[First 4 Pages to Be Created in Assembly Font By

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Housing in Wales: HQN's Pre-Election Briefing

Housing in Wales: HQN’s pre-election briefing MARCH 2016 Keith Edwards Introduction “In the other countries of the UK, devolved powers mean that many aspects of housing policy will be determined locally” Roger Jarman Many of the big policy levers that impact on housing – taxation and welfare benefits for example – remain the prerogative of the UK government. Indeed a 2015 report by the Auditor General for Wales confirmed that changes to welfare benefits instigated by the UK Government had adversely affected a greater proportion of tenants of social housing in Wales than in either England or Scotland. It is, however, the case that a different narrative and agenda for action are being developed for housing in Wales. Nothing illustrates this better than whole system approach, a concept first developed by the Chartered Institute of Housing (CIH) Cymru and now championed by Welsh Government, with significant cross-party support. Central to this is positioning government as system steward, legislating, regulating, funding, nudging and encouraging innovation across all partners and tenures to deliver housing solutions. As a consequence there are now significant areas where housing policy and practice in Wales are taking a completely different tack to that of other administrations, most notably in comparison with the UK government. For example Wales has a fundamentally different position in relation to the Right to Buy, regulating the private rented sector and preventing homelessness. When elections to the National Assembly for Wales come around there is a genuine opportunity to hold politicians to account and try to shape the priorities of the next administration. -

The National Assembly for Wales

Oral Assembly Questions tabled on 27 March 2014 for answer on 1 April 2014 R - Signifies the Member has declared an interest. W - Signifies that the question was tabled in Welsh. (Self identifying Question no. shown in brackets) The Presiding Officer has agreed to call the Party Leaders to ask questions without notice to the First Minister after Question 2. To ask the First Minister 1. Llyr Gruffydd (North Wales): Will the First Minister make a statement on the Welsh Government’s implementation of the reformed Common Agricultural Policy in Wales? OAQ(4)1600(FM)W WITHDRAWN 2. Paul Davies (Preseli Pembrokeshire): Will the First Minister make a statement on what the Welsh Government is doing to support town centres in west Wales? OAQ(4)1589(FM) 3. Christine Chapman (Cynon Valley): What actions is the Welsh Government taking to improve the role of women in the Welsh economy? OAQ(4)1598(FM) 4. Mark Isherwood (North Wales): Will the First Minister outline Welsh Government support for dementia sufferers in Wales? OAQ(4)1602(FM) 5. Mick Antoniw (Pontypridd): Will the First Minister provide an update on First World War commemorations in Wales? OAQ(4)1597(FM) 6. Alun Ffred Jones (Arfon): Will the First Minister make a statement on the operation of the Government’s Welsh language unit? OAQ(4)1596(FM)W 7. Aled Roberts (North Wales): Will the First Minister provide an update on the North Wales Neonatal Review? OAQ(4)1591(FM)W 8. Ann Jones (Vale of Clwyd): What assessment has the First Minister made of the impact of the cost of living on families in Wales? OAQ(4)1590(FM) 9. -

Europe Matters

National Assembly for Wales EU Office Europe Matters Issue 30 – Summer/Autumn 2014 The National Assembly for Wales is the democratically elected body that represents the interests of Wales and its people, makes laws for Wales and holds the Welsh Government to account. © National Assembly for Wales Commission Copyright 2014 The text of this document may be reproduced free of charge in any format or medium providing that it is reproduced accurately and not used in a misleading or derogatory context. The material must be acknowledged as copyright of the National Assembly for Wales Commission and the title of the document specified. Introduction Dame Rosemary Butler AM Presiding Officer I am delighted to introduce the 30th issue of Europe Matters, our update on the work of the National Assembly for Wales on European issues. It was a privilege and an honour to participate on 16 August at the inauguration of the Welsh Memorial in Langemark, Flanders, to the Welsh soldiers who lost their lives in Flanders Fields during the First World War. Over 1,000 people from Wales and Flanders attended the ceremony, including the three leaders of the opposition parties in the Assembly, Andrew RT Davies AM, Leanne Wood AM and Kirsty Williams AM, and of course the First Minister Carwyn Jones AM. I and my fellow Commissioners, Sandy Mewies AM and Rhodri Glyn Thomas AM, will attend a special commemoration in Flanders next month, at the invite of the President of the Flemish Parliament Jan Peumans. This is another example of the strong co-operation and warmth between our two nations. -

Cofnod Pleidleisio Voting Record 06/05/2015

Cofnod Pleidleisio Voting Record 06/05/2015 Cynnwys Contents NDM5750 Dadl y Ceidwadwyr Cymreig - Cynnig heb ei ddiwygio NDM5750 Welsh Conservatives Debate - Motion without amendment NDM5750 Gwelliant 1 NDM5750 Amendment 1 NDM5750 Gwelliant 2 NDM5750 Amendment 2 NDM5750 Gwelliant 3 NDM5750 Amendment 3 NDM5750 Gwelliant 4 NDM5750 Amendment 4 NDM5750 Dadl y Ceidwadwyr Cymreig - Cynnig fel y'i diwygiwyd NDM5750 Welsh Conservatives Debate - Motion as amended NDM5752 Dadl y Ceidwadwyr Cymreig - Cynnig heb ei ddiwygio NDM5752 Welsh Conservatives Debate - Motion without amendment NDM5752 Gwelliant 1 NDM5752 Amendment 1 NDM5752 Dadl y Ceidwadwyr Cymreig - Cynnig fel y'i diwygiwyd NDM5752 Welsh Conservatives Debate - Motion as amended NDM5751 Dadl Plaid Cymru - Cynnig heb ei ddiwygio NDM5751 Welsh Plaid Cymru Debate - Motion without amendment Cofnod Pleidleisio | Voting Record | 06/05/2015 Senedd Cymru | Welsh Parliament NDM5750 Dadl y Ceidwadwyr Cymreig - Cynnig heb ei ddiwygio NDM5750 Welsh Conservatives Debate - Motion without amendment Gwrthodwyd y cynnig Motion not agreed O blaid / For: 10 Yn erbyn / Against: 23 Ymatal / Abstain: 0 Mohammad Asghar Leighton Andrews Peter Black Mick Antoniw Andrew R.T. Davies Christine Chapman Paul Davies Jeff Cuthbert Suzy Davies Alun Davies Russell George Jocelyn Davies William Graham Keith Davies Darren Millar Mark Drakeford Nick Ramsay Rebecca Evans Aled Roberts Janice Gregory Llyr Gruffydd Edwina Hart Mike Hedges Julie James Elin Jones Huw Lewis Sandy Mewies Gwyn R. Price Kenneth Skates Gwenda Thomas Rhodri Glyn Thomas Simon Thomas Lindsay Whittle Cofnod Pleidleisio | Voting Record | 06/05/2015 Senedd Cymru | Welsh Parliament NDM5750 Gwelliant 1 NDM5750 Amendment 1 Gwrthodwyd y gwelliant Amendment not agreed O blaid / For: 16 Yn erbyn / Against: 17 Ymatal / Abstain: 0 Mohammad Asghar Leighton Andrews Peter Black Mick Antoniw Andrew R.T. -

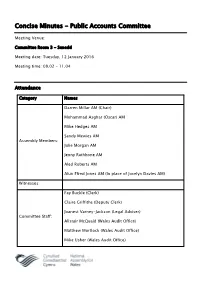

Concise Minutes - Public Accounts Committee

Concise Minutes - Public Accounts Committee Meeting Venue: Committee Room 3 - Senedd Meeting date: Tuesday, 12 January 2016 Meeting time: 09.02 - 11.04 Attendance Category Names Darren Millar AM (Chair) Mohammad Asghar (Oscar) AM Mike Hedges AM Sandy Mewies AM Assembly Members: Julie Morgan AM Jenny Rathbone AM Aled Roberts AM Alun Ffred Jones AM (In place of Jocelyn Davies AM) Witnesses: Fay Buckle (Clerk) Claire Griffiths (Deputy Clerk) Joanest Varney-Jackson (Legal Adviser) Committee Staff: Alistair McQuaid (Wales Audit Office) Matthew Mortlock (Wales Audit Office) Mike Usher (Wales Audit Office) Huw Vaughan Thomas (Wales Audit Office) 1 Introductions, apologies and substitutions 1.1 The Chair welcomed the Members to the meeting. 1.2 Jocelyn Davies excluded herself for the meeting under Standing Order 18.8. Alun Ffred Jones substituted. 2 Papers to note 2.1 The paper was noted. 3 Senior Management Pay: Update on the implementation of recommendations contained in the Committee's Report 3.1 The Committee noted the update on the implementation of the recommendations contained in the Committee’s report. 3.2 Members agreed that the Chair should reply to the Permanent Secretary seeking further clarification on a number of issues. 4 NHS Wales Health Board’s Governance: Consideration of evidence received 4.1 Members noted and discussed the additional information that had been received following the evidence sessions held in November 2015. 5 Regeneration Investment Fund for Wales: Consideration of Draft Report 5.1 Members considered the draft report noted that a revised draft would be available for further discussion at the Committee meeting on 19 January.. -

Concise Record (26-01-2011) 1

26.01.2011 "Gallwch weld crynodeb o ganlyniad y cyfarfod hwn yn y ""Pleidleisiau a Thrafodion,"" gan gynnwys manylion y pleidleisiau ar gynigion a gwelliannau a’r cynnydd a waned o ran y cwestiynau llafar. You can access a summary of the outcome of this meeting in the ""Votes and Proceedings"" including details of votes on motions and amendments and progress made on oral questions." "Cyfarfu’r Cynulliad am 1.30 p.m. gyda’r Llywydd (Dafydd Elis-Thomas) yn y Gadair The Assembly met at 1.30 p.m. with the Presiding Officer (Dafydd Elis-Thomas) in the Chair." Cwestiynau i’r Cwnsler Cyffredinol Questions to the Counsel General Cofnod ....|.... senedd.tv (cym) ....|..... senedd.tv (eng) "Dyma drefn yr Aelodau a gyfrannodd at yr eitem hon: The following is the order in which Members contributed to this item:" 1. Alun Davies....|.... Rhaglen Ddeddfwriaethol Flynyddol ....|.... Annual Legislative Programme Y Cwnsler Cyffredinol ac Arweinydd y Rhaglen Ddeddfwriaethol/The Counsel General and Leader of the Legislative Programme (John Griffiths) Alun Davies John Griffiths Nick Ramsay John Griffiths Leanne Wood Y Llywydd/The Presiding Officer John Griffiths 2. Christine Chapman ....|.... Rhaglen Ddeddfwriaethol ....|.... Legislative Programme John Griffiths Christine Chapman John Griffiths Jonathan Morgan John Griffiths 3. Lorraine Barrett ....|.... Gweinyddiaethau Datganoledig ....|.... Devolved Administrations John Griffiths Lorraine Barrett John Griffiths Darren Millar 1.45 p.m. John Griffiths David Lloyd John Griffiths 4. Sandy Mewies ....|.... Gwasanaethau -

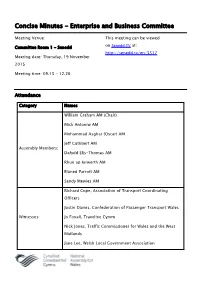

Concise Minutes - Enterprise and Business Committee

Concise Minutes - Enterprise and Business Committee Meeting Venue: This meeting can be viewed Committee Room 1 - Senedd on Senedd TV at: http://senedd.tv/en/3317 Meeting date: Thursday, 19 November 2015 Meeting time: 09.15 - 12.26 Attendance Category Names William Graham AM (Chair) Mick Antoniw AM Mohammad Asghar (Oscar) AM Jeff Cuthbert AM Assembly Members: Dafydd Elis-Thomas AM Rhun ap Iorwerth AM Eluned Parrott AM Sandy Mewies AM Richard Cope, Association of Transport Coordinating Officers Justin Davies, Confederation of Passenger Transport Wales Witnesses: Jo Foxall, Traveline Cymru Nick Jones, Traffic Commissioner for Wales and the West Midlands Jane Lee, Welsh Local Government Association Huw Morgan, Association of Transport Co-ordinating Officers John Pockett, Confederation of Passenger Transport Darren Thomas, Pembrokeshire County Council Graham Walter, Traveline Cymru Gareth Price (Clerk) Martha Da Gama Howells (Second Clerk) Committee Staff: Rachel Jones (Deputy Clerk) Andrew Minnis (Researcher) Transcript View the meeting transcript. 1 Introductions, apologies and substitutions 1.1 Apologies were received from Joyce Watson AM, Keith Davies AM and Gwenda Thomas AM. 1.2 Sandy Mewies AM substituted for Joyce Watson AM. 2 Inquiry into Bus and Community Transport Services in Wales 2.1 John Pockett and Justin Davies answered questions from Members of the Committee. 3 Inquiry into Bus and Community Transport in Wales 3.1 Jane Lee, Darren Thomas, Richard Cope and Huw Morgan answered questions from Members of the Committee. 4 Inquiry into Bus and Community Transport in Wales 4.1 Nick Jones, Graham Walter and Jo Foxall answered questions from Members of the Committee. 5 Papers to note 5.1 Rugby World Cup Transport Planning 5.1.1 The paper was noted by the Committee. -

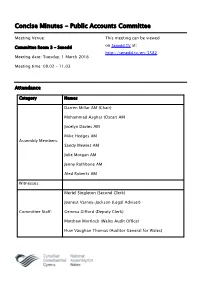

Concise Minutes - Public Accounts Committee

Concise Minutes - Public Accounts Committee Meeting Venue: This meeting can be viewed Committee Room 3 - Senedd on Senedd TV at: http://senedd.tv/en/3383 Meeting date: Tuesday, 8 March 2016 Meeting time: 09.02 - 11.01 Attendance Category Names Darren Millar AM (Chair) Mohammad Asghar (Oscar) AM Jocelyn Davies AM Mike Hedges AM Assembly Members: Sandy Mewies AM Jenny Rathbone AM Aled Roberts AM David Rees AM (In place of Julie Morgan AM) Gareth Bullock, Finance Wales Witnesses: James Price, Welsh Government Meriel Singleton (Clerk) Claire Griffiths (Deputy Clerk) Committee Staff: Joanest Varney-Jackson (Legal Adviser) Huw Vaughan Thomas (Auditor General for Wales) Mark Jones (Wales Audit Office) Mike Usher (Wales Audit Office) Transcript View the meeting transcript (PDF 311KB) View as HTML (351KB) 1 Introductions, apologies and substitutions 1.1 The Chair welcomed the Members to the meeting. 1.2 Apologies were received from Julie Morgan. David Rees substituted. 2 Papers to note 2.1 The paper was noted. Members agreed to include a recommendation in its Legacy Report, that the successor Committee considers undertaking an inquiry into this topic. 2.1 Letter to the Chair from the Auditor General for Wales 3 Welsh Government Investment in Next Generation Broadband Infrastructure: Consideration of response to the Committees Report 3.1 Members noted the responses and agreed to include a recommendation in the Committee’s Legacy Report that the successor Committee seeks a further update on progress made in autumn 2016. 3.2 The Chair agreed to write to the Welsh Government seeking further clarification on the complexity of installing Broadband (R1), an indication of the possible cost over and above the value of the vouchers on offer (R2), what ‘dynamic’ means with regards to the consumer (R8) and a description of how the website has been improved. -

(Public Pack)Agenda Document for Assembly Commission, 21/05/2015

Assembly Commission Meeting Venue: Presiding Officer’s office, 4th floor - Tŷ Hywel Meeting date: Thursday, 21 May 2015 Meeting time: 13.00 For further information please contact: Sulafa Thomas, x8669 Commission Secretariat 0300 200 6565 [email protected] Agenda AC(4)2015(7) 1 Introduction Introduction and apologies Declarations of interest Minutes of the previous meeting (Pages 1 - 3) 2 Procurement Report (Jan-March) (Pages 4 - 8) 3 Highlight Report (Jan to March) (Pages 9 - 45) 4 Corporate Performance Report (Apr 14-Mar 15) (Pages 46 - 71) 5 Remuneration Committee Annual Report (Pages 72 - 81) 6 Audit Committee minutes 20/4/15 (Pages 82 - 88) 7 Any other business Assembly Commission Venue: Presiding Officer’s office, 4th floor - Tŷ Hywel Date: Thursday, 23 April 2015 Time: 13.00 - 14.30 Minutes: AC(4)2015(6) Commission Dame Rosemary Butler AM (Chair) Peter Black AM Members: Sandy Mewies AM Rhodri Glyn Thomas AM Officials present: Claire Clancy, Chief Executive & Clerk of the Assembly Craig Stephenson, Director of Commission Services Dave Tosh, Director of Resources Nicola Callow, Director of Finance Kevin Tumelty, Head of Security Sulafa Thomas, Head of Commission Secretariat Others in David Melding AM, Deputy Presiding Officer Helena Feltham, Independent Adviser attendance: 1 Introduction 1.1 Introduction and apologies Angela Burns AM had sent her apologies. 1.2 Declarations of interest There were no declarations of interest. 1.3 Minutes of the previous meeting The minutes of the 5 March meeting were agreed. 2 Draft Budget Strategy 2016-17 Commissioners considered a paper which outlined the suggested approach and budget options for the Commission’s 2016-17 Budget. -

FLINTSHIRE LOCAL VOLUNTARY COUNCIL Cyngor Gwirfoddol Lleol Sir Fflint

FLINTSHIRE LOCAL VOLUNTARY COUNCIL Cyngor Gwirfoddol Lleol Sir Fflint Minutes of the Sixteenth Annual General Meeting Held at Deeside College Thursday, 26 September 2013, 7.00 pm PRESENT: M Manley Elfed High School Marjorie Thomson CAB/FLVC Mandy Deyes BADG Will Hastings Flintshire Fairtrade Coalition Anita James Daffodils John Clutton Coleg Cambria Paul Shotton FCC Michael Dixon Hope Mountain RDA Cllr Carolyn Preece Buckley Town Council Mary Southall Sealand Manor Residents Association Sian Edwards FLVC Volunteer Rachael Partington FLVC Veronica Gay FDF P Lawton-Hughes Sychdyn Memorial Hall Shaun Darlington FLVC M Langton-Davies Gardners I Langton-Davies Gardners Allan Young MS Society Flintshire Steve Nash FLVC Fred Evans RSVP/Hawarden Rangers M Parry FYRD Margaret Jones FLVC Fran Parry Community Health Council Jasbir Dhesi Coleg Cambria Barrie Potter FLIME June Brady FLVC Sue Williams FLVC Mike Ritchie Royal Voluntary Service Chelsea Hibbert TFC Tara Griffiths TFC Irene Langford FLVC D Healey Hope & Caergwrle David Cox FCC John Gray FLVC Ann Woods Home-Start Julie Evans Dangerpoint Wendy Carter FLVC Yvette Bracewell FLVC Gill Stephen MISYFF FLVC AGM 26 September 2013 1 Alwyn Jones FCC Terry Williams NWFRS Gerry Kitney Over 50s Action Group Pat Mee Transition Town Holywell & District Vy Cochran Wales & West Housing James Johnson FLVC Harold Taylor Hawarden Singers Paul Garner Cornerstone Eileen Griffiths Llwynegrin Singers Christine Bevan Llwynegrin Singers Purdy Edwards FLVC Chris Ablett FLVC Sheila Bacon FLVC Clive Bracewell FLVC -

The National Assembly for Wales

Oral Assembly Questions tabled on 28 February 2013 for answer on 5 March 2013 R - Signifies the Member has declared an interest. W - Signifies that the question was tabled in Welsh. (Self identifying Question no. shown in brackets) The Presiding Officer has agreed to call the Party Leaders to ask questions without notice to the First Minister after Question 2. To ask the First Minister 1. Sandy Mewies (Delyn): What support is the Welsh Government giving to International Women’s day. OAQ(4)0940(FM) 2. Vaughan Gething (Cardiff South and Penarth): Will the First Minister make a statement on child poverty in Cardiff South and Penarth. OAQ(4)0945(FM) 3. Rebecca Evans (Mid and West Wales): Will the First Minister provide an update on road safety in Wales. OAQ(4)0949(FM) 4. Alun Ffred Jones (Arfon): What discussions has the Welsh Government had with the UK Government regarding the plans to privatise vast areas of the probation service. OAQ(4)0938(FM)W 5. Jenny Rathbone (Cardiff Central): What are the lessons for Wales from the Francis Report into the care of patients at the Mid Staffordshire NHS Trust Hospital. OAQ(4)0937(FM) 6. Lynne Neagle (Torfaen): Will the First Minister make a statement outlining the benefits of Minerals Technical Advice Note 2: Coal to communities in Wales. OAQ(4)0941(FM) 7. Peter Black (South Wales West): Will the First Minister make a statement on the implementation of the Welsh Government’s mortgage guarantee scheme. OAQ(4)0939(FM) 8. Antoinette Sandbach (North Wales): What are the Welsh Government’s plans for safeguarding neonatal care in North Wales. -

Concise Minutes - Public Accounts Committee

Concise Minutes - Public Accounts Committee Meeting Venue: This meeting can be viewed Committee Room 3 - Senedd on Senedd TV at: http://senedd.tv/en/3382 Meeting date: Tuesday, 1 March 2016 Meeting time: 09.02 - 11.03 Attendance Category Names Darren Millar AM (Chair) Mohammad Asghar (Oscar) AM Jocelyn Davies AM Mike Hedges AM Assembly Members: Sandy Mewies AM Julie Morgan AM Jenny Rathbone AM Aled Roberts AM Witnesses: Meriel Singleton (Second Clerk) Joanest Varney-Jackson (Legal Adviser) Committee Staff: Gemma Gifford (Deputy Clerk) Matthew Mortlock (Wales Audit Office) Huw Vaughan Thomas (Auditor General for Wales) Transcript View the meeting transcript. 1 Introductions, apologies and substitutions 1.1 The Chair welcomed the Members to the meeting. 1.2 There were no apologies. 2 Papers to note 2.1 The papers were noted. 2.1 Cardiff Airport: Additional information from Simon Jones, Chair of Holdco (19 February 2016) 2.2 Cardiff Airport: Welsh Government Response to the Auditor General's Report (22 February 2016) 2.3 Cardiff Airport: Letter from the Football Association of Wales (24 February 2016) 2.4 Cardiff Airport: Additional information from Chris Cain, Northpoint Aviation (23 February 2016) 2.5 Cardiff Airport: Letter from the Welsh Rugby Union (24 February 2016) 2.6 Cardiff Airport: Letter from James Price, Welsh Government (24 February 2016) 3 Scrutiny of Accounts 2014-15: Consideration of responses to the Committees Report 3.1 Members considered and noted the response received from the organisations with regard to the recommendations directed to them in the Committee’s report which was published in December 2015.