What Your Car Really Costs: How to Keep a Financially Safe Driving Record

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Installation for Lexus IS 350 & GS 350 PN-11898, 11935

BORLA PERFORMANCE INDUSTRIES 500 Borla Drive Johnson City TN, 37604-7523 805-986-8600 Installation for Lexus IS 350 & GS 350 PN-11898, 11935 ***** Please compare the parts in the box with the bill of materials provided ***** to assure that you have all the parts necessary for this installation. These instructions have been written to help you with the installation of your Borla Performance Exhaust System. Please read this document com- pletely before beginning the installation of your system. To ensure this part number fits your specific model year, please visit our website for the latest model year listings at www.BORLA.com Thank you for purchasing a Borla Performance Rear Section Exhaust System. Borla Performance Rear Section (PN-11898) is designed for the Lexus IS 350 equipped with a 3.5L V6 engine, automatic transmission. Borla Performance Rear Section (PN-11935) is designed for the Lexus GS 350 equipped with a 3.5L V6 engine, automatic transmission. Borla Performance Industries recommends that an exhaust shop or professional after market parts installer, who has all the necessary equipment, tools and experienced personnel needed for proper installation, should perform the installation of this system. However, if you decide to perform the installation, we recommend someone should help you. Ensure the installer uses all under car safety precautions including eye protection. Please take time to read and understand the following… By installing your Borla Performance Exhaust System, you indicate that you have read this document and you agree with the terms stated below. It is the responsibility of the purchaser to follow all installation instruction guidelines and safety procedures supplied with your Borla Performance Exhaust System. -

Dodge/Eagle/Mitsubishi/Plymouth 1990-2005 99-7001

INSTALLATION INSTRUCTIONS FOR PART 99-7001 APPLICATIONS See application list inside WIRING & ANTENNA CONNECTIONS (sold separately) Dodge/Eagle/Mitsubishi/Plymouth 1990-2005 Wiring Harness: 99-7001 • 70-1743 • 70-7001 KIT FEATURES • 70-7003 • Single DIN radio provision Antenna Adapter: • Equalizer provision • Not required KIT COMPONENTS TOOLS REQUIRED • A) Radio housing • B) Bracket set #1 • C) Bracket set #2 • D) Bracket set #3 • E) Faceplate • Phillips screwdriver • Cutting tool • F) (2) #6 x 3/4” Phillips flat-head screws • G) Filler bar • H) Equalizer dummy plate • Socket wrench A B C D CAUTION: Metra recommends disconnecting the negative battery terminal before beginning any E F G H installation. All accessories, switches, and especially air bag indicator lights must be plugged in before reconnecting the battery or cycling the ignition. NOTE: Refer to the instructions included with the REV. 8/13/2014 INST99-7001 REV. aftermarket radio. METRA. The World’s best kits.™ 1-800-221-0932 metraonline.com © COPYRIGHT 2004-2014 METRA ELECTRONICS CORPORATION 99-7001 Applications Table of Contents DODGE MITSUBISHI (continued) Dash Disassembly Colt ...................................... 1993-1995 Mirage ................................. 1993-1996 – Dodge Colt/Eagle Summit 1993-1995, Mitsubishi Mirage 1993-1996 .................3 Stealth ................................. 1991-1996 Mirage ................................. 1997-2002 – Dodge Stealth 1991-1996, Mitsubishi 3000GT 1991-1998 ..................................4 Montero .............................. -

The Lexus Range Experience Amazing

THE LEXUS RANGE EXPERIENCE AMAZING Since the launch of the LS 400 sedan in 1989, Lexus has become a synonym for exceptional quality and incredibly refined luxury cars. Determined to offer more than this, recently we’ve launched a new generation of vehicles: cars that stand out from the crowd and defy convention. Models like the exciting new UX compact crossover and the provocative yet elegant ES executive sedan. Based on a uniquely Japanese aesthetic of harmony without compromise, Lexus design is now more distinctive and single-minded than ever. However, head turning looks would be nothing without incredible performance. Inspired by the iconic Lexus LFA supercar that was launched in 2010, our ‘Master Drivers’, have worked tirelessly to identify and articulate the unique flavour of driving excitement. With this hard won knowledge we’ve now enhanced the precise and elegant nature of every Lexus with a sizeable dose of adrenaline: creating an exhilarating new driving experience that starts when you approach a car like the LC luxury coupé, and continues as long as you drive and cherish it. Unsurprisingly, technology plays a huge role in our work. We see innovation as a never-ending process, and are committed to anticipating future needs and desires. This approach has led to major automotive breakthroughs like the world’s first Self-Charging Hybrid in 2004 – the RX 400h – and now Multi Stage Hybrid that powers the LS 500h and LC 500h. Despite our intense focus on the future, we’re immensely proud of the world-class build quality of our cars, which is overseen by our ‘Takumi’ artisans. -

2012 MODEL VIN CODES This VIN Chart Is Available Online At

2012 MODEL VIN CODES This VIN chart is available online at www.mitsubishicars.com. Select “Owners”, ⇒ “Support”, ⇒ “VIN Information”, then select the appropriate year. Use this chart to decode Vehicle Identification Numbers for 2012 model year MMNA vehicles. VEHICLE IDENTIFICATION NUMBER 4 A 3 1 K 2 D F * C E 123456 1. Country of Mfg. 12 − 17 Plant Sequence No. 4 = USA (MMNA) J = Japan (MMC) 2. Manufacturer 11. Assembly Plant A = Mitsubishi E = Normal (USA) U = Mizushima 3. Vehicle Type Z = Okazaki 3 = Passenger Car 4 = Multi−Purpose Vehicle 10. Model Year 4. Restraint System C = 2012 All with Front Driver and Passenger Air Bags Passenger Car 1 = 1st Row Curtain + Seat Air Bags 9. Check Digit 2 = 1st & 2nd Row Curtain + Seat Air Bags 7 = Seat Mounted Air Bags MPV up to 5,000 lbs GVWR 8. Engine/Electric Motor A = 1st & 2nd Row Curtain + Seat Air Bags F = 2.4L SOHC MIVEC (4G69) MPV over 5,000 lbs GVWR S = 3.8L SOHC (6G75) J = 1st & 2nd Row Curtain + Seat Air Bags T = 3.8L SOHC MIVEC (6G75) U = 2.0L DOHC MIVEC (4B11) 5 & 6. Make, Car Line & Series V = 2.0L DOHC TC/IC MIVEC (4B11) B2 = Mitsubishi Galant FE (Fleet Package) W = 2.4L DOHC MIVEC (4B12) B3 = Mitsubishi Galant ES/SE X = 3.0L MIVEC (6B31) H3 = Mitsubishi RVR ES/SE (FWD) (Canada only) J3 = Mitsubishi RVR SE (4WD) (Canada only) 1 = 49Kw Electric Motor (Y4F1) J4 = Mitsubishi RVR GT (4WD) (Canada only) K2 = Mitsubishi Eclipse GS (M/T) 7. Type K3 = Mitsubishi Eclipse GT A = 5−door Wagon/SUV (Outlander, Outlander Sport) K5 = Mitsubishi Eclipse GS (A/T) / GS Sport / SE D = 3−door Hatchback -

Processing End-Of-Life Vehicles: a Guide for Environmental Protection, Safety and Profit in the United States-Mexico Border Area

Processing End-of-Life Vehicles: A Guide for Environmental Protection, Safety and Profit in the United States-Mexico Border Area JULY 2017 U.S. Environmental Protection Agency (EPA) Office of Resource Conservation and Recovery EPA530-R-15-007 epa.gov/border2020 Contents Introduction ................................................................1 Purpose of This Guide .......................................................1 Overview of an End-of-Life Vehicle ...........................................2 Scrap Vehicle and Metal Recovery Operations ................................2 1. Accepting and Storing Discarded Vehicles .............................2 2. Removing Hazardous Materials ........................................3 3. Dismantling Vehicles for Usable or Recyclable Parts ....................4 4. Storing Vehicle Hulks ..................................................4 5. Storing Hazardous Fluids and Materials ................................5 6. Crushing Vehicle Hulks ................................................5 Responsible Disposal ........................................................6 Cost Recovery ..............................................................6 Health, Safety and Security. .7 Worker and Public Safety ................................................7 Environmental Health and Safety ........................................7 Site Security ............................................................8 Industry Standards and Additional Guidance .................................8 For More Information .......................................................8 -

Diamond-Star Motors / Mitsubishi Motors Collection

McLean County Museum of History Diamond-Star Motors / Mitsubishi Motors Collection Processed by Blake Sheehan June 2016 Collection Info VOLUME OF COLLECTION: 5 Boxes COLLECTION DATES: 1979 - 2015 RESTRICTIONS: None REPRODUCTION RIGHTS: Permission to reproduce or publish material in this collection must be obtained in writing from the McLean County Museum of History ALTERNATIVE FORMATS: None OTHER FINDING AIDS: None LOCATION: Archives NOTES: None Brief History Diamond-Star Motors (DSM) opened in Bloomington-Normal in 1988 to expand the Mitsubishi and Chrysler manufacturing capacity in America. DSM became a result of the lasting past relationship between Mitsubishi and Chrysler that dated back to 1970 when Mitsubishi was able to sell their first products in the United States through Chrysler. DSM became a 50/50 joint venture between both companies, splitting both investment and profits equally. The facility was described as representing the best in Japanese and American plant technology to help produce high class automobiles. DSM also helped provide almost three thousand jobs in production and management Potential employees had to compelte a three month training program before beginning work. Mitsubishi and Chrysler choose Bloomington-Normal area due to the to multiple interstate highways and along with easy access to railroads and air transport. DSM started to produce three new kinds of vehicles: the Mitsubishi Eclipse, the Plymouth Laser, and the Eagle Talon during its first few years and the 100,000th car rolled off the line on January 22, 1990. In 1991, Mitsubishi took sole ownership of the plant by purchasing Chrysler’s interest. By 1995, Mitsubishi had renamed DSM to Mitsubishi Motors Manufacturing of America (MMMA) reflecting Mitsubishi's total ownership. -

Trends in the Static Stability Factor of Passenger Cars, Light Trucks, and Vans

DOT HS 809 868 June 2005 NHTSA Technical Report Trends in the Static Stability Factor of Passenger Cars, Light Trucks, and Vans This document is available to the public from the National Technical Information Service, Springfield, Virginia 22161 The United States Government does not endorse products or manufacturers. Trade or manufacturers’ names appear only because they are considered essential to the object of this report. Technical Report Documentation Page 1. Report No. 2. Government Accession No. 3. Recipient’s Catalog No. DOT HS 809 868 4. Title and Subtitle 5. Report Date June 2005 Trends in the Static Stability Factor of Passenger Cars, Light Trucks, and Vans 6. Performing Organization Code 7. Author(s) 8. Performing Organization Report No. Marie C. Walz 9. Performing Organization Name and Address 10. Work Unit No. (TRAIS) Office of Regulatory Analysis and Evaluation Planning, Evaluation and Budget 11. Contract or Grant No. National Highway Traffic Safety Administration Washington, DC 20590 12. Sponsoring Agency Name and Address 13. Type of Report and Period Covered Department of Transportation NHTSA Technical Report National Highway Traffic Safety Administration 14. Sponsoring Agency Code Washington, DC 20590 15. Supplementary Notes 16. Abstract Rollover crashes kill more than 10,000 occupants of passenger vehicles each year. As part of its mission to reduce fatalities and injuries, since model year 2001 NHTSA has included rollover information as part of its NCAP ratings. One of the primary means of assessing rollover risk is the static stability factor (SSF), a measurement of a vehicle’s resistance to rollover. The higher the SSF, the lower the rollover risk. -

GM Truck Fire Complaints

11/9/2016 Top 52 Complaints and Reviews about GM Truck Fires Menu Overall Satisfaction Rating ★★☆☆☆☆ Based on 22 ratings out of 52 reviews show rating distribution Compare Car Models Research top Car Models recommendations on ConsumerAffairs Compare Companies Are you this business? Learn about ConsumerAffairs for Brands! 168 people found this page helpful GM Truck Fires Home Automotive Car Models Last updated: 03/27/2016 AdChoices GMC Truck Fire Truck Fire 4X4 Chevy Truck New Pickup Truck GM Truck Fires does NOT participate in the ConsumerAffairs accreditation program. Learn More Consumer Complaints and Reviews pridemore of Hemet, CA on March 22, 2016 ★☆☆☆☆ Smoke starts rising from dashboard, nothing electrical on, no AC, no radio, nothing. Having paid $600 per month for 5 years on the only new vehicle ever purchased I am left with the notice from GMC that I am out of luck and I am left with a useless piece of junk. Victoria, TX Tow Truck 24/7 Car & Truck Towing Services. Call Our Capable Fleet Today! allanswreckerservice.com Helpful? Yes No s of Toronto, ON on Oct. 26, 2015 ★★☆☆☆ Bought this van 6 weeks ago (used from a dealer - as is). Had it certified and emissions passed. Driven last at 5 PM on Friday. 1 AM Sunday it caught fire all by itself on our driveway. Thank goodness a neighbor saw it. Complete loss also fully destroyed our Ford Escape... Thank goodness it was not near the house or any neighbors property. Very, very upsetting... https://www.consumeraffairs.com/automotive/gm_truck_fires.html 1/10 11/9/2016 Top 52 Complaints and Reviews about GM Truck Fires Menu Man Cheats Credit Score 1 simple trick & my credit score jumped 217 pts. -

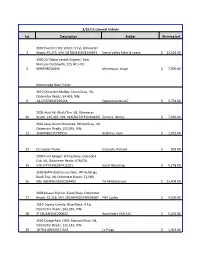

White, 5 Cyl, Odometer Reads

2/25/15 General Vehicle Lot Description Bidder Winning bid 2007 Hummer H3: White, 5 Cyl, Odometer 3 Reads: 97,273, VIN: 5GTDN13E678149873 Sierra Valley Fleet & Lease $ 12,501.00 1990 25' Mako Vessel: Engines: Twin Mercury Outboards, 225 HP, HID: 4 MRKP0803G990 Montequin, Jorge $ 7,900.00 Homemade Boat Trailer 2010 Chevrolet Malibu: Silver/Gray, V6, Odometer Reads: 54,453, VIN: 9 1G1ZC5EB9AF296164 Ezgoautosales LLC $ 5,754.00 2005 Audi A6: Black/Tan, V8, Odometer 10 Reads: 125,465, VIN: WAUDL74F45N108435 Zamora, Alvaro $ 7,026.00 2001 Jeep Grand Cherokee: White/Gray, V6, Odometer Reads: 152,095, VIN: 11 1J4GX48S21C736553 Arellano, Juan $ 1,952.00 12 EZ Loader Trailer Elizondo, Richard $ 801.00 2009 Ford Ranger: White/Gray, Extended Cab, V6, Odometer Reads: 678,076, 14 VIN:1FTYR14E59PA11021 SoCal Recycling $ 4,278.00 2009 BMW 650i Convertible: White/Beige, Black Top, V8, Odometer Reads: 72,589, 16 VIN: WBAEB53569CX64402 Tri-M-Motorcars $ 23,404.00 1998 Nissan Skyline: Silver/Gray, Odometer 17 Reads: 32,226, VIN: 1K1AAWDD19K001587 PNP Cycles $ 4,300.00 2010 Toyota Corolla: Blue/Black, 4 Cyl, Odometer Reads: 162,939, VIN: 18 2T1BU4EE0AC200652 AutoSmart USA, LLC $ 5,201.00 2003 Dodge Ram 1500: Maroon/Gray, V8, Odometer Reads: 121,142, VIN: 19 1D7HA18NX3S371543 La Pulga $ 1,901.00 2008 Nissan Altima: Silver/Grey, 4 Cyl, Odometer Reads: 31,527, VIN: 20 1N4AL21E48N555197 Ezgoautosales LLC $ 6,667.00 2008 GMC Acadia: White/Brown, V6, VIN: 21 1GKEV33738J220857 Double w Truck & Trailer Sales Iinc. $ 5,001.00 2010 Kawasaki Brute Force ATV: Black, -

Toyota Gear Shift/Select Cable

INDEX PAGES TOYOTA 1 ~ 53 NISSAN 54 ~ 91 MAZDA 92 ~ 104 HINO 105 ~ 115 ISUZU 116 ~ 137 MITSUBISHI 138 ~ 160 PROTON 161 ~ 164 DAIHATSU 165 ~ 172 SUZUKI 173 ~ 180 HONDA 181 ~ 193 SUBARU 194 ~ 195 HYUNDAI 196 ~ 199 DAEWOO & KIA & SSANGYONG 200 ~ 203 AMERICAN & EUROPEAN VEHICLES 204 ~ 212 MOTORCYCLES 213 ~ 215 KUBOTA,TRACTOR & FORK LIFT 216 ~ 218 OTHERS 219 ~ 221 CABLES FOR SOUTH AFRICA MAKET 222 ~ 229 ADDITIONAL ITEMS 230 TOYOTA OEM NUMBER ICI NUMBER MODEL TOYOTA ACCELERATOR CABLE 35520-12050 CATY123 AE 8# 35520-12072 CATY145 KE70 ATM 81.08- 35520-12110 CATY124 TE 7# 35520-12200 CATY158 35520-12201 CATY158 35520-12240 CATY126 HILUX LN85/106 88-92, AE101, AE92, AT171 35520-12300 CATY148 AE100,101,110 4FC 91.08- 35520-12310 CATY151 COROLLA AE101 4A-FE 91.06-93.05 35520-12370 CATY122 35520-12390 CATY150 COROLLA AE101 4A-FE 93.05- , AE102,111 1991-1995 RHD 35520-12391 CATY150 COROLLA AE101 4A-FE 93.05- , AE102,111 1991-1995 RHD 35520-16090 CATY147 EE101,92.05-95.05,EP82 3F .92.01- 35520-20070 CATY141 CRESSIDA 35520-28011 CATY133 35520-30030 CATY146 MS112,122,132,133 8MX73 84.08- 35520-33010 CATY217 CAMRY SXV10# 2.2L 5S-FE DOHC 16V MPFI 4CYL 4SP AUTO, VCV10, MCV10 ATM 1992-2001 35520-33050 CATY234 AVALON XL,XLS (MCX10) 1996-1999/CAMRY CE,LE,XLE (MCV20) 1997-2001/SOLARA MCV20 1999-2003/LEXUS ES300 (MCV20) 1996-2001 47616-26040 CATY192 62-CATY002 CATY002 HILUX LN50 62-CATY004 CATY004 HILUX 62-CATY026 CATY026 HILUX HIACE Y SERIES LN80/85/106/130 LHD 92-94 3L 78120-35013 CATY156 78120-90506 CATY159 DYNA RB10 '77-79 78150-06020 CATY220 TOYOTA CAMRY -

Modern Moparmopar ER CAR SL C Y L R U H B

HRYSLE R C O C A F R S C O L U U T B H A U A STR ALI Modern Mopar ER CAR SL C Y L R U H B C O F A I S L O A GHFHPEHURPDUFKR U R TH AUST President Iain Carlin General monthly meetings are held on the FIRST Tuesday of every month at: Vice President Hugh Mortimer The West Adelaide Football Club, 57 Milner Rd, Richmond. Secretary Di Hastwell Treasurer Greg Helbig Events Coordinator Damian Tripodi ACF Coordinator Jason Rowley Regular - $40.00 per year (& quarterly magazine) Events Organisers John Leach Historic Registration - $50 per year (& quarterly magazine) Chris Taylor Historic Registrar Stuart Croser Inspectors North John Eckermann Jason Rowley South Chris Hastwell Charles Lee Central Rob McBride Dave Hocking Sponsorship & Marketing Evan Lloyd Club Library Iain Carlin Editorial / Design Dave Heinrich Webmasters Iain Carlin Dave Heinrich Photography Mary Heath Iain Carlin Lesley Little Ingrid Matschke Damian Tripodi Paris Charles John Antinow Charles Lee Mandy Walsh Contributors Iain Carlin Hugh Mortimer Lesley Little Rick Saxon John Antinow Guy Oakes Stuart Croser Damian Tripodi Source Wikipedia Allpar Hot Rod Car Advice Car & Driver FourWheeler.com DISCLAIMER CarWeekly.co.uk Chrysler, Jeep®, Dodge and Mopar are registered trademarks of FCA LLC and are used with permission by the Chrysler Car Club of South Australia. Enquiries Torqueback is not a commercial publication and is only published in good faith as a newsletter for a not-for-proÀt organisation. Club Mobile The mention of companies, products or services, and the inclusion of advertisements in this magazine does not immediately 0412 426 360 imply any automatic endorsement by the Chrysler Car Club of South Australia or its editorial team. -

Carplay/Android Auto for Lexus Manual

Instruction Manual Apple Car Play RF CABLE RF TOGLE SWITCH TOGLE car-solutions.comLVDS HDMI IN USB / VIDEO CAN Main Specifications For Siri function perfect performance, we use the Car original Mic, if you Audi car is no Mic, there will can not use the siri (Andriod Auto is “OK Google”) function The CarPlay and Android Auto sound source is pass by the Aux in sound path, but when you use the Android Auto for a call ,Please connect the Car BT first. For safety consideration, before Install the Carplay active adapter, please make sure the Power can cable pin is same the original car cable, if not ,do not install. Input Voltage 12~16V DC RF CABLE RF TOGLE SWITCH TOGLE Rated Current 2A Rated Power 24W Material Housing aluminum Connection Wirelesss , USB LVDS HDMI IN USB / VIDEO CAN Control Original car knob control, voice control Working Temperature -20 ~ 80 degree car-solutions.com [email protected] car-solutions.com Components Screen Cable AV,USB Cable ANTENNA Important !! Optional Parts (You need to check the Main harness and GVIF cable type) ? High Type Harness New Type Harness OLD Type Harness Power Cable ? car-solutions.com LVDS Cable [email protected] OLD Type GVIF NEW Type GVIF car-solutions.com Important !! Optional Parts (You need to check the Main harness and GVIF cable type) Package OLD Type OEM Radio Unit Harness #1 Screen Cable OLD Type GVIF Car Model Years Screen Size Main Harness Type GVIF type CT (A10) 2015 ~ 7 inch OLD Type OLD GVIF Type IS (XE30) 2013 7 inch OLD Type OLD GVIF Type Package New Type OEM Radio