Chapter 1: Executive Summary Scope and Methodology Food Bar Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Q3 14 Choice Plus Approved Products Choice Plus Snack Requirements

Q3 14 Choice Plus Approved Products Choice Plus Snack Requirements (per package): ≤ 250 calories, ≤ 10 g fat*, ≤ 3 g saturated fat, 0 g trans fat, ≤ 230 mg of sodium, ≤ 20 g of sugar** (*Nuts and seeds are exempt from the total fat criteria due to their fiber, vitamin E and better fat content. These items must still meet the criteria for sodium and calories. **unsweetened dried fruit exempt) PLEASE NOTE: Snack products that meet ALL Choice Plus requirements above are approved for usage. Manufacturer Product (* Items qualify for 2bU program) Distributor(s) Size (oz) Size (g) Cal Cal Fat % Fat Fat (g) Sat. Fat (g) % Sat Fat Chol. (mg) Sod. (mg) Carb (g) Prot. (g) Trans fat Sugars (g) Dietary Fiber (g) 20/20 LifeStyles Protein Bar Cocoa Almond Vistar 1.00 27 110 50 8.00% 5 1 5 0 60 11 8 0 6 2 Cherry/Banana Vistar/Direct 0.64 18 55 3 1.00% 1 0 0% 0 0 12 1 0 6 2 Bare Fruit Mango/ Pineapple Vistar/Direct 0.64 18 34 2 1.00% 1 0 0% 0 7 8 1 0 8 1 Mini Chocolate Chunk Cookies* UNFI 9.50 26 130 50 9.00% 6 1.5 8% 0 70 17 2 0 9 1 SNACKWELL'S MINI Creme Sandwich Cookies Vistar 1.00 48 210 50 8.00% 5 1.5 8% 0 170 38 2 0 17 0 Back To Nature SNACKWELL'S COOKIE CAKES DEVIL'S FOOD FAT FREE Vistar 1.00 28 85 3 0.00% 0.0 0.0 0% 0 49 21 1 0 12 0 Honey Graham Stick Cookies* UNFI 8.00 31 130 25 5.00% 3 0 0% 0 170 25 30 0 9 1 Balance Bar Peanut Butter Vistar 1.00 50 200 60 11.00% 7 3 15 0 170 21 15 0 17 <1 Barbara's Bakery Snackimals Animal Cookies Chocolate Chip Vistar 1.00 30 120 35 6.00% 4 0 0 0 80 19 1 0 8 0 Biscomerica Basil's Low Fat Animal Snackers Vistar -

Mars, Incorporated Donates Nearly Half a Million Dollars to Recovery

Mars, Incorporated Donates Nearly Half a Million Dollars to Recovery Efforts Following Severe Winter Storms Cash and in-kind donations will support people and pets in affected Mars communities McLEAN, Va. (February 26, 2021) — In response to the devasting winter storms across many communities in the U.S., Mars, Incorporated announced a donation of nearly $500,000 in cash and in-kind donations, inclusive of a $100,000 donation to American Red Cross Disaster Relief. Grant F. Reid, CEO of Mars said: “We’re grateful that our Mars Associates are safe following the recent destructive and dangerous storms. But, many of them, their families and friends have been impacted along with millions of others We’re thankful for partner organizations like the American Red Cross that are bringing additional resources and relief to communities, people and pets, and we’re proud to play a part in supporting that work.” Mars has more than 60,000 Associates in the U.S. and presence in 49 states. In addition to the $100,000 American Red Cross donation, Mars Wrigley, Mars Food, Mars Petcare and Royal Canin will make in-kind product donations to help people and pets. As an extension of Mars Petcare, the Pedigree Foundation is supporting impacted pets and animal welfare organizations with $25,000 in disaster relief grants. Mars Veterinary Health practices including Banfield Pet Hospital, BluePearl and VCA Animal Hospitals are providing a range of support in local communities across Texas. In addition, the Banfield Foundation and VCA Charities are donating medical supplies, funding veterinary relief teams and the transport of impacted pets. -

Healthy Candy Bars

[Market Trends] Vol. 21 No. 6 June 2011 Candy Bars You Can Feel Good About By Kimberly J. Decker, Contributing Editor Paul Frantellizzi thinks we should all just give up the guilt and make like the ancients. The founder and CEO of Good Cacao, Boise, ID, notes the “many recent articles and studies now surfacing to confirm what the Mayan culture knew all along: Chocolate is good for you." To those of us who always considered a premium bar a bit of an over-the-counter “wonder drug, “this comes as little surprise. But to others— enamored of the notion that whatever tastes good must be bad for you—it flies in the face of conventional wisdom. But convention isn’t what it used to be, as more of us accept that a judiciously savored (and strategically formulated) candy bar need not oblige one to do penance. “The response we’ve gotten Candy a Top Impulse Buy at Checkout has been huge," Frantellizzi says of his company’s organic “functional" chocolates. A recent consumer survey regarding front-end checkout reveals But no shine from a healthy halo can that candy, magazines and soft drinks are the top impulse buys supplant what’s made candy bars so by most shoppers at the checkout line and retailers are missing opportunities for impulse sales. irresistible all along: pure sensory pleasure. As he says, “I have always believed that The study, “Front-End Focus,” was sponsored by Mars Chocolate acceptance of chocolate’s health benefits North America, a Division of Mars, Inc., Time-Warner Retail Sales will come with a great-tasting, quality & Marketing a division of Time Warner, The Wm. -

NEW PRODUCTS and PROMOTIONS By

Frito-Lay North America USA NEW PRODUCTS Cheetos Sweetos Cinnamon Sugar Puffs are a cinnamon sugar puff snack, an exten - AND PROMOTIONS sion of the original Cheetos line. Sold as a limited edition for spring with Easter colors by and graphics on the package. A 7 oz bag has DIRE CT ORY an DCB of $3.49. Tel: +1 (972) 334 7000 www.fritolay.com Mars UK UK Blue Diamond Growers UK Galaxy Salted Caramel bar is a Krunchies Crispy Coated California chocolate bar filled with soft Almonds are snack almonds with a flavored salted caramel. Available in a crisp coating. Available in Salt & Vinegar 48 g single bar ( DCB 60p) and a 135 g large bar ( DCB £1.39). and Spicy BBQ flavors. They are sold in the A permanent addition to the Galaxy Caramel Collection, United Kingdom in 70 g packs with an DCB which now features a redesign of the packaging. of £1.39. Tel: +44 (1753) 550 055 www.mars.co.uk Tel: +1 (916) 446 8500 www.bluediamond.com Nestlé UK UK Lindt USA USA Toffee Crisp Honeycomb bar Lindt Creation Crème Brülée is a milk is a combination of crunchy chocolate bar filled with crème and honeycomb pieces, crispy cereal caramelized sugar crystals. The new Creation and honeycomb-flavor toffee, covered in milk chocolate. collection of filled specialty bars also No artificial flavors, colors or preservatives. The limited- includes Molten Lava Cake (milk chocolate edition bar has an DCB of 59p. Available through whole - bar with a chocolate layer and dark chocolate sale and convenience channels only. -

Kosher Nosh Guide Summer 2020

k Kosher Nosh Guide Summer 2020 For the latest information check www.isitkosher.uk CONTENTS 5 USING THE PRODUCT LISTINGS 5 EXPLANATION OF KASHRUT SYMBOLS 5 PROBLEMATIC E NUMBERS 6 BISCUITS 6 BREAD 7 CHOCOLATE & SWEET SPREADS 7 CONFECTIONERY 18 CRACKERS, RICE & CORN CAKES 18 CRISPS & SNACKS 20 DESSERTS 21 ENERGY & PROTEIN SNACKS 22 ENERGY DRINKS 23 FRUIT SNACKS 24 HOT CHOCOLATE & MALTED DRINKS 24 ICE CREAM CONES & WAFERS 25 ICE CREAMS, LOLLIES & SORBET 29 MILK SHAKES & MIXES 30 NUTS & SEEDS 31 PEANUT BUTTER & MARMITE 31 POPCORN 31 SNACK BARS 34 SOFT DRINKS 42 SUGAR FREE CONFECTIONERY 43 SYRUPS & TOPPINGS 43 YOGHURT DRINKS 44 YOGHURTS & DAIRY DESSERTS The information in this guide is only applicable to products made for the UK market. All details are correct at the time of going to press but are subject to change. For the latest information check www.isitkosher.uk. Sign up for email alerts and updates on www.kosher.org.uk or join Facebook KLBD Kosher Direct. No assumptions should be made about the kosher status of products not listed, even if others in the range are approved or certified. It is preferable, whenever possible, to buy products made under Rabbinical supervision. WARNING: The designation ‘Parev’ does not guarantee that a product is suitable for those with dairy or lactose intolerance. WARNING: The ‘Nut Free’ symbol is displayed next to a product based on information from manufacturers. The KLBD takes no responsibility for this designation. You are advised to check the allergen information on each product. k GUESS WHAT'S IN YOUR FOOD k USING THE PRODUCT LISTINGS Hi Noshers! PRODUCTS WHICH ARE KLBD CERTIFIED Even in these difficult times, and perhaps now more than ever, Like many kashrut authorities around the world, the KLBD uses the American we need our Nosh! kosher logo system. -

Health, Nutrition & Fitness Report

Market Analysis Spring 2012 Health, Nutrition & Fitness Report Growth Opportunities Presented by the Current Focus on Healthier Living Kurt Roth Christopher Harned W. Andrew Martin Joseph Pellegrini Director Managing Director Managing Director Managing Director [email protected] [email protected] [email protected] [email protected] +1.312.609.4689 +1.414.765.3908 +1.704.553.6615 +1.704.553.6612 Christopher Sciortino Peter Kies Vinay Ghai Anthony Siu Managing Director Managing Director Managing Director Managing Director [email protected] Co-Head of Equity Capital Markets European Investment Banking Head of Asia Investment Banking +1.312.609.4923 [email protected] [email protected] [email protected] +1.414.765.7262 +44.207.667.8225 +86.21.6182.0980 Please refer to Appendix – Disclaimers and Other Disclosures on page 34. Table of Contents Page Investment Thesis.............................................................................................. 1 Growth Trends in Health, Nutrition & Fitness ..................................................... 2 Factors Driving the Trend Toward Healthier Living .......................................... 17 Selected Health, Nutrition & Fitness Companies ............................................... 24 Comparable Company Analysis ......................................................................... 28 Health, Nutrition & Fitness Deal Activity .......................................................... 31 Baird’s Health, Nutrition & Fitness Transaction Experience ............................. -

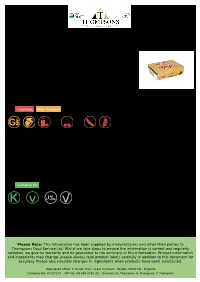

Allergy Information Nutritional Information Mars Twix Chocolate

Thompsons Food Service Ltd. Tel: 01493 249649 26 - 28 Southgates Road Fax: 0845 051 8772 Great Yarmouth E-Mail: [email protected] Norfolk Web: www.tfsltd.co.uk NR30 3LL Mars Twix Chocolate Bar (2x25g) - Information TFS Product Code: 012451 Suppliers Product Code: Information Last Updated: 10/09/2019 Date Produced: 28/09/2021 Allergy Information Nutritional Information Key: Contains May Contain Serving Unit: 100g or 100ml Energy (kcal) 495.00 Energy (kJ) 2074.00 Protein (g) 4.50 Gluten Nuts Milk Sulphur Dioxide Soya Cereal Carb (g) 64.60 Of Which Sugars (g) 48.80 Fat (g) 24.00 Of Which Saturates (g) 13.90 Fibre (g) 0.00 Salt (g) 0.44 Dietary Information Key: Suitable for Kosher Vegetarian Halal Vegan Please Note: This information has been supplied by manufacturers and other third parties to Thompsons Food Service Ltd. Whilst we take steps to ensure the information is correct and regularly updated, we give no warranty and no guarantee to the accuracy of this information. Product information and ingredients may change; please always read product labels carefully in addition to this document for accuracy. Please also consider changes to ingredients when products have been substituted. Registered Office: 7 Church Plain, Great Yarmouth, Norfolk, NR30 1PL, England Company No: 07107278 VAT No: GB 986 0801 93 Directors: E. Thompson, R. Thompson, T. Thompson Thompsons Food Service Ltd. Tel: 01493 249649 26 - 28 Southgates Road Fax: 0845 051 8772 Great Yarmouth E-Mail: [email protected] Norfolk Web: www.tfsltd.co.uk NR30 3LL Mars Twix Chocolate -

Confection/Snack/Bakery

04 December 2017 CONFECTION/SNACK/BAKERY NEW Hershey Items Jolly Rancher Sweetarts Gummies Hershey Gold 24ct Sour Surge 12ct-6.5z U of M Bag 8ct-8z 11852-4 [1185248] 11854-0 [1185404] 13068-0 [1306802] Hershey Gold @Jolly Rancher King Size 18ct Sour Surge 1ct-6.5z 11850-8 [1185081] 11855-9 [1185594] >Available in Walker Warehouse Only 11853-2 Jolly Rancher Sour Surge 12ct 11853-2 [1185321] Airhead 5-Bar Pack 18ct Items in RED Shipping to 12863-5 PACESETTER Customers Kit Kat Dark [1286350] King Size 24ct 13185-7 Hershey’s Gold Caramelized Creme with Peanuts and Pretzels features a caramelized creme, with a [1318575] combination of sweet, salty, crunchy and creamy. CONFECTION/SNACK/BAKERY Mars announces exciting new products and line NEW Mars-Wrigley Items extensions to deliver on- M&M King Size trend product innovation... Twix White King Size 20ct White Chocolate 24ct [1449321] 14493-2 14183-6 [1418367] Dove Chocolate-Covered Dusted Nuts feature cashews dipped in Twix White 20ct milk chocolate dusted with sea salt and almonds dipped in dark 14489-5 [1448950] chocolate dusted with cinnamon. Snickers KS PB Snickers Peanut Butter Crisper Crisper 18ct provides the perfect balance of [1418441] sweet, salty, creamy, and crispy. 14184-4 M&M’s White Chocolate Candies is a new, year-round offering that Dove Chocolate featured creamy white chocolate enclosed in a colorful candy shell. Almond 10-1.6z [1418607] Maltesers treats feature light, 14186-0 crispy, airy centers, dipped in smooth chocolatey deliciousness, Maltesers KS 8ct Dove Chocolate now available in Share Size. -

Brooks Default Orientation UTR

Tested textiles for: Brooks Default Orientation UTR Textiles are a critical component of our seating and screen products. The following list is intended to facilitate selection of textiles for use on our products. COM Selections Stylex is pleased to accept COM selections, but they must be approved. Stylex reserves the right to reject textiles to ensure that quality and construction are satisfactory for intended use. Once COM is approved, Stylex assumes no responsibility for its overall appearance, durability, colorfastness, or any other quality issues after upholstered on a Stylex product. Textile Orientation Textile orientation is determined by Stylex on a per product basis. Yardage requirements shown in the Stylex price list are calculated based on the product’s default orientation. Yardage requirements may increase for COM’s that require an orientation differing from the default. Please see textile orientation explanations below: 1. Railroaded (RR) – The textile is applied to the unit perpendicular to the direction of the roll. 2. Up the Roll (UTR) – The textile is applied to the unit parallel to the direction of the roll. Textile Maintenance Please note that the below textiles identified as bleach cleanable were indicated as such by the textile supplier as of 6/1/2020. Detailed cleaning instructions and confirmation of disinfecting processes are provided by the textile supplier. As always, failure to follow cleaning instructions may result in damage to textiles. Stylex is not responsible for any damage that may occur from cleaning or maintenance. Approvals Please be advised that all approvals listed here are provisional. We reserve the right to withdraw approval at any time, including after an order has been placed. -

Cadenza Document

VGM Club Report Date: Jul 2019 Contracted Manufacturer Report Mfr Name Has Rebate Has Pricing 3M Y Y Abbott Nutrition Y N ACH Food Companies Y N Advance Food Products LLC AFP Y Y AdvancePierre Y Y Agro Farma Inc Y Y Ajinomoto Windsor Inc (formerly Windsor Frozen Foods) Y N Allied Buying Corporation (ABC) Y N All Round Foods Bakery Products Y N Alpha Baking/National Baking Y N American Licorice Co Y N American Metalcraft Y N American Roland Food Corp Y N Amplify Snack Brands Y N Amy's Kitchen Inc Y N Anchor Packaging Y Y Antonio Mozzarella Factory Y N Appetizers And Inc Y Y Apple & Eve Y Y Argo Tea Y Y Arizona Tea - Hornell Brewing Company Y Y Armanino Foods Y Y Armour-Eckrich Meats LLC DBA Carando Y N Armour Eckrich - Smithfield Y Y Ateeco/Mrs T's Pierogies Y Y Atlantic Mills Co Y Y Awake Chocolate Y N Azar Nut Company Y N Bagcraft Packaging LLC Y N Bake N Joy Inc Y N Bakery De France Y Y Ballard Brands Y Y BarFresh Corporation Inc Y Y Barilla America Inc Y Y Basic American Food Co Y Y Bay Valley Foods LLC Y N Belgioioso Cheese Inc Y N Bel Kaukauna Cheese Co Y Y Berks Packing Co Inc Y N Berry Plastics Diet Kits Y N Berry Plastics Liners Y Y Beverage Air Y N Page 1 Of 9 VGM Club Report Date: Jul 2019 Contracted Manufacturer Report Mfr Name Has Rebate Has Pricing Beyond Meat Y Y B&G Foods Inc Y Y Big City Reds /American Foods Y N Big Red Inc Y Y BioSelect N Y Biscomerica Corp. -

Sweet Inspirations from MARS Candy Brands

from MARS candy brands Sweet Inspirations Discover exciting ways to bring the power of MARS Candy Brands to your menu. Frozen Vanilla Chai Frappe made with TWIX® page 13 Sweet Appreciation Explore this collection of sweet inspirations that bring the popularity and convenience of MARS Candy inclusions to your menu. TREAT ME NOW Our well-known and loved brands can add a new appeal that will Studies show that your customers love make your baked goods, specialty drinks, dairy–based treats and to indulge away from home. Get inspired holiday offerings even more attractive. to make the most of every sweet opportunity with our featured concepts. WHY BRING MARS CANDY INCLUSIONS • 52% of consumers say they eat some type 5 IN ON YOUR MENU? of dairy-based treat away from home • 33% of consumers eat a baked dessert5 • 90% of customers say a brand name positively influences their away from home at least occasionally choice of menu items1 • 65% of all consumers say they snack5 • Studies show consumers are willing to pay 10% more for a MARS between meals branded dessert1 • M&M’S® is the #1 Confectionery Brand with 100% awareness2 • SNICKER’S® is America’s #1 candy bar3 • TWIX® is one of America’s favorite chocolate brands and one of the top 5 “most loved” brands among those age 13 to 494 Dessert Pizza Dough Knots made with SNICKERS® page 11 Harvest Muffins & Streusel Topping made with TWIX® page 14 2 3 COCO-CHOCOLATE CHAI MILKSHAKE Ice Cream Shakes MADE WITH M&M’S® Popular chai tea latte spiced with the traditional & aromatics of cardamom, cinnamon, ginger and clove, VANILLA MILKSHAKE blended with frosty-cold vanilla ice cream and M&M’S® ® MADE WITH M&M’S Brand Coconut Chocolate Candies for a modern Classic cold-and-creamy real vanilla milkshake twist on a classic drugstore dessert. -

Snack, Cereal and Nutrition Bars in the United States

International Markets Bureau MARKET ANALYSIS REPORT | SEPTEMBER 2013 Snack, Cereal and Nutrition Bars in the United States Source: Mintel GNPD. Source: Mintel GNPD. Snack, Cereal and Nutrition Bars in the United States EXECUTIVE SUMMARY INSIDE THIS ISSUE Total health and wellness food and beverage sales in the Executive Summary 2 United States are on the rebound, growing by 2% from 2011 to 2012 (and 6% from 2010 to 2012), despite the economic Market Snapshot 3 slowdown that the U.S. experienced these past 5 years. It now appears that with a recovering economy, Americans are again Snack Bars Market Sizes 4 receptive to buying health foods. However, future growth may be hampered by the frugality that American consumers have Health and Wellness Snack 5 adopted, meaning that consumers may be more price-sensitive Bars Market in shopping for healthy options. Organic Snack Bars 6 U.S. packaged food as a whole is recovering from the economic downturn; U.S. organic packaged food sales are also Energy and Nutrition Bars 7 recovering. Organic products are sub-category of the health and wellness sector. Organic products carry a higher price Consumer Trends 8 than their conventional counterparts, so it is not surprising that sales were affected by the economic slowdown. Before the Claims Analysis 11 recession of 2008, organic packaged food value sales enjoyed double-digit growth before plunging. Now organic packaged Market Shares by Brand 12 food value sales are recovering again; they increased by 2.1% and Company between 2011 and 2012, to reach US$12.2 billion. Distribution Channels 13 Snack, cereal and nutrition bars continued their growth in 2012, with an ever-expanding array of flavours and healthy varieties.