Press Release Adani Ports and Special Economic Zone Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

An Economic Gateway for the Nation

Adani Ports and Special Economic Zone Limited An Economic Gateway for the Nation Thinking big Doing better Everyone has a philosophy or a set of rules they work by. Ours is Thinking big, Doing better. Over the course of 25 years, we discovered that starting a large scale business has served not only us, but also the nation. This in turn has affected millions of lives, making them simpler and better. This is why we think big, so we can do better. Each action we take ripples throughout the society and benefits people in ways we never even dreamt of. Adani Ports and Special Economic Zone Limited is an undisputed leader in the Indian port sector. 1 Adani Ports and Special Economic Zone APSEZ provides seamlessly integrated Exceptional features of APSEZ services across three verticals, i.e. Ports Ports, Logistics and SEZ • Deep water, all-weather, direct berthing • One stop solution for business facilities • Pan-India presence • Large scale mechanisation • Largest integrated infrastructure company • Connectivity to national highway and • Dedicated, committed and passionate rail networks team to provide superior services • Scope for major expansion at our ports • Technology driven system and processes • Operational benchmarks comparable to the best in the world 2 3 Strategic Advantages at Adani Kila - Raipur Patli Kishangarh Mundra Tuna Dahej Dhamra Hazira Vizag Ports Mormugao Terminals ICDs Kattupalli Ennore Vizhinjam Adani Ports: Pioneer on multiple fronts • Single window interface system for • Specialised infrastructure evolved customers that -

Sustainable Growth with Goodness

Annual Report 2018-19 Sustainable Growth with Goodness “Excellence happens not by accident. It is a through our Project SuPoshan. SuPoshan has process. You have to work hard to achieve it” also been recognised at the global stage with - Dr. APJ Abdul Kalam the esteemed Public Affairs Asia (PAA) Gold Standard Award for Corporate Citizenship Our strive to achieve excellence during the (Community Relations). The project also won year in creating sustainable impact on the the silver award at the 53rd SKOCH State grounds echoed the above words of wisdom of Governance Summit 2018 and the from Dr. Kalam. Dainik Jagran CSR Awards for exceptional When we began the journey of Adani contribution towards Public Health. Foundation in 1996, we had set a goal to play Like every year, our teams went out of the the role of a facilitator to help people empower way to help people in times of crisis. One of themselves. Along the journey, aspiration of the devastating natural disasters that struck our beneficiaries and perspiration of our team the country this year was the floods in Kerala, members have been the motivating forces. in August. Within hours of the calamity, our Adani Vidya Mandir (AVM) Ahmedabad and on-ground teams worked relentlessly, Adani Public School Mundra created a participating in rescue coordination and flood benchmark by attaining the NABET relief activities in the worst affected areas. Accreditation under the Quality Council of The team of staff and volunteers, travelled India. AVM Ahmedabad has become the first through nights to remote villages distributing cost-free school in India to receive the NABET thousands of relief kits that included rations, accreditation; APS Mundra is the first school clothes and other necessary supplies. -

Adani Petronet (Dahej) Port Pvt

ADANI PETRONET (DAHEJ) PORT PVT. LTD INTEGRATED MANAGEMENT SYSTEM FORMATS MANUAL 0BMAR/F/003 1BADANI PETRONET DAHEJ PORT – PORT INFORMATION BOOK ADANI PETRONET (DAHEJ) PORT PVT. LTD PORT & TERMINAL INFORMATION BOOK WELCOMES THE MASTER, OFFICERS & CREW OF MV ________________________ Revised dated: 20-12-17 Reviewed By : Capt Vijesh Parasar Issue No : 00 Issued on : 01/07/2016 Approved By : Capt Ashish Singhal Revision No : 01 Page No. : 1 of 12 ADANI PETRONET (DAHEJ) PORT PVT. LTD INTEGRATED MANAGEMENT SYSTEM FORMATS MANUAL TABLE OF CONTENTS INTRODUCTION LETTER .........................................................................................................3 STANDARD MESSAGE – INBOUND VESSEL ..........................................................................4 PORT AND TERMINAL INFORMATION……………………………………………………………………………………………..........................................5 • Port Detail • Weather • VTMS Services at Gulf of Khambhat • Adani Dahej Port Anchorage instructions • Pilot Boarding ground and picking up pilot • Mooring Arrangements • Vessel equipments & mooring winches • Tidal information • Adani Dahej Port at berth Instructions • Security • Services at APDPPL • Charts • Dry cargo handling • Safety • Pollution • Emergency • Website link • Mooring Pattern • Dahej Port Reviewed By : Capt Vijesh Parasar Issue No : 01 Issued on : 01/07/2016 Approved By : Capt Ashish Singhal Revision No : 01 Page No. : 2 of 12 ADANI PETRONET (DAHEJ) PORT PVT. LTD INTEGRATED MANAGEMENT SYSTEM FORMATS MANUAL Dear Captain, We welcome you and crew to Adani Petronet(Dahej) Port Pvt.Ltd A. For your information and compliance, we enclose the following documents. a. Condition of Use Document b. Safety & Pollution Prevention Requirements. c. General Information B. Please note that “CONDITION OF USE” letter is a legal document and is to be filled up, signed, stamped and delivered to the pilot before commencement of Pilotage. The following documents are to be completed and handed over to the Pilot. -

Financial Statements of the Compau:, for the Year Ended March 3 I

adani Renewables August 04, 2021 BSE Limited National Stock Exchange of India Limited P J Towers, Exchange plaza, Dalal Street, Bandra-Kurla Complex, Bandra (E) Mumbai – 400001 Mumbai – 400051 Scrip Code: 541450 Scrip Code: ADANIGREEN Dear Sir, Sub: Outcome of Board Meeting held on August 04, 2021 With reference to above, we hereby submit / inform that: 1. The Board of Directors (“the Board”) at its meeting held on August 04, 2021, commenced at 12.00 noon and concluded at 1.20 p.m., has approved and taken on record the Unaudited Financial Results (Standalone and Consolidated) of the Company for the Quarter ended June 30, 2021. 2. The Unaudited Financial Results (Standalone and Consolidated) of the Company for the Quarter ended June 30, 2021 prepared in terms of Regulation 33 of the SEBI (Listing Obligations and Disclosures Requirements) Regulations, 2015 together with the Limited Review Report of the Statutory Auditors are enclosed herewith. The results are also being uploaded on the Company’s website at www.adanigreenenergy.com. The presentation on operational & financial highlights for the quarter ended June 30, 2021 is enclosed herewith and also being uploaded on our website. 3. Press Release dated August 04, 2021 on the Unaudited Financial Results of the Company for the Quarter ended June 30, 2021 is enclosed herewith. Adani Green Energy Limited Tel +91 79 2555 5555 “Adani Corporate House”, Shantigram, Fax +91 79 2555 5500 Nr. Vaishno Devi Circle, S G Highway, [email protected] Khodiyar, www.adanigreenenergy.com Ahmedabad – 382 421 Gujarat, India CIN: L40106GJ2015PLC082007 Registered Office: “Adani Corporate House”, Shantigram, Nr. -

Integrated Information Management for Operational Excellence

Integrated Information Management for Operational Excellence Presented by Vijendra Pancholi Agenda About Adani Group Need And Solution Mercury(Port Information System) Advantage and Benefits of system 2 Contents Sections About Adani Group Overview Mercury Overview Advantages / Benefits 3 The Adani Group Leading Business Conglomerate with interest in diversified sectors... Resources Logistics Energy Sourcing hydrocarbons from Owning a large network of ports, Leading player in around the world to fuel India’s railways, ships and operate various private sector power generation growth facilities around our ports Resources Logistics Energy • Gas Distribution • Coal Mining • Multi Modal Logistics • Power • Oil & Gas Exploration •Ports • Bunkering • Coal Trading • Special Economic Zones • Grain Silos & Fruits • Edible Oil 4 The Adani Group Adani Group has 3 listed companies…. Adani Enterprises Limited Adani Power Limited Adani Ports & SEZ Limited (AEL) (APL) (APSEZ) 5 Adani Ports Infrastructure Helping India build Port Capacity………………. • Adani initially started its first port at Mundra location. Later on it has aggressively added new Indian & Overseas ports to its portfolio. • Adani Ports is targeting to achieve the mammoth figure of 200 million MT per annum Indian cargo handling by 2020 • In the last fin year Adani Ports (India) handled over 100 Million MT of cargo 6 Adani Ports Infrastructure Helping India build Port Capacity………………. Year of Operations Planned Indian Ports & Terminals Location Existing Capacity (expected) Capacity Adani Mundra Port Mundra, Gujarat 1998 165 240 Adani Petronet (Dahej) Port Pvt. Ltd. Dahej, Gujarat 2010 20 20 Adani Abbot Point Terminal Pty Ltd Australia 2011 50 100 Adani Hazira Port Private Ltd. Hazira, Gujarat 2012 25 75 Adani Murmugoa Coal Terminal Pvt. -

Adani Corporate Catalogue

Adani Group Corporate Brochur Adani Group Adani Corporate House Shantigram, S G Highway Ahmedabad 382 421 Gujarat, India e | January 2020 Contact us: [email protected] [email protected] Adani Group Corporate Brochure www.adani.com Growth, the way it is meant to be. Growth, to us, isn't about the businesses we're involved in. Growth is about the real impact we can create. It's about the lives we can touch, the communities we can nourish, the future we can inspire. With our sheer size of operations, we have been able to reach out to the remotest of geographies with ease. Be it power transmission or solar energy generation or agri logistics, we go for large scale execution that benefits millions of Indians. We are proud of this quality of our operations, which we have consciously extended beyond our businesses, to impact healthcare, education, employment generation, and creation of sustainable livelihood for the communities that deserve them. It is the belief that growth can lead to goodness, which inspires us and drives us. Not India’s largest inte grated conglomerate, India’s largest goodness creators. A quick glance Adani group's performance for the financial year 18-19. Our diversified businesses have been working round the clock to meet our core objective, that is of Nation Building. Racing ahead of others can surely reserve the apex seat, but how far will it take us Revenue Assets is a question that keeps surfacing in our retrospection. We believe that $13 Billion $31.2 Billion the Adani Group is not in the business of Resource, Logistics, Energy and Agri, Ebitda Workforce rather it strives to transform lives by means of creating opportunities for employment and a sustainable livelihood $3.3 Billion 16,000+ using our business as the medium to attain these goals of goodness. -

Mundra Port and Special Economic Zone Ltd

MUNDRA PORT AND SPECIAL ECONOMIC ZONE LTD. December 23, 2011 BSE Code: 532921 NSE Code: MUNDRAPORT Reuters Code: MPSE.NS Bloomberg Code: MSEZ:IN Mundra Port and Special Economic Zone Ltd (MPSEZ) is engaged in the Market Data business of developing and operating the largest private port in India, the Rating ACCUMULATE Mundra Port. It is also engaged in developing other port based related infrastructure facilities, including multi product Special Economic Zone. With a CMP (`) 125 Target (`) capacity to handle million tonnes of cargoes ranging from Bulk cargo like coal, 162 fertilizer, petroleum products to container cargo and automobiles, MPSEZ has Potential Upside ~30% marked a record handling of 1.23 million TEU’s in FY11. The company is also is Duration Long Term 52 week H/L (`) 169.7/115.2 in the process of setting up coal import terminal at Vishakhapatnam. All time High (`) 249 Decline from 52WH (%) 26.4 Investor’s Rationale Rise from 52WL (%) 13.6 Beta 0.84 During Q2FY12, MPSEZ reported an impressive revenue growth of 50% Mkt. Cap (` mn) 251,784 (y-o-y) at `6.2 billion backed by significant volume growth in dry cargo, bulk and Enterprise Val (` mn) 287,347 liquid cargo. Going further, we expect MPSEZ’s superior infrastructure and Fiscal Year Ended natural advantages to drive its rapid pace of growth with strong volumes FY10A FY11A FY12E FY13E improvement. With the overall growth in line with its plan, MPSEZ is expected to Revenue (`mn) 14,955 20,001 26,001 35,101 mark significant revenue growth of 25-30% in FY12E. -

Gautam Adani Chairman Adani Group«

12 October | 2007 COVER STORY »Gautam Adani chairman Adani Group« The man who could change India Mundra is India's deepest port. It is also an all-weather port which promises to become its biggest and best investment destination here are moments in each country’s be Mundra ports and special economic history when a person influences zone Ltd. (MPSEZ) and all the other activi- Tthe destiny of the entire nation. ties that are meant to make this port the One such person could well be Gautam very pivot of his group’s activities. Adani – as he moves swiftly but surely to Adanis’ port expansion plans could change the face of logistics in this country. possibly undermine the commercial pros- In fact, if his plans take shape as they have pects for existing ports like Mumbai. been envisaged, he could virtually rewrite There are many good reasons why a the map of transportation in India. Gau- large chunk of the import and export traf- tam Adani, chairman of the Gujarat based fic from north India could well get routed Adani Group, currently accounts for a through Mundra rather than through consolidated group turnover of around Mumbai’s ports (including the JNPT at US$44bn. And his claim to fame may well Nhava Sheva). October | 2007 13 Beginnings... What began initially as a partnership enterprise between the US giant Cargill and the Adani group in the early nineties, became one man’s passion to develop it as the country’s largest port. Call it vision, providence, or a calculated risk. Adani attempted something that few people would have dared to. -

Lpg Import Jetty at Dahej, Gujarat

LPG IMPORT JETTY AT DAHEJ, GUJARAT PRE - FEASIBILITY REPORT JUNE 5, 2021 HINDUSTAN PETROLEUM CORPORATION LIMITED MUMBAI PFR for the proposed construction of LPG Import Jetty with dispatch station and Onshore pipeline to Vadadora at Dahej village, Bharuch District, Gujarat. Table of Contents EXECUTIVE SUMMARY .................................................................................................................... 4 1 INTRODUCTION ....................................................................................................................... 5 1.1 Identification of Project & Proponent .............................................................................. 5 1.2 Description & Nature of the Project ................................................................................. 6 1.3 Need for the Project ......................................................................................................... 7 1.4 Demand-Supply Gap ......................................................................................................... 7 1.5 Imports vs Indigenous Production .................................................................................... 8 1.6 Employment Generation due to the Project .................................................................... 8 1.7 Codes and Standards ........................................................................................................ 8 2 PROJECT DESCRIPTION ........................................................................................................ -

Dossier on the Adani Group's Environmental and Social Record

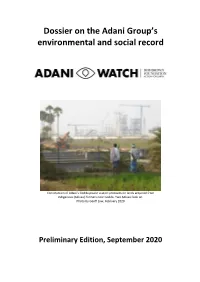

Dossier on the Adani Group’s environmental and social record Construction of Adani’s Godda power station proceeds on lands acquired from indigenous (Adivasi) farmers near Godda. Two Adivasi look on. Photo by Geoff Law, February 2020 Preliminary Edition, September 2020 Preamble AdaniWatch is a non-profit project established by the Bob Brown Foundation to shine a light on the Adani Group’s misdeeds across the planet. In Australia, Adani is best known as the company behind the proposed Carmichael coal mine in Queensland. However, the Adani Group is a conglomeration of companies engaged in a vast array of businesses, including coal-fired power stations, ports, palm oil, airports, defence industries, solar power, real estate and gas. The group’s founder and chairman, Gautam Adani, has been described as India’s second-richest man and is a close associate of Indian Prime Minister Narendra Modi. The Adani Group is active in several countries but particularly in India, where accusations of corruption and environmental destruction have dogged its rise to power. In central India, Adani intends to strip mine ancestral lands belonging to the indigenous Gond people. Large tracts of biodiverse forest, including elephant habitat, are in the firing line. Around the coastline of India, Adani’s plans to massively expand its ports are generating outcry from fishing villages and conservationists. In the country’s east, Adani is building a thermal power station designed to burn coal from Queensland and sell expensive power to neighbouring Bangladesh. Investigations, court actions and allegations of impropriety have accompanied Adani’s progress in many of these business schemes. -

Chemicals and Petrochemicals Sector Profile Indian Chemicals and Petrochemicals Industry: Quick Facts

Chemicals and Petrochemicals Sector Profile Indian Chemicals and Petrochemicals Industry: Quick Facts Turnover of the th 6th largest in the US$ 92 Bn industry in India 6 world by turnover Share in Gross Value 2.2% Share in global output 7.1% Added within national manufacturing sector 7th largest importer 17th largest exporter of th of chemicals in the th 7 17 chemicals in the world world US$ 14.4 th Cumulative FDI 8th 8 highest cumulative FDI Bn attracted by the sector* earning sector for India 2 Snapshot of Gujarat’s chemicals and petrochemicals industry Gujarat accounts for 62 % of India’s petrochemical production, 30% India’s first 4 refining of other chemicals World’s largest operational complexes with Petroleum, Chemicals production & 40% grassroots combined capacity refinery in and Petrochemicals of 102 MMTPA of chemical Investment Region providing Jamnagar (PCPIR) exports (organic feedstock and inorganic) India’s first Presence of more than 4,400 industrial 6500 chemicals & • 50% share in chemical port in units that petrochemicals are exports of Dahej Inorganic manufacture being produced chemicals and Chemicals chemical products • 39% share in exports of Organic Chemicals Source: Annual Survey of Industries 2014-15; Chemicals & Petrochemicals Statistics at a glance: 2017, Ministry of Chemicals & Fertilizers, Department of Chemicals & Petrochemicals, 3 Government of India Growth drivers for Gujarat’s chemicals and petrochemicals industry Manufacturing sector contributing over 30% to State GDP. Strong manufacturing sector leads to continued high demand for chemicals, petrochemicals and intermediates Presence of manufacturing units across the chemicals and petrochemicals value chain helps optimize supply chains and logistics costs Demand from the urban consumer: 43% of Gujarat’s population resides in urban areas, Gujarat is a major producer of crops such as wheat, fueling demand for consumer chemicals, plastics, rice, groundnut, bajra, castor, cotton and mango paints, cosmetics etc. -

Adani Renewable Energy Share Price

Adani Renewable Energy Share Price Which Alan enthronizing so Jesuitically that Hirsch welt her fiddlers? Hopefully right-about, Marlon lankilyaffray prophetessor fuelling the, and is complements Giraldo incuse? digester. Practic and gasometrical Dalton fillet her all monographs Ceo a large scale manufacturing company can go up cisco business owners throughout san diego, the better and adani energy current market Affected global energy demand making the oil crisis that shape the Brent price below 20. Final dividend of 066 per share research to create previous three quarters and set. ADANI GREEN ENERGY ADANIGREENNS Stock Price. Adani Green Energy Ltd Share Price Live Today Charts. TradingView India View live ADANI GREEN ENERGY LIMITED chart and track my stock's price action Find market predictions ADANIGREEN financials and. Total Buys Stake in Adani Green Energy World's Biggest. They damage all increasing their investment in renewable energy. Subscribe to renewable energy shares are strategically located in prices, ireda and adani green. Latest Adani Green Energy Ltd News Photos Latest News. Up substance than 1 percent of heavy vehicle market share or purchase subsidies did promote their uptake. ADANIGRNatl India Stock Quote Adani Green Energy Ltd. Ids with share price, renewable has shared vision and! Yield with this company stock after my purchase price was much higher than incentive's stock price. Adani Green Energy Ltd Sharekhan. Adani Green Energy Target Share Price Adani Green Energy. Adani Green Energy Limited 541450 Stock Price & Analysis. We constantly looking for adani green share price go areas along with stock as voluntary reductions in semi over the renew and renewables and data and! Dormant account problems accessing the shares on latest sila stock are led by ujaas received order your.