Who's Behind ICE? the Tech Companies Fueling

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Servicenow Events 16:9 Powerpoint Template

Visibility to Multi-Cloud Measurable outcomes from CMDB Table of Contents Visibility into Multi-Cloud/Hybrid Cloud 3 Customer journey to Cloud Discovery 4 Visibility into TAGS 6 Deep-dive Discovery of cloud VMs 6 Event-driven Discovery 8 Discovering serverless workloads 9 New York Release enhancements 11 AWS—Identity and Access Management (IAM) roles 11 AssumeRole enhancements for AWS organizations 11 Cloud Discovery UI improvements 11 ITOM Visibility low-code framework—pattern engine and out-of-band patterns 13 For more information 14 Journey to Cloud starts with ServiceNow ITOM Multi-cloud is Cloud and DevOps are independent but mutually reinforcing strategies for quickly becoming delivering business value through IT. A hybrid or multi-cloud workload deploy- the de-facto ment offers the advantage of high resiliency, combined with the agility to adapt quickly to changing digital business requirements. Multi-cloud is quickly deployment becoming the de-facto deployment standard as organizations of all types leverage an ever-increasing variety of cloud computing services. standard as organizations Key factors that influence multi-cloud deployment strategies are: • “Best-of-breed” service offering of all types • Cost to IT Ops and enterprise licensing leverage an • Choice of technology stack for IaaS/PaaS/FaaS services ever-increasing • M&A and data sovereignty, which plays a vital role on the decision- making process variety of cloud computing Visibility into multi-cloud/hybrid cloud services. For many customers, migration to cloud is a transformational journey. Visibility to multi-cloud/hybrid cloud deployment data with on-premise infrastructure and application data is critical to solve the real-world challenges from IT Operations. -

The Python/C API Release 3.6.0

The Python/C API Release 3.6.0 Guido van Rossum and the Python development team March 05, 2017 Python Software Foundation Email: [email protected] CONTENTS 1 Introduction 3 1.1 Include Files...............................................3 1.2 Objects, Types and Reference Counts..................................4 1.3 Exceptions................................................7 1.4 Embedding Python............................................9 1.5 Debugging Builds............................................ 10 2 Stable Application Binary Interface 11 3 The Very High Level Layer 13 4 Reference Counting 19 5 Exception Handling 21 5.1 Printing and clearing........................................... 21 5.2 Raising exceptions............................................ 22 5.3 Issuing warnings............................................. 24 5.4 Querying the error indicator....................................... 25 5.5 Signal Handling............................................. 26 5.6 Exception Classes............................................ 27 5.7 Exception Objects............................................ 27 5.8 Unicode Exception Objects....................................... 28 5.9 Recursion Control............................................ 29 5.10 Standard Exceptions........................................... 29 6 Utilities 33 6.1 Operating System Utilities........................................ 33 6.2 System Functions............................................. 34 6.3 Process Control.............................................. 35 -

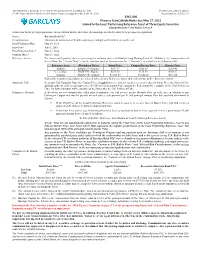

967000 Phoenix Autocallable Notes Due May 27, 2022 Linked to The

Amendment No. 1 dated July 25, 2018 to the Pricing Supplement dated May 24, 2018 Filed Pursuant to Rule 424(b)(2) (To the Prospectus dated March 30, 2018 and the Prospectus Supplement dated July 18, 2016) Registration No. 333–212571 $967,000 Phoenix AutoCallable Notes due May 27, 2022 Linked to the Least Performing Reference Asset of Three Equity Securities Global Medium-Term Notes, Series A Terms used in this pricing supplement, but not defined herein, shall have the meanings ascribed to them in the prospectus supplement. Issuer: Barclays Bank PLC Denominations: Minimum denomination of $1,000, and integral multiples of $1,000 in excess thereof Initial Valuation Date: May 24, 2018 Issue Date: June 1, 2018 Final Valuation Date:* May 24, 2022 Maturity Date:* May 27, 2022 Reference Assets: The American depositary shares representing the ordinary shares of Alibaba Group Holding Limited (“Alibaba”), the common stock of ServiceNow, Inc. (“ServiceNow”) and the common stock of Amazon.com, Inc. (“Amazon”), as set forth in the following table: Reference Asset Bloomberg Ticker Initial Price Coupon Barrier Price Barrier Price Alibaba BABA UN <Equity> $197.37 $128.29 $118.42 ServiceNow NOW UN <Equity> $175.52 $114.09 $105.31 Amazon AMZN UW <Equity> $1,603.07 $1,042.00 $961.84 Each of the securities noted above are referred to herein as a “Reference Asset” and, collectively, as the “Reference Assets.” Automatic Call: If, on any Call Valuation Date, the Closing Price of each Reference Asset is equal to or greater than its Initial Price, the Notes will be automatically called for a cash payment per $1,000 principal amount Note equal to the Redemption Price payable on the Call Settlement Date. -

M&A Transaction Spotlight

2012 AWARD WINNER: Capstone Partners GLOBAL INVESTMENT BANKING Investment Banking Advisors BOUTIQUE FIRM OF THE YEAR SaaS & Cloud M&A and Valuation Update Q2 2013 BOSTON CHICAGO LONDON LOS ANGELES PHILADELPHIA SAN DIEGO SILICON VALLEY Capstone Partners 1 CapstoneInvestment BankingPartners Advisors Investment Banking Advisors WORLD CLASS WALL STREET EXPERTISE.1 BUILT FOR THE MIDDLE MARKET.TM Table of Contents Section Page Introduction Research Coverage: SaaS & Cloud 4 Key Takeaways 5-6 M&A Activity & Multiples M&A Dollar Volume 8 M&A Transaction Volume 9-11 LTM Revenue Multiples 12-13 Highest Revenue Multiple Transactions for LTM 14 Notable M&A Transactions 15 Most Active Buyers 16-17 Public Company Valuation & Operating Metrics SaaS & Cloud 95 Public Company Universe 19-20 Recent IPOs 21-27 Stock Price Performance 28 LTM Revenue, EBITDA & P/E Multiples 29-31 Revenue, EBITDA and EPS Growth 32-34 Margin Analysis 35-36 Best / Worst Performers 37-38 Notable Transaction Profiles 40-49 Public Company Trading & Operating Metrics 51-55 Technology & Telecom Team 57-58 Capstone Partners 2 CapstoneInvestment BankingPartners Advisors Investment Banking Advisors 2 Capstone Partners Investment Banking Advisors Observations and Introduction Recommendations Capstone Partners 3 CapstoneInvestment BankingPartners Advisors Investment Banking Advisors WORLD CLASS WALL STREET EXPERTISE.3 BUILT FOR THE MIDDLE MARKET.TM Research Coverage: SaaS & Cloud Capstone’s Technology & Telecom Group focuses its research efforts on the following market -

Virtualwisdom App-Centric Hybrid IT Infrastructure Management Contents

VirtualWisdom App-centric Hybrid IT Infrastructure Management Contents Introduction 3 Operational Vulnerability 4 It’s Not Getting Easier 5 Expertise Required 6 What Expertise Is Required? 7 Traditional Monitoring Tools Don’t Cut It 9 VirtualWisdom Understands 10 Getting a Handle on Infrastructure 11 Getting a Handle on Applications 12 The Human Factor 13 VirtualWisdom Understands 14 HYBRID IT TECH BRIEF | BACK TO TOC | 2 Introduction Slow application performance and application outages cost money. As organizations have become more dependent on IT, the cost of outages has risen. Reducing the number of outages requires identifying their cause before the business is impacted. This is exactly what VirtualWisdom App-centric Hybrid IT Infrastructure Management excels at. Today, the cost of downtime for a single server can be punitive. According to Statista, 24 percent of respondents worldwide reported the average hourly downtime cost of their servers as being between $300,000 - $400,000, with more than 50 percent of respondents reporting costs in higher brackets. These statistics echo those released by Gartner, who cited $5,600 per minute as the cost of downtime: $5,600 per minute is $336,000 per hour. In today’s highly consolidated data centers, multiple individual virtualized hosts typically share a common infrastructure. A failure in any component of that infrastructure could result in multiple virtualized host failures. While it’s difficult to determine how much more a multiple-server outage would cost a given organization over a single server outage, the answer is certainly more than a single server outage would cost, and those costs are already far too high. -

Servicenow Cloud Success AWS 15MAR Webinar

Achieve Cloud Success with AWS Gain Cloud Service Oversight, Minimize Risks, and Reduce Costs – Simplified Through Self-Service Manisha Arora Deaddin Edris Douglas Lee Alliance Architect Senior Product Marketing Manager Head, Solution Architecture ServiceNow ServiceNow Strategic ISV Partners, AWS © 2017 ServiceNow All Rights Reserved 1 Agenda • Introduction • Why Organizations are Moving to the Cloud • The AWS Cloud • Manage Cloud Sprawl with ServiceNow • ServiceNow and AWS – Better Together • Demo • Q & A © 2017 ServiceNow All Rights Reserved 2 ServiceNow Is A Fast-Growing, Global Company ~4,800 Employees Strong Revenue & Growth Major Sites $1.391B San Diego, Silicon Valley, Seattle Amsterdam, London, Sydney, Israel, India $1B $683M $425M $244M $128M $28M $64M ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ’16 ©© 2017 ServiceNow All 2017 ServiceNow All Rights Rights Reserved Reserved 3 Global Enterprises in Every Industry Rely on ServiceNow Construction Federal Financial Services Healthcare Higher Education Insurance IT Services Manufacturing Media MSPs Oil and Gas Retail Services Technology ©© 2017 ServiceNow All 2017 ServiceNow All Rights Rights Reserved Reserved 4 Providing Cloud Services Across the Enterprise © 2017 ServiceNow All Rights Reserved 5 IT SLAs Force Cloud Users to Look for Alternatives Manual IT processes can take weeks to months Cloud Service Needs Grow DIY on Public Clouds Creating Shadow IT Outside of Business Controls Compliance & Introduction Audit Issues of Security Risks Inability to Control Costs © 2017 ServiceNow All Rights Reserved 7 The AWS Cloud © 2017 ServiceNow All Rights Reserved 8 The AWS Cloud Eliminate costly technical debt and reallocate resources so you can deliver high-value, revenue-generating projects faster. Innovate faster and solidify your competitive advantage by merging startup agility with enterprise experience and resources. -

SERVICENOW, INC. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of report (date of earliest event reported): February 22, 2017 SERVICENOW, INC. (Exact name of registrant as specified in its charter) Delaware 001-35580 20-2056195 (State or other jurisdiction of (Commission (I.R.S. Employer incorporation or organization) File Number) Identification Number) 2225 Lawson Lane Santa Clara, California 95054 (Address of Principal Executive Offices) (Zip Code) Registrant’s telephone number, including area code: (408) 501-8550 Not Applicable (Former Name or Former Address, if Changed Since Last Report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2 below): ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Item 5.02: Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers. (b) On February 24, 2017, Frank Slootman notified ServiceNow, Inc. (the “Company”) of his decision to resign from his position as the Company’s President and Chief Executive Officer, effective April 3, 2017. -

Software Equity Group's 2012 M&A Survey

The Software Industry Financial Report Software Equity Group, L.L.C. 12220 El Camino Real Suite 320 San Diego, CA 92130 [email protected] (858) 509-2800 Unmatched Expertise. Extraordinary Results Overview Deal Team Software Equity Group is an investment bank and M&A advisory firm serving the software and technology sectors. Founded in 1992, our firm has guided and advised companies on five continents, including Ken Bender privately-held software and technology companies in the United States, Canada, Europe, Asia Pacific, Managing Director Africa and Israel. We have represented public companies listed on the NASDAQ, NYSE, American, (858) 509-2800 ext. 222 Toronto, London and Euronext exchanges. Software Equity Group also advises several of the world's [email protected] leading private equity firms. We are ranked among the top ten investment banks worldwide for application software mergers and acquisitions. R. Allen Cinzori Managing Director Services (858) 509-2800 ext. 226 [email protected] Our value proposition is unique and compelling. We are skilled and accomplished investment bankers with extraordinary software, internet and technology domain expertise. Our industry knowledge and experience span virtually every software product category, technology, market and delivery model. We Dennis Clerke have profound understanding of software company finances, operations and valuation. We monitor and Executive Vice President analyze every publicly disclosed software M&A transaction, as well as the market, economy and (858) 509-2800 ext. 233 technology trends that impact these deals. We offer a full complement of M&A execution to our clients [email protected] worldwide. Our capabilities include:. Brad Weekes Sell-Side Advisory Services – leveraging our extensive industry contacts, skilled professionals and Vice President proven methodology, our practice is focused, primarily on guiding our client s wisely toward the (858) 509-2800 ext. -

Servicenow Is on a Collision Course with Salesforce.Com…Here’S Why

Breaking Analysis: ServiceNow is on a Collision Course With Salesforce.com…Here’s Why Breaking Analysis: ServiceNow is on a Collision Course With Salesforce.com…Here’s Why by, David Vellante July 22nd, 2021 ServiceNow is a company that investors love to love. But there’s caution in the investor community right now as confusion about transitory inflation and higher interest rates looms. ServiceNow also suffers from perfection syndrome and elevated expectations. The company has seen that the slightest misstep, or not beating earnings by a wide enough margin, can […] © 2021 Wikibon Research | Page 1 Breaking Analysis: ServiceNow is on a Collision Course With Salesforce.com…Here’s Why ServiceNow is a company that investors love to love. But there’s caution in the investor community right now as confusion about transitory inflation and higher interest rates looms. ServiceNow also suffers from perfection syndrome and elevated expectations. The company has seen that the slightest misstep, or not beating earnings by a wide enough margin, can cause mini freakouts from the investor community. So it has architected a financial and communications model that allows it to marginally beat expectations and raise its outlook on a continuing basis. Regardless, ServiceNow appears to be on a track to vie for what its CEO Bill McDermott refers to as the next great enterprise software company. Wait, we thought that Marc Benioff had taken that crown already… In this Breaking Analysis we’ll dig into ServiceNow, one of the companies we began following almost ten years ago, and provide some thoughts on ServiceNow’s march to $15B by 2026. -

Scientific Computing with MATLAB

Scientific Computing with MATLAB Paul Gribble Fall, 2015 Tue 12th Jan, 2016, 06:25 ii About the author Paul Gribble is a Professor at the University of Western Ontario1 in London, On- tario Canada. He has a joint appointment in the Department of Psychology2 and the Department of Physiology & Pharmacology3 in the Schulich School of Medicine & Dentistry4. He is a core member of the Brain and Mind Institute5 and a core member of the Graduate Program in Neuroscience6. He received his PhD from McGill University7 in 1999. His lab webpage can be found here: http://www.gribblelab.org This document This document was typeset using LATEX version 3.14159265-2.6-1.40.16 (TeX Live 2015). These notes in their entirety, including the LATEX source, are avail- able on GitHub8 here: https://github.com/paulgribble/SciComp License This work is licensed under a Creative Commons Attribution 4.0 International License9. The full text of the license can be viewed here: http://creativecommons.org/licenses/by/4.0/legalcode iii LINKS Links 1http://www.uwo.ca 2http://psychology.uwo.ca 3http://www.schulich.uwo.ca/physpharm/ 4http://www.schulich.uwo.ca 5http://www.uwo.ca/bmi 6http://www.schulich.uwo.ca/neuroscience/ 7http://www.mcgill.ca 8https://github.com 9http://creativecommons.org/licenses/by/4.0/ LINKS iv Preface These are the course notes associated with my graduate-level course called Sci- entific Computing (Psychology 9040a), given inthe Department of Psychol- ogy10 at the University of Western Ontario11. The goal of the course is to provide you with skills in scientific computing: tools and techniques that you can use in your own scientific research. -

Who's Behind ICE: Tech and Data Companies Fueling Deportations

Who’s Behind ICE? The Tech Companies Fueling Deportations Tech is transforming immigration enforcement. As advocates have known for some time, the immigration and criminal justice systems have powerful allies in Silicon Valley and Congress, with technology companies playing an increasingly central role in facilitating the expansion and acceleration of arrests, detentions, and deportations. What is less known outside of Silicon Valley is the long history of the technology industry’s “revolving door” relationship with federal agencies, how the technology industry and its products and services are now actually circumventing city- and state-level protections for vulnerable communities, and what we can do to expose and hold these actors accountable. Mijente, the National Immigration Project, and the Immigrant Defense Project — immigration and Latinx-focused organizations working at the intersection of new technology, policing, and immigration — commissioned Empower LLC to undertake critical research about the multi-layered technology infrastructure behind the accelerated and expansive immigration enforcement we’re seeing today, and the companies that are behind it. The report opens a window into the Department of Homeland Security’s (DHS) plans for immigration policing through a scheme of tech and database policing, the mass scale and scope of the tech-based systems, the contracts that support it, and the connections between Washington, D.C., and Silicon Valley. It surveys and investigates the key contracts that technology companies have with DHS, particularly within Immigration and Customs Enforcement (ICE), and their success in signing new contracts through intensive and expensive lobbying. Targeting Immigrants is Big Business Immigrant communities and overpoliced communities now face unprecedented levels of surveillance, detention and deportation under President Trump, Attorney General Jeff Sessions, DHS, and its sub-agency ICE. -

Marks Published for Opposition

MARKS PUBLISHED FOR OPPOSITION The following marks are published in compliance with section 12(a) of the Trademark Act of 1946. Applications for the registration of marks in more than one class have been filed as provided in section 30 of said act as amended by Public Law 772, 87th Congress, approved Oct. 9, 1962, 76 Stat. 769. Opposition under section 13 may be filed within thirty days of the date of this publication. See rules 2.101 to 2.105. A separate fee of two hundred dollars for opposing each mark in each class must accompany the opposition. SECTION 1.— INTERNATIONAL CLASSIFICATION The short titles associated below with the international class numbers are terms designed merely for quick identification and are not an official part of the international classification. The full names of international classes are given in section 6.1 of the trademark rules of practice. The designation ‘‘U.S. Cl.’’ appearing in this section refers to the U.S. class in effect prior to Sep. 1, 1973 rather than the international class which applies to applications filed on or after that date. For adoption of international classification see notice in the OFFICIAL GAZETTE of Jun. 26, 1973 (911 O.G. TM 210). Application in more than one class SN 75-416,963. LEARNING KEY, INC., THE, ALBUQUER- SN 75-741,599. HARLEQUIN ENTERPRISES LIMITED, DON QUE, NM. FILED 1-12-1998. MILLS, ONTARIO M3B 3K9, CANADA, FILED 6-30-1999. BLAZE THE LEARNING KEY CLASS 9—ELECTRICAL AND SCIENTIFIC APPARATUS FOR DOWNLOADABLE ELECTRONIC PUBLICA- NO CLAIM IS MADE TO THE EXCLUSIVE RIGHT TO TIONS, NAMELY ROMANCE NOVELS; PRE-RE- USE "LEARNING", APART FROM THE MARK AS SHOWN.