Report of the Comptroller and Auditor General of India on State Finances for the Year Ended March 2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MAHARASHTRA Not Mention PN-34

SL Name of Company/Person Address Telephone No City/Tow Ratnagiri 1 SHRI MOHAMMED AYUB KADWAI SANGAMESHWAR SANGAM A MULLA SHWAR 2 SHRI PRAFULLA H 2232, NR SAI MANDIR RATNAGI NACHANKAR PARTAVANE RATNAGIRI RI 3 SHRI ALI ISMAIL SOLKAR 124, ISMAIL MANZIL KARLA BARAGHAR KARLA RATNAGI 4 SHRI DILIP S JADHAV VERVALI BDK LANJA LANJA 5 SHRI RAVINDRA S MALGUND RATNAGIRI MALGUN CHITALE D 6 SHRI SAMEER S NARKAR SATVALI LANJA LANJA 7 SHRI. S V DESHMUKH BAZARPETH LANJA LANJA 8 SHRI RAJESH T NAIK HATKHAMBA RATNAGIRI HATKHA MBA 9 SHRI MANESH N KONDAYE RAJAPUR RAJAPUR 10 SHRI BHARAT S JADHAV DHAULAVALI RAJAPUR RAJAPUR 11 SHRI RAJESH M ADAKE PHANSOP RATNAGIRI RATNAGI 12 SAU FARIDA R KAZI 2050, RAJAPURKAR COLONY RATNAGI UDYAMNAGAR RATNAGIRI RI 13 SHRI S D PENDASE & SHRI DHAMANI SANGAM M M SANGAM SANGAMESHWAR EHSWAR 14 SHRI ABDULLA Y 418, RAJIWADA RATNAGIRI RATNAGI TANDEL RI 15 SHRI PRAKASH D SANGAMESHWAR SANGAM KOLWANKAR RATNAGIRI EHSWAR 16 SHRI SAGAR A PATIL DEVALE RATNAGIRI SANGAM ESHWAR 17 SHRI VIKAS V NARKAR AGARWADI LANJA LANJA 18 SHRI KISHOR S PAWAR NANAR RAJAPUR RAJAPUR 19 SHRI ANANT T MAVALANGE PAWAS PAWAS 20 SHRI DILWAR P GODAD 4110, PATHANWADI KILLA RATNAGI RATNAGIRI RI 21 SHRI JAYENDRA M DEVRUKH RATNAGIRI DEVRUK MANGALE H 22 SHRI MANSOOR A KAZI HALIMA MANZIL RAJAPUR MADILWADA RAJAPUR RATNAGI 23 SHRI SIKANDAR Y BEG KONDIVARE SANGAM SANGAMESHWAR ESHWAR 24 SHRI NIZAM MOHD KARLA RATNAGIRI RATNAGI 25 SMT KOMAL K CHAVAN BHAMBED LANJA LANJA 26 SHRI AKBAR K KALAMBASTE KASBA SANGAM DASURKAR ESHWAR 27 SHRI ILYAS MOHD FAKIR GUMBAD SAITVADA RATNAGI 28 SHRI -

List of New Construction Works Under NRHM (2008-2009)

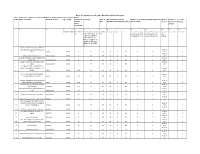

1 List of New Construction Works under NRHM (2008-2009) Sub Centre Financial Progress Physical Progress Amount If Completed Sr No District Block Name of Sub Centre Date/Month of Work Sanctioned Expenditure (Rs. Name of Execution agency If not completed Tentative date of Sanctioned (Rs. In Date/Month of Work In Lakhs) Stage of Progress completion Lakhs) Completion 1 Kalyan Manivali 20.09.2008 8.75 8.52 IDW Apr-10 2 Kalyan Shirdhon Vadavali 04.10.2008 8.80 8.61 IDW Nov-09 3 Kalyan Golivali 07.08.2008 8.74 7.98 IDW Nov-09 4 Thane Ambernath Bohnoli 04.10.2008 10.36 9.72 IDW Apr-10 5 Bhiwandi Hiwali 08.10.2008 7.98 6.93 IDW Mar-09 6 Bhiwandi Khaling 08.10.2008 7.98 6.78 IDW Mar-09 7 Vasai Kaular 04.10.2008 11.94 11.54 IDW Jan-11 8 Karjat Kondivade 6/11/2008 13.61 12.45 IDW 28/02/2011 9 Khalapur Mohapada 6/11/2008 13.61 12.61 IDW 31/03/2011 10 Khalapur Bid Khurd 6/11/2008 13.61 11.31 IDW 17/03/2011 11 Khalapur Kalote 6/11/2008 13.61 12.12 IDW 29/03/2011 12 Mahad Kumbhe Shivthar 6/11/2008 13.61 12.75 IDW 11/12/2010 13 Mangaon Lonere 19/11/2008 13.61 11.39 IDW 17/06/2011 14 Mangaon Pansai 6/11/2008 13.61 11.99 IDW 31/03/2011 15 Mangaon Amdoshi 6/11/2008 13.61 11.81 IDW 29/03/2011 16 Panvel Gulsunde 6/11/2008 13.61 12.57 IDW 20/02/2010 17 Panvel Asudgaon 6/11/2008 13.61 12.35 IDW 28/08/2011 18 Panvel Rohinjan 6/11/2008 13.61 12.33 IDW 28/03/2011 19 RAIGAD Roha Virzoli 6/11/2008 13.61 11.36 IDW 20/03/2010 20 Roha Nahave 6/11/2008 13.61 11.70 IDW 31/03/2011 21 Roha Wali 6/11/2008 13.61 12.74 IDW 31/03/2011 22 Roha Ainghar 6/11/2008 13.61 11.75 IDW -

Bpc(Maharashtra) (Times of India).Xlsx

Notice for appointment of Regular / Rural Retail Outlet Dealerships BPCL proposes to appoint Retail Outlet dealers in Maharashtra as per following details : Sl. No Name of location Revenue District Type of RO Estimated Category Type of Minimum Dimension (in Finance to be arranged by the applicant Mode of Fixed Fee / Security monthly Site* M.)/Area of the site (in Sq. M.). * (Rs in Lakhs) Selection Minimum Bid Deposit Sales amount Potential # 1 2 3 4 5 6 7 8 9a 9b 10 11 12 Regular / Rural MS+HSD in SC/ SC CC1/ SC CC- CC/DC/C Frontage Depth Area Estimated working Estimated fund required Draw of Rs in Lakhs Rs in Lakhs Kls 2/ SC PH/ ST/ ST CC- FS capital requirement for development of Lots / 1/ ST CC-2/ ST PH/ for operation of RO infrastructure at RO Bidding OBC/ OBC CC-1/ OBC CC-2/ OBC PH/ OPEN/ OPEN CC-1/ OPEN CC-2/ OPEN PH From Aastha Hospital to Jalna APMC on New Mondha road, within Municipal Draw of 1 Limits JALNA RURAL 33 ST CFS 30 25 750 0 0 Lots 0 2 Draw of 2 VIllage jamgaon taluka parner AHMEDNAGAR RURAL 25 ST CFS 30 25 750 0 0 Lots 0 2 VILLAGE KOMBHALI,TALUKA KARJAT(NOT Draw of 3 ON NH/SH) AHMEDNAGAR RURAL 25 SC CFS 30 25 750 0 0 Lots 0 2 Village Ambhai, Tal - Sillod Other than Draw of 4 NH/SH AURANGABAD RURAL 25 ST CFS 30 25 750 0 0 Lots 0 2 ON MAHALUNGE - NANDE ROAD, MAHALUNGE GRAM PANCHYAT, TAL: Draw of 5 MULSHI PUNE RURAL 300 SC CFS 30 25 750 0 0 Lots 0 2 ON 1.1 NEW DP ROAD (30 M WIDE), Draw of 6 VILLAGE: DEHU, TAL: HAVELI PUNE RURAL 140 SC CFS 30 25 750 0 0 Lots 0 2 VILLAGE- RAJEGAON, TALUKA: DAUND Draw of 7 ON BHIGWAN-MALTHAN -

Umri District: Nanded Bhokar

Village Map Taluka: Umri District: Nanded Bhokar Karla Mudkhed Shivangaon Dholumri Kalgaon µ 2 1 0 2 4 6 Sawargaon (Dakshin) Shirur Palasgaon km Turati Aswaldari Sindhi Mokhandi (Jagir) Durganagar Fulsingnagar Jirona Ishwarnagar Location Index Somthana P.U. Shelgaon Bothi Bitnal Sawargaon (kala) Vasantnagar District Index Ganipur Nandurbar Jamgaon Bhandara Dhule Amravati Nagpur Gondiya Hunda (patti ganga) Gortha Jalgaon UMRI Hunda patti umari Akola Wardha !( Buldana Mandala Nashik Washim Chandrapur Ramkhadak Yavatmal Hiradgaon Kudla Peth Umri (M Cl) Palghar Aurangabad Hunda Tanda Hangiranga Waghala Jalna Hingoli Gadchiroli Thane Ahmednagar Parbhani Telangana State Mumbai Suburban Nanded Mumbai Bid Bolsa Raigarh Pune Abdulapur Latur Bidar Osmanabad Ilegaon P. G. Dilawarpur Satara Solapur Chinchala patti umri Talegaon Dhanora Bk. Ratnagiri Sangli Bhayegaon Manur Maharashtra State Kolhapur Amdapur Sindhudurg Rahati Kh. Dharwad Ijjatgaon Nagthana Kh. Nagthana Bk. Bolsa Kh Bolsa Bk Miyadadpur Taluka Index Mahoor Kinwat Beldara Nimtek Balegaon Hadgaon Himayatnagar Karkala Ardhapur Hatni Bhokar NandedMudkhed Borjuni Loha Umri Mahati Golegaon Waghalwada Dharmabad Naigaon (Khairgaon) Kandhar Biloli Endala Bijegaon Legend Dharmabad Kaudgaon Mukhed Deglur !( Taluka Head Quarter Naigaon (Khairgaon) Railway Hassa District: Nanded Singnapur National Highway Kawalguda Bk. State Highway Village maps from Land Record Department, GoM. Kawalguda kh. Data Source: State Boundary Waterbody/River from Satellite Imagery. District Boundary Generated By: Taluka Boundary Maharashtra Remote Sensing Applications Centre Village Boundary Autonomous Body of Planning Department, Government of Maharashtra, VNIT Campus, Biloli Waterbody/River South Am bazari Road, Nagpur 440 010. -

Government of India Ministry of Human Resource Development Department of School Education and Literacy Minutes of the Meeting Of

` Government of India Ministry of Human Resource Development Department of School Education and Literacy Minutes of the meeting of the Project Approval Board held on 20th May 2019 to consider the Annual Work Plan & Budget (AWP&B) 2019-20 of Samagra Shiksha for the State of Maharashtra 1. Introduction The meeting of the Project Approval Board for considering the Annual Work Plan and Budget (AWP&B) 2019-20 for SAMAGRA SHIKSHA for the State of Maharashtra was held on 20th May 2019. The list of participants who attended the meeting is attached at Annexure-I. 2. Initiatives of the State Ms. Rina Ray, Secretary (SE&L) invited Maharashtra to give a presentation on school education in the State. Ms. Vandana Krishna Additional Chief Secretary (Maharashtra), gave a presentation which included the following major points: a) The online recruitment system called PAVITRA is introduced by the Government of Maharashtra in order to provide transparent recruitment process. Around 4800 primary teachers and 7200 subject teachers are expected to be appointed before commencing this educational year. Transfers of teachers are also online. b) State has undertaken a massive exercise of absorption of surplus teachers at division as well as state level. The State could absorb 890 out of 1221 surplus teachers at Primary level and 2094 out of 3254 teachers at secondary level. c) Kumathe Beat Model in Satara district is popular in the state where 40 schools have been covered for child friendly and joyful learning with no textbooks .Teachers have developed learning material to suit children’s needs. d) Pune ZP has piloted “One Book One Note Book” by combining all subjects’ textbooks of Class IV to Class VII into one common textbook, and dividing it into monthly sections. -

List of Candidates

List of Candidates Sr.No NAME OF CANDIDATE MARKS OBTAINRD SET/NET ADDRESS SUBJECT B.Pharm. CATEGORY SC 1 SHRI BHUKTARE SANJAY GANPATHRAO 908 GATE AT SNGVAI (B) 1300 POST THORDA (B) 69.85 TQ & DIST NANDED List of Candidates Sr.No NAME OF CANDIDATE MARKS OBTAINRD SET/NET ADDRESS SUBJECT Bio Technology CATEGORY SC 1 SHRI SUTAR VIJAYAKUMAR BHANYDASRAO NET AT. B.K. SUTAR, AMBEDKAR CHAUK, NEAR VAISHALI BAUDDHAVIHAR, BAUDDHNAGAR LATUR. TQ.DIST. LAUTR. 2 SHRI TIGOTE DHANANJAY DASHARATH 805 NET AT POST KUMATHA(BK) 1200 TQ AHEMEDPUR 67.08 DIST LATUR 3 SHRI DHOLE NAGESH ARJUNRAO 1423 PH.D SUMEDH NAGAR, POST TARODA 2400 TARODA(KD), PURNA ROAD, 59.29 NANDED. List of Candidates Sr.No NAME OF CANDIDATE MARKS OBTAINRD SET/NET ADDRESS SUBJECT BIOCHEMISTRY CATEGORY SC 1 SHRI ADHAV SANTOSH KACHRU 872 NET AT ZARI , POST VISHNUPURI 1200 TQ. LOHA 72.67 DIST NANDED List of Candidates Sr.No NAME OF CANDIDATE MARKS OBTAINRD SET/NET ADDRESS SUBJECT Botany CATEGORY NT1 1 SHRI UMATE SATISH KESHAVRAO 941 SET C-60, KABRA NAGAR 1200 NANDED- 431602 78.42 SUBJECT Botany CATEGORY OBC 1 SHRI THORAT RAJKUMAR HANUMANRAO 842 SET AMRUTESHWAR NAGAR 1300 PH.D BEHIND YOGESHWARI COLLEGE, AMBAJOGAI 64.77 TQ. AMBAJOGAI DIST BEED - 431517 SUBJECT Botany CATEGORY SC 1 SHRI GACCHE RAJU NIWARTTI 760 SET AT SAYAL, POST MARLAK (B) 1000 TAL & DIST NANDED 76.00 2 SHRI SARTAPE HARSHDEEP BUDDHAJI 910 SET AT. POST. MALHIVARA 1200 NET TQ & DIST. HINGOLI - 431513 75.83 3 SHRI RAIBHOLE UDDHAV KISHANRAO 565 PH.D V.G.Iondhle,Railway Driver 1000 Railway Colony H.No.101/1 Purna 56.50 dist.Parbhani. -

Yashwant Rao Chavan Maharashtra Open University HEI Profile & Administrative Information

Yashwant Rao Chavan Maharashtra Open University HEI Profile & Administrative Information : HEI Basic Information : Registration ID: HEI-P-U-0335 Name of the HEI: Yashwant Rao Chavan Maharashtra Open Institution Type: University State Open Year of Establishment: Jul 1989 Mode of Education: City: Nashik District: Nashik Single Mode Address_1: Dnyngangotri, Near Gangapur Dam, Govardhan, Address_2: Nashik, Maharashtra, INDIA Pin Code: 422203 Email: [email protected] Telephone: 02532230228 Fax: 02532231205 State: MAHARASHTRA Official Website of HEI: Official website for Open & Distance Learning: https://ycmou.ac.in/ https://ycmou.ac.in/ HEI Authorities Vice Chancellor Name of the Vice Chancellor: Prof.E.Vayunandan Vice Chancellor Email: Vice Chancellor Mobile: [email protected] 9403774888 Phone (Office): Phone (Residence): Highest Education Qualification: Ph.D Public Adm Experience: 33 Years 02532230228 02532230048 Registrar Name of the Registrar: Dr Dinesh Bhonde Registrar Email: [email protected] Registrar Mobile: 9423983006 Phone (Office): 02532230229 Phone (Residence): 02532230229 Highest Education Qualification: Ph.D Civil engg Experience: 36 years CIQA Whether Center for Internal Quality Assurance (CIQA) is establised or not : Yes School of Studies Name of Head of School of Highest Education Date of Appointment Srno Name of School of Studies studies Designation Mobile No Qualification Joining Letter 1 School of Computer Science Dr.Pramod Khandare Associate 9403774524 Ph.D 29-02-1992 View -

39Th Week, 2011

DISEASE ALERTS/OUTBREAKS REPORTED AND RESPONDED TO BY STATES/UTs THROUGH INTEGRATED DISEASE SURVEILLANCE PROJECT (IDSP) th nd 39 week (ending 2 October) 2011 District wise disease alerts/outbreaks reported in the 39th week, 2011 REPORTING STATUS OF STATES/UTs No. of States /UTs submitted outbreak report 23 (including NIL report) No. of States/ UTs submitted “NIL” outbreak report 10 INTEGRATED DISEASE SURVEILLANCE PROJECT, NATIONAL CENTRE FOR DISEASE CONTROL, DELHI Tel No. 23913148, Fax No. 23922677; www.idsp.nic.in Sl. Name of Name of Disease/ Illness No. of Date of Date of Current Comments/ Action taken No. State/UT District cases/ start of reporting Status deaths outbreak Cases of diarrhoea reported from Village Khalihamari, SC Amoni, BPHC Samaguri. PHC Medical Officer visited and investigated the outbreak. 2 patients i Acute died at home. 4 patients referred to Nagaon BPHC for treatment. Three water Under Nagaon Diarrhoeal 8 / 2 22.09.11 27.09.11 samples collected by H S strip; result is awaited. 3 stool samples collected and surveillance 2 Disease sent to Golaghat District priority lab under IDSP found negative for cholera culture. Active survey done to find new cases. Health education given regarding hygiene and sanitation. Cases with symptoms of headache, vomiting, fever and pain abdomen reported from Village Ajokha, SC Hankhati, BPHC Kakopather, MPHC Dholla after consumption of local wine with some traditional food in Tiplang in Arunachal Under Pradesh. 4 patients died at their home. 13 patients admitted at Kakopathar PHC Tinsukia ii Food Poisoning 17 / 4 21.09.11 26.09.11 surveillance for treatment have improved. -

DISTRICT NANDED MAHARASHTRA 4Th March 1994

DISTRICT NANDED MAHARASHTRA 4th March 1994 NIEPA DC D08263 li b r a r y & DOCUiVid ' ' , i ; -.-jli ■]:. h ! Hi. Natio lnsi;icu*e cf h.cucationuj P'fliinMiij at;(i Administration. T' ri Aurobindo Marg, U*e........... \ A ND IS"T AREA: 10502 Sq.Km. POPULATION: Male: 1 1.97 .007 Female: ll,32,-!;86 TOTAL 23,29.493 PERCENTAGE OF LITERACY Male: 51.89% Female: 24.96% TOTAL 38.81% : PR03ECT, DOCUMENT OUTLINE 1 INTRODUCTION 1 2 SITUATIONAL ANALYSIS 6 2.1 Demographic & Educational Profile 6 2.2 Educational Profile 2 5 2.3 Pre-Primary Education 53 2 A Approaches in Primary Education 5^ 2.5 Back-up programme 56 2.6 Management of Primary Education 5 7 2.7 Special Trible Sub-Plan - KINWAT 60 3 PROBLEMS & ISSUES IN PRIMARY EDUCATION 72 3.1 General 7 2 3.2 The problems of accessebility 7 3 3.3 The problems of retention 7^ Infrastructural and other problems 7^f GOALS, TARGETS STRATEGIES & INTERVENTIONS 76 ^.1 Project goals 76 ^.2 Project Objectives 77 ^.3 Process of project preparation 78 Rationale behind selection of the district 81 The project 82 ^.6 Teacher efforts 87 ^.7 Retention 88 ^.8 Creating conducive eviornment 90 Achievement 91 ^.10 Special efforts 95 (2) 5. PROGRAMMES & ACTIVITIES 97 3.1 Introduction 97 5.2 Pre-School Education 97 5.3 Primary Schools 99 5.^ Incentives and facilities to the students 105 5.5 Girls Education & Woman empovernment 109 Pre-Project Cost 118 6. PROJECT COST 122 6.1 Introduction 122 6.2 Access 122 6.3 Retention 127 6 A Quality Improvement 131 6.5 Summery of project cost 136 7. -

Government of Maharashtra

REPORT OF THE COMPTROLLER AND AUDITOR GENERAL OF INDIA FOR THE YEAR ENDED 31 MARCH 2009 (CIVIL) GOVERNMENT OF MAHARASHTRA REPORT OF THE COMPTROLLER AND AUDITOR GENERAL OF INDIA FOR THE YEAR ENDED 31 MARCH 2009 (CIVIL) GOVERNMENT OF MAHARASHTRA www.cag.gov.in TABLE OF CONTENTS Reference Paragraph Page No. Preface CHAPTER I INTRODUCTION About this Report 1.1 1 Auditee profile 1.2 1 Authority for audit 1.3 2 Planning and conduct of audit 1.4 2 Organisational structure of the offices of the Principal 1.5 3 Accountant General (Audit)-I, Mumbai and the Accountant General (Audit)-II, Nagpur Significant audit observations 1.6 4 Budget and expenditure controls 1. 7 7 Response of the departments to draft paragraphs 1.8 8 CHAPTER II PERFORMANCE REVIEWS Public Health Department National Rural Health Mission 2.1 9 School Education and Sports Department Development of Sports in Maharashtra 2.2 34 Rural Development and Panchayat Raj Department Working of District Rural Development Agencies 2.3 60 (DRDAs)in Maharashtra Rural Development and Water Conservation Department 2.4 80 Minor Irrigation (Local Sector) Projects Home Department Computerisation in Police Department 2.5 94 Audit Report (Civil) for the year ended 31 March 2009 CHAPTER III Reference AUDIT OF TRANSACTIONS Paragraph Page No. Fraudulent drawal/misappropriation/ 3.1 embezzlement/losses Public Health Department. Fraudulent payment of medical reimbursement claims 3.1.1 109 Excess payment/overpayment/wasteful/infructuous 3.2 expenditure General Administration Department Overpayment of incentive -

Final List of Contesting Candidates

GENERAL ELECTION TO MAHARASHTRA STATE LEGISLATIVE ASSEMBLY-2014 List of Contesting Candidates MAHARSHTRA STATE DATE OF POLL 15TH OCTOBER 2014 Sr. No. Name Of Candidate Address Of Candidate Party Affiliation Symbol Allottted 1-Akkalkuwa (ST) 1 Aamshya Fulji Padavi At- Koylivihir, Post - British Ankushvihir Tal- Akkalkuwa Shivsena Bow And Arrow Dist- Nandurbar 2 Paradake Vijaysing Rupsing At June Dhadgaon, Post- Dhadgaon Tal- Akrani Dist- Nationalist Congress Party Clock Nandurbar 3 Padavi Adv. K.C. At Asali, Post Talai, Tal- Akkalkuwa Dist- Nandurbar Indian National Congress Hand 4 Padavi Nagesh Dilwarsing At Post Vanyavihir, Tal - Akkalkuwa Dist- Nandurbar Bharatiya Janata Party Lotus 5 Mamata Ravindra Valavi At Post Mundalvad, Tal- Akrani Dist- Nandurbar Maharashtra Navnirman Sena Railway Engine 6 Adv. Ranjit Jugla Padavi At Danel, Post- Bhagdari Tal- Akkalkuwa Dist- Bahujan Mukti Party Cot Nandurbar 7 Padavi Narendrasing Bhagatsing At- Sorapada, Post- Akkalkuwa Tal- Akkalkuwa, Dist - Independent Cup And Saucer Nandurbar 8 Padavi Madhukar Shamsing At- Khatwani, Post- British Ankushvihir Tal- Akkalkuwa, Independent Slate Dist- Nandurbar 9 Madan Jahangir Padavi At Post- Jamana, Tal- Akkalkuwa, Dist- Nandurbar Independent Table 2-Sahada (ST) 1 Kisan Runjya Pawar Balaji, 35-Bramhastrushti Colony, Juna Mohida Road, Maharashtra Navnirman Sena Railway Engine Post Shahada, Tal. Shahada, Dist.Nandurbar Shahada 2 Gavit Rajendrakumar Krushnarao Plot No.5, Pratap Nagar, Taloda, Tal.Taloda Nationalist Congress Party Clock Dist.Nandurbar Taloda 3 Naik Suresh Sumersing At.Post Chikhali Digar Tal.Shahada Dist.Nandurbar Shivsena Bow And Arrow Chikhali Digar 4 Padmakar Vijaysing Valvi At.Post Modalpada, Tal.Taloda Dist.Nandurbar Indian National Congress Hand Modalpada 5 Padvi Udesing Kocharu At.Somaval Bk, Post.Nalgavhan, Tal.Taloda, Bharatiya Janata Party Lotus Dist.Nandurbar At.Somaval Bk Post.Nalgavhan 6 Padvi Savitri Magan At Post. -

Selection List of Gramin Dak Sevak for Maharashtra Circle Cycle II ESTT/4-1/GDS 2ND CYCLE ONLINE ENGAGEMENT/2019 DATED at MUMBAI the 01.11.2019

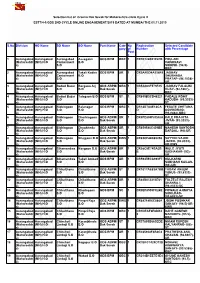

Selection list of Gramin Dak Sevak for Maharashtra circle Cycle II ESTT/4-1/GDS 2ND CYCLE ONLINE ENGAGEMENT/2019 DATED AT MUMBAI THE 01.11.2019 S.No Division HO Name SO Name BO Name Post Name Cate No Registration Selected Candidate gory of Number with Percentage Post s 1 Aurangabad Aurangabad Aurangabad Assegaon GDS BPM OBC 1 CR1E124B21F47B PHULARI (Maharashtr (MH) H.O Cantonment B.O VAISHNAVI a) S.O SHIRISH- (94.5)- OBC 2 Aurangabad Aurangabad Aurangabad Takali Kadim GDS BPM UR 1 CR5AFED4A156F9 JADHAV (Maharashtr (MH) H.O Cantonment B.O SHUBHADA a) S.O PRATAP- (96.1538)- UR 3 Aurangabad Aurangabad Badod Bazar Borgaon Arj GDS ABPM/ OBC 1 CR54A63F573F85 JADHAV FALGUNI (Maharashtr (MH) H.O S.O B.O Dak Sevak VIJAY- (92.1667)- a) OBC 4 Aurangabad Aurangabad Badod Bazar Talegaon B.O GDS BPM ST 1 CR655B3CD46221 PADALE ROHIT (Maharashtr (MH) H.O S.O KADUBA- (89.3333)- a) ST 5 Aurangabad Aurangabad Bidkingaon Balanagar GDS BPM OBC 1 CR14D7A8E14CA FESATE CHETANA (Maharashtr (MH) H.O S.O B.O D GOVINDRAO- a) (93.8462)-OBC 6 Aurangabad Aurangabad Bidkingaon Dhorkingaon GDS ABPM/ UR 1 CR8FE894F8CA8A KALE PRAJKTA (Maharashtr (MH) H.O S.O B.O Dak Sevak JIVAN- (93.3333)- a) UR 7 Aurangabad Aurangabad Bidkingaon Dhupkheda GDS ABPM/ UR 1 CR659586C439BE MAHESH SANTOSH (Maharashtr (MH) H.O S.O B.O Dak Sevak BARGAL- (94)-UR a) 8 Aurangabad Aurangabad Bidkingaon Nilajgaon B.O GDS ABPM/ EWS 1 CR83CF44B85296 SAYYED VAJED (Maharashtr (MH) H.O S.O Dak Sevak JAVED- (92.8333)- a) UR-EWS 9 Aurangabad Aurangabad Bihamandwa Navgaon B.O GDS ABPM/ UR 1 CR08C9E74BA3B