MENA Real Estate Mar Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Saudi Arabia Infrastructure “Projects Galore”

Disclaimer & Disclosure By accepting this publication you agree to be bound by the foregoing terms and conditions. You acknowledge that KFH Research Limited (“KFHR”) is part of the worldwide Kuwait Finance House Group of subsidiaries and affiliates (KFH Group), each of which is a separate legal entity. KFHR alone is responsible for this publication and for the performance of related services and/or other obligations. The recipient agrees not to make any claim or bring proceedings as regards to this publication or related services and obligations as against any other entity within the KFH Group, or any of their subcontractors, members, shareholders, directors, officers, partners, principals or employees. KFHR has prepared this publication for general information purposes only and this does not constitute a prospectus, offering document or circular or offer, invitation or solicitation to purchase, subscribe for or sell any security, financial product or other investment instrument (“Investments”), or to engage in, lead into, conclude or refrain from engaging in any transaction. In preparing this publication, KFHR did not take into account the investment objectives, financial situation and particular needs of the recipient. Before making an investment decision on the basis of this publication, the recipient needs to make its own independent decision, preferably, with the assistance of a financial and/or legal adviser, in evaluating the Investment in light of its particular investment needs, objectives and financial circumstances. Any Investments discussed may not be suitable for all investors; there are risks involved in trading in or dealing with Investments and it is highlighted that the value, yields, price or income from Investments may go up or down. -

Saudi Arabia Land of Opportunities

SAUDI ARABIA LAND OF OPPORTUNITIES INDUSTRIAL INVESTORS GUIDE My first objective is for our country to be a pioneering and successful global model of excellence, on all fronts, and I will work with you to achieve that The Custodian of The Two Holy Mosques King Salman bin Abdulaziz Al Saud Contents Saudi Vision 2030 8 16 Why Saudi Arabia? 40 Industrial Clusters (IC) Saudi Vision 2030 8 Saudi Arabia Vision 2030 Our Vision for Saudi Arabia is to be the heart of the Arab and Islamic worlds, the investment powerhouse, and the hub beneath our lands. But our real wealth lies in the ambition of our people and the connecting three continents potential of our younger generation. They are our nation’s pride and the architects It is my pleasure to present Saudi Arabia’s of our future. We will never forget how, Vision for the future. It is an ambitious yet under tougher circumstances than today, achievable blueprint, which expresses our nation was forged by collective our long-term goals and expectations determination when the late King Abdulaziz and reflects our country’s strengths and Al-Saud – may Allah bless his soul – united capabilities. All success stories start with the Kingdom. Our people will amaze the a vision, and successful visions are based world again. on strong pillars. The first pillar of our vision is our status as the heart of the Arab and We are confident about the Kingdom’s Islamic worlds. We recognize that Allah the future. With all the blessings Allah has Almighty has bestowed on our lands a gift bestowed on our nation, we cannot help but more precious than oil. -

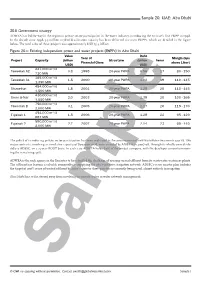

Sample 20. UAE: Abu Dhabi

Sample 20. UAE: Abu Dhabi 20.11 Government strategy ADWEA has led the way in the region in private sector participation in the water industry, introducing the emirate’s first IWPP in 1998. In the decade since 1998, 3.3 million m3/d of desalination capacity has been delivered via seven IWPPs, which are detailed in the figure below. The total value of these projects was approximately USD 13.4 billion. Figure 20.x: Existing independent power and water projects (IWPPs) in Abu Dhabi Value Debt Year of Margin (bps Project Capacity (billion Structure (billion Tenor Financial Close above Libor) USD) USD) 227,000 m³/d Taweelah A2 0.8 1998 20-year PWPA 0.56 17 80 - 150 710 MW 385,000 m³/d Taweelah A1 1.5 2000 20-year PWPA 1.02 19 110 - 145 1,350 MW 454,000 m³/d Shuweihat 1.8 2001 20-year PWPA 1.28 20 110 - 145 1,500 MW 430,000 m³/d Umm al-Nar 2.0 2003 20-year PWPA 1.39 20 100 - 165 1,550 MW 750,000 m³/d Taweelah B 3.1 2005 20-year PWPA 2.17 20 115 - 170 2,000 MW 454,000 m³/d Fujairah 1 1.5 2006 20-year PWPA 1.28 22 65 - 120 887 MW 590,000 m³/d Fujairah 2 2.7 2007 20-year PWPA 2.14 23 65 - 110 2,000 MW The policy of introducing private sector participation has been replicated in the procurement of new wastewater-treatment capacity. Two major contracts, involving a cumulative capacity of 800,000 m3/d, were awarded by ADWEA in 2007-08, through its wholly owned sub- sidiary ADSSC, on a 25-year BOOT basis. -

Knowledge and Attitude of Stroke Among Saudi Population in Riyadh, Kingdom of Saudi Arabia

International Journal of Academic Scientific Research ISSN: 2272-6446 Volume 5, Issue 1 (February - March 2017), PP 149-157 www.ijasrjournal.org Knowledge and Attitude of Stroke Among Saudi Population in Riyadh, Kingdom of Saudi Arabia Muteb Khadran AlOtaibi 1, Fawaz Fahad AlOtaibi 2, Yara Osama AlKhodair 3 , Eiman Mohammed Falatah 4, Haneen Ali AlMutairi 5 1Neurologist Assistant Consultant/King Abdulaziz Medical City/National Guard Health Affairs -Riyadh, Saudi Arabia 2Medical Intern/College of Medicine/ Majmaah University -Riyadh, Saudi Arabia 3Medical Intern/College of Medicine/ King Saud bin Abdulaziz for Health Science University -Riyadh , Saudi Arabia 4Medical Resident /College of Medicine/ King Abdulaziz University -Jeddah , Saudi Arabia 5Medical Intern/ Batterjee Medical College -Jeddah , Saudi Arabia ABSTRACT Background: A stroke occurs when the blood supply to the brain is either interrupted or reduced. When this occurs, the brain does not get enough oxygen or nutrients which cause brain cells to die 2. In 2009, stroke was proclaimed as the underlying cause of death in 128,842 persons in the US, resulting in the rate of 38.9 deaths per 100,000 population.There are two broad types of stroke: ischemic and hemorrhagi 4. The risk factors for stroke are categorized into two principal subdivisions of risk factors: First; The Modifiable Risk factors, which are known to be adjustable with effort and proper knowledge, e.g., smoking and obesity. The other subtype is The Non-modifiable Risk Factors, such as age and positive family history. Aims: To measure the knowledge and attitude of stroke among Riyadh city population, along with determining their source of information and the reliability of these sources. -

Publication.Pdf

In The Name Of Allah, The Most Merciful, The Most Compassionate Arriyadh holds a strategic and pivotal role as the capital of the Kingdom of Saudi Arabia which is the birthplace of the Message of Prophet Mohammed (Peace be upon Him) and the location of the Two Holy Mosques. The dynamic capital hosts diplomatic, Islamic, political, economic, financial, trade, scientific, technological and educational institutions and is a fast developing national, regional and international center. Arriyadh is also a hub of administration with national cultural and heritage bodies and activities. the Custodian of the Two Holy Mosques King Salman Bin Abdulaziz (may God bless him) has over many decades actively supported Arriyadh and its remarkable development. Today, with his Crown Prince, Deputy Prime Minister, Minister of Interior; and the Deputy Crown Prince and Defence Minister; King Salman is ably guiding the development of the Kingdom, its capital and provinces and ensuring the welfare, security and prosperity of the nation’s population. Evidence of this is seen in the range of visionary development and infrastructure projects, which are helping to transform the Kingdom and the wider region. The development process in Arriyadh does not focus on specific areas or sectors. Rather it embraces a wide and comprehensive range of projects and needs. These include ambitious programs in transportation. The King Abdulaziz Public Transport Project in Arriyadh City is the largest of its kind and will provide a network of metro and bus services in the capital. The King Khaled International Airport Development Project will considerably expand passenger and airfreight capacity; and national and regional projects to develop railroad and road networks will soon offer remarkable improvements in transportation within the Kingdom and GCC. -

Saudi Arabia – Industrial Sector Overview August 2016

Saudi Arabia – Industrial Sector Overview August 2016 WWW.JEG.ORG.SA Saudi Arabia – Industrial Sector Overview Report, 2016 TABLE OF CONTENTS Executive Summary 06 1. Introduction 07 2. Saudi Arabia – Industry Overview 08 2.1 Industry 2020: The National Industrial Strategy 08 2.2 National Transformation Program 2020 09 3. Construction & Cement 10 3.1 Construction 10 3.1.1 Infrastructure Construction 12 3.1.2 Office Construction 12 3.1.3 Building Sector Construction 13 3.1.4 Oil & Gas Sector Construction 14 3.1.5 Power & Water Sector Construction 14 3.1.6 Industrial Construction 15 3.1.7 Retail Construction 15 3.1.8 Hospitality Construction Market 16 3.2 Top Construction Players in the Saudi Arabian Market 17 3.3 Construction Industry Drivers and Constraints 18 3.4 Regulatory Reforms in Construction Sector in Saudi Arabia 18 3.4.1 Green Building Regulations 18 3.4.2 Restrictions on Working Hours 19 3.5 SWOT Analysis 19 3.6 Cement 19 3.6.1 Major Market Players 21 3.6.2 Cement Sector – Issues 21 3.6.3 SWOT Analysis 22 4. Petrochemicals & Refineries 23 4.1 Petrochemicals 23 4.1.1 Major Market Players 24 4.1.2 SWOT Analysis 26 4.2 Refining 26 4.2.1 SWOT Analysis 27 5. Mining & Metals 28 5.1 Major Market Players 29 5.2 SWOT Analysis 29 6. Regulations and Ease of Doing Business 30 Saudi Arabia – Industrial Sector Overview Report, 2016 2 7. Industry – Outlook 31 7.1 Non-oil Sector Growth Contracts 31 7.2 Implications of Global Oil Market for Saudi Arabia 31 7.3 USD 4 Trillion Investment Needed to Sustain Job Demand in Non-oil Economy 31 7.4 Privatization and an Open Stock Exchange 31 8. -

Case Study: Gate Towers, Abu Dhabi

ctbuh.org/papers Title: Case Study: Gate Towers, Abu Dhabi Authors: Gurjit Singh, Chief Development Officer, Aldar Properties Hossam Eldin Elsouefi, Senior Project Manager, Aldar Properties Peter Brannan, Managing Director, Arquitectonica Subjects: Architectural/Design Building Case Study Keywords: Construction Design Process Façade Skybridges Publication Date: 2013 Original Publication: CTBUH Journal, 2013 Issue IV Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Gurjit Singh; Hossam Eldin Elsouefi; Peter Brannan About the Council The Council on Tall Buildings and Urban Habitat, based at the Illinois Institute of CTBUH Journal Technology in Chicago, is an international International Journal on Tall Buildings and Urban Habitat not-for-profi t organization supported by architecture, engineering, planning, development, and construction professionals. Founded in 1969, the Council’s mission is to disseminate multi-disciplinary information on Tall buildings: design, construction, and operation | 2013 Issue IV tall buildings and sustainable urban environments, to maximize the international interaction of professionals involved in creating Case Study: Gate Towers, Abu Dhabi the built environment, and to make the latest knowledge available to professionals in a useful Designing Tall to Promote Physical Activity in China form. The Monadnock Building, Technically Reconsidered The CTBUH disseminates -

How Benchmarking Can Support the Selection, Planning and Delivery of Nuclear Decommissioning Projects

This is a repository copy of How benchmarking can support the selection, planning and delivery of nuclear decommissioning projects. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/117185/ Version: Accepted Version Article: Invernizzi, DC, Locatelli, G orcid.org/0000-0001-9986-2249 and Brookes, NJ (2017) How benchmarking can support the selection, planning and delivery of nuclear decommissioning projects. Progress in Nuclear Energy, 99. pp. 155-164. ISSN 0149-1970 https://doi.org/10.1016/j.pnucene.2017.05.002 (c) 2017, Elsevier Ltd. This manuscript version is made available under the CC BY-NC-ND 4.0 license http://creativecommons.org/licenses/by-nc-nd/4.0/ Reuse Items deposited in White Rose Research Online are protected by copyright, with all rights reserved unless indicated otherwise. They may be downloaded and/or printed for private study, or other acts as permitted by national copyright laws. The publisher or other rights holders may allow further reproduction and re-use of the full text version. This is indicated by the licence information on the White Rose Research Online record for the item. Takedown If you consider content in White Rose Research Online to be in breach of UK law, please notify us by emailing [email protected] including the URL of the record and the reason for the withdrawal request. [email protected] https://eprints.whiterose.ac.uk/ Please cite this as Diletta Colette Invernizzi, Giorgio Locatelli, Naomi J. Brookes, How benchmarking can support the selection, planning and delivery of nuclear decommissioning projects, Progress in Nuclear Energy, Volume 99, August 2017, Pages 155-164, https://doi.org/10.1016/j.pnucene.2017.05.002. -

Saudi Arabia HVAC-R Market Outlook, 2021

Saudi Arabia HVAC-R Market Outlook, 2021 Market Intelligence . Consulting Table of Contents S. No. Contents Page No. 1. Saudi Arabia HVAC-R: Key Projects 5 2. Saudi Arabia Thermal Insulation Market Outlook 12 2.1. Market Size & Forecast 2.1.1. By Value 13 2.2. Market Share & Forecast 2.2.1. By Type 14 2.2.2 By Application 15 3. Saudi Arabia District Cooling Market Outlook 16 3.1. Market Size & Forecast 3.1.1. By Value & Volume 17 4. Saudi Arabia Refrigeration Market Outlook 19 4.1. Market Size & Forecast 4.1.1. By Value 20 5. Saudi Arabia HVAC-R Market Outlook 21 5.1. Market Size & Forecast 5.1.1. By Value 23 5.2. Market Share & Forecast 5.2.1. By Region 25 6. Sustainability and Energy Saving in HVAC-R Saudi Arabia Market 30 7. About Us & Disclaimer 37 2 8. About HVACR Expo Saudi 38 © TechSci Research List of Figures Figure No. Figure Title Page No. Figure 1: Saudi Arabia GDP, 2013-2019F (USD Billion) 6 Figure 2: Saudi Arabia Sector-wise Construction Spending Share, 2014 6 Figure 3: Saudi Arabia Thermal Insulation Market Size, By Value, 2011-2021F (USD Million) 13 Figure 4: Saudi Arabia Thermal Insulation Market Share, By Type, By Value, 2015 & 2021F 14 Figure 5: Saudi Arabia Electricity Consumption Share, By Sector, By Value, 2014 14 Figure 6: Saudi Arabia Thermal Insulation Market Share, By Application, By Value, 2015 & 2021F 15 Saudi Arabia District Cooling Market Size, By Value (USD Billion), By Volume (Million Figure 7: 17 TR), 2011-2021F Figure 8: Saudi Arabia District Cooling Market Share in GCC Region, By Value, 2015 18 Figure -

Sustainable Desirable Reliable

SUSTAINABLE DESIRABLE RELIABLE ALDAR PROPERTIES ANNUAL REPORT 2020 About Us Aldar Properties PJSC is the leading real estate SUSTAINABLE CONTENTS We aim to create a business culture where STRATEGIC REPORT developer, manager and owner in Abu Dhabi and sustainability is at the heart of everything we 2 Financial Highlights do, and where the concept of sustainability 4 Highlights of 2020 informs the way we operate, collaborate, through its iconic developments, it is one of the At a Glance innovate and grow. Our responsibility towards 8 most well known in the United Arab Emirates our stakeholders, the community, and the 10 Chairman’s Statement environment will continue to drive our business 12 Chief Executive Officer’s and the wider Middle East region. decisions and long-term value creation. Statement Statement 14 Why Abu Dhabi? Read more on page 20. 20 Case Studies Since Aldar was established, it has 26 Business Model continued to shape and enhance the DESIRABLE 28 Our Strategy urbanisation of the UAE’s capital city Customers are at the heart of all aspects of our 32 Our Strategic Themes by delivering desirable destinations business. Our mission is to create exceptional 42 Sustainability where communities can work, live and and memorable experiences that maximise 48 Operational Review value for all customers and outperform their visit. Those destinations include Yas 76 Financial Review Island, Reem Island, Al Raha Beach, expectations. We are engaged with our 80 EPRA Reporting Saadiyat Island and now Mina Zayed. customers in all areas of the customer journey from design and development, to purchase 84 Historical Financial Performance and handover to ensure a better process and 86 Risk Management increased satisfaction. -

List of Projects

084-CB-QMS / EMS / OHSMS ISO 9001:2015, ISO 14001:2015 & OHSAS 18001:2007 01-26 01 02 03 05 07 08 09 10 11 13 14 15 24 25 PAGE 01 PAGE 02 PAGE 03 PAGE 04 Abi Baker El Siddique Road Riyadh, KSA Abu Dhabi International Airport - Midfield Terminal Building Abu Dhabi, UAE ADIC Development Tower Abu Dhabi, UAE ADNIC Project Abu Dhabi, UAE ADNOC 7010C1 - Ruwais Housing Complex Expansion Phase IV, New Water Pipeline Abu Dhabi, UAE ADNOC New Medical Centre at Khalidiya Villas Abu Dhabi, UAE Al Bustan Street North (P007 C7 P2) Doha, Qatar Al Furjan Dubai, UAE Al Mafraq Interchange Abu Dhabi, UAE Al Marjan Island Development for Island 3 & 4 Ras Al Khaima, UAE Al Maryah Island Infrastructure Abu Dhabi, UAE Al Ra'idah Housing Complex at Jeddah Riyadh, KSA Al Reef Villas Abu Dhabi, UAE Al Reem Island Development, Plot 4, Central Business District of Plot RT-4-C33, Abu Dhabi, UAE C34, C38 and C39 ADNOC Consultancy Agreement Abu Dhabi, UAE Chilled Water Piping Network at Sector 2 & 3, Canal South & North Side Abu Dhabi, UAE Tamouh, Reem Island Danet Abu Dhabi District Cooling Works Abu Dhabi, UAE Development of Eastern Part of King Abdullah Road Riyadh, KSA Development of Roads in Dubai & All Infrastructure Works Dubai, UAE Dragon Mart Dubai, UAE Eastern Part of King Abdullah Road (P2B1) Riyadh, KSA Eastern Province - Water Transmission System Dammam, KSA Empower Project Dubai, UAE EPC Project with ARAMCO at Eastern Province Riyadh, KSA Falcon Eye Project in 7089 Drive 1 Zone D1 & D2 Abu Dhabi, UAE PAGE 05 Fire Station at Al Meena Abu Dhabi, UAE Ibn Battuta Mall Expansion - E4 & E5 Buildings Dubai, UAE ICAD Project, 992 Abu Dhabi, UAE Infrastructure Project in West Bank Palestine Jerusalem, Palestine Internal Roads and Services in Al Rahba City Abu Dhabi, UAE Lusail Commercial Boulevard - Public Realm Doha, Qatar Mafraq to Al Ghwaifat Border Post Highway Section No. -

Urgent Action

Further information on UA: 175/07 Index: MDE 23/002/2013 Saudi Arabia Date: 07 January 2013 URGENT ACTION SRI LANKAN AT RISK OF EXECUTION IN SAUDI ARABIA After exhausting all of her appeals, Rizana Nafeek is at imminent risk of execution in Saudi Arabia for a crime she allegedly committed while under the age of 18. Aged only 17 years at the time, Sri Lankan domestic worker Rizana Nafeek was arrested in May 2005 on charges of murdering an infant in her care. On 16 June 2007, she was sentenced to death by a court in Dawadmi, a town west of the capital Riyadh. The sentence was subsequently upheld by the Court of Cassation and sent for ratification by the Supreme Judicial Council. However, it was sent back to the lower court for further clarification. The case went back and forth until on or around 25 October 2010, when the Supreme Court in Riyadh upheld the death sentence. The case was then sent to the King for ratification of the death sentence. Recent media reports indicate that the family of the infant who died have refused to pardon her and her execution is now imminent. Rizana Nafeek had no access to lawyers either during her pre-trial interrogation or at her first trial. She initially “confessed” to the murder during interrogation, but has since retracted this account. Rizana Nafeek says she was forced to make the “confession” under duress following a physical assault. The man who translated her statement was not an officially recognized translator and it appears that he may not have been able to adequately translate between Tamil and Arabic.