The Case of Telecommunications Systems Production in Estonia

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Theme – Embracing Uncertainty and Adapting to Change

The World’s Most Important Gathering of MFG Supply Chain Leaders March 30-31, 2016 Shanghai Marriott Hotel Pudong, China Theme – http://manufacturing.sco-summit.com/2016 Embracing Uncertainty and Adapting to Change Keynote Presentations; Case Study Presentations; Senior-level executives 40+ Executive Panel Discussions and decision makers to 300+ attend Hour for dedicated World-class peer-to-peer networking manufacturing 10+ opportunities 200+ organizations to gather Honored Speaker Line-up John Gattorna Ram Kuppuswamy Author and "Thought Leader" Global Chief Sourcing Officer Re-designing Contemporary Airtel Supply Chains End-to-end Porcurement Strategy Johannes Giloth Scott Preston Senior Vice President Global CSCO, CPO,Tronox Operations, Nokia Networks Big Data Analytics in Supply Chain Transformation Supply Chain • Book early and save up to US$ 600! Two Ways to Save $ • Get the group rate by sending four or more from your team. Tel: +86 21 3639 7572 Email: [email protected] MSCO STORY Over 1500 senior supply chain and logistics professionals from 600+ diversified companies and more than 30 countries were present at MSCO summits in the past 5 years, making MSCO the most important gathering of senior manufacturing supply chain professionals worldwide. 91% previous attendees rated the event excellent and very good. PAST SPEAKERS “ Excellent job on the summit organization and content. It was a very interesting conference both from the perspective of the people and companies attending, and also the content of the presentations. Arrangements and organization were excellent. Many thanks once again. ” NAVICO, Jim Brailey, EVP Supply Chain Management & Operations “ Very good mix of speakers and industries represented. -

Annual-Report-2016.Pdf

Annual Report 2016 INDEX Index GENERAL FINANCIAL STATEMENTS 3 Information to shareholders 22 Report of Board of Directors 2016 4 Scanfil in brief 26 Consolidated income statement, IFRS 6 CEO’s review 27 Consolidated statement of financial position, IFRS 8 Key figures 2016 28 Consolidated cash flow statement, IFRS 10 Customers 29 Consolidated statement of changes in equity, IFRS 14 Business operations 30 Accounting principles for consolidated financial statements 18 Personnel 35 Notes to the consolidated financial statements, IFRS 20 Board of Directors and 56 Key financial indicators Management Team 57 Key ratios 58 Parent company income statement, FAS 59 Parent company balance sheet, FAS 60 Parent company cash flow statement, FAS 61 Notes to the parent company financial statements, FAS 66 Shares and shareholders 68 Board of Directors´ proposal for the distribution of profit 69 Auditors’ report 70 Corporate governance statement 2016 INFORMATION TO SHAREHOLDERS Turnover 508 million EUR Information to shareholders Shareholder’s meetings The dividend matching day is 28 April 2017 and the dividend Scanfil plc’s Annual General Meeting (AGM) will be held on payment date 8 May 2017. The dividend will be paid to Wednesday 26 April 2017 in the Company’s main office at shareholders who are registered in the Register of Shareholders Yritystie 6, Sievi. The AGM will discuss the matters listed in the maintained by Euroclear Finland Ltd on the matching date. notice of the meeting, in accordance with the company’s Articles of Association. In addition, the meeting agenda will be published Financial information in a stock exchange release concerning the AGM and on the In 2017, Scanfil plc will publish the following financial reviews: company’s website at www.scanfil.com. -

Electronics, Multinationals and Labour Rights in Mexico.Pdf

Electronicsmultinationals and labour rights in Mexico Second report on working conditions in the Mexican electronics industry Centre for Reflection and Action on Labour Issues (CEREAL) October 2007 1 Centre for Reflection and Action on Labour Issues (CEREAL) CEREAL is a project of Fomento Cultural y Educativo A.C. (Cultural and Educational Promotion A.C.), part of the apostolic works of the Mexican Province of the Company of Jesus, which for the last 35 years has been devoted to educating and organising Mexican popular sectors. CEREAL provides legal assistance, labour rights training and organisational support for workers’ groups; it also carries out research on working conditions in different productive sectors in the country and promotes public awareness campaigns with regard to workers’ situation. 2 Table of Contents 4 Introduction. 5 Chapter 1. The Electronics Industry in 2006-7 15 Chapter 2. Working Conditions in the Mexican Electronics Industry 16 Outsourcing and labour rights violations 20 Discrimination 27 Constant work instability 33 Unsafe practices: Work-related accidents and illnesses 49 Exposure to toxic materials and work related illnesses 56 Sexual harassment 58 Excessive wage deductions 59 Humiliating treatment and work overloads 63 Lack of Trade Union Freedom 73 Chapter 3. Overall balance 77 Chapter 4. One year later: Collaboration between Canieti and Cereal 83 Recommendations 84 Annexes 3 Introduction. This is Cereal’s second report on working publication. These are the cases conditions in the Mexican electronics described in this report. All cases were industry. Being the second report means forwarded to the companies for that its nature has changed slightly. Now, consideration and most companies gave in addition to describing the current a reply in writing. -

1. Plant Competition As a Challenge for the EWC 2

Welcome to issue no. 1 / 2007 of EWC News. 11 th April 2007 The training and consultancy network "euro-workscouncil.net" is there to inform you about the activities of European works councils and related subjects. EWC News appears four times a year. You can download this newsletter as a pdf file and print it out. You can find past issues in the newsletter archives . Dieser Newsletter auf Deutsch Cette newsletter en français Contents: 1. Plant competition as a challenge for the EWC 2. What EWC work after a merger? 3. European Works Councils take legal action 4. Employers consider legal proceedings to be a risk 5. Minimum social standards agreed 6. Newly founded SEs 7. European Works Councils in the service sector 8. Czech Republic: New labour code and EWC work 9. EWC research 10. Interesting web sites 11. New publications 12. Training and consultancy network: Examples of our work 13. Details of seminars planned 14. Imprint 1. Plant competition as a challenge for the EWC EADS in crisis? The aircraft manufacturer, Airbus, the most important division of the EADS group, has not yet come to a halt. With the program "Power8", costs amounting to billions will be cut, even though the company’s books are full of orders. Administrative costs are supposed to be reduced by 30 per cent, the production tightened up and distributed around the plants more efficiently. Part of the production will go to companies outside the group and a number of sites will be sold to investors. These plans were triggered off by a delay in supplies to the wide-body aircraft A 380. -

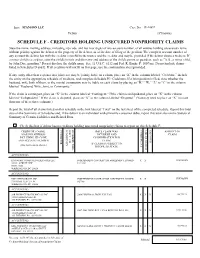

Creditors Holding Unsecured Nonpriority

In re SPANSION LLC Case No. 09-10692 Debtor (if known) SCHEDULE F - CREDITORS HOLDING UNSECURED NONPRIORITY CLAIMS State the name, mailing address, including zip code, and last four digits of any account number, of all entities holding unsecured claims without priority against the debtor or the property of the debtor, as of the date of filing of the petition. The complete account number of any account the debtor has with the creditor is useful to the trustee and the creditor and may be provided if the debtor chooses to do so. If a minor child is a creditor, state the child's initials and the name and address of the child's parent or guardian, such as "A.B., a minor child, by John Doe, guardian." Do not disclose the child's name. See, 11 U.S.C. §112 and Fed. R. Bankr. P. 1007(m). Do not include claims listed in Schedules D and E. If all creditors will not fit on this page, use the continuation sheet provided. If any entity other than a spouse in a joint case may be jointly liable on a claim, place an “X” in the column labeled “Codebtor,” include the entity on the appropriate schedule of creditors, and complete Schedule H - Codebtors. If a joint petition is filed, state whether the husband, wife, both of them, or the marital community may be liable on each claim by placing an “H,” “W,” “J,” or “C” in the column labeled “Husband, Wife, Joint, or Community.” If the claim is contingent, place an “X” in the column labeled “Contingent.” If the claim is unliquidated, place an “X” in the column labeled “Unliquidated.” If the claim is disputed, place an “X” in the column labeled “Disputed.” (You may need to place an “X” in more than one of these three columns.) Report the total of all claims listed on this schedule in the box labeled “Total” on the last sheet of the completed schedule. -

THE FLEX SYNDROME Working Conditions in the Hungarian Electronics Sector

THE FLEX SYNDROME Working conditions in the Hungarian electronics sector ACC and SOMO December 2012 COLOPHON THE FLEX SYNDROME Working conditions in the Hungarian electronics sector December 2012 AUTHORS: Zsófia Perényi (ACC), Kristóf Rácz & Irene Schipper (SOMO) RESEARCH: TÁRKI & SOMO & ACC PUBLISHED BY: SOMO – Centre for Research on Multinational Corporations COVER DESIGN: Justar.nl ISBN: 978-94-6207-014-1 This report is published as part of the makeITfair campaign, a European-wide project on consumer electronics. makeITfair aims to inform young consumers about human rights, social and environmental issues along the supply chain. It also addresses consumer electronics companies to contribute to change. makeITfair is coordinated by the Dutch organisation SOMO (Centre for Research on Multinational Corporations). Project partners are: SwedWatch and Fair Trade Center from Sweden; FinnWatch and Pro Ethical Trade Finland from Finland; DanWatch from Denmark; Germanwatch from Germany; Association of Conscious Consumers (ACC) from Hungary; ACIDH from the DR Congo; CIVIDEP from India; Workers Assistance Center (WAC) from the Philippines; and Civil Society Research and Support Collective (CSRSC) from South Africa. FUNDING: This publication has been produced with the assistance of the European Union. The content of this publication is the sole responsibility of SOMO and can in no way be taken to reflect the views of the European Union. CONTACT DETAILS: SOMO, Coordinator makeITfair Sarphatistraat 30, 1018 GL Amsterdam, The Netherlands Tel: +31 (0)20 639 12 91, [email protected], www.makeitfair.org SOMO: The Centre for Research on Multinational Corporations (SOMO) is a non-profit Dutch research and advisory bureau. SOMO investigates the policies of multinational enterprises and the internationalisation of business worldwide. -

Elcoteq Network Corporation Company Presentation March 2003

Elcoteq Network Corporation Company presentation March 2003 Slide 1 Elcoteq in brief • Largest European EMS provider, #6 globally, #3 in wireless communications • Focus on communications technology products • Founded in 1984 by Lohja Corporation • Listed on the Helsinki Exchanges since 1997 • Net sales MEUR 1,840.2 in 2002 • Operations in 12 countries on three continents • Approx. 10,200 employees • Total plant floor space 183,500 m2 Slide 2 CAGR of net sales 58% between 1991 and 2002 MEUR % 3500 250 3000 194% 200 2500 150 2000 132% 100 1500 82% 91% 63% 70% 44% 50 1000 31% 40% -1% 500 0 -16% 0 -50 94 9 1991 1992 1993 1 1995 1996 1997 1998 1999 2000 2001 2002 2003 Net sales, MEUR Estimate Year to year growth, % Slide 3 Elcoteq’s strategy Focus on communications technology Products – Terminal products, cellular networks, broadband communications networks and wireless local area networks – Wider service offering to meet customer needs and demand • Specific development areas: design & NPI services, sourcing and repair services Customers – Global, medium size and smaller start-up OEM’s Company image and brand – Unique global electronics manufacturing company for communications technology products Slide 4 Competitive advantages – Elcoteq’s 7 C’s Concentration - Focus on communications technology products Competence - Expertise especially in wireless telecom - Skilled personnel, high technology competence Co-evolution - Superb customer service - Close co-operation and confidentiality Consistency - Consistent plant network, machinery, uniform systems and processes - Transferability of resources on a global basis Cost-efficiency - 100 % of volume capacity in low-cost countries - Sourcing power through focusing Coverage - Global operations network; European origin - Full service range Continuous improvement - Competitive and unique service offering Slide 5 Organization CEO Lasse Kurkilahti TP* CNE/IE** GROUP FUNCTIONS: EUROPE EUROPE ASIA-PACIFIC AMERICAS Business Control Teo Ottola Harri Ollila Jukka Jäämaa Jouni Hartikainen Douglas Brenner Treasury Tuula Hatakka Corp. -

The Mobile Telephone Cluster in the Nordic Countries: Policies to Foster Innovation and Success Through Provider Competition and Knowledge Alliance Development

The Mobile Telephone Cluster in the Nordic Countries: Policies to Foster Innovation and Success through Provider Competition and Knowledge Alliance Development John L. Rice Dr Mark A. Shadur PhD Student Research Fellow School of Management School of Management Queensland University of Technology Queensland University of Technology GPO Box 2434 GPO Box 2434 Brisbane Queensland 4001 Brisbane Queensland 4001 Australia Australia Ph: + 61 7 3864 1345 Ph: + 61 7 3864 2053 Fax: + 61 7 3864 1766 Fax: + 61 7 3864 1766 Abstract The Nordic countries, and most especially Finland and Sweden, have been very successful in the development of international leadership in both mobile telephone penetration and mobile terminal and infrastructure manufacturing. Nokia and Ericsson are often discussed as world leaders in product design and innovation for both terminal and network infrastructure. Their success is the product of many years government focus in developing the mobile telecommunications industry as a whole, with a key policy aim of having a innovative manufacturing sector anchored within an advanced and demanding regional mobile telecommunications market. We examine here the policy and market environment in these countries that has supported the development of this highly vertically integrated and successful industry. Some attention has been given to the development of science parks, support of collaborative research that has supported both research and development and the development of a skilled labor market to assist firms growth. Less attention has been given to the success of government policies that have promoted the firms core technological competencies in supranational fora (most notably the promotion of firm competencies in the GSM standard) and the positive impact of the deregulated competitive telecommunications market, especially in Finland. -

Academy of Finland 59 Box 5.8 Elearning 60 Box 6.1 Case of Ahlström and Altim Control Ltd

39378 The World Bank 1818 H Street, N.W. Washington, D.C. 20433 USA Public Disclosure AuthorizedPublic Disclosure Authorized Finland Finland has been ranked number one for the fourth time since 2000 in the World Economic Forum’s Global Competitiveness Index. as a “…The country owes its strong showing to one of the most innovative Knowledge Economy business environments in the world, particularly critical to driving Elements of Success and Lessons Learned productivity in the country, given its advanced stage of development. This is coupled with a very healthy macroeconomic environment, at a Public Disclosure AuthorizedPublic Disclosure Authorized time when many other industrial countries are struggling in this area. Edited by The willingness of Finnish governments to run budget surpluses, so as to Carl J. Dahlman be able to meet future social commitments linked to the aging of the Jorma Routti population is particularly impressive. This approach to macroeconomic policy highlights a degree of political maturity in Finnish society worthy Pekka Ylä-Anttila of emulation. Furthermore, Finland has an institutional environment that is among the world’s finest: the business community operates in a climate Public Disclosure AuthorizedPublic Disclosure Authorized of respect for the law, unusually low levels of corruption, and an openness and transparency which other countries would do well to study.” Dr. Augusto Lopez-Claros, Chief Economist and Director, Global Competitiveness Programme, World Economic Forum in The Global Competitiveness Report 2005–2006, Executive Summary, pages xiv–xv. Houndmills, UK: Palgrave Macmillan. Public Disclosure AuthorizedPublic Disclosure Authorized i-xiv_Finland_FM.qxd 2/8/06 4:21 PM Page i Finland as a Knowledge Economy Elements of Success and Lessons Learned Edited by Carl J. -

Company Vendor ID (Decimal Format) (AVL) Ditest Fahrzeugdiagnose Gmbh 4621 @Pos.Com 3765 0XF8 Limited 10737 1MORE INC

Vendor ID Company (Decimal Format) (AVL) DiTEST Fahrzeugdiagnose GmbH 4621 @pos.com 3765 0XF8 Limited 10737 1MORE INC. 12048 360fly, Inc. 11161 3C TEK CORP. 9397 3D Imaging & Simulations Corp. (3DISC) 11190 3D Systems Corporation 10632 3DRUDDER 11770 3eYamaichi Electronics Co., Ltd. 8709 3M Cogent, Inc. 7717 3M Scott 8463 3T B.V. 11721 4iiii Innovations Inc. 10009 4Links Limited 10728 4MOD Technology 10244 64seconds, Inc. 12215 77 Elektronika Kft. 11175 89 North, Inc. 12070 Shenzhen 8Bitdo Tech Co., Ltd. 11720 90meter Solutions, Inc. 12086 A‐FOUR TECH CO., LTD. 2522 A‐One Co., Ltd. 10116 A‐Tec Subsystem, Inc. 2164 A‐VEKT K.K. 11459 A. Eberle GmbH & Co. KG 6910 a.tron3d GmbH 9965 A&T Corporation 11849 Aaronia AG 12146 abatec group AG 10371 ABB India Limited 11250 ABILITY ENTERPRISE CO., LTD. 5145 Abionic SA 12412 AbleNet Inc. 8262 Ableton AG 10626 ABOV Semiconductor Co., Ltd. 6697 Absolute USA 10972 AcBel Polytech Inc. 12335 Access Network Technology Limited 10568 ACCUCOMM, INC. 10219 Accumetrics Associates, Inc. 10392 Accusys, Inc. 5055 Ace Karaoke Corp. 8799 ACELLA 8758 Acer, Inc. 1282 Aces Electronics Co., Ltd. 7347 Aclima Inc. 10273 ACON, Advanced‐Connectek, Inc. 1314 Acoustic Arc Technology Holding Limited 12353 ACR Braendli & Voegeli AG 11152 Acromag Inc. 9855 Acroname Inc. 9471 Action Industries (M) SDN BHD 11715 Action Star Technology Co., Ltd. 2101 Actions Microelectronics Co., Ltd. 7649 Actions Semiconductor Co., Ltd. 4310 Active Mind Technology 10505 Qorvo, Inc 11744 Activision 5168 Acute Technology Inc. 10876 Adam Tech 5437 Adapt‐IP Company 10990 Adaptertek Technology Co., Ltd. 11329 ADATA Technology Co., Ltd. -

And Excluding Restructuring Expenses -22.3 in January-March 2007)

Elcoteq SE Stock Exchange Release April 23, 2007, at 9.00 am (EET) ELCOTEQ SE’S INTERIM REPORT JANUARY–MARCH 2008 (UNAUDITED) Elcoteq SE’s net sales between January and March totaled 908.7 million euros (952.5 in January-March 2007). Operating income was -9.5 million euros (-52.4 and excluding restructuring expenses -22.3 in January-March 2007). Operating income has clearly improved compared to the first quarter of the previous year even with lower net sales. The action plans to improve the company’s profitability and competitiveness are proceeding in accordance with expectations. • Net sales 908.7 million euros (952.5) • Operating income -9.5 million euros (-52.4 and excluding restructuring expenses -22.3) • Income before taxes -15.4 million euros (-59.0) • Earnings per share (EPS) -0.35 euros (-1.49) • Cash flow after investing activities -1.1 million euros (-40.9) • Rolling 12-month return on capital employed (ROCE) -10.7% (-2.9%) • Gearing 0.8 (0.7) This interim report has been prepared using IFRS recognition and measuring principles. Tables have been prepared in compliance with the IAS 34 requirements approved by the EU. The comparative figures given in the body text of this report are figures for the corresponding period in the previous year, unless stated otherwise. Net Sales and Result Elcoteq recorded net sales of 908.7 million euros (952.5) between January and March. Operating income totaled -9.5 million euros (-52.4) which was a clear improvement from previous year especially when taking into account the lower net sales. -

Embassy of Mexico

EMBAJADA DE MEXICO EMBASSY OF MEXICO Expanding Australia’s trade and investment relations with Mexico Prepared by the Embassy of Mexico For the Trade Sub-Committee of the Joint Standing Committee on Foreign Affairs. Parliament of Australia Canberra September, 2008 CONTENTS 1. Introduction 2. Background on the Mexican Economy and International trade 3. Overview of Bilateral Relations between Mexico and Australia 4. Trade between Mexico and Australia: what works and what needs more work 5. Administration of President Felipe Calderon: framework of Trade Policies and Priorities • ProMexico • National Infrastructure Plan • Investments • Mining Sector • Agriculture and Agri-Business • Manufacturing Sector • Services • Food and beverages • Education, Science and Technology • Tourism 6. Final remarks 2 1.- INTRODUCTION The economy of Mexico has enjoyed strong macroeconomic fundamentals and positive rates of growth since 2001. This macroeconomic stability has reduced inflation and interest rates to record lows and has increased per capita income. Certain challenges in income equality and infrastructure modernization exist, which the current Government is tackling with positive success. The Government of President Felipe Calderon (2006-2012), has implemented a ten step program to continue to incentivise Mexico’s economy: tax reductions, fiscal incentives to small and medium size companies, simplified paperwork for companies wanting to trade internationally, Government support (5% of the amount companies pay) to the Mexican Social Security System, increasing the amount spent on the National Employment Program, the creation of an internet-based job fair, increase in the amount spent on Mexico’s National Petroleum Company (PEMEX) in order to upgrade gas ducts, modernise and create more jobs in the energy sector, provide more resources to promote growth in marginalised parts of the country, increase funding to the development banking sector.