Mineral Sands

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

West Coast Land Use Planning Strategy

" " " " " " " " " !"#$%&'(#$%&')*&+,%,(*-%)#"%.,(**+*/%#$0($"/1%" " #".$"23"0%4567% " " " " " " " " " " " " " " " " " " " " " " " " " " " Prepared for West Coast Council" " By:" ႛ Integrated Planning Solutions; ႛ Essential Economics; and ႛ Ratio Consultants " " " " !" !" #$%&'()*%#'$+ , 6868 '9:;<=>?;@%AB%=C;%,DEF%)@;%.GDEE>EH%#=ID=;HJ% K 6848 $C;%2;=CAFAGAHJ% L -" ./0$$#$1+*'$%23%+ 4 4868 .GDEE>EH%&AE=IAG@% M #$!$!$ %&'()" * #$!$#$ +,((')-&.'" * #$!$/$ 0-1232'" !4 #$!$5$ %((32'" !! #$!$6$ 7&)(8(19" !# #$!$:$ ;,<<23" !# #$!$=$ >?(1<29)"2'@"A&@()" !/ 5" %62+/21#7/0%#82+9&0:2;'&<+ !, N868 ,DEF%)@;%.GDEE>EH%DEF%(OOIA?DG@%(<=%6MMN%P$D@Q% 6K N848 #=D=;%.GDEE>EH%'9:;<=>?;@% 6K N8N8 #=D=;%DEF%0;H>AEDG%.AG><>;@% 6L /$/$!$ 0-2-("B<2''C'D"B&<CEC()" !6 /$/$#$ 7(DC&'2<"B<2''C'D"B&<CEC()" !6 ," ./0$$#$1+*'$7#(2&0%#'$7+ != K868 '?;I?>;R% 67 5$!$!$ +,((')-&.'" !F 5$!$#$ 0-1232'" !F 5$!$/$ %((32'" !* 5$!$5$ 7&)(8(19" !* 5$!$6$ ;,<<23" !* 5$!$:$ G12'?C<<("H218&,1"2'@";1C2<"H218&,1" !* K848 !CD=%>@%=C;%<SII;E=%OGDEE>EH%<AE=;T=%BAI%=C;%!;@=%&AD@=U% 45 5$#$!$ G(&D12I3CE"E&'-(J-"K&1"-3("1(DC&'" #4 5$#$#$ L(9"M2E-&1)" #4 5$#$#$!$ B&I,<2-C&'"-1('@)" #! 5$#$#$#$ B&I,<2-C&'"I1&N(E-C&')" #! 5$#$#$/$ 0&EC&O(E&'&PCE"A3212E-(1C)-CE)" #6 5$#$#$5$ L(9"QE&'&PCE"R'@CE2-&1)" #= 5$#$/$ L(9"R'@,)-1C()" /# 5$#$/$!$ SC'C'D" /# 5$#$/$#$ ;&,1C)P" // #" K8N8 !CD=%DI;%=C;%@=I;EH=C@V%R;DWE;@@;@V%AOOAI=SE>=>;@%DEF%=CI;D=@%R>=C>E% =C;%GA<DG%@=ID=;H><%OGDEE>EH%<AE=;T=U% NL 5$/$!$ 0-1('D-3)" /6 5$/$#$ T(2U'())()" /: 5$/$/$ >II&1-,'C-C()" /: 5$/$5$ ;31(2-)" /: K8K8 .I;G>X>EDIJ%GDEF%@SOOGJ%<AE@>F;ID=>AE@% -

Australian Investment Strategy

2 November 2016 Asia Pacific/Australia Equity Research Investment Strategy Australian Investment Strategy Research Analysts STRATEGY Hasan Tevfik ,CFA 61 2 8205 4284 [email protected] Aussie darlings Peter Liu 61 2 8205 4071 ■ Aussies love their darlings: Australia currently has the most expensive [email protected] equity market "Darlings" in the world. Our darlings trade on a forward P/E Damien Boey of 38x. The other commodity-focused market, Canada, has the second 61 2 8205 4615 [email protected] most expensive darlings. Darlings in Australia have been more expensive only during the Nasdaq bubble when they touched 45x. ■ Darling derating: Buying Australian darlings at these valuations has been a poor strategy in the past. Also, the current high valuation for Australia's darlings suggest they are especially vulnerable to rising bond yields and the coming end of the Australian profits recession. A rising discount rate and a lower premium for growth suggest investors should focus on stocks that could be future darlings. ■ Hello Daaarling: Future market darlings have shared many similar characteristics over the last 20 years. They are generally well managed, have strong balance sheets and operate on high margins. Our "Hello Daaarling" strategy highlights potential future darlings and they currently trade on just 17x P/E and include Caltex, Eclipx, Mayne Pharma, Nufarm, Star Entertainment and South 32. We add Eclipx to our long Portfolio. Figure 1: Australia has the most expensive darlings in the world Median 12-month forward P/E of "market darlings" around the world* 40 35 30 25 20 15 10 Australia Canada Cont. -

For Personal Use Only Use Personal For

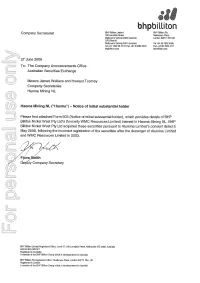

.1 S. bhpbi ILl ton Company Secretariat BHP Billiton Limited BHP BullIon Plc 180 Lonscfale Street Neatliouse Place Melbourne Victoda 3000 Austra8a London SW1V 1BH UK GPO Box 86 Melbourne Vicfoda 3001 Australia Tel ^44 20 7802 4000 Tel^61 1300554757Fax+61 396094372 Fax +44 20 7802 4111 bhpbilliton.com bhpbillilon.cotrt 27 June 2008 To: The Company Announcements Office Australian Securities Exchange Messrs James Wallace and Howard Toomey Company Secretaries Haoma Mining NL Haoma Mining NL ("Haoma") Notice of initial substantial holder Please find attached Form 603 (Notice of initial substantial holder), which provides details of BHP Billiton Nickel West Pty Ltd's (formerly WMC Resources Limited) interest in Haoma Mining NL. BHP Billiton Nickel West Pty Ltd acquired these securities pursuant to Alumina Limited's consent dated 5 May 2008, following the incorrect registration of the securities after the demerger of Alumina Limited and WMC Resources Limited in 2003. ' /. / ,'' // F)ona,Smlth V Deity Company Secretary For personal use only BHP BullIon Limded Registered Offica: Level 27, 180 Lonsdale Street, Melbourne VIC 3000, Australia AGN 49004 028 077 Registered in Australia A member of the BHP Billiton Group which is headquartered in Australia BHP Billiton Plc Registered Office: Neathouse Place, London SWIV IBH, UK Registered in London A member of Ihe BHP BullIon Group which is headquartered in Australia 603 page 1/2 153u1y2001 Form 603 Corporations Act 2001 Section 671B Notice of initial substantial holder 1g. Company Name/Scheme Haoma Mining NL ACNIARSN 008 676 177 1. Details of substantial holder (1) Name BlIP Billiton Limited ACN/ARSN (if applicable) 004 028 077 This notice is given by BHP Billiton Limited on behalf of BHP Billiton Limited's controlled bodies corporate (Limited Subsidiaries), on behalf of BlIP Billilon Plc, and on behalf of BF-IP Bifiton Plc's controlled bodies corporate (Plc Subsidiaries) including those named in the list annexed to this Form 603 and marked Annexure A. -

2020 ACARP Report

2020 THE COAL INDUSTRY’S RESEARCH PROGRAM WWW.ACARP.COM.AU 1 CHAIRMAN’S REPORT ACARP’s role is to identify the coal industry’s research needs; Welcome to our 2020 ACARP Report. select and award research projects; and manage the research Ken Singer Manager Mine Control (UMM) BMA Much has been and will be written of 2020 with the impacts program, including communicating the outcomes to the industry of COVID-19 far reaching. ACARP was not immune. Saleable in a way that best accelerates their implementation. The focus Peter Smith General Manager HS Centennial Coal production recorded by ACARP for FY20 was 444.8 million tonnes continues to be on improving safety, boosting productivity and and ACARP funded $18.7 million in direct research spend. During minimising the environmental impacts of mining. Considerable Trevor Stay General Manager Gas Anglo American the second half of 2020 coal production reduced in response to focus this year has included research of dust particulate matter depressed coal demand. COVID-19 has had a minimal impact Andrew Swiericzuk Project Manager-Studies, Coal Australia Rio Tinto measurement, impacts and prevention and mine site rehabilitation on ACARP operations as we elected to curtail some service and the re-purposing of final voids in post mining landscapes. activities such as face to face meetings and travel. Reduced work A number of significant projects included in this report are funding approved 2015 arrangements introduced by Researchers including access to continuing, and we believe that these too will provide great workplaces and laboratories, travel restrictions limiting access benefits to the industry. -

1. Gina Rinehart 2. Anthony Pratt & Family • 3. Harry Triguboff

1. Gina Rinehart $14.02billion from Resources Chairman – Hancock Prospecting Residence: Perth Wealth last year: $20.01b Rank last year: 1 A plunging iron ore price has made a big dent in Gina Rinehart’s wealth. But so vast are her mining assets that Rinehart, chairman of Hancock Prospecting, maintains her position as Australia’s richest person in 2015. Work is continuing on her $10billion Roy Hill project in Western Australia, although it has been hit by doubts over its short-term viability given falling commodity prices and safety issues. Rinehart is pressing ahead and expects the first shipment late in 2015. Most of her wealth comes from huge royalty cheques from Rio Tinto, which mines vast swaths of tenements pegged by Rinehart’s late father, Lang Hancock, in the 1950s and 1960s. Rinehart's wealth has been subject to a long running family dispute with a court ruling in May that eldest daughter Bianca should become head of the $5b family trust. 2. Anthony Pratt & Family $10.76billion from manufacturing and investment Executive Chairman – Visy Residence: Melbourne Wealth last year: $7.6billion Rank last year: 2 Anthony Pratt’s bet on a recovering United States economy is paying off. The value of his US-based Pratt Industries has surged this year thanks to an improving manufacturing sector and a lower Australian dollar. Pratt is also executive chairman of box maker and recycling business Visy, based in Melbourne. Visy is Australia’s largest private company by revenue and the biggest Australian-owned employer in the US. Pratt inherited the Visy leadership from his late father Richard in 2009, though the firm’s ownership is shared with sisters Heloise Waislitz and Fiona Geminder. -

Mineral Facilities of Asia and the Pacific," 2007 (Open-File Report 2010-1254)

Table1.—Attribute data for the map "Mineral Facilities of Asia and the Pacific," 2007 (Open-File Report 2010-1254). [The United States Geological Survey (USGS) surveys international mineral industries to generate statistics on the global production, distribution, and resources of industrial minerals. This directory highlights the economically significant mineral facilities of Asia and the Pacific. Distribution of these facilities is shown on the accompanying map. Each record represents one commodity and one facility type for a single location. Facility types include mines, oil and gas fields, and processing plants such as refineries, smelters, and mills. Facility identification numbers (“Position”) are ordered alphabetically by country, followed by commodity, and then by capacity (descending). The “Year” field establishes the year for which the data were reported in Minerals Yearbook, Volume III – Area Reports: Mineral Industries of Asia and the Pacific. In the “DMS Latitiude” and “DMS Longitude” fields, coordinates are provided in degree-minute-second (DMS) format; “DD Latitude” and “DD Longitude” provide coordinates in decimal degrees (DD). Data were converted from DMS to DD. Coordinates reflect the most precise data available. Where necessary, coordinates are estimated using the nearest city or other administrative district.“Status” indicates the most recent operating status of the facility. Closed facilities are excluded from this report. In the “Notes” field, combined annual capacity represents the total of more facilities, plus additional -

Telfer W with Pr 800,000 Copper Signific Resourc

4420 Newcrest Cover 04 6pp 16/9/04 9:52 AM Page 2 Telfer will be the largest gold mine in Australia, with projected annual production of more than 800,000 ounces of gold and 30,000 tonnes of copper for 24 years, positioning Newcrest as a significant and profitable Australian-based resources business. Newcrest Mining Limited Newcrest – The Sustainable Section 5 Resource Business 1 Sustainability and People 38 Section 1 Health and Safety 40 Our Results 2 Environment 42 Human Resources 43 Performance in Brief 2 Chairman’s Review 4 Section 6 ABN: 20 005 683 625 ABN: Managing Director and Corporate Governance 44 Chief Executive Officer’s Report 5 Board of Directors 45 Newcrest Senior Management 10 Corporate Governance 46 Financial Report 11 Section 7 Section 2 Concise Annual Report 2004 Financials 49 Operations 12 Directors’ Report 50 Cadia Valley Operations 14 Management Discussion and Analysis Ridgeway Gold/Copper Mine 14 of the Financial Statements 56 Cadia Hill Gold/Copper Mine 16 Statement of Financial Performance 58 Toguraci Gold Mine 19 Statement of Financial Position 59 Section 3 Statement of Cash Flows 60 Projects 22 Notes to the Concise Financial Report 61 Directors’ Declaration 68 Telfer Gold/Copper Project 24 Independent Audit Report 69 Cracow 26 Cadia East 28 Shareholder Information 70 Boddington Expansion Project 29 Five Year Summary 72 Section 4 Corporate Directory IBC Exploration 30 Strategy and Review 32 Mineral Resources and Ore Reserves 34 Newcrest Mining Limited Newcrest ABN: 20 005 683 625 Notice of Meeting Notice is hereby given that the 24th Annual General Newcrest Mining Limited Meeting will be held at the Hyatt Regency Hotel, Concise Annual Report 2004 99 Adelaide Terrace, Perth, Western Australia on Wednesday 27 October 2004 at 9.30am. -

The Information Quality of Derivative Disclosures in Corporate Annual Reports of Australian Firms in the Extractive Industries

THE INFORMATION QUALITY OF DERIVATIVE DISCLOSURES IN CORPORATE ANNUAL REPORTS OF AUSTRALIAN FIRMS IN THE EXTRACTIVE INDUSTRIES Mohamat Sabri Hassan B.Ac (Hons.) (Universiti Kebangsaan Malaysia), M.Social Science (Southampton) A dissertation submitted for the degree of Doctor of Philosophy within the School of Accountancy at Queensland University of Technology 2004 Keywords: Disclosure quality; transparency; disclosure index; financial instruments; derivative instruments; market value; extractives industries. ii ABSTRACT Recent events in the business world have focused attention on the importance of high quality financial reporting. Of particular interest is where the collapse of prominent companies such as Baring Plc. was due to the company’s involvement with derivative instruments. In Australia, some derivative instruments are not recognised in the balance sheet. However, the Australian accounting standard AASB 1033 Presentation and Disclosure of Financial Instruments requires extensive disclosures to overcome the lack of guidance with regard to the recognition and measurement. Therefore, AASB 1033 may be regarded as a high quality disclosure standard. This thesis investigates the transparency or information quality of derivative disclosures of Australian firms in the extractive industries using 1998 to 2001 financial reports. The extractive industries play a major role in the Australian economy, where they generated exports worth more than A$30billion in 2000 to 2002 (Department of Foreign Affairs and Trade, 2003a and 2003b). Further, firms in the extractive industries extensively use derivative instruments for hedging purposes (Berkman, Bradbury, Hancock and Innes, 1997). The objective of this study is, first, to examine the relationship between the transparency or disclosure quality of derivative information and firm characteristics. -

A Structural Examination of the Telfer Gold-Copper Deposit And

ResearchOnline@JCU This file is part of the following reference: Hewson, Simon Andrew John (1996) A structural examination of the Telfer gold-copper deposit and surrounding region, northwest Western Australia: the role of polyphase orogenic deformation in ore-deposit development and implications for exploration. PhD thesis, James Cook University. Access to this file is available from: http://eprints.jcu.edu.au/27718/ If you believe that this work constitutes a copyright infringement, please contact [email protected] and quote http://eprints.jcu.edu.au/27718/ A Structural Examination of the Telfer Gold-Copper Deposit and Surrounding Region. northwest Western Australia: The Role of Polyphase Orogenic Deformation in Ore-deposit Development and Implications for Exploration. VOLUME 1 Thesis submitted by Simon Andrew John HEWSON BSc (Hans) (Curtin) in October, 1996 for the degree of Doctor of Philosophy in the Department of Earth Sciences at James Cook University of North Queensland. I, the undersigned, the author of this thesis, understand that the following restriction placed by me on access to this thesis will not extend beyond three years from the date on which the thesis is submitted to the University. I wish that access to this thesis not to be permitted for a period of three years. After this period has elapsed I understand that James Cook University of North Queensland will make it available for use within the University Library and, by microfilm or other photographic means, allow access to users in other approved libraries. All users consulting this thesis will have to sign the following statement: " In consulting this thesis I agree not to copy or closely para-phrase it in whole or in part without the written consent of the author; and to make proper written acknowledgement for any assistance which I have obtained from it. -

Content/Dam/Mercer/Attachments/Asia

Participant profile List of contributors The following 370 organisations contributed to the 2020 Australian Benefits Review. 3M Australia Aquila Resources 7-Eleven Aristocrat Technologies Australia A. Menarini Australia Arrow Electronics Australia Abbott Australasia ARTC AbbVie Ascender Accenture Australia* Aspen Australia Acrux DDS Astellas Pharma Australia ADCO Constructions Astrazeneca Adelaide Brighton AT&T Global Network Services Australia* Adobe Systems Australia* ATCO Australia AECOM Australia Aurizon Holdings Agilent Technologies Ausenco AGL AusGroup AIA Australia Australian Premium Iron Management Akamai Technologies Netherlands Australian Turf Club Alliance Mineral Asset Autodesk* Alliance Mining Commodities AVJennings Amazon* B. Braun Australia AMD Australia* B. Braun Avitum Amdocs Australia* Baker McKenzie Amgen Australia Bausch and Lomb Amway Of Australia Baxter Healthcare APA Group Bayer Apple* Bechtel Australia 2.14 Australian Benefits Review © 2020 Mercer Consulting (Australia) Pty Ltd Participant profile Becton Dickinson Celine Australia* beIN Media Group CenturyLink Technology Australia Besins Healthcare Christian Dior Australia* Biogen Church & Dwight BIS Industries Cipla Bluewaters Power 2 Cisco Systems Australia* Bluewaters Power Services Citrix* Boehringer Ingelheim Clean TeQ Bolton Clarke Cleanaway Boston Scientific Clough Projects Bouygues Construction Australia CNH Industrial Bowen and Pomeroy Cochlear BP Australia Colgate-Palmolive* Brisbane City Council Collins Foods Bristol-Myers Squibb Computershare British -

Aussie Mine 2016 the Next Act

Aussie Mine 2016 The next act www.pwc.com.au/aussiemine2016 Foreword Welcome to the 10th edition of Aussie Mine: The next act. We’ve chosen this theme because, despite gruelling market conditions and industry-wide poor performance in 2016, confidence is on the rise. We believe an exciting ‘next act’ is about to begin for our mid-tier miners. Aussie Mine provides industry and financial analysis on the Australian mid-tier mining sector as represented by the Mid-Tier 50 (“MT50”, the 50 largest mining companies listed on the Australian Securities Exchange with a market capitalisation of less than $5bn at 30 June 2016). 2 Aussie Mine 2016 Contents Plot summary 04 The three performances of the last 10 years 06 The cast: 2016 MT50 08 Gold steals the show 10 Movers and shakers 12 The next act 16 Deals analysis and outlook 18 Financial analysis 22 a. Income statement b. Cash flow statement c. Balance sheet Where are they now? 32 Key contributors & explanatory notes 36 Contacting PwC 39 Aussie Mine 2016 3 Plot summary The curtain comes up Movers and shakers The mining industry has been in decline over the last While the MT50 overall has shown a steadying level few years and this has continued with another weak of market performance in 2016, the actions and performance in 2016, with the MT50 recording an performances of 11 companies have stood out amongst aggregated net loss after tax of $1bn. the crowd. We put the spotlight on who these movers and shakers are, and how their main critic, their investors, have But as gold continues to develop a strong and dominant rewarded them. -

The Mineral Industry of Australia in 2012

2012 Minerals Yearbook AUSTRALIA U.S. Department of the Interior February 2015 U.S. Geological Survey THE MINERAL INDUSTRY OF AUSTRALIA By Pui-Kwan Tse Australia was subject to volatile weather in recent years Government Policies and Programs that included heavy rains and droughts. The inclement weather conditions affected companies’ abilities to expand The powers of Australia’s Commonwealth Government are their activities, such as port, rail, and road construction and defined in the Australian Constitution; powers not defined in the repair, as well as to mine, process, manufacture, and transport Constitution belong to the States and Territories. Except for the their materials. Slow growth in the economies of the Western Australian Capital Territory (that is, the capital city of Canberra developed countries in 2012 affected economic growth and its environs), all Australian States and Territories have negatively in many counties of the Asia and the Pacific region. identified mineral resources and established mineral industries. China, which was a destination point for many Australian Each State has a mining act and mining regulations that mineral exports, continued to grow its economy in 2012, regulate the ownership of minerals and the operation of mining although the rate of growth was slower than in previous years. activities in that State. The States have other laws that deal with As a result, Australia’s gross domestic product (GDP) increased occupational health and safety, environment, and planning. at a rate of 3.1% during 2012, which was higher than the All minerals in the land are reserved to the Crown; however, 2.3% rate of growth recorded in 2011.