Voice of the Broadcasting Industry Volume 23, Issue 2

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Radio Stations in Michigan Radio Stations 301 W

1044 RADIO STATIONS IN MICHIGAN Station Frequency Address Phone Licensee/Group Owner President/Manager CHAPTE ADA WJNZ 1680 kHz 3777 44th St. S.E., Kentwood (49512) (616) 656-0586 Goodrich Radio Marketing, Inc. Mike St. Cyr, gen. mgr. & v.p. sales RX• ADRIAN WABJ(AM) 1490 kHz 121 W. Maumee St. (49221) (517) 265-1500 Licensee: Friends Communication Bob Elliot, chmn. & pres. GENERAL INFORMATION / STATISTICS of Michigan, Inc. Group owner: Friends Communications WQTE(FM) 95.3 MHz 121 W. Maumee St. (49221) (517) 265-9500 Co-owned with WABJ(AM) WLEN(FM) 103.9 MHz Box 687, 242 W. Maumee St. (49221) (517) 263-1039 Lenawee Broadcasting Co. Julie M. Koehn, pres. & gen. mgr. WVAC(FM)* 107.9 MHz Adrian College, 110 S. Madison St. (49221) (517) 265-5161, Adrian College Board of Trustees Steven Shehan, gen. mgr. ext. 4540; (517) 264-3141 ALBION WUFN(FM)* 96.7 MHz 13799 Donovan Rd. (49224) (517) 531-4478 Family Life Broadcasting System Randy Carlson, pres. WWKN(FM) 104.9 MHz 390 Golden Ave., Battle Creek (49015); (616) 963-5555 Licensee: Capstar TX L.P. Jack McDevitt, gen. mgr. 111 W. Michigan, Marshall (49068) ALLEGAN WZUU(FM) 92.3 MHz Box 80, 706 E. Allegan St., Otsego (49078) (616) 673-3131; Forum Communications, Inc. Robert Brink, pres. & gen. mgr. (616) 343-3200 ALLENDALE WGVU(FM)* 88.5 MHz Grand Valley State University, (616) 771-6666; Board of Control of Michael Walenta, gen. mgr. 301 W. Fulton, (800) 442-2771 Grand Valley State University Grand Rapids (49504-6492) ALMA WFYC(AM) 1280 kHz Box 669, 5310 N. -

Campus Building: Monday Through Thursday 7:00 A.M

HOURS Campus Building: Monday through Thursday 7:00 a.m. to 10:00 p.m. Friday 7:00 a.m. to 5:00 p.m. Saturday 8:00 a.m. to 2:00 p.m. Admissions Office: Monday through Thursday 8:00 a.m. to 6:00 p.m. Friday 8:00 a.m. to 5:00 p.m. Academic Resource Center: Fall, Winter, and Spring Quarters Monday through Thursday 8:00 a.m. to 10:00 p.m. Friday 8:00 a.m. to 5:00 p.m. Saturday 8:00 a.m. to 2:00 p.m. Summer quarter and break hours will be posted in June. Bookstore Hours: Monday through Thursday 8:00 a.m. to 5:00 p.m. Friday and Saturday CLOSED Bookstore hours may vary and students are encouraged to refer to posted hours. Bookstore hours are extended during the last week of each quarter along with the week before classes start and week one of each quarter. During those weeks we will be open Friday 8:00 a.m. to 1:00 p.m. Saturday 9:00 a.m. to 1:00 p.m. OFFICE HOURS Academic Office: Monday through Thursday 7:00 a.m. to 6:00 p.m. Friday 8:00 a.m. to 5:00 p.m. Summer hours vary and will be posted in June. Admissions Office: Monday through Thursday 9:00 a.m. to 6:00 p.m. Friday 8:00 a.m. to 5:00 p.m. Finance Office: Monday through Friday 7:30 a.m. to 4:30 p.m. -

Stations Coverage Map Broadcasters

820 N. Capitol Ave., Lansing, MI 48906 PH: (517) 484-7444 | FAX: (517) 484-5810 Public Education Partnership (PEP) Program Station Lists/Coverage Maps Commercial TV I DMA Call Letters Channel DMA Call Letters Channel Alpena WBKB-DT2 11.2 GR-Kzoo-Battle Creek WOOD-TV 7 Alpena WBKB-DT3 11.3 GR-Kzoo-Battle Creek WOTV-TV 20 Alpena WBKB-TV 11 GR-Kzoo-Battle Creek WXSP-DT2 15.2 Detroit WKBD-TV 14 GR-Kzoo-Battle Creek WXSP-TV 15 Detroit WWJ-TV 44 GR-Kzoo-Battle Creek WXMI-TV 19 Detroit WMYD-TV 21 Lansing WLNS-TV 36 Detroit WXYZ-DT2 41.2 Lansing WLAJ-DT2 25.2 Detroit WXYZ-TV 41 Lansing WLAJ-TV 25 Flint-Saginaw-Bay City WJRT-DT2 12.2 Marquette WLUC-DT2 35.2 Flint-Saginaw-Bay City WJRT-DT3 12.3 Marquette WLUC-TV 35 Flint-Saginaw-Bay City WJRT-TV 12 Marquette WBUP-TV 10 Flint-Saginaw-Bay City WBSF-DT2 46.2 Marquette WBKP-TV 5 Flint-Saginaw-Bay City WEYI-TV 30 Traverse City-Cadillac WFQX-TV 32 GR-Kzoo-Battle Creek WOBC-CA 14 Traverse City-Cadillac WFUP-DT2 45.2 GR-Kzoo-Battle Creek WOGC-CA 25 Traverse City-Cadillac WFUP-TV 45 GR-Kzoo-Battle Creek WOHO-CA 33 Traverse City-Cadillac WWTV-DT2 9.2 GR-Kzoo-Battle Creek WOKZ-CA 50 Traverse City-Cadillac WWTV-TV 9 GR-Kzoo-Battle Creek WOLP-CA 41 Traverse City-Cadillac WWUP-DT2 10.2 GR-Kzoo-Battle Creek WOMS-CA 29 Traverse City-Cadillac WWUP-TV 10 GR-Kzoo-Battle Creek WOOD-DT2 7.2 Traverse City-Cadillac WMNN-LD 14 Commercial TV II DMA Call Letters Channel DMA Call Letters Channel Detroit WJBK-TV 7 Lansing WSYM-TV 38 Detroit WDIV-TV 45 Lansing WILX-TV 10 Detroit WADL-TV 39 Marquette WJMN-TV 48 Flint-Saginaw-Bay -

Fake TV News: Widespread and Undisclosed

Fake TV News: Widespread and Undisclosed A multimedia report on television newsrooms’ use of material provided by PR firms on behalf of paying clients Diane Farsetta and Daniel Price, Center for Media and Democracy April 6, 2006 Center for Media and Democracy 520 University Ave., Suite 227 Madison, WI 53703 Phone: 608-260-9713 Fax: 608-260-9714 Website: www.prwatch.org Contents News Release - 2 Executive Summary - 4 Introduction - 9 Findings: Video News Releases - 14 Findings: TV Stations - 19 Findings: Corporations - 22 Recommendations - 26 Take Action - 32 Frequently Asked Questions - 33 Appendix A: About This Report - 39 Appendix B: VNRs in Detail - 40 1 News Release Press Advisory: New Report: Fake TV News Widespread and Undisclosed Investigation catches 77 local TV stations presenting corporate PR as real news Groups file complaints urging FCC to take action against deceptive broadcasters WASHINGTON The Center for Media Democracy and Free Press today exposed an epidemic of fake news infiltrating local television broadcasts across country. At a press conference in Washington with FCC Commissioner Jonathan S. Adelstein, the groups called for a crackdown on stations that present corporate-sponsored videos as genuine news to an unsuspecting audience. CMD, which unveiled the results of a 10-month investigation, found scores of local stations slipping commercial “video news releases,” or VNRs, into their regular news programming. The new multimedia report released today includes footage of 36 separate VNRs and their broadcast as “news” by TV stations and networks nationwide, including those in the nation’s biggest markets. The full report -- “Fake TV News: Widespread and Undisclosed” -- is now available complete with VNR and TV station video footage at www.prwatch.org/fakenews/execsummary. -

Voice of the Broadcasting Industry Volume 22, Issue 12

December 2005 Voice of the Broadcasting Industry Volume 22, Issue 12 $8.00 USA $12.50 Canada-Foreign RADIORADIO NEWS ® NEWS Froogle shopping site, found a grand total of three possibilities—two Hurry 2006, we can’t wait! actually, since two were for the same Panasonic in-dash car receiver. It From listening to the Q3 Wall Street conference calls, it seems to did not have multicasting and was offered by a total of 56 merchants us that many broadcasters would be happy to have 2006 begin for prices ranging from $308 to $500. The other listing was for the right away and not have to deal with Q4 of 2005. Pretty much Boston Acoustics Receptor Radio, a table model which does have HD everyone complained that the national spot market is soft, so multicasting—at least, it will once the manufacturer actually begins they all touted how great their stations are doing on pushing shipping them. J&R Music is taking reservations at $499. Although it local sales. Even the normally red-hot Spanish broadcasting sec- didn’t come up on Froogle, Crutchfield is also taking reservations for tor is singing the blues, projecting single digit revenue gains rather the same model, although it is charging 99 cents more. We actually than double digits. But then, many of their general market breth- had better luck on eBay, where quite a few people were offering ren would be happy to see any positive number. various Kenwood and Panasonic in-dash models. Of course, the lack of political dollars hit TV stations hard in the By the way, a Froogle search for XM radios produced over second half of 2005, so everyone is salivating over their expected 14,000 hits and a search for Sirius radios brought over 11,000. -

Alphabetical Index

Alphabetical Index 1st Source Corporation 3 Aerojet-General Corporation 12 Allied/Egry Business Systems, Inc 25 20th Century Industries 3 Aeronautical Electric Co 13 Allied Materials Corporation 26 3COM Corporation 3 Aeronca Inc 13 Allied Paper Inc 26 3M 3 Aeroquip Corporation 13 Allied Products Company 26 A A Brunell Electroplating Aerospace Corporation 13 Allied Products Corporation 26 Corporation 4 Aetna Life & Casualty Company 13 Allied Security Inc 26 A B Dick Company 4 Aetna Life Insurance & Annuity Co 13 Allied Stores Corporation 26 A C Nielsen Co 4 Aetna Life Insurance Co 14 Allied Van Lines, Inc 27 A E Staley Mfg Co 4 Affiliated Bank Corporation of Allied-Lyons North America A G Edwards Inc 4 Wyoming 14 Corporation 27 A H Belo Corporation 4 Affiliated Bankshares of Colorado 14 Allied-Signal Aerospace Company 27 A H Robins Company, Inc 4 Affiliated Food Stores, Inc 14 Allied-Signal, Inc 27 A Johnson & Company, Inc 4 Affiliated Hospital Products, Inc 14 Allis-Chalmers Corporation 28 A L Williams Corporation (The) 4 Affiliated Publications, Inc 15 Allstate Insurance Group 28 A M Castle & Co 4 AFG Industries, Inc 15 Alltel Corporation 28 A 0 Smith Corporation 4 Ag Processing Inc 15 Alma Plastics Companies 28 A P Green Refractories Co 4 Agency-Rent-A-Car Inc 15 Aloha Inc 28 A Schulman Inc 4 AGRI Industries 16 Alpha Corporation of Tennessee 28 AT Cross Co 4 AGRIPAC Inc 16 Alpha Industries Inc 28 A Y McDonald Industries, Inc 4 Ags Computers Inc 16 Alpha Metals, Inc 29 A&E Products Group, Inc 4 AGWAY Inc 16 Alpha Microsystems 29 A&M Food -

Federal Communications Commission Record DA 96-262

11 FCC Red No.7 Federal Communications Commission Record DA 96-262 3. Under the Act, however, the Commission is also di- Before the rected to consider changes in AD! areas. Section Federal Communications Commission 614(h)(1)(C) provides that the Commission may: Washington, D.C. 20554 with respect to a particular television broadcast sta- tion, include additional communities within its tele- In re vision market or exclude communities from such station's television market to better effectuate the Liberty Corporation CSR-41 10-A purposes of this section. Biloxi, Mississippi In considering such requests, the Act provides that: For Modification of the Biloxi-Gulfport- Pascagoula, Mississippi AD! the Commission shall afford particular attention to the value of localism by taking into account such factors as -- MEMORANDUM OPINION AND ORDER (I) whether the station, or other stations located in Adopted: February 28, 1996; the same area, have been historically carried on the Released: March 20, 1996 cable system or systems within such community; By the Cable Services Bureau: (II) whether the television station provides coverage or other local service to such community; (III) whether any other television station that is eli- INTRODUCTION gible to be carried by a cable system in such commu- nity in fulfillment of the requirements of this section 1. Liberty Corporation,1 licensee of Station WLOX-TV provides news coverage of issues of concern to such (ABC, Ch. 13), Biloxi, Mississippi, has filed a petition for community or provides carriage or coverage of sport- special relief seeking to include the communities of Pica- ing and other events of interest to the community; yune, Kiln, Lucedale, and the unincorporated areas of and Hancock County, Mississippi in the Biloxi-Gulfport- (IV) evidence of viewing patterns in cable and Pascagoula, Mississippi AD! for purposes of the Commis- noncable households within the areas served by the sion's mandatory signal carriage rules. -

Broadcast Actions 9/23/2004

Federal Communications Commission 445 Twelfth Street SW PUBLIC NOTICE Washington, D.C. 20554 News media information 202 / 418-0500 Recorded listing of releases and texts 202 / 418-2222 REPORT NO. 45826 Broadcast Actions 9/23/2004 STATE FILE NUMBER E/P CALL LETTERS APPLICANT AND LOCATION N A T U R E O F A P P L I C A T I O N Actions of: 09/13/2004 DIGITAL TV APPLICATIONS FOR LICENSE TO COVER GRANTED ND BLEDT-20031104ABX KSRE-DT PRAIRIE PUBLIC License to cover construction permit no: BMPEDT-20030616AAE, 53313 BROADCASTING, INC. callsign KSRE. E CHAN-40 ND , MINOT Actions of: 09/20/2004 FM TRANSLATOR APPLICATIONS FOR MAJOR MODIFICATION TO A LICENSED FACILITY DISMISSED NC BMJPFT-20030312AJR DW282AJ TRIAD FAMILY NETWORK, INC. Major change in licensed facilities 87018 E NC , BURLINGTON Dismissed per applicant's request-no letter was sent. 104.5 MHZ TELEVISION APPLICATIONS FOR ASSIGNMENT OF LICENSE DISMISSED MT BALCT-20040305ACI KTGF 13792 MMM LICENSE LLC Voluntary Assignment of License, as amended From: MMM LICENSE LLC E CHAN-16 MT , GREAT FALLS To: THE KTGF TRUST, PAUL T. LUCCI, TRUSTEE Form 314 AM STATION APPLICATIONS FOR RENEWAL GRANTED OH BR-20040329AIT WJYM 31170 FAMILY WORSHIP CENTER Renewal of License CHURCH, INC. E 730 KHZ OH , BOWLING GREEN Page 1 of 158 Federal Communications Commission 445 Twelfth Street SW PUBLIC NOTICE Washington, D.C. 20554 News media information 202 / 418-0500 Recorded listing of releases and texts 202 / 418-2222 REPORT NO. 45826 Broadcast Actions 9/23/2004 STATE FILE NUMBER E/P CALL LETTERS APPLICANT AND LOCATION N A T U R E O F A P P L I C A T I O N Actions of: 09/20/2004 AM STATION APPLICATIONS FOR RENEWAL GRANTED MI BR-20040503ABD WLJW 73169 GOOD NEWS MEDIA, INC. -

First Amendment Awards Sponsors Diamond Hubbard Broadcasting, Inc

First AmendmentHONORING CHAMPIONS OF Awards FREEDOM OF THE PRESS March 14, 2017 | Grand Hyatt Washington | #RTDNFirst CNN Newsource Since 1987, CNN Newsource has partnered with you to bring local audiencesAd theFull best Page news coverage possible. In 2017, there has never been a greater time or need for excellence in journalism. WE SALUTE THIS YEAR’S HONOREES. CNN Newsource is a proud sponsor of RTDNF. Two organizations committed to excellence in journalism. cnn.com/newsource CongratulationsTO THE 2017 RTDNF FIRST AMENDMENT AWARD HONOREES YOUR FriendsAT RTDNA AND RTDNF VINCENT DUFFY DAVID WAGNER KYM GEDDES News Director, Michigan Radio News Director, KLST/KSAN-TV News Director, CFRB-AM RTDNA Chairman Region 6 Director Region 14 Director KATHY WALKER JAM SARDAR SEAN MCGARVY News Director News Director, WLNS-TV Managing Editor, KDVR/KWGN-TV KOA-AM, RTNDF Chairwoman Region 7 Director Director-at-Large SCOTT LIBIN ANDREA PARQUET-TAYLOR CHIP MAHANEY Hubbard Senior Fellow News Director, WNCN-TV News Director, WCPO-TV University of Minnesota Region 8 Director Director-at-Large RTDNA Chair-Elect GARY WORDLAW KIMBERLY WYATT LOREN TOBIA News Director, WVLA/WGMB-TV News Director, WEAR-TV RTDNA Treasurer Region 9 Director Director-at-Large DAN SHELLEY ANDREW VREES BLAISE LABBE RTDNF Treasurer Vice President of News News Director, WOAI/KABB-TV Hearst Television Director-at-Large ERICA HILL Region 10 Director News Director, KCPQ-TV DAVID LOUIE Region 1 Director TIM SCHELD Reporter, KGO-TV Director of News and Programming RTDNF Trustee BRANDON MERCER WCBS-AM Executive Producer, SFGATE Region 11 Director JANICE GIN Region 2 Director Assistant News Director, KRON-TV MARK KRAHAM RTDNF Trustee SHERYL WORSLEY News Director, WHAG-TV News Director, KSL-AM Region 12 Director MIKE CAVENDER Region 3 Director Executive Director, RTDNA/F TERENCE SHEPHERD MARK MILLAGE News Director, WLRN-FM Regional Director, Media Mindield Region 13 Director Region 4 Director Text GIVE to 202-471-1949 | 1 Thank you to our Oldfield Founders Circle donors for your generosity and commitment to our mission. -

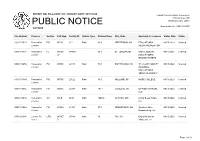

Public Notice >> Licensing and Management System Admin >>

REPORT NO. PN-2-200917-01 | PUBLISH DATE: 09/17/2020 Federal Communications Commission 445 12th Street SW PUBLIC NOTICE Washington, D.C. 20554 News media info. (202) 418-0500 ACTIONS File Number Purpose Service Call Sign Facility ID Station Type Channel/Freq. City, State Applicant or Licensee Status Date Status 0000113523 Renewal of FM WCVJ 612 Main 90.9 JEFFERSON, OH EDUCATIONAL 09/15/2020 Granted License MEDIA FOUNDATION 0000114058 Renewal of FL WSJB- 194835 96.9 ST. JOSEPH, MI SAINT JOSEPH 09/15/2020 Granted License LP EDUCATIONAL BROADCASTERS 0000116255 Renewal of FM WRSX 62110 Main 91.3 PORT HURON, MI ST. CLAIR COUNTY 09/15/2020 Granted License REGIONAL EDUCATIONAL SERVICE AGENCY 0000113384 Renewal of FM WTHS 27622 Main 89.9 HOLLAND, MI HOPE COLLEGE 09/15/2020 Granted License 0000113465 Renewal of FM WCKC 22183 Main 107.1 CADILLAC, MI UP NORTH RADIO, 09/15/2020 Granted License LLC 0000115639 Renewal of AM WILB 2649 Main 1060.0 CANTON, OH Living Bread Radio, 09/15/2020 Granted License Inc. 0000113544 Renewal of FM WVNU 61331 Main 97.5 GREENFIELD, OH Southern Ohio 09/15/2020 Granted License Broadcasting, Inc. 0000121598 License To LPD W30ET- 67049 Main 30 Flint, MI Digital Networks- 09/15/2020 Granted Cover D Midwest, LLC Page 1 of 62 REPORT NO. PN-2-200917-01 | PUBLISH DATE: 09/17/2020 Federal Communications Commission 445 12th Street SW PUBLIC NOTICE Washington, D.C. 20554 News media info. (202) 418-0500 ACTIONS File Number Purpose Service Call Sign Facility ID Station Type Channel/Freq. -

530 CIAO BRAMPTON on ETHNIC AM 530 N43 35 20 W079 52 54 09-Feb

frequency callsign city format identification slogan latitude longitude last change in listing kHz d m s d m s (yy-mmm) 530 CIAO BRAMPTON ON ETHNIC AM 530 N43 35 20 W079 52 54 09-Feb 540 CBKO COAL HARBOUR BC VARIETY CBC RADIO ONE N50 36 4 W127 34 23 09-May 540 CBXQ # UCLUELET BC VARIETY CBC RADIO ONE N48 56 44 W125 33 7 16-Oct 540 CBYW WELLS BC VARIETY CBC RADIO ONE N53 6 25 W121 32 46 09-May 540 CBT GRAND FALLS NL VARIETY CBC RADIO ONE N48 57 3 W055 37 34 00-Jul 540 CBMM # SENNETERRE QC VARIETY CBC RADIO ONE N48 22 42 W077 13 28 18-Feb 540 CBK REGINA SK VARIETY CBC RADIO ONE N51 40 48 W105 26 49 00-Jul 540 WASG DAPHNE AL BLK GSPL/RELIGION N30 44 44 W088 5 40 17-Sep 540 KRXA CARMEL VALLEY CA SPANISH RELIGION EL SEMBRADOR RADIO N36 39 36 W121 32 29 14-Aug 540 KVIP REDDING CA RELIGION SRN VERY INSPIRING N40 37 25 W122 16 49 09-Dec 540 WFLF PINE HILLS FL TALK FOX NEWSRADIO 93.1 N28 22 52 W081 47 31 18-Oct 540 WDAK COLUMBUS GA NEWS/TALK FOX NEWSRADIO 540 N32 25 58 W084 57 2 13-Dec 540 KWMT FORT DODGE IA C&W FOX TRUE COUNTRY N42 29 45 W094 12 27 13-Dec 540 KMLB MONROE LA NEWS/TALK/SPORTS ABC NEWSTALK 105.7&540 N32 32 36 W092 10 45 19-Jan 540 WGOP POCOMOKE CITY MD EZL/OLDIES N38 3 11 W075 34 11 18-Oct 540 WXYG SAUK RAPIDS MN CLASSIC ROCK THE GOAT N45 36 18 W094 8 21 17-May 540 KNMX LAS VEGAS NM SPANISH VARIETY NBC K NEW MEXICO N35 34 25 W105 10 17 13-Nov 540 WBWD ISLIP NY SOUTH ASIAN BOLLY 540 N40 45 4 W073 12 52 18-Dec 540 WRGC SYLVA NC VARIETY NBC THE RIVER N35 23 35 W083 11 38 18-Jun 540 WETC # WENDELL-ZEBULON NC RELIGION EWTN DEVINE MERCY R. -

Liberty Industries, LC

Tower Engineering Packages MOECKER AUCTIONS, INC. www.moeckerauctions.com AUCTION CATALOG LIBERTY INDUSTRIES, L.C. Case #18-14231-EPK LIBERTY PROPERTIES AT NEWBURGH, L.C. Case #18-14232-EPK Liberty Industries, LC Intellectual Property List - COMPANY CONFIDENTIAL BROADCAST TOWER PORTFOLIO Color Key Fab Fabrication Design Drawings Install Installation Drawing FND Foundation Design Drawings Soil Info Geotechnical Data Survey Site Survey Data Steel Yld Steel Yield Strength Data Pkg. Repack Towers Impacted by FCC Mandated Repack Tower Soil Lot # Job # City State Call Letters Company Fab Install FND Survey Steel Yld Repack Height Info 2 3876 Anniston AL 502 WJSU X X X X X 3 523 Birmingham AL 709 Dick Broadcasting Co. X X X X X X 4 3305 Birmingham2 AL 986 WBRC WBRC, LLC X X X X X X 5 4202 Birmingham4 AL 964 WVTM Reliable Broadcasting, Inc. X X X X 6 ST Birmingham4 AL 964 WVTM WVTM Hearst Television Inc X 7 2497 Bradley AL 1100 WFBD Flinn Broadcasting Corp X X X X X X X 8 249 Centerville AL 407 Mike Tierney X X X X X X 9 1078 Clear Springs AL 942 CR Baldwin L.L.C. X X X X X X 10 277 Elgin AL 499 WFIX WFIX-FM X X X X X X 11 658 Florence AL 1350 WOWL WOWL-TV X X X X X X 12 3895 Gadsden AL 961 WNAL Cox Radio X X X X 13 5074-1 Mobile AL 1197 WALA X X X X 14 7281 Montgomery2 AL 729 WKAB X X X X X X 15 3083 Montgomery3 (1 OF 2) AL 2000 WSFA WSFA LLC X X X X X X X 16 3346 Montgomery4 AL 1745.5 WHOA KAMR-TV X X X X X X 17 69 Opelika AL 640 WLGA American Tower LLC X X X X X X 18 3228 Tuscaloosa AL 2000 WDBB WTTO Inc.