Viacom18 Media Private Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Declaration Under Sec 4(4)

KABLE FIRST INDIA PRIVATE LIMITED BANGALORE Declaration under Section 4(4) of the Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable Systems) Regulations, 2017 (No. 1 of 2017) 4(4) a: Target Market : States/Parts of State covered as "Coverage Area" Bangalore 4(4) b: Total Channel carrying capacity Distribution Network Location / States / Parts of State covered Capacity in SD Headend as "Coverage Area" Terms Bangalore Bangalore 543 Kindly Note : 1. Local Channels considered as 1 SD; 2. Consideration in SD Terms is clarified as 1 SD = 1 SD; 1 HD = 2SD; 3. Number of channels will vary within the area serviced by a distribution network location depending upon available Bandwidth Capacity. 4(4) c: List of Channels available on the network: Distribution Network Location: Bangalore Sl. No Service Name COUNT IN SD TERMS SD/HD 1 DD CHANDANA 1 SD 2 ZEE KANNADA 1 SD 3 COLORS KANNADA 1 SD 4 NAPTOL KANNADA 1 SD 5 COLORS SUPER 1 SD 6 STAR SUVARNA 1 SD 7 UDAYA TV 1 SD 8 BHIMA TV 1 SD 9 EXPRESS TV 1 SD 10 ZEE PICTURE 1 SD 11 PUBLIC MOVIES 1 SD 12 COLORS KANNADA CINEMA 1 SD 13 SUVARNA PLUS 1 SD 14 SIRI KANNADA 1 SD 15 UDAYA COMEDY 1 SD 16 UDAYA MOVIES 1 SD 17 PUBLIC MUSIC 1 SD 18 RAJ MUSIX KANNADA 1 SD 19 UDAYA MUSIC 1 SD 20 SUVARNA NEWS 1 SD 21 B TV News 1 SD 22 TV 9 KANNADA 1 SD 23 DIG VIJAY 1 SD 24 PUBLIC TV 1 SD 25 POWER TV 1 SD 26 NEWS18 KANNADA 1 SD 27 PRAJA TV NEWS 1 SD 28 TV 5 KANNADA NEWS 1 SD 29 RAJ NEWS KANNADA 1 SD 30 AAYUSH TV 1 SD 31 CHINTU TV 1 SD 32 ETV BAL BHARAT 1 SD 33 SRI SANKARA 1 SD 34 DD PODHIGAI 1 -

11. Mumbai & Thane

11. MUMBAI & THANE Service Name City BST Silver Gold Sony Mumbai & Thane N Y Y Sony SAB Mumbai & Thane N Y Y Colors Mumbai & Thane N Y Y Rishtey Mumbai & Thane N Y Y Sony PAL Mumbai & Thane N Y Y Shop CJ Mumbai & Thane N Y Y Home Shop 18 Mumbai & Thane Y Y Y I D Mumbai & Thane N Y Y Zoom Mumbai & Thane N N Y Epic Mumbai & Thane N N N ETV Bihar JH Mumbai & Thane N Y Y ETV MP CG Mumbai & Thane N Y Y ETV Rajasthan Mumbai & Thane N Y Y ETV UP UK Mumbai & Thane N Y Y DEN snapdeal tv-shop Mumbai & Thane Y Y Y Sahara One Mumbai & Thane N Y Y DD National Mumbai & Thane Y Y Y DD Rajasthan Mumbai & Thane Y Y Y DD Uttar Pradesh Mumbai & Thane Y Y Y DD Madhya Pradesh Mumbai & Thane Y Y Y DD Bihar Mumbai & Thane Y Y Y Sony MAX Mumbai & Thane N Y Y SONY MAX 2 Mumbai & Thane N Y Y B4U Movies Mumbai & Thane N Y Y Cinema TV Mumbai & Thane N Y Y Multiplex Mumbai & Thane Y Y Y DEN Cinema Mumbai & Thane Y Y Y Filmy Mumbai & Thane N N Y DEN Movies Mumbai & Thane N Y Y AXN Mumbai & Thane N Y Y Comedy Central Mumbai & Thane N Y Y Colors Infinity Mumbai & Thane N Y Y DSN INFO Mumbai & Thane Y Y Y Sony PIX Mumbai & Thane N Y Y Movies Now Mumbai & Thane N N Y Romedy Now Mumbai & Thane N N Y Discovery Turbo Mumbai & Thane N Y Y TLC Mumbai & Thane N Y Y Fashion TV Mumbai & Thane N N Y Food Food Mumbai & Thane N N Y News 18 India Mumbai & Thane N Y Y India TV Mumbai & Thane Y Y Y News 24 Mumbai & Thane N N N Aajtak Tez Mumbai & Thane N Y Y ABP News Mumbai & Thane Y Y Y Aajtak Mumbai & Thane N Y Y News Nation Mumbai & Thane Y Y Y India News Mumbai & Thane Y Y Y DD -

SL.NO CHANNEL LCN Genre STAR PLUS 101 HINDI GEC

SL.NO CHANNEL LCN Genre 1 STAR PLUS 101 HINDI GEC PAY 2 ZEE TV 102 HINDI GEC PAY 3 SET 103 HINDI GEC PAY 4 COLORS 104 HINDI GEC PAY 5 &TV 105 HINDI GEC PAY 6 SAB 106 HINDI GEC PAY 7 STAR BHARAT 107 HINDI GEC PAY 8 BIG MAGIC 108 HINDI GEC PAY 9 PAL 109 HINDI GEC PAY 10 COLORS RISHTEY 110 HINDI GEC PAY 11 STAR UTSAV 111 HINDI GEC PAY 12 ZEE ANMOL 112 HINDI GEC PAY 13 BINDASS 113 HINDI GEC PAY 14 ZOOM 114 HINDI GEC PAY 15 DISCOVERY JEET 115 HINDI GEC PAY 16 STAR GOLD 135 HINDI MOVIES PAY 17 ZEE CINEMA 136 HINDI MOVIES PAY 18 SONY MAX 137 HINDI MOVIES PAY 19 &PICTURES 138 HINDI MOVIES PAY 20 STAR GOLD 2 139 HINDI MOVIES PAY 21 ZEE BOLLYWOOD 140 HINDI MOVIES PAY 22 MAX 2 141 HINDI MOVIES PAY 23 ZEE ACTION 142 HINDI MOVIES PAY 24 SONY WAH 143 HINDI MOVIES PAY 25 COLORS CINEPLEX 144 HINDI MOVIES PAY 26 UTV MOVIES 145 HINDI MOVIES PAY 27 UTV ACTION 146 HINDI MOVIES PAY 28 ZEE CLASSIC 147 HINDI MOVIES PAY 29 ZEE ANMOL CINEMA 148 HINDI MOVIES PAY 30 STAR GOLD SELECT 149 HINDI MOVIES PAY 31 STAR UTSAV MOVIES 150 HINDI MOVIES PAY 32 RISHTEY CINEPLEX 151 HINDI MOVIES PAY 33 MTV 175 HINDI MUSIC PAY 34 ZING 178 HINDI MUSIC PAY 35 MTV BEATS 179 HINDI MUSIC PAY 36 9X M 181 HINDI MUSIC PAY 37 CNBC AWAAZ 201 HINDI NEWS PAY 38 ZEE BUSINESS 202 HINDI NEWS PAY 39 INDIA TODAY 203 HINDI NEWS PAY 40 NDTV INDIA 204 HINDI NEWS PAY 41 NEWS18 INDIA 205 HINDI NEWS PAY 42 AAJ TAK 206 HINDI NEWS PAY 43 ZEE NEWS 207 HINDI NEWS PAY 44 ZEE HINDUSTAN 209 HINDI NEWS PAY 45 TEZ 210 HINDI NEWS PAY 46 STAR JALSHA 251 BENGALI GEC PAY 47 ZEE BANGLA 252 BENGALI GEC PAY 48 COLORS -

Declaration Under Section 4 (4) of the Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No

Version 1.0/2019 Declaration Under Section 4 (4) of The Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No. 1 of 2017) 4(4)a: Target Market Distribution Network Location States/Parts of State covered as "Coverage Area" Bangalore Karnataka Bhopal Madhya Pradesh Delhi Delhi; Haryana; Rajasthan and Uttar Pradesh Hyderabad Telangana Kolkata Odisha; West Bengal; Sikkim Mumbai Maharashtra 4(4)b: Total Channel carrying capacity Distribution Network Location Capacity in SD Terms Bangalore 506 Bhopal 358 Delhi 384 Hyderabad 456 Kolkata 472 Mumbai 447 Kindly Note: 1. Local Channels considered as 1 SD; 2. Consideration in SD Terms is clarified as 1 SD = 1 SD; 1 HD = 2 SD; 3. Number of channels will vary within the area serviced by a distribution network location depending upon available Bandwidth capacity. 4(4)c: List of channels available on network List attached below in Annexure I 4(4)d: Number of channels which signals of television channels have been requested by the distributor from broadcasters and the interconnection agreements signed Nil Page 1 of 37 Version 1.0/2019 4(4)e: Spare channels capacity available on the network for the purpose of carrying signals of television channels Distribution Network Location Spare Channel Capacity in SD Terms Bangalore Nil Bhopal Nil Delhi Nil Hyderabad Nil Kolkata Nil Mumbai Nil 4(4)f: List of channels, in chronological order, for which requests have been received from broadcasters for distribution of their channels, the interconnection agreements -

MRP of Pay Channels , Offered by Broadcasters to Subscriber As Reported to TRAI (New Regulatory Framework) (As on 19Th January 2019) S.No Name of the Broadcaster Sl

MRP of pay channels , offered by broadcasters to subscriber as reported to TRAI (New Regulatory Framework) (as on 19th January 2019) S.No Name of the broadcaster Sl. No Name of the channel Channel logo Reported Genre as Reported Language MRP as per Declared as per new Regulatory New SD or HD framework Regulatory Framework 2017 1 ABP News Network Pvt Limited 1 ABP Ananda News Bengali 0.50 SD 2 ABP Majha News Marathi 0.50 SD 2 AETN 18 Media Pvt Limited 3 The History Channel Infotainment Hindi 3.00 SD 4 FY1 TV18 Infotainment English 0.25 SD 5 FY1 TV18 (HD) Infotainment English 1.00 HD 6 Histroy TV 18 HD Infotainment Hindi 7.00 HD 3 Bangla Entertainment Private 7 AATH GEC Bangla 4.00 SD Limited 8 SONY Marathi GEC Marathi 4.00 SD 4 BBC Global News India Private 9 BBC World News News English 1.00 SD Limited 5 Bennett, Coleman & Company 10 Zoom GEC Hindi 0.50 SD Limited S.No Name of the broadcaster Sl. No Name of the channel Channel logo Reported Genre as Reported Language MRP as per Declared as per new Regulatory New SD or HD framework Regulatory Framework 2017 11 Romedy Now Movies English 6.00 SD 12 MN + Movies English 10.00 HD 13 Mirror Now News English/Hindi 2.00 SD 14 ET NOW News English/Hindi 3.00 SD 15 Times Now News English/Hindi 3.00 SD 16 Romedy Now HD Movies English 9.00 HD 17 Movies Now HD Movies English 12.00 HD 18 MNX HD Movies English 9.00 HD 19 MNX Movies English 6.00 SD 20 Times Now HD News English 5.00 HD 6 Celebrities Management Pvt 21 Travel XP HD Lifestyle English 9.00 HD Limited S.No Name of the broadcaster Sl. -

Entertainment

TVml August 28, 2020 National Stock Exchange of India Limited BSE Limited Exchange Plaza, Plot No. C/1, P J Towers G-Block Bandra-Kurla Complex, Dalal Street Bandra (E) Mumbai - 400051 Mumbai - 400 001 Trading Symbol: TV18BRDCST SCRIP CODE: 532800 Dear Sirs, Sub: Annual Report for the financial year 2019-20 including Notice of Annual General Meeting The Annual Report for the financial year 2019-20, including the Notice convening Annual General Meeting, being sent to the members through electronic mode, is attached. The Secretarial Audit Report of material unlisted subsidiary is also attached. The Annual Report including Notice is also uploaded on the Company's website www.nw18.com. This is for your information and records. Thanking you, Yours faithfully, For TV18 Broadcast Limited c ~~ ~"OrJ . )," ('.i/'. ~ . .-...e:--.-~ l \ I Ratnesh Rukhariyar Company Secretary Encl. As Above TV18 Broadcast Limited (eIN - L74300MH2005PLC281753) Regd. office: First Floor, Empire Complex, 414- Senopoti Sopot Marg, Lower Parel, Mumboi-400013 T +91 2240019000,66667777 W www.nw18.com E:[email protected] CONTENTS 01 - 11 Corporate Overview 01 Information. Entertainment. Impact TV18 is as unique as 02 Driven to Inform 04 Inspired to Involve it is impactful. It blends 06 Brands that Stimulate compelling and insightful 08 Letter to Shareholders news with inspiring and 09 Corporate Information stimulating entertainment; 10 Board of Directors an attribute that makes it 12 - 68 stand out amongst peers Statutory Reports regardless of size or vintage. 12 Management Discussion and Analysis 29 Board’s Report 40 Business Responsibility Report India’s largest News Broadcast network and the third 49 Corporate Governance Report largest player in the Television entertainment space, TV18 has infused into the Media and Entertainment industry a large dose of youthful dynamism. -

Corporate Presentation Media & Investments

Media & Investments Corporate Presentation FY19-20 OVERVIEW 2 Key Strengths Leading Media company in India with largest bouquet of channels (56 domestic channels and 16 international beams), and a substantial digital presence Market-leader in multiple genres (Business News #1, Hindi General News & Entertainment #2 Urban, Kids #1, English #1) Key “Network effect” and play on Vernacular media growth - Benefits of Strengths Regional portfolio across News (14) and Entertainment (9) channels Marquee Digital properties (MoneyControl, BookMyShow) & OTT video (VOOT) provides future-proof growth and content synergy Experienced & Professional management team, Strong promoters 3 Network18 group : TV & Digital media, specialized Print & Ticketing ~75% held by Independent Media Trust, of which RIL is Network18 Strategic Investment the sole beneficiary Entertainment Ticketing & Live Network18 has ~39% stake Digital News Broadcasting Print + Digital Magazines Business Finance News Auto Entertainment News & Niche Opinions Infotainment All in standalone entity Network18 holds ~92% in Moneycontrol. Network18 holds ~51% of subsidiary TV18. Others are in standalone entity. TV18 in turn owns 51% in Viacom18 and 51% in AETN18 (see next page for details) TV18 group – Broadcasting pure-play, across News & Entertainment ENTITY GENRE CHANNELS Business News (4 channels, 1 portal) Standalone entity TV18 TV18 General News Group (Hindi & English) Regional News 50% JV with Lokmat group (14 geographies) IBN Lokmat AETN18 Infotainment (Factual & Lifestyle) 51% subsidiary -

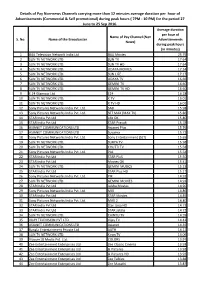

Details of Pay Non-News Channels Carrying More Than 12 Minutes

Details of Pay Non-news Channels carrying more than 12 minutes average duration per hour of Advertisements (Commercial & Self promotional) during peak hours ( 7PM - 10 PM) for the period 27 June to 25 Sep 2016. Average duration per hour of Name of Pay Channel (Non S. No. Name of the Broadcaster Advertisements News) during peak hours (in minutes) 1 B4U Television Network India Ltd B4U Movies 25.79 2 SUN TV NETWORK LTD. SUN TV 17.64 3 SUN TV NETWORK LTD. SUN TV HD 17.64 4 SUN TV NETWORK LTD. UDAYA MOVIES 17.34 5 SUN TV NETWORK LTD. SUN LIFE 17.17 6 SUN TV NETWORK LTD. UDAYA TV 16.66 7 SUN TV NETWORK LTD. GEMINI TV 16.60 8 SUN TV NETWORK LTD. GEMINI TV HD 16.60 9 E 24 Glamour Ltd E24 16.18 10 SUN TV NETWORK LTD. K TV 16.01 11 SUN TV NETWORK LTD. K TV HD 16.01 12 Sony Pictures Networks India Pvt. Ltd. SAB 15.98 13 Sony Pictures Networks India Pvt. Ltd. SET MAX (MAX TV) 15.86 14 STAR India Pvt Ltd Life OK 15.80 15 STAR India Pvt Ltd STAR Pravah 15.78 16 ASIANET COMMUNICATIONS LTD Asianet Plus 15.76 17 ASIANET COMMUNICATIONS LTD Suvarna 15.72 18 Sony Pictures Networks India Pvt. Ltd. Sony Entertainment (SET) 15.65 19 SUN TV NETWORK LTD. SURYA TV 15.58 20 SUN TV NETWORK LTD. CHUTTI TV 15.58 21 Sony Pictures Networks India Pvt. Ltd. PAL 15.54 22 STAR India Pvt Ltd STAR PluS 15.50 23 STAR India Pvt Ltd Movies OK 15.41 24 SUN TV NETWORK LTD. -

Corporate Presentation Media & Investments

Media & Investments Corporate Presentation FY18-19 OVERVIEW 2 Key Strengths Leading Media company in India with largest bouquet of channels (55 domestic channels and 16 international beams), and a substantial digital presence Market-leader in multiple genres (Business News #1, Hindi General News & Entertainment #2 Urban, Kids #1, English #1) Key “Network effect” and play on Vernacular media growth - Benefits of Strengths Regional portfolio across News (14) and Entertainment (8) channels Marquee Digital properties (MoneyControl, BookMyShow) & OTT video (VOOT) provides future-proof growth and content synergy Experienced & Professional management team, Strong promoters 3 Building India’s leading media company 2016+ • OTT video platform, revamp of portals Filling whitespaces, umbrella branding, • Hindi Movie and Music channels thrust on digital • News (TV+Digital) expanded and relaunched • ETV acquisition (Regional News +Entertainment) 2012-2015 • Indiacast setup for distribution of TV bouquet Regional entry to tap vernacular market • NW18 acquired by RIL, corporatization thrust • JVs with Viacom & A+E networks, Forbes 2005-2011 • Invest in Home shopping, Online Ticketing Entry into Entertainment and Digital • News, Opinions & Info portals 1999-2005 • Business News (CNBC cluster) Built core platforms and launched • General News (IBN cluster) flagships • Finance portal (MoneyControl) 4 Network18 group : TV & Digital media, specialized Print & Ticketing ~75% held by Independent Media Trust, of which RIL is Network18 Strategic Investment the sole beneficiary Entertainment Ticketing Network18 has ~39% stake Digital News Broadcasting Print + Digital Magazines Business Finance News Auto Entertainment News & Niche Opinions Infotainment All in standalone entity Infotainment Network18 holds ~51% of subsidiary TV18. TV18 in turn owns 51% in Viacom18 and 51% in AETN18 (see next page for details) Network18 holds ~92% in Moneycontrol. -

Annual Report 2019-20

Annual Report 2019-20 Creating Experiences The Group commissioned India’s largest integrated TV and Digital Newsroom at Mumbai. What’s Inside Corporate Overview 01 Creating Experiences 02 Across Mediums 03 Across Languages 04 Across Screens 05 Across Narratives 06 Across Genres 08 Letter to Shareholders 09 Corporate Information 10 Board of Directors Statutory Reports 12 Management Discussion and Analysis 30 Board’s Report 40 Business Responsibility Report 49 Corporate Governance Report Financial Statements 71 Standalone Financial Statements 121 Consolidated Financial Statements Notice 181 Notice of Annual General Meeting View this report online or download at www.nw18.com A large bouquet of diversified brands, crafted to meet the diverse needs of audiences across regions, cultures, segments, genres and languages, defines the ethos of Network18 Media & Investments Limited (Network18). As one of India’s largest media conglomerates, Network18 has redefined the Media and Entertainment sector of the country, while carving a distinctive niche for itself as a thought leader in the industry. With our finger on the pulse of people across the culturally contrasting milieus of Bharat and India, we remain closely connected with audiences through multiple channels of mediums, languages, platforms, screens, devices and formats. At the heart of this consumer connect lies our ability to align ourselves to the differentiated and evolving aspirations, needs and consumption patterns of people across the country. From News to Entertainment and across TV, Digital and Print, our portfolio of offerings is designed to engage with audiences across segments and genres. We create enriching experiences for them with our quality content that caters as effectively to the premium audiences as it does to the masses. -

Corporate Presentation Media & Investments

Media & Investments Corporate Presentation FY20-21 OVERVIEW 2 Key Strengths Leading Media company in India with largest bouquet of channels (56 domestic channels and 16 international beams), and a substantial digital presence Market-leader in multiple genres (Global top 20 in news pay-apps; top 2 in Digital News in India, #1 Business News channel, top 3 in National News, #2 premium Hindi GEC, Kids #1, English #1) Key “Network effect” and play on Vernacular media growth - Benefits of Strengths Regional portfolio across News (14) and Entertainment (10) channels Marquee Digital properties (MoneyControl, BookMyShow) & OTT video (VOOT) provides future-proof growth and content synergy Experienced & Professional management team, Strong promoters 3 Network18 group : TV & Digital media, specialized Print & Ticketing ~73.15% held by Independent Media Trust, of Network18 Strategic Investment which RIL is the sole beneficiary (total promoter Entertainment holding is 75%) Ticketing & Live Network18 has ~39% stake Digital News Broadcasting Print + Digital Magazines Business Finance News Auto Entertainment News & Niche Opinions Infotainment All in standalone entity Network18 holds ~92% in e-Eighteen Network18 holds ~51% of subsidiary TV18. (Moneycontrol). Others are in standalone TV18 in turn owns 51% in Viacom18 and entity. 51% in AETN18 (see next page for details) TV18 group – Broadcasting pure-play, across News & Entertainment ENTITY GENRE CHANNELS Business News (4 channels, 1 portal) Standalone entity TV18 TV18 General News Group (Hindi & English) Regional News 50% JV with Lokmat group (14 geographies) IBN Lokmat AETN18 Infotainment (Factual & Lifestyle) 51% subsidiary - JV with A+E Networks Entertainment VIACOM18 (inc. Movie production / distribution & OTT) 51% subsidiary - JV with Viacom Inc Regional Entertain. -

List of Ala-Carte Paid Channels

List of Ala-carte Paid channels Total Price Sr. No. Broadcaster Channel Genre Channel type MRP (Rs.) DRP (Rs.) GST (Rs.) (Rs, incl Tax) 1 Disney Bindass Hindi Entertainment SD 0.10 0.10 0.02 0.12 2 TV18 News18 Bangla Bengali SD 0.10 0.10 0.02 0.12 3 TV18 News18 Gujarati Gujarati SD 0.10 0.10 0.02 0.12 4 TV18 News18 Rajasthan Hindi News SD 0.10 0.10 0.02 0.12 5 TV18 News18 Kannada Kannada SD 0.10 0.10 0.02 0.12 6 TV18 News18 Kerala Malayalam SD 0.10 0.10 0.02 0.12 7 TV18 News18 Lokmat Marathi SD 0.10 0.10 0.02 0.12 8 TV18 News18 Tamil Nadu Tamil SD 0.10 0.10 0.02 0.12 9 TV18 News18 Urdu Urdu SD 0.10 0.10 0.02 0.12 10 TV18 News18 Bihar Jharkhand Hindi News SD 0.10 0.10 0.02 0.12 11 TV18 News18 UP UK Hindi News SD 0.10 0.10 0.02 0.12 12 TV18 News18 MPCG Hindi News SD 0.10 0.10 0.02 0.12 13 TV18 News18 Punjab Haryana Himachal Hindi News SD 0.10 0.10 0.02 0.12 14 TV18 News18 Oriya Oriya SD 0.10 0.10 0.02 0.12 15 TV18 MTV Beats Music SD 0.10 0.10 0.02 0.12 16 TV18 News18 India Hindi News SD 0.10 0.10 0.02 0.12 17 TV18 News18 Assam/North East Assamese SD 0.10 0.10 0.02 0.12 18 Zee 24 Ghanta Bengali SD 0.10 0.10 0.02 0.12 19 Zee Zee Bihar Jharkhand Bhojpuri SD 0.10 0.10 0.02 0.12 20 Zee Zee 24 Kalak Gujarati SD 0.10 0.10 0.02 0.12 21 Zee Big Magic Hindi Entertainment SD 0.10 0.10 0.02 0.12 22 Zee Zee News Hindi News SD 0.10 0.10 0.02 0.12 23 Zee Zee Hindustan Hindi News SD 0.10 0.10 0.02 0.12 24 Zee Zee Business Hindi News SD 0.10 0.10 0.02 0.12 25 Zee Zee MPCG Hindi News SD 0.10 0.10 0.02 0.12 26 Zee Zee Rajasthan News Hindi News SD 0.10 0.10