Embracing China's Economic Shift Through the Total China Concept

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hong Kong's Role in China's Financial Reform

The LEXIS PRACTICE ADVISOR Journal TM WINTER 2015 / 2016 www.lexispracticeadvisor.com Start your free trial today 300+ 11 900+ LEXISNEXIS.COM/FINISH-BIG OR CALL 800.628.3612 ATTORNEY PRACTICE SEARCHABLE AUTHORS AREAS DEAL POINTS Contents WINTER 2015 / 2016 PRACTICE NEWS PRACTICE PROJECTIONS 4 A BRIEFING ON EMERGING ISSUES 35 DUE DILIGENCE IN LIFE SCIENCES IMPACTING TRANSACTIONAL PRACTICE MERGERS & ACQUISITIONS Business & Commercial, Banking & Finance, Labor & Mergers & Acquisitions Employment, Securities & Capital Markets, Real Estate 46 “REGULATION A-PLUS” LIMITED PUBLIC PRACTICE NOTES OFFERINGS UNDER SECURITIES ACT 10 UNDERSTANDING THE NLRB’S SECTION 3(B)(2) POSITIONS ON REGULATING Securities & Capital Markets EMPLOYEES’ SOCIAL MEDIA USAGE Labor & Employment 52 FDA RELEASES FIRST TWO RULES UNDER THE FOOD SAFETY MODERNIZATION ACT 18 CONFIDENTIALITY, NONDISCLOSURE Business & Commercial & SECRECY AGREEMENTS IP & Technology PRACTICE POINTERS 56 DRAFTING AND NEGOTIATING EFFECTIVE PRACTICE TRENDS CLOUD COMPUTING AGREEMENTS 24 CHALLENGES OF TAXING IP & Technology THE SHARING ECONOMY Tax 66 DRAFTING ADVICE: DEVELOPING SOCIAL MEDIA POLICIES 28 CARSHARING GETS EASY Labor & Employment REGULATORY RIDE Business & Commercial JURISDICTIONAL PRACTICE 69 MANAGERS, AGENTS & ATTORNEYS PRACTICE PROFILE California Business & Commercial 31 A VIEW OF ASSET-BASED LENDING GLOBAL PRACTICE WITH DAVID W. MORSE, BANKING & FINANCE CHAIR, OTTERBOURG PC 75 HONG KONG’S ROLE IN CHINA’S FINANCIAL Banking & Finance REFORM - THE ERA OF THE “NEW NORMAL” Banking & Finance -

Tapping Into a Broader Range of Investment Opportunities As China Market Opens Up

Avenir - main text Gotham Sub text CMYK For professional / institutional investors only Tapping into a broader range of investment opportunities as China market opens up RISK FACTORS This is a financial promotion for The FSSA China Strategy. This information is for professional clients only in the UK and EEA and elsewhere where lawful. Investing involves certain risks including: • The value of investments and any income from them may go down as well as up and are not guaranteed. Investors may get back significantly less than the original amount invested. • Currency risk: the Fund invests in assets which are denominated in other currencies; changes in exchange rates will affect the value of the Fund and could create losses. Currency control decisions made by governments could affect the value of the Fund’s investments and could cause the Fund to defer or suspend redemptions of its shares. • Single country / specific region risk: investing in a single country or specific region may be riskier than investing in a number of different countries or regions. Investing in a larger number of countries or regions helps spread risk. • China market Risk: although China has seen rapid economic and structural development, investing there may still involve increased risks of political and governmental intervention, potentially limitations on the allocation of the Fund’s capital, and legal, regulatory, economic and other risks including greater liquidity risk, restrictions on investment or transfer of assets, failed/delayed settlement and difficulties valuing securities. • Concentration risk: the Fund invests in a relatively small number of companies which may be riskier than a fund that invests in a large number of companies. -

This Circular Is Important and Requires Your Immediate Attention

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Fuyao Glass Industry Group Co., Ltd., you should at once hand this circular, together with the accompanying proxy form and the reply slip, to the purchaser(s) or transferee(s) or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser(s) or transferee(s). Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. This circular is for information purpose only and does not constitute an invitation or offer to acquire, purchase or subscribe for any securities of the Company. (A joint stock limited company incorporated in the People’s Republic of China with limited liability) (Stock Code: 3606) PROPOSED ISSUANCE OF ADDITIONAL H SHARES UNDER SPECIFIC MANDATE AND PROPOSED AMENDMENTS TO THE ARTICLES OF ASSOCIATION AND CERTAIN CORPORATE GOVERNANCE POLICIES Placing Agent The 2021 second extraordinary general meeting (the “EGM”) of Fuyao Glass Industry Group Co., Ltd. will be held in the conference room of the Company located at Fuyao Industrial Zone, Rongqiao Economic & Technological Development Zone, Fuqing City, Fujian Province, the PRC at 2:00 p.m. -

ANNUAL REPORT 2016/17 5-Year Financial Summary

HOPEWELL HOLDINGS LIMITED Stock Code: 54 ANNUAL 2016/17 REPORT 64th Floor, Hopewell Centre 183 Queen’s Road East A Wan Chai, Hong Kong N N Tel: (852) 2528 4975 U A Fax: (852) 2861 2068 L REPORT www.hopewellholdings.com 2 0 1 6 / 1 7 Hopewell Holdings Limited, a Hong Kong-based group listed on the Stock Exchange since 1972 (stock code: 54). The Group has continuously grown and become one of the leading business conglomerates in Hong Kong. The Group is actively engaged in property development and investment, highway infrastructure, power, hotel & hospitality and other businesses. While achieving substantial long term growth, the Group recognises the vital importance of promoting sustainable development. It devotes significant resources to enhance corporate governance, promote environmental protection, make community investment, instill best workplace practices and engage stakeholders. CONTENTS 2 Financial Highlights 3 5-Year Financial Summary 4 Chairman’s Statement 10 Awards & Recognition 12 Profile of Directors 21 Management Discussion and Analysis 21 Business Review 59 Financial Review 68 Others 69 Highlights of Sustainability Report 71 Corporate Governance Report 89 Report of the Directors 101 Independent Auditor’s Report 107 Consolidated Statement of Profit or Loss and Other Comprehensive Income 108 Consolidated Statement of Financial Position 110 Consolidated Statement of Changes in Equity 111 Consolidated Statement of Cash Flows 113 Notes to the Consolidated Financial Statements 113 Company’s Statement of Financial Position 114 Notes -

Special Award Title Sponsors

Special Award Title Sponsors Chow Tai Fook Jewellery Group Limited (Excellence in Use of Data) Citibank (Hong Kong) Limited (Excellence in Innovation) Manulife (International) Limited (Excellence in Social Media Marketing) McDonald’s Hong Kong (Excellence in Branding) Tai Hing Group Holdings Ltd. (Excellence in Marketing Collaboration) China Tonghai International Financial Ltd (Excellence in Customer Insights) Corporate Sponsors American Express International, Inc. AXA Hong Kong and Macau CLP Power Hong Kong Limited Eu Yan Sang (HK) Limited Fantastic Natural Fuji Photo Products Cosmetics Limited Company Limited The Hong Kong and Hong Kong Economic Times China Gas Company Limited HKT Limited MTR Corporation PrimeCredit Limited SKECHERS Hong Kong Limited The Standard Supporting Organizations The Hong Kong Advertisers Metro Finance Association Sales and Marketing Digital Marketing Community Executives Club CAMPAIGN AWARDS SPECIAL AWARD TITLE SPONSORS CHOW TAI FOOK EXCELLENCE IN USE OF DATA About Chow Tai Fook Jewellery Group Chow Tai Fook Jewellery Group Limited was listed on the Main Board of The Stock Exchange of Hong Kong in December 2011. The Group’s vision is to become the most trusted jewellery group in the world. Founded in 1929, the Group’s iconic brand “CHOW TAI FOOK” is widely recognised for its trustworthiness and authenticity, and is renowned for its product design, quality and value. The Group’s differentiation strategy continues to make inroads into diverse customer segments by catering to a bespoke experience for different lifestyles and personalities, as well as customers’ different life stages. Offering a wide variety of products, services and channels, the Group’s brand portfolio comprises the CHOW TAI FOOK flagship brand with curated retail experiences, and other individual brands including HEARTS ON FIRE, ENZO, SOINLOVE and MONOLOGUEs. -

Bilibili Announces Strategic Equity Investment in China Telecom

Bilibili Announces Strategic Equity Investment in China Telecom August 11, 2021 SHANGHAI, China, Aug. 11, 2021 (GLOBE NEWSWIRE) -- Bilibili Inc. (the “Company” or “Bilibili”) (Nasdaq: BILI and HKEX: 9626), an iconic brand and a leading video community for young generations in China, today announced that its PRC subsidiary Shanghai Bilibili Technology Co., Ltd. (“Shanghai Bilibili”) has entered into a strategic investor allotment agreement (the “Allotment Agreement”) with China Telecom Corporation Limited (or “China Telecom”) (HKEX: 0728) and a sponsor (the “Sponsor”) for China Telecom’s proposed offering of A shares in conjunction with its listing on the Shanghai Stock Exchange. China Telecom is an integrated intelligent information service provider in the PRC with full-service capabilities. Pursuant to the Allotment Agreement, Shanghai Bilibili is investing an aggregate amount of approximately RMB500 million in China Telecom’s newly issued A shares. Based on an offering price of RMB4.53 per A share, Shanghai Bilibili has been allocated 110,375,000 of the newly issued A shares. Shanghai Bilibili will be subject to 36 months of lock-up obligations over the A shares allocated to it. In addition, Shanghai Kuanyu Digital Technology Co., Ltd., an affiliate of Bilibili, enters into a strategic collaboration agreement with China Telecom, to pursue collaboration opportunities in areas including user growth, brand promotion, IDC and cloud services. Mr. Rui Chen, Chairman of the Board and Chief Executive Officer of Bilibili, said, “We are excited to have this opportunity to join hands with China Telecom at this pivotal moment, as state-run enterprises returning to their home capital market and leading China’s industrial digitization in building the nation’s 5G infrastructure and more. -

The Diminishing Power and Democracy of Hong Kong: an Analysis of Hong Kong's Umbrella Movement and the Anti-Extradition Law Amendment Bill Movement

Portland State University PDXScholar University Honors Theses University Honors College Summer 2021 The Diminishing Power and Democracy of Hong Kong: An Analysis of Hong Kong's Umbrella Movement and the Anti-Extradition Law Amendment Bill Movement Xiao Lin Kuang Portland State University Follow this and additional works at: https://pdxscholar.library.pdx.edu/honorstheses Part of the Asian Studies Commons, and the Other International and Area Studies Commons Let us know how access to this document benefits ou.y Recommended Citation Kuang, Xiao Lin, "The Diminishing Power and Democracy of Hong Kong: An Analysis of Hong Kong's Umbrella Movement and the Anti-Extradition Law Amendment Bill Movement" (2021). University Honors Theses. Paper 1126. https://doi.org/10.15760/honors.1157 This Thesis is brought to you for free and open access. It has been accepted for inclusion in University Honors Theses by an authorized administrator of PDXScholar. Please contact us if we can make this document more accessible: [email protected]. The diminishing power and democracy of Hong Kong: an analysis of Hong Kong’s Umbrella Movement and the Anti-extradition Law Amendment Bill Movement by Xiao Lin Kuang An undergraduate honors thesis submitted in partial fulfillment of the Requirements for the degree of Bachelor of Arts In University Honors And International Development Studies And Chinese Thesis Adviser Maureen Hickey Portland State University 2021 The diminishing power and democracy of Hong Kong Kuang 1 Abstract The future of Hong Kong – one of the most valuable economic port cities in the world – has been a key political issue since the Opium Wars (1839—1860). -

10. HONG KONG's STRATEGIC IMPORTANCE UNDER CHINESE SOVEREIGNTY Tai Ming Cheung Hong Kong Has Come a Long Way Since It Was

- 170 - 10. HONG KONG’S STRATEGIC IMPORTANCE UNDER CHINESE SOVEREIGNTY Tai Ming Cheung Hong Kong has come a long way since it was dismissed as a barren rock a century and a half ago. This bastion of freewheeling capitalism today is a leading international financial, trading and communications center serving one of the world’s fastest growing economic regions. But Hong Kong is also entering a period of considerable change and uncertainty following its reversion to Chinese sovereignty that is likely to have a far- reaching impact on its strategic importance and role over the coming years. As a British colony, Hong Kong was an important outpost for the West to keep an eye on China and safeguard busy sea-lanes. Under Chinese rule, the Hong Kong Special Administrative Region (SAR) will play a crucial role in boosting China’s economic growth and promoting Beijing’s long-term goal of reunification with Taiwan. How China handles Hong Kong’s return will have major consequences for the territory as well as for China’s relations with the international community. The world will be watching very carefully whether Beijing will adhere to its international commitments of allowing the SAR to retain a high degree of autonomy. The U.S. has said that the transition will be a key issue in determining its future relations with China. This paper will examine the strategic implications of Hong Kong's return to Chinese rule. Several key issues will be explored: • Hong Kong's past and present strategic significance. • The stationing of the People's Liberation Army (PLA) in Hong Kong. -

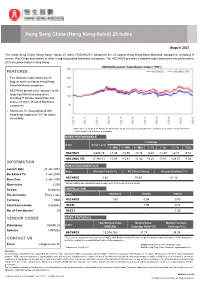

Hang Seng China (Hong Kong-Listed) 25 Index

Hang Seng China (Hong Kong-listed) 25 Index August 2021 The Hang Seng China (Hong Kong- listed) 25 Index ("HSCHK25") comprises the 25 largest Hong Kong-listed Mainland companies, including H shares, Red Chips and shares of other Hong Kong-listed Mainland companies. The HSCHK25 provides a tradable index that tracks the performance of China plays listed in Hong Kong. FEATURES ■ This thematic index tracks the 25 biggest and most liquid Hong Kong- listed Mainland companies ■ HSCHK25 provides an exposure to the large-cap Mainland companies, including H Shares, Red Chips and shares of other HK-listed Mainland companies ■ Stocks are freefloat-adjusted with weightings capped at 10% for higher investibility Data has been rebased at 100.00. All information for an index prior to its launch date is back-tested, back-tested performance reflects hypothetical historical performance. INDEX PERFORMANCE % Change Index Index Level 1 - Mth 3 - Mth 6 - Mth 1 - Yr 3 - Yr 5 - Yr YTD HSCHK25 8,630.19 +1.49 -13.50 -14.18 -0.67 -11.29 +6.71 -9.51 HSCHK25 TRI 17,191.11 +1.80 -11.81 -11.82 +2.47 -0.70 +28.57 -7.02 INFORMATION INDEX FUNDAMENTALS Launch Date 20 Jan 2003 Index Dividend Yield (%) PE Ratio (Times) Annual Volatility*(%) Backdated To 3 Jan 2000 HSCHK25 3.32 10.02 21.12 Base Date 3 Jan 2000 Base Index 2,000 *Annual Volatility was calculated based on daily return for the past 12-month period. Review Quarterly CORRELATION Dissemination Every 2 sec Index HSCHK25 HSCEI HSCCI Currency HKD HSCHK25 1.00 0.98 0.73 Total Return Index Available HSCEI - 1.00 0.73 No. -

Chinese Equities – the Guide March 2021

Chinese equities – the guide March 2021 For professional investors only. In Switzerland for Qualified Investors. In Australia for wholesale clients only. Not for use by retail investors or advisers. Introduction Investors who venture into the Chinese stock universe face an alphabet soup of seemingly random letters. There are A-shares, H-shares and S-chips to name just a few (see Chart 1). These letters represent various attempts to develop the equity market in a country where people traded the first shares as long ago as the 1860s. But something resembling a modern stock market, the Shenzhen Stock Exchange, didn’t start operations until 1 December 1990.1 Shenzhen beat Shanghai as the first exchange of the modern era by some three weeks.2 The Hong Kong Stock Exchange, a forerunner to the city’s current bourse, began operations in 1914 but developed under British colonial rule.3 Investors view Hong Kong as a separate and distinct market. Chart 1: Alphabet soup of Chinese equities Shares Listing Currency Country of Country Examples Index inclusion Comments Can Chinese incorporation where investors buy? company does most business A-share Shanghai + Renminbi China China Shanghai CSI 300 or MSCI Some have dual Y Shenzhen International China A Onshore. listing in H-share Airport Co. MSCI EM since market June 2018 B-share Shanghai + US dollar + China China N/A None Interest has Y Shenzhen Hong Kong collapsed since dollar H-shares H-share Hong Kong Hong Kong China China PetroChina, China MSCI China All Often dual listing Y dollar Construction -

Made in China, Financed in Hong Kong

China Perspectives 2007/2 | 2007 Hong Kong. Ten Years Later Made in China, financed in Hong Kong Anne-Laure Delatte et Maud Savary-Mornet Édition électronique URL : http://journals.openedition.org/chinaperspectives/1703 DOI : 10.4000/chinaperspectives.1703 ISSN : 1996-4617 Éditeur Centre d'étude français sur la Chine contemporaine Édition imprimée Date de publication : 15 avril 2007 ISSN : 2070-3449 Référence électronique Anne-Laure Delatte et Maud Savary-Mornet, « Made in China, financed in Hong Kong », China Perspectives [En ligne], 2007/2 | 2007, mis en ligne le 08 avril 2008, consulté le 28 octobre 2019. URL : http://journals.openedition.org/chinaperspectives/1703 ; DOI : 10.4000/chinaperspectives.1703 © All rights reserved Special feature s e v Made In China, Financed i a t c n i e In Hong Kong h p s c r e ANNE-LAURE DELATTE p AND MAUD SAVARY-MORNET Later, I saw the outside world, and I began to wonder how economic zones and then progressively the Pearl River it could be that the English, who were foreigners, were Delta area. In 1990, total Hong Kong investments repre - able to achieve what they had achieved over 70 or 80 sented 80% of all foreign investment in the Chinese years with the sterile rock of Hong Kong, while China had province. The Hong Kong economy experienced an accel - produced nothing to equal it in 4,000 years… We must erated transformation—instead of an Asian dragon specialis - draw inspiration from the English and transpose their ex - ing in electronics, it became a service economy (90% of ample of good government into every region of China. -

Global Offering E

(a joint stock limited company incorporated in the People’s Republic of China with limited liability) Stock code : 2120 RESPECTING LIFE HUMBLE SERVICE GLOBAL OFFERING Joint Sponsors (in alphabetical order) Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers IMPORTANT IMPORTANT: If you are in any doubt about any of the contents of this Prospectus, you should obtain independent professional advice. Wenzhou Kangning Hospital Co., Ltd. 溫州康寧醫院股份有限公司 (a joint stock limited company incorporated in the People’s Republic of China with limited liability) GLOBAL OFFERING Number of Offer Shares under the Global Offering : 17,600,000 H Shares (subject to adjustment and the Over-allotment Option) Number of Hong Kong Offer Shares : 1,760,000 H Shares (subject to adjustment) Number of International Offer Shares : 15,840,000 H Shares (subject to adjustment and the Over-allotment Option) Maximum Offer Price : HK$38.7 per H Share, plus brokerage of 1%, SFC transaction levy of 0.0027%, and Stock Exchange trading fee of 0.005% (payable in full on application in Hong Kong dollars and subject to refund on final pricing) Nominal value : RMB1.00 per H Share Stock code : 2120 Joint Sponsors (in alphabetical order) Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this Prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this Prospectus.