE has TRAINING solutions that provide Tel: 0302 716986/ 716983/ 717039 Outsourcing Email: [email protected] Training managers like Yaaba with improved sta www.lainejobs.com Payroll Services www.laineservices.com Career Guidance performance. Wondering how? ASK L’AINE www.hrfocusmagazine.com Organisational Development 3 CONTENT 17-18 20-21 20 -21 5 - 7 9 16 - 17 NEWS ARTICLE: SPOTLIGHT: My Expectations as an NSP Ms. Dinah Glover 10 -11 Toyota Ghana Limited 20 - 21 22 - 23 24 - 25 EVENT SPOTLIGHT: ONLINE SURVEY: PRODUCT SPOTLIGHT: 10 - 11 HR Focus Conference 2016 Top 5 Companies to Work CFAO - Mitsubishi Pajero Sports is THEME STORY: for in Ghana the New Baby in Town! HR Metrics: Staying Accountable 27 29 32 - 33 37 FINANCE COLUMN: HEALTH COLUMN: HR COLUMN: TESTIMONIALS: Demystifying Planning, Cheers to a Healthy HR Audit; What our Readers Forecasting & Budgeting Christmas A Strategic Intervention are Saying PUBLISHING CREDITS Publishing House - Focus Digital TO ADVERTISE Contact the Media and Events Manager Mob: +233 244 819 228 CEO - Dr. Mrs. Ellen M. Hagan SPECIAL THANKS TO Email: [email protected], Publisher - Kofy Mensah Hagan Ms. Dinah Glover, Mrs. Suzy Ansah [email protected] General Manager - Nana Serwah A.