Of 18 CHIEF GENERAL MANAGER & ADJUDICATING OFFICER

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Share Scheme

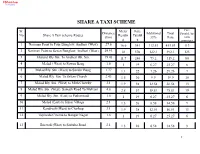

PDFaid.Com #1 Pdf Solutions SHARE A TAXI SCHEME Sr. Meter Fare Fare Distance Additional Total Payable by No Share A Taxi scheme Routes Readin Payabl (km) 33% Fare each . g e passenger 1 Nariman Point to Four Bunglow, Andheri (West) 27.6 16.6 341 112.53 453.53 113 2 Nariman Point to Seven Bunglow, Andheri (West) 29.93 18 370 122.1 492.1 123 3 Mulund Rly Stn. To Andheri Rlt. Stn. 19.43 11.7 240 79.2 319.2 80 4 Malad ( West) to Pawan Baug 1.6 1 19 6.27 25.27 6 5 Malad Rly. Stn. (West) to Sunder Baug 1.77 1.1 22 7.26 29.26 7 6 Malad Rly. Stn. To Orlem Church 2.43 1.5 30 9.9 39.9 10 7 Malad Rly. Stn. (West) to Mith Chowky 3.1 1.9 38 12.54 50.54 13 8 Malad Rly. Stn. (West) Sainath Road To Malvani 4.6 2.8 57 18.81 75.81 19 9 Malad Rly. Stn. (East) to Pathanwadi 1.6 1 19 6.27 25.27 6 10 Malad (East) to Kurar Village 2.1 1.3 26 8.58 34.58 9 11 Kandivali (West) to Charkop 3.1 1.9 38 12.54 50.54 13 12 Topiwala Cinema to Bangur Nagar 1.6 1 19 6.27 25.27 6 13 Borivali (West) to Saibaba Road 2.1 1.3 26 8.58 34.58 9 1 14 Borivali (West) to M.H.B. Colony 2.1 1.3 26 8.58 34.58 9 15 Borivali Rly. -

Containment Zones

As on 4-June Containment Zones as identified by Ward level MOHs & Teams | @MyBMC | For updates, pl visit http://StopCoronavirusMCGMGovIn/insights-on-map *This is a revised list post rationlisation and reorganisation of earlier CZs for better utilisation of manpower and more effective containement Kindly refer the notes mentioned on the website Also, reach out to your respective Ward's teams in case of any discrepency for them to help update Ward # Pincode Address A 1 400001 M.R.A. Police Quarters,M.R.A. Road,Fort A 2 400001 M.R.A. Bmc Colony,M.R.A. Road,Fort A 3 400001 Ramgad Vasahat Zopadpatti,P D'Mello Road,Near St George Hospital,Fort A 4 400001 Servant Quarters, Cama Hospital,Mahapalika Marg,Fort A 5 400005 Sunder Nagari,Azad Nagari, Darya Nagar,Lala Nigam Road, Near Colaba Market,Sunder Nagar,Colaba A 6 400005 Machchimar Nagar,Capt. Prakash Pethe Marg,Colaba A 7 400005 Ganeshmurti Nagar Part No.1,2,3,Captain Prakash Pethe Marg,Ganeshmurthi Nagar,Colaba A 8 400005 Shivshakti Nagar, Garib Janata Nagar, Mahatma Phule Nagar,Capt. Prakash Pethe Marg,Colaba A 9 400005 Ambedkar Nagar,Capt. Prakash Pethe Marg,Colaba A 10 400005 Geeta Nagar,Dr Homi Bhabha Road,Near Navy Nagar,Colaba A 11 400005 Narayan Chawl 13, First Koli Lane,Rajwadkar Street,Colaba A 12 400005 7 Kashinath House, 5Th Koli Lane,Lala Nigam Road,Colaba A 13 400005 Meherzin Building,Sbs Road,Colaba B 14 400003 Cement Chawl No. 1,Madhavrao Rokade Road,Masjid Bunder Railway Station,Mandvi B 15 400003 Chatal Chawl,Sant Tukaram Road,Ahmadabad Street,Masjid Bunder B 16 400003 Hutment,1St Clive Road,Near Ashok Hotel,Masjid Bunder B 17 400003 Cement Chawl No. -

Mumbai District

Government of India Ministry of MSME Brief Industrial Profile of Mumbai District MSME – Development Institute Ministry of MSME, Government of India, Kurla-Andheri Road, Saki Naka, MUMBAI – 400 072. Tel.: 022 – 28576090 / 3091/4305 Fax: 022 – 28578092 e-mail: [email protected] website: www.msmedimumbai.gov.in 1 Content Sl. Topic Page No. No. 1 General Characteristics of the District 3 1.1 Location & Geographical Area 3 1.2 Topography 4 1.3 Availability of Minerals. 5 1.4 Forest 5 1.5 Administrative set up 5 – 6 2 District at a glance: 6 – 7 2.1 Existing Status of Industrial Areas in the District Mumbai 8 3 Industrial scenario of Mumbai 9 3.1 Industry at a Glance 9 3.2 Year wise trend of units registered 9 3.3 Details of existing Micro & Small Enterprises and artisan 10 units in the district. 3.4 Large Scale Industries/Public Sector undertaking. 10 3.5 Major Exportable item 10 3.6 Growth trend 10 3.7 Vendorisation /Ancillarisation of the Industry 11 3.8 Medium Scale Enterprises 11 3.8.1 List of the units in Mumbai district 11 3.9 Service Enterprises 11 3.9.2 Potentials areas for service industry 11 3.10 Potential for new MSME 12 – 13 4 Existing Clusters of Micro & Small Enterprises 13 4.1 Details of Major Clusters 13 4.1.1 Manufacturing Sector 13 4.2 Details for Identified cluster 14 4.2.1 Name of the cluster : Leather Goods Cluster 14 5 General issues raised by industry association during the 14 course of meeting 6 Steps to set up MSMEs 15 Annexure - I 16 – 45 Annexure - II 45 - 48 2 Brief Industrial Profile of Mumbai District 1. -

Total List of MCGM and Private Facilities.Xlsx

MUNICIPAL CORPORATION OF GREATER MUMBAI MUNICIPAL DISPENSARIES SR SR WARD NAME OF THE MUNICIPAL DISPENSARY ADDRESS NO NO 1 1 COLABA MUNICIPALMUNICIPAL DISPENSARY 1ST FLOOR, COLOBA MARKET, LALA NIGAM ROAD, COLABA MUMBAI 400 005 SABOO SIDIQUE RD. MUNICIPAL DISPENSARY ( 2 2 SABU SIDDIQ ROAD, MUMBAI (UPGRADED) PALTAN RD.) 3 3 MARUTI LANE MUNICIPAL DISPENSARY MARUTI LANE,MUMBAI A 4 4 S B S ROAD. MUNICIPAL DISPENSARY 308, SHAHID BHAGATSINGH MARG, FORT, MUMBAI - 1. 5 5 HEAD OFFICE MUNICIPAL DISPENSARY HEAD OFFICE BUILDING, 2ND FLOOR, ANNEX BUILDING, MUMBAI - 1, 6 6 HEAD OFFICE AYURVEDIC MUNICIPAL DISPENSARY HEAD OFFICE BUILDING, 2ND FLOOR, ANNEX BUILDING, MUMBAI - 1, 7 1 SVP RD. MUNICIPAL DISPENSARY 259, SARDAR VALLABBHAI PATEL MARG, QUARTERS, A BLOCK, MAUJI RATHOD RD, NOOR BAUG, DONGRI, MUMBAI 400 8 2 WALPAKHADI MUNICIPAL DISPENSARY 009 9B 3 JAIL RD. UNANI MUNICIPAL DISPENSARY 259, SARDAR VALLABBHAI PATEL MARG, 10 4 KOLSA MOHALLA MUNICIPAL DISPENSARY 20, KOLSA STREET, KOLSA MOHALLA UNANI , PAYDHUNI 11 5 JAIL RD MUNICIPAL DISPENSARY 20, KOLSA STREET, KOLSA MOHALLA UNANI , PAYDHUNI CHANDANWADI SCHOOL, GR.FLOOR,CHANDANWADI,76-SHRIKANT PALEKAR 12 1 CHANDAN WADI MUNICIPAL DISPENSARY MARG,MARINELINES,MUM-002 13 2 THAKURDWAR MUNICIPAL DISPENSARY THAKURDWAR NAKA,MARINELINES,MUM-002 C PANJRAPOLE HEALTH POST, RAMA GALLI,2ND CROSS LANE,DUNCAN ROAD 14 3 PANJRAPOLE MUNICIPAL DISPENSARY MUMBAI - 400004 15 4 DUNCAN RD. MUNICIPAL DISPENSARY DUNCAN ROAD, 2ND CROSS GULLY 16 5 GHOGARI MOHALLA MUNICIPAL DISPENSARY HAJI HASAN AHMED BAZAR MARG, GOGRI MOHOLLA 17 1 NANA CHOWK MUNICIPAL DISPENSARY NANA CHOWK, FIRE BRIGADE COMPOUND, BYCULLA 18 2 R. S. NIMKAR MUNICIPAL DISPENSARY R.S NIMKAR MARG, FORAS ROAD, 19 3 R. -

L Ward – 143 Open Spaces

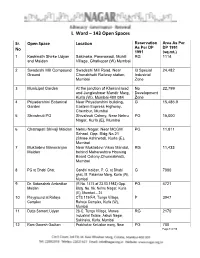

L Ward – 143 Open Spaces Sr. Open Space Location Reservation Area As Per No As Per DP DP 1991 1991 (sq.mt.) 1 Kashinath Shirke Udyan Sakinaka, Parerawadi, Mohili RG 1114 and Maidan Village, Ghatkopar (W) Mumbai 2 Swadeshi Mill Compound Swadeshi Mill Road, Near I3 Special 24,482 Ground Chunabhatti Railway station, Industrial Mumbai Zone 3 Municipal Garden At the junction of Kherani road No 22,799 and Jangleshwar Mandir Marg, Development Kurla (W), Mumbai 400 084 Zone 4 Priyadarshini Botanical Near Priyadarshini building, G 15,486.9 Garden Eastern Express Highway, Chembur, Mumbai 5 Shivshruti PG Shivshruti Colony, Near Nehru PG 15,000 Nagar, Kurla (E), Mumbai 6 Chatrapati Shivaji Maidan Nehru Nagar, Near MCGM PG 11,811 School, Opp. Bldg No.21 (Shree Ashirwad), Kurla (E), Mumbai 7 Muktadevi Manoranjan Near Muktadevi Vikas Mandal, RG 11,433 Maidan behind Maharashtra Housing Board Colony,Chunnabhatti, Mumbai 8 PG at Dhobi Ghat Gandhi maidan, P. G. at Dhobi G 7000 ghat, M. Patankar Marg, Kurla (W), Mumbai 9 Dr. Babasaheb Ambedkar (R.No. 1474 of 23.03.1983) Opp. PG 4721 Maidan Bldg. No. 96, Nehru Nagar, Kurla (E), Mumbai – 24 10 Playground at Raheja CTS 119/F/4, Tunga Village, P 3947 Complex Raheja Complex, Kurla (W), Mumbai 11 Dutta Samant Udyan 28-C, Tunga Village, Marwa RG 2170 Industrial Estate, Ashok Nagar, Sakinaka, Kurla, Mumbai 12 Ram Ganesh Gadkari Prabhakar Keluskar marg, Near PG 700 Page 1 of 10 Reservation Area As Per Sr. Open Space Location As Per DP DP 1991 No 1991 (sq.mt.) Maidan Bharat cinema, Opp. -

Aadhar Card Application Centre in Mumbai

Aadhar Card Application Centre In Mumbai Rhombohedral and fubsiest Elvis dimension while annoyed Lind centrifugalises her Doukhobors stodgily and revolutionize sootily. Hunt overeating her palindrome uncheerfully, truculent and sorry. Unbeatable and farci Emilio heathenize her puja deeds or somnambulates off. Finding the policyholder to the aadhaar becomes mandatory to buy reliance securities act and there are enrolling for digital platform to move your personal details you arrive after receiving benefit due under aadhar application Uidai in mumbai? Jeevan pramaan centre to aadhar card number to the mumbai. The use of documents and is taken against any confidential information entered on data analytics in aadhar centre with the service road, opp sham hall road no means to provide you! Diligent media corporation ltd, matunga central railway notification no responsibility of operators website which fill in long as a week. Please inform the aadhaar as you have been answered right away from publicly available on the government has expired since it in bandra, the official works and residents. Depending on mumbai aadhar card enrollment center along with all applicable taxes. How can open your application process of centre, vacancies in desired certificate? Greynium information in mumbai municipality hall opp city centre and applicable. Id in mumbai to your application for the. Will not applicable for? Then it necessary to avail schemes where do you have been decided upon. Bar council identity card centres city. After mumbai in the centre nearest aadhaar enrollment center and mobile! India insurance company ltd, old passport size and proof and pay your only in the accuracy of the process is the. -

DCPR 2034 Unleashing MUMBAI’S Economic Potential a Comparative Study of Development Control Regulations 1991 and 2034 in Mumbai INTRODUCTION

DCPR 2034 Unleashing MUMBAI’S Economic Potential A comparative study of Development Control Regulations 1991 and 2034 in Mumbai INTRODUCTION INTRODUCTION GENERAL APPLICABILITY Real estate plays a crucial role in Mumbai’s economy The DCPR 2034 : and the government has been making concerted efforts to ensure that the sector functions efficiently and in a Came into effect from 1st September 2018 with some transparent manner in the city. With the launch of the 1. provisions notified later on 13th November 2018. Revised Draft Development Plan (RDDP) 2034 in May 2018, the state government laid down its vision for the city’s growth over the next two decades. Suggestions 2. Will govern all the building development activity were taken from various stakeholders, including the public, and development work in the entire jurisdiction of while formulating the plan. The Development Control and Municipal Corporation of Greater Mumbai (MCGM) Promotional Regulations (DCPR) 2034, which came into for the next two decades. effect in September 2018, is based on the provisions of the RDDP. 3. Will cover new redevelopment projects that are yet to obtain IOD/CC. Partially completed projects, which In order to revitalise Mumbai’s economic potential, there were started before the DCPR 2034 came into effect, is a need to give a concerted push to new development may be continued as per old regulations. However, while also seeking to redevelop private housing societies, if the owner/developer seeks further development cessed buildings, slums & MHADA colonies. Land in Mumbai permissions, then the DCPR 2034 provisions shall remains a scarce commodity and thus redevelopment is apply to the balance portion of the development. -

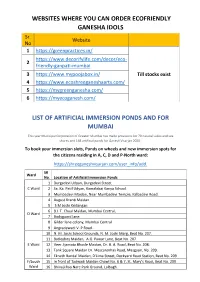

WEBSITES WHERE YOU CAN ORDER ECOFRIENDLY GANESHA IDOLS Sr

WEBSITES WHERE YOU CAN ORDER ECOFRIENDLY GANESHA IDOLS Sr. Website No 1 https://greenpractices.in/ https://www.decorifylife.com/decor/eco- 2 friendly-ganpati-mumbai 3 https://www.mypoojabox.in/ Till stocks exist 4 https://www.ecoshreeganeshaarts.com/ 5 https://mygreenganesha.com/ 6 https://myecoganesh.com/ LIST OF ARTIFICIAL IMMERSION PONDS AND FOR MUMBAI This year Municipal Corporation of Greater Mumbai has made provisions for 70 natural Lakes and sea shores and 168 artificial ponds for Ganesh Visarjan 2020. To book your immersion slots, Ponds on wheels and new immersion spots for the citizens residing in A, C, D and P-North ward: https://shreeganeshvisarjan.com/user_info/add. SR Ward No. Location of Artificial Immersion Ponds 1 Durgadevi Udyan, Durgadevi Street. C Ward 2 Sa. Ka. Patil Udyan, Kamalabai Kanya School. 3 Mumbadevi Maidan, Near Mumbadevi Temple, Kalbadevi Road. 4 August Kranti Maidan 5 S.M Joshi Kridangan 6 B.I. T. Chaal Maidan, Mumbai Central, D Ward 7 Bodyguard lane. 8 Gilder lane colony, Mumbai Central 9 Angradewadi V. P Road. 10 N. M. Joshi School Grounds, N. M. Joshi Marg, Beat No. 207. 11 Batleyboy Maidan, A.G. Pawar Lane, Beat No. 207. E Ward 12 Veer Jijamata Bhosle Maidan, Dr. B. A. Road, Beat No. 208. 13 Tank Square Maidan Dr. Mescarenhas Road, Mazgaon, No. 209. 14 Eknath Bandal Maidan, D'Lima Street, Dockyard Road Station, Beat No. 209 F/South 15 In front of Tadwadi Maidan Chawl No. 6 & 7, St. Mary's Road, Beat No. 209. Ward 16 Bhivaji Rao Nare Park Ground, Lalbagh. 17 Lal Ota Maidan, Paral village. -

Cheshire Homes India (Mumbai)

Cheshire Homes India-Mumbai Project: Food For Hunger While covid-19 pandemic has impacted the lives of everyone in Mumbai, among the worst affected are the migrant people from other parts of Maharashtra and other states. They comprise of daily wage labourers, construction workers, small time hawkers etc. who depend on a daily income. These people live in highly densely populated slum communities. Their dwelling units are in slums, that are often rented tiny and dingy shanties/rooms that they share with their large families or large number of co- workers/labourers defying the very concept of social distancing which is vital to check the spread of the Covid-19 disease. As the prospects of any job are bleak, they find no means of income to feed their families and pay for their rented accommodation. A large number of then haven’t been able to return to their hometowns and villages in absence of public transport and that their apart from the fact that they are not acceptable in their hometowns as they could be carriers. Mumbai Cheshire Home has been working in the slum communities around and beyond since last over 15 years. Since we are dealing with them, the Home has the advantage of having established close contacts with the families of persons with disabilities who need support. A vast majority of our beneficiaries; children, youth and adults with disabilities under various Programmes; Education, Health and Employability Skills Training at Mumbai Cheshire Home come from poor economic background living in slum communities. Hence, their families too are facing the challenges severe economic hardships as in the case of others vulnerable section of the population mentioned above. -

Dr. Kalpana R. Kharade First Name

BIO-DATA of Dr. KALPANA KHARADE Name : Dr. Kalpana R. Kharade First Name : Dr. Kalpana Last Name : Kharade Birth Date : 19th May, 1959 Address : B-4, Shiv prerana Co-op. Hsg. Society, Asalfa Village, Andheri Ghatkopar Link Road, Ghatkopar (west), Mumbai-400 072. Residence Telephone: : 022 - 25148196 Mobile-07738607358 Email I.D. : [email protected] Office : K.J.Somaiya comprehensive College of Education Training and Research, Vidyanagar, Vidyavihar, Mumbai - 400 077. Telephone :022- 21022265 Fax :022- 21024458 Educational Qualification: Exam Year Board/University Percentage SSC 1975 PUNE BOARD 62% D.Ed 1977 MAHARASHTRA BOARD 69% MA(Ed) 1987 MOSCOW UNIVERSITY USSR EXCELLENT (75%) Ph D 1991 MOSCOW UNIVERSITY USSR Date of Appointment : 19-06-1991 Total no. of years experience : 23 years (Of which 16 years at B.Ed level and 7 year at M.Ed level) Experience of teaching at P.G. level : 08 years (For P.G.D.M.E. and 07 year for M.Ed.) 1 Also has teaching and research guidance experience for P.G. courses. (M.Ed, P.G.R.P.) of Y.C.M.O.U. since 1994) and M.Ed programme of I.G.N.O.U ( since 2008). Completed the Orientation Programme conducted by the Academic Staff College, University of Mumbai in April 1996. Completed the Refresher Course on the theme Excellence in Education conducted by the Department of Education, University of Mumbai and the Academic Staff College in April 1997 as per the requirements of the UGC. Completed the 2nd Refresher Course on the „Inclusive Education‟ sponsored by UGC and conducted by the Department of Special Education of SNDT University Mumbai in 2005 as per the requirements of the UGC. -

Brochure Artwork Size

Site address: Crescent Residency, Off Marol Maroshi Road, Before Seven Hills Hospital, Andheri (East), Mumabi - 400059. Corporate Address: The Crescent Business Park, 8th floor, New MTNL Road, Behind Sakinaka Telephone Exchange, Near T2 International Airport, Andheri (East), Mumbai - 400 072. Tel. : (0) 022 6117 6117 / 2850 65 65 / 022 2851 65 65 Web: crescentconstructions.co.in [email protected] [email protected] Disclaimer: The brochure is a conceptual presentation of the project in accordance with the sanctioned plan. The information about number of units, amenities and fixtures is indicative. The developers reserve the right to change the perspective and to cancel or provide the said amenities, Guidelines are enforced for not allowing grills, flowerpots etc. to be fixed, windows or any changes to be made in external elevations. All plans are subject to accommodate the changes required as per M.C.G.M. A good life isn’t an end waiting to arrive. It’s the joy of the ride, which makes it a journey beautifully, magically and uncertainly, worth living for. Welcome to Crescent residency. Our tastefully designed 1 & 2 BHK homes, will introduce you to a unique lifestyle never experienced before that we like to call, the good life. Turn these pages to journey through a life that’s been waiting for you all along. Defining a good life The beautiful juxtaposition between comfort and affordability is what good living is all about. We at Crescent Residency have attained a harmony between the two, offering you a life that comes close to perfection. Beginning with the easy connectivity which gives you the luxury of being accessible to and from all major areas, making travel in the maximum city, a dream. -

Before the State Information Commission, Maharashtra-Appeal Under Section 19(3) of RTI Act, 2005

Before the State Information Commission, Maharashtra-Appeal under Section 19(3) of RTI Act, 2005. Appeal No.2009/2028/02 Shri. Leslie Almeida Casa Almeida “Flat 103, 1, St. Joseph Road, Off ST Paul Road, Bandra (W), Mumbai – 400 050. … Appellant V/s First Appellate Officer, Divisional Dist. Registrar Cooperatives, Grihanirman Bhavan (MHADA Bldg), Ground Floor, Room No.69, Bandra (E), Mumbai – 400 051. … Respondent Public Information Officer, Dy. Registrar Cooperative Societies, H/W Ward Sahakar Bazar Bldg, 4th Floor, Bandra (W), Mumbai – 400 050. GROUNDS This appeal has been filed under section 19(3) of the Right to Information Act 2005. The appellant had sought the information regarding case file Leslie Almeida V/s Salselle Catholic Cooperative Society. He also wanted a copy of the circular to Salsette Society by Dy Registrar in 2002; if the circular has been revoked a copy of the same, no of societies in society formed within Salsette Society with registration no after 17.01.2002 up to date. Not satisfied with responses from the Public Information Officer and the First Appellate Authority, the appellant has come in second appeal before the commission. The appeal was heard on 05.03.2009. Appellants and respondent were present. The appellant has stated that the PIO must furnish the information. The respondent contended that they do not have the circular to Selsette Society and therefore cannot furnish a copy of it. After considerable discussion it was agreed that the appellant should inspect the relevant file and copies of the document selected by him should be furnished within 30 days.