Listing PRC Companies in Hong Kong Using VIE Structures

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Integration of International Financial Regulatory Standards for the Chinese Economic Area: the Challenge for China, Hong Kong, and Taiwan Lawrence L.C

Northwestern Journal of International Law & Business Volume 20 Issue 1 Fall Fall 1999 Integration of International Financial Regulatory Standards for the Chinese Economic Area: The Challenge for China, Hong Kong, and Taiwan Lawrence L.C. Lee Follow this and additional works at: http://scholarlycommons.law.northwestern.edu/njilb Part of the International Law Commons, International Trade Commons, Law and Economics Commons, and the Securities Law Commons Recommended Citation Lawrence L.C. Lee, Integration of International Financial Regulatory Standards for the Chinese Economic Area: The hC allenge for China, Hong Kong, and Taiwan, 20 Nw. J. Int'l L. & Bus. 1 (1999-2000) This Article is brought to you for free and open access by Northwestern University School of Law Scholarly Commons. It has been accepted for inclusion in Northwestern Journal of International Law & Business by an authorized administrator of Northwestern University School of Law Scholarly Commons. ARTICLES Integration of International Financial Regulatory Standards for the Chinese Economic Area: The Challenge for China, Hong Kong, and Taiwan Lawrence L. C. Lee* I. INTRODUCTION ................................................................................... 2 II. ORIGINS OF THE CURRENT FINANCIAL AND BANKING SYSTEMS IN THE CHINESE ECONOMIC AREA ............................................................ 11 * Lawrence L. C. Lee is Assistant Professor at Ming Chung University School of Law (Taiwan) and Research Fellow at Columbia University School of Law. S.J.D. 1998, Univer- sity of Wisconsin-Madison Law School; LL.M. 1996, American University Washington College of Law; LL.M. 1993, Boston University School of Law; and LL.B. 1991, Soochow University School of Law (Taiwan). Portions of this article were presented at the 1999 Con- ference of American Association of Chinese Studies and the 1997 University of Wisconsin Law School Symposium in Legal Regulation of Cross-Straits Commercial Activities among Taiwan, Hong Kong, and China. -

This Circular Is Important and Requires Your Immediate Attention

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Fuyao Glass Industry Group Co., Ltd., you should at once hand this circular, together with the accompanying proxy form and the reply slip, to the purchaser(s) or transferee(s) or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser(s) or transferee(s). Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. This circular is for information purpose only and does not constitute an invitation or offer to acquire, purchase or subscribe for any securities of the Company. (A joint stock limited company incorporated in the People’s Republic of China with limited liability) (Stock Code: 3606) PROPOSED ISSUANCE OF ADDITIONAL H SHARES UNDER SPECIFIC MANDATE AND PROPOSED AMENDMENTS TO THE ARTICLES OF ASSOCIATION AND CERTAIN CORPORATE GOVERNANCE POLICIES Placing Agent The 2021 second extraordinary general meeting (the “EGM”) of Fuyao Glass Industry Group Co., Ltd. will be held in the conference room of the Company located at Fuyao Industrial Zone, Rongqiao Economic & Technological Development Zone, Fuqing City, Fujian Province, the PRC at 2:00 p.m. -

Hang Seng Mainland China Companies High Dividend Yield Index

Hang Seng Mainland China Companies High Dividend Yield Index August 2021 The Hang Seng Mainland China Companies High Dividend Yield Index ("HSMCHYI") reflects the overall performance of Hong Kong listed Mainland companies with high dividend yield. FEATURES ■ The index comprises the 50 highest dividend yielding stocks among sizable Mainland companies that have demonstrated relatively lower price volatility and a persistent dividend payment record for the latest three fiscal years. ■ The index is net dividend yield- weighted with 10% cap on individual constituents. Data has been rebased at 100.00. All information for an index prior to its launch date is back-tested, back-tested performance INFORMATION reflects hypothetical historical performance. Launch Date 9 Sep 2019 INDEX PERFORMANCE Backdated To 31 Dec 2014 % Change Index Index Level Base Date 31 Dec 2014 1 - Mth 3 - Mth 6 - Mth 1 - Yr 3 - Yr 5 - Yr YTD Base Index 3,000 HSMCHYI 3,191.64 +7.42 -11.33 -7.46 +5.16 -7.37 +21.68 +2.40 Review Half-yearly HSMCHYI TRI 4,541.18 +7.76 -7.28 -2.51 +12.13 +10.20 +57.98 +7.87 Dissemination Every 2 sec INDEX FUNDAMENTALS Currency HKD Index Dividend Yield (%) PE Ratio (Times) Annual Volatility*(%) Total Return Index Available HSMCHYI 7.01 5.91 17.47 No. of Constituents 49 *Annual Volatility was calculated based on daily return for the past 12-month period. HSIDVP 602.10 VENDOR CODES All data as at 31 Aug 2021 Bloomberg HSMCHYI Refinitiv .HSMCHYI CONTACT US Email [email protected] Disclaimer All information contained herein is provided for reference only. -

Initial Public Offering (Ipo) and Listing Process on the Sehk with Highlights

September 2019 RESEARCH REPORT INITIAL PUBLIC OFFERING (IPO) AND LISTING PROCESS ON THE SEHK WITH HIGHLIGHTS CONTENTS Page Summary ........................................................................................................................................ 1 1. General requirements for listing in Hong Kong ......................................................................... 2 1.1 Main Board listing conditions ........................................................................................... 2 1.2 Shareholding structures for listing in Hong Kong ............................................................. 3 Jurisdictions acceptable as place of incorporation ............................................... 3 Shareholding structures of Mainland companies seeking to list in Hong Kong ..... 3 Red-chip structure ............................................................................................... 4 Variable Interest Entity (VIE) structure ................................................................. 5 H-share structure ................................................................................................. 6 1.3 Listing of H-shares: An update ........................................................................................ 9 H-share companies have become an important part of the Hong Kong stock market ................................................................................................................. 9 Successful implementation of the H-share full circulation pilot programme -

俊盟國際控股有限公司 (Incorporated in the Cayman Islands with Limited Liability) Stock Code: 8062

EFT Solutions Holdings Limited 俊盟國際控股有限公司 (Incorporated in the Cayman Islands with limited liability) Stock Code: 8062 PUBLIC OFFER AND PLACING Sole Sponsor Sole Bookrunner and Sole Lead Manager IMPORTANT If you are in any doubt about any of the contents of this prospectus, you should obtain independent professional advice. EFT Solutions Holdings Limited 俊盟國際控股有限公司 (Incorporated in the Cayman Islands with limited liability) LISTING ON THE GROWTH ENTERPRISE MARKET OF THE STOCK EXCHANGE OF HONG KONG LIMITED BY WAY OF PUBLIC OFFER AND PLACING Number of Offer Shares : 120,000,000 Shares, comprising 96,000,000 New Shares and 24,000,000 Sale Shares Number of Placing Shares : 108,000,000 Shares, comprising 84,000,000 New Shares and 24,000,000 Sale Shares (subject to re-allocation) Number of Public Offer Shares : 12,000,000 New Shares (subject to re-allocation) Offer Price : Not more than HK$0.60 and expected to be not less than HK$0.40 per Offer Share, plus brokerage of 1%, SFC transaction levy of 0.0027% and Stock Exchange trading fee of 0.005% (payable in full on application in Hong Kong dollars and subject to refund) Nominal value : HK$0.01 per Share Stock code : 8062 Sole Sponsor Sole Bookrunner and Sole Lead Manager Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this prospectus. -

List of CMU Members 2021-08-18

List of CMU Members 2021-09-23 Member Bond Code Member Name Bank Repo CMUBID Connect ABCI ABCI SECURITIES COMPANY LIMITED - Y Y ABNA ABN AMRO BANK N.V. - Y - ABOC AGRICULTURAL BANK OF CHINA LIMITED - Y Y AIAT AIA COMPANY (TRUSTEE) LIMITED - - - ASBK AIRSTAR BANK LIMITED - Y - ACRL ALLIED BANKING CORPORATION (HONG KONG) LIMITED - Y - ANTB ANT BANK (HONG KONG) LIMITED - - - ANZH AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED - - Y AMCM AUTORIDADE MONETARIA DE MACAU - Y - BEXH BANCO BILBAO VIZCAYA ARGENTARIA, S.A. - Y - BSHK BANCO SANTANDER S.A. - Y Y BBLH BANGKOK BANK PUBLIC COMPANY LIMITED - - - BCTC BANK CONSORTIUM TRUST COMPANY LIMITED - - - SARA BANK J. SAFRA SARASIN LTD - Y - JBHK BANK JULIUS BAER AND CO. LTD. - Y - BAHK BANK OF AMERICA, NATIONAL ASSOCIATION - Y Y BCHK BANK OF CHINA (HONG KONG) LIMITED - Y Y CDFC BANK OF CHINA INTERNATIONAL LIMITED - Y - BCHB BANK OF CHINA LIMITED, HONG KONG BRANCH - Y - CHLU BANK OF CHINA LIMITED, LUXEMBOURG BRANCH - - Y BMHK BANK OF COMMUNICATIONS (HONG KONG) LIMITED - Y - BCMK BANK OF COMMUNICATIONS CO., LTD. - Y - BCTL BANK OF COMMUNICATIONS TRUSTEE LIMITED - - Y DGCB BANK OF DONGGUAN CO., LTD. - - - BEAT BANK OF EAST ASIA (TRUSTEES) LIMITED - - - BEAH BANK OF EAST ASIA, LIMITED (THE) - Y Y BOIH BANK OF INDIA - - - BOFM BANK OF MONTREAL - - - BNYH BANK OF NEW YORK MELLON - - - BNSH BANK OF NOVA SCOTIA (THE) - - - BOSH BANK OF SHANGHAI (HONG KONG) LIMITED - Y Y BTWH BANK OF TAIWAN - Y - SINO BANK SINOPAC, HONG KONG BRANCH - - Y BPSA BANQUE PICTET AND CIE SA - - - BBID BARCLAYS BANK PLC - Y - EQUI BDO UNIBANK, INC. -

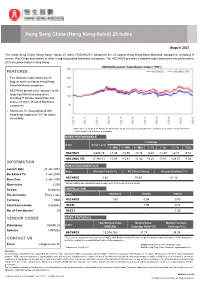

Hang Seng China (Hong Kong-Listed) 25 Index

Hang Seng China (Hong Kong-listed) 25 Index August 2021 The Hang Seng China (Hong Kong- listed) 25 Index ("HSCHK25") comprises the 25 largest Hong Kong-listed Mainland companies, including H shares, Red Chips and shares of other Hong Kong-listed Mainland companies. The HSCHK25 provides a tradable index that tracks the performance of China plays listed in Hong Kong. FEATURES ■ This thematic index tracks the 25 biggest and most liquid Hong Kong- listed Mainland companies ■ HSCHK25 provides an exposure to the large-cap Mainland companies, including H Shares, Red Chips and shares of other HK-listed Mainland companies ■ Stocks are freefloat-adjusted with weightings capped at 10% for higher investibility Data has been rebased at 100.00. All information for an index prior to its launch date is back-tested, back-tested performance reflects hypothetical historical performance. INDEX PERFORMANCE % Change Index Index Level 1 - Mth 3 - Mth 6 - Mth 1 - Yr 3 - Yr 5 - Yr YTD HSCHK25 8,630.19 +1.49 -13.50 -14.18 -0.67 -11.29 +6.71 -9.51 HSCHK25 TRI 17,191.11 +1.80 -11.81 -11.82 +2.47 -0.70 +28.57 -7.02 INFORMATION INDEX FUNDAMENTALS Launch Date 20 Jan 2003 Index Dividend Yield (%) PE Ratio (Times) Annual Volatility*(%) Backdated To 3 Jan 2000 HSCHK25 3.32 10.02 21.12 Base Date 3 Jan 2000 Base Index 2,000 *Annual Volatility was calculated based on daily return for the past 12-month period. Review Quarterly CORRELATION Dissemination Every 2 sec Index HSCHK25 HSCEI HSCCI Currency HKD HSCHK25 1.00 0.98 0.73 Total Return Index Available HSCEI - 1.00 0.73 No. -

FTSE Asia Pacific Ex Japan Australia and NZ Net 20 May 2014

FTSE PUBLICATIONS FTSE Asia Pacific ex Japan Australia 20 May 2014 and NZ Net Indicative Index Weight Data as at Closing on 31 March 2014 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) AAC Technologies Holdings 0.12 HONG Beijing Capital International Airport (H) 0.03 CHINA China Development Financial Holdings 0.13 TAIWAN KONG Beijing Enterprises Holdings (Red Chip) 0.15 CHINA China Dongxiang Group (P Chip) 0.02 CHINA ABB India 0.02 INDIA Beijing Enterprises Water Group (Red Chip) 0.09 CHINA China Eastern Airlines (H) 0.02 CHINA Aboitiz Equity Ventures 0.09 PHILIPPINES Beijing Jingneng Clean Energy (H) 0.02 CHINA China Everbright (RED CHIP) 0.04 CHINA Aboitiz Power 0.04 PHILIPPINES Beijing North Star (H) 0.01 CHINA China Everbright International (Red Chip) 0.12 CHINA ACC 0.03 INDIA Belle International (P Chip) 0.17 CHINA China Foods (Red Chip) 0.01 CHINA Acer 0.05 TAIWAN Bengang Steel Plates (B) <0.005 CHINA China Galaxy Securities (H) 0.02 CHINA Adani Enterprises 0.05 INDIA Berjaya Sports Toto 0.03 MALAYSIA China Gas Holdings (P Chip) 0.08 CHINA Adani Ports and Special Economic Zone 0.05 INDIA Berli Jucker 0.02 THAILAND China Hongqiao Group (P Chip) 0.02 CHINA Adani Power 0.01 INDIA Bharat Electronics 0.01 INDIA China Huishan Dairy Holdings (P Chip) 0.03 CHINA Adaro Energy PT 0.04 INDONESIA Bharat Forge-A 0.02 INDIA China International Marine Containers (H) 0.04 CHINA Aditya Birla Nuvo 0.02 INDIA Bharat Heavy Elect .LS 0.06 INDIA China Life Insurance (H) 0.67 CHINA Advanced Info Serv 0.27 THAILAND Bharat Petroleum Corp 0.04 INDIA China Longyuan Power Group (H) 0.11 CHINA Advanced Semiconductor Engineering 0.22 TAIWAN Bharti Airtel 0.22 INDIA China Machinery Engineering (H) 0.01 CHINA Advantech 0.06 TAIWAN Bharti Infratel 0.02 INDIA China Mengniu Dairy 0.22 HONG Agile Property Holdings (P Chip) 0.03 CHINA Big C Supercenter 0.04 THAILAND KONG Agricultural Bank of China (H) 0.32 CHINA Biostime International Holdings (P Chip) 0.03 CHINA China Merchant Holdings (Red Chip) 0.13 CHINA AIA Group Ltd. -

Chinese Equities – the Guide March 2021

Chinese equities – the guide March 2021 For professional investors only. In Switzerland for Qualified Investors. In Australia for wholesale clients only. Not for use by retail investors or advisers. Introduction Investors who venture into the Chinese stock universe face an alphabet soup of seemingly random letters. There are A-shares, H-shares and S-chips to name just a few (see Chart 1). These letters represent various attempts to develop the equity market in a country where people traded the first shares as long ago as the 1860s. But something resembling a modern stock market, the Shenzhen Stock Exchange, didn’t start operations until 1 December 1990.1 Shenzhen beat Shanghai as the first exchange of the modern era by some three weeks.2 The Hong Kong Stock Exchange, a forerunner to the city’s current bourse, began operations in 1914 but developed under British colonial rule.3 Investors view Hong Kong as a separate and distinct market. Chart 1: Alphabet soup of Chinese equities Shares Listing Currency Country of Country Examples Index inclusion Comments Can Chinese incorporation where investors buy? company does most business A-share Shanghai + Renminbi China China Shanghai CSI 300 or MSCI Some have dual Y Shenzhen International China A Onshore. listing in H-share Airport Co. MSCI EM since market June 2018 B-share Shanghai + US dollar + China China N/A None Interest has Y Shenzhen Hong Kong collapsed since dollar H-shares H-share Hong Kong Hong Kong China China PetroChina, China MSCI China All Often dual listing Y dollar Construction -

Made in China, Financed in Hong Kong

China Perspectives 2007/2 | 2007 Hong Kong. Ten Years Later Made in China, financed in Hong Kong Anne-Laure Delatte et Maud Savary-Mornet Édition électronique URL : http://journals.openedition.org/chinaperspectives/1703 DOI : 10.4000/chinaperspectives.1703 ISSN : 1996-4617 Éditeur Centre d'étude français sur la Chine contemporaine Édition imprimée Date de publication : 15 avril 2007 ISSN : 2070-3449 Référence électronique Anne-Laure Delatte et Maud Savary-Mornet, « Made in China, financed in Hong Kong », China Perspectives [En ligne], 2007/2 | 2007, mis en ligne le 08 avril 2008, consulté le 28 octobre 2019. URL : http://journals.openedition.org/chinaperspectives/1703 ; DOI : 10.4000/chinaperspectives.1703 © All rights reserved Special feature s e v Made In China, Financed i a t c n i e In Hong Kong h p s c r e ANNE-LAURE DELATTE p AND MAUD SAVARY-MORNET Later, I saw the outside world, and I began to wonder how economic zones and then progressively the Pearl River it could be that the English, who were foreigners, were Delta area. In 1990, total Hong Kong investments repre - able to achieve what they had achieved over 70 or 80 sented 80% of all foreign investment in the Chinese years with the sterile rock of Hong Kong, while China had province. The Hong Kong economy experienced an accel - produced nothing to equal it in 4,000 years… We must erated transformation—instead of an Asian dragon specialis - draw inspiration from the English and transpose their ex - ing in electronics, it became a service economy (90% of ample of good government into every region of China. -

Bank of Shanghai (Hong Kong) Limited

BANK OF SHANGHAI (HONG KONG) LIMITED DIRECTORS’ REPORT AND CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2020 Bank of Shanghai (Hong Kong) Limited Year ended 31 December 2020 CONTENTS Page(s) Report of the directors 1 Independent auditor’s report 4 Consolidated statement of profit or loss and other comprehensive income 7 Consolidated statement of financial position 8 Consolidated statement of changes in equity 10 Consolidated statement of cash flows 11 Notes to the consolidated financial statements 12 Corporate Governance Report (unaudited) 89 Bank of Shanghai (Hong Kong) Limited Year ended 31 December 2020 Report of the directors The directors submit herewith their annual report together with the audited financial statements for the year ended 31 December 2020. Principal place of business Bank of Shanghai (Hong Kong) Limited (the Company) is a restricted licence bank incorporated and domiciled in Hong Kong and has its registered office and principal place of business at 34th Floor, Champion Tower, 3 Garden Road, Central, Hong Kong. Principal activities The principal activities of the Company are to provide financial services to corporations and individuals. The principal activities and other particulars of the Company’s subsidiaries are stated in Note 19 to the financial statements. Transfer to reserves The profit attributable to shareholders of HK$227,808,000 (2019: HK$308,294,000) has been transferred to reserves. Other movements in reserves are shown in the consolidated statement of changes in equity on page 10. Recommended dividend The directors do not recommend payment of a final dividend for the financial year ended 31 December2020 (2019: Nil). -

Room Document 9 Statistics and Data on the Securities and Futures Markets of Hong Kong by Mr. Mark Dickens Asian Development

Fourth Round Table on Capital Market Reform in Asia 09-10 April 2002, Tokyo Room Document 9 Statistics and Data on the Securities and Futures Markets of Hong Kong By Mr. Mark Dickens ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT Asian Development Bank Institute 1 Statistics/data on the Securities and Futures Markets of Hong Kong Table 1 – Major Indicators of the Securities Markets in Hong Kong (Period-end figures unless otherwise specified) Cash Market 1996 1997 1998 1999 2000 2001 Main Board Number of Listed Companies 583 658 680 701 736 756 Market Capitalisation Total 3,476 3,202 2,662 4,728 4,795 3,885 (HK$ billion) HSI Constituents 2,436 2,132 2,106 3,744 3,866 3,136 Worldwide Ranking by Market Capitalisation 7 9 11 10 10 10 Market Capitalisation to GDP (%) 292 242 211 384 377 306 Market Value of Top 10 Stocks over Total Market Capitalisation (%) 52 n.a. n.a. 66 66 63 Average Daily Turnover Total 5,672 15,465 6,887 7,757 12,338 8,025 (HK$ million) HSI Constituents 3,075 5,534 4,550 3,766 5,677 4,558 Number of Trading Days 249 245 247 247 247 243 Liquidity (%) (Turnover / Year-end Market Capitalisation) 41 118 64 41 64 50 Hang Seng Index 13,451 10,723 10,049 16,962 15,096 11,397 P/E ratio (HSI) 17.30 12.29 12.36 27.88 12.74 15.06 Funds Raised (HK$ billion, annual) 100 248 38 148 451 59 Growth Enterprise Market Number of Listed Companies n.a.