5.2 Relationship Between Benefits and Social Housing (2016)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Under-Occupying Social Housing: Housing Benefit Entitlement

BRIEFING PAPER Number 06272, 1 November 2019 Under-occupying social By Wendy Wilson housing: Housing Benefit entitlement Inside: 1. Why does under-occupation arise? 2. The rationale for Government intervention 3. Defining under-occupation and who is affected 4. The options for tenants 5. What can landlords do? www.parliament.uk/commons-library | intranet.parliament.uk/commons-library | [email protected] | @commonslibrary Number 06272, 1 November 2019 2 Contents Summary 3 1. Why does under-occupation arise? 4 2. The rationale for Government intervention 6 3. Defining under-occupation and who is affected 9 3.1 Continuous entitlement to HB since at least 1 January 1996 9 3.2 How many bedrooms are allowed? 10 3.3 Defining a bedroom 11 Bedroom size 12 Bedrooms used for other purposes 13 3.4 What is working-age? 16 3.5 How much Housing Benefit is lost? 17 3.6 Disabled occupants 18 Overnight care 19 Disabled children sharing a room 21 Disabled adults sleeping in separate rooms 25 Spare rooms and storage of disability related equipment 26 Significantly adapted accommodation 27 3.7 Shared care of children 27 Legal challenges 28 3.8 Sheltered and supported housing 30 3.9 Foster carers and adoptive parents 31 3.10 Temporary absences from home 33 Students 33 Armed forces personnel 34 Legal challenges 35 3.11 Separated couples living together 35 3.12 Bereavement, temporary protection and reporting changes of circumstances 36 4. The options for tenants 37 4.1 Discretionary Housing Payments 37 4.2 Moving to a smaller home 38 4.3 Taking in a lodger 39 4.4 Earning more money 40 5. -

OFFICIAL REPORT (Hansard)

Committee for Social Development OFFICIAL REPORT (Hansard) Welfare Reform Bill: Universal Credit (Clauses 1-44) 10 October 2012 NORTHERN IRELAND ASSEMBLY Committee for Social Development Welfare Reform Bill: Universal Credit (Clauses 1-44) 10 October 2012 Members present for all or part of the proceedings: Mr Alex Maskey (Chairperson) Mr Mickey Brady (Deputy Chairperson) Ms Paula Bradley Ms Pam Brown Mr Gregory Campbell Mrs Judith Cochrane Mr Michael Copeland Mr Sammy Douglas Mr Mark Durkan Mr Fra McCann Witnesses: Ms Martina Campbell Department for Social Development Ms Anne McCleary Department for Social Development Mr Michael Pollock Department for Social Development Ms Margaret Stitt Social Security Agency The Chairperson: I welcome formally officials Anne McCleary, Michael Pollock, Martina Campbell and Margaret Stitt. Thank you very much for being here. You are very welcome. I hope that you get home a wee bit earlier this evening. Obviously, the purpose of today's session is to deal with all matters that relate to universal credit, which is covered by clauses 1 to 44 of the Welfare Reform Bill. During this session, officials will outline that particular part in as much detail as they can. I remind members that the purpose of the session is not to debate the issues, but to have the Bill and that particular set of clauses explained and for members to explore the detail of that. On that basis, members may raise any specific issues with the officials. As per our schedule, which members have agreed, we intend to have a number of these sessions to work our way through the Bill clause by clause. -

134060 Radius Housing

Case Study What action should you take? Bill and Marie live in a 3 bedroom Radius If you have an extra bedroom/s, you should property with their daughter Lucy, aged 7. think about how the Social Sector Size Criteria / ‘Bedroom Tax’ will apply to your They receive Housing Benefit to help pay household. their rent which is £100 per week. This is • You should consider how you will manage paid to Radius Housing on their behalf. to pay any shortfall. • You could also consider moving to a As they currently under occupy by one smaller property. Your Housing Officer can Social Sector Size bedroom their Housing Benefit is reduced assist you to look at alternative housing by 14%. Thus they have a £14 per week options. Criteria (SSSC) shortfall. • If you require the extra room for care needs you should apply to the NIHE Housing Benefits Section and ask for this to be Bedroom Tax Bill and Marie have to pay the shortfall taken into account when assessing your of £14 per week in their rent to their housing costs. landlord. Help and Support If you are concerned about the ‘Bedroom Tax’ and would like further information or advice, please contact our Welfare Advice Service on Tel 0330 123 0888. Alternatively you can get further information on our website www.radiushousing.org or visit www.nidirect.gov.uk/changes-to- housing-benefit @RadiusHousing /RadiusHousing radiushousing © Radius Housing, May 2019 Registered Office: Radius Housing Association, 38 – 52 Lisburn Road, Belfast BT9 6AA Registered in Northern Ireland (No. IP169), VAT Reg. -

General Election - Housing Policy Update 1

GENERAL ELECTION - HOUSING POLICY UPDATE 1 Briefing note April 2015 GENERAL ELECTION - HOUSING POLICY UPDATE Over recent weeks each of the main parties have released their manifestos, including details of their housing policies, and we set out below highlights from them. Our summary is arranged under key topics and the contrast in policy positions is clear. A coalition or minority government may necessitate compromises to many of these policies and it will be interesting to see which of them are eventually implemented. RIGHT TO BUY Conservative Extend Right to Buy ("RTB") to housing association tenants in England. The replacement of properties to be sold under the scheme to be funded by the sale of expensive Council properties as they fall vacant. Labour Have not outrightly opposed the Conservative RTB proposal but have commented that the potential loss of affordable housing could not work unless it was matched by a "massive Government-led house- building programme". UKIP Apply all revenue from RTB sales (after essential costs) into new community housing and prevent non- British nationals accessing RTB or Help to Buy schemes, unless they have served in HM Armed Forces. Liberal Devolve full control of the RTB scheme to Councils. Democrats Do not support the Conservative proposal to extend RTB scheme to housing association tenants. Green Party End RTB discounts SNP The RTB scheme has already been abolished in Scotland and the SNP have criticised the Conservative proposal to extend the RTB scheme to housing association tenants. Plaid Cymru Have criticised the Conservative proposal to extend the RTB scheme to housing association tenants. -

Accommodation Finder Self Help Pack (PDF, 370

Accommodation finder self-help pack Contents Page 1. Introduction 3 2. Finding a suitable home that you can afford 3 a) Bedroom calculator 3 b) LHA rates in Cheshire West and Chester 3 c) Benefits calculator 4 d) Financial statement 4 3. Choosing the right housing option 4 a) Private rented 4 b) Registered providers (housing associations) 5 c) Council housing 6 d) House shares and room renting 7 e) ‘Forfutures’ supported housing 8 f) Other supported housing 8 g) Lodging 8 h) Buying your own home 9 i) Home swap 10 j) Sheltered and extra care housing 10 4) Homelessness 11 Page 2 1. Introduction This self-help pack can be used by anyone trying to find accommodation in the Cheshire West and Chester area. You can increase your chances of finding something suitable by considering the full range of housing options available to you as well as knowing what you can afford. 2. Finding a suitable home that you can afford It is important that the property you choose is both suitable for your households needs and is affordable. a) Bedroom calculator If you claim Housing Benefit (HB), Universal Credit (UC) or Local Housing Allowance (LHA), it is important that you look for a property with the correct number of bedrooms for your household so that you are not impacted by the ‘Spare Room Subsidy’ (more commonly known as ‘Bedroom Tax’). Even if you don’t currently claim HB, UC or LHA it will be a good idea to do this check in case you need to do so in future. -

Factsheet 14: Benefit Cap

Factsheet 14: Benefit Cap What is the benefit cap? From summer 2013 a limit will be put on the total amount of benefits that most people aged 16 to 64 can get. This is called a benefit cap. This aim of the benefit cap is to ensure that workless households do not receive more in benefit payments than the average earnings of a working household. What benefits will get capped? The cap will apply to the total amount that the people in your household get from the following benefits: Bereavement Allowance Carer’s Allowance Child Benefit Child Tax Credit Employment and Support Allowance (unless you get the support component) Guardian’s Allowance Housing Benefit Incapacity Benefit Income Support Jobseeker’s Allowance Maternity Allowance Severe Disablement Allowance Widowed Parent’s Allowance (or Widowed Mother’s Allowance or Widows Pension you started getting before 9 April 2001) Who won’t be affected? You won’t be affected by the benefit cap if you qualify for Working Tax Credit (whether or not you claim it), or if you get any of the following benefits: Disability Living Allowance Personal Independence Payment (from April 2013) Attendance Allowance Industrial Injuries Benefits (and equivalent payments as part of a war disablement pension or the Armed Forces Compensation Scheme) Employment and Support Allowance, if you get the support component War Widow’s or War Widower’s Pension How much is the benefit cap? The level of the cap will be: £500 a week for couples (with or without children living with them) £500 a week for single parents whose children live with them £350 a week for single adults who don’t have children, or whose children don’t live with them 1 How will I be affected? You can use the calculator on the Government’s Directgov website is available which can be used to get an estimate of how your Housing Benefit might be impacted. -

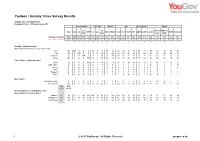

Yougov / Sunday Times Survey Results

YouGov / Sunday Times Survey Results Sample Size: 1903 GB Adults Fieldwork: 12th - 13th September 2013 Voting intention 2010 Vote Gender Age Social grade Region Lib Lib Rest of Midlands Total Con Lab UKIP Con Lab Male Female 18-24 25-39 40-59 60+ ABC1 C2DE London North Scotland Dem Dem South / Wales Weighted Sample 1903 472 538 129 171 556 490 426 923 980 226 481 651 544 1085 818 244 618 407 468 166 Unweighted Sample 1903 441 586 123 194 554 494 451 884 1019 166 462 751 524 1271 632 280 626 389 464 144 % % % % % % % % % % % % % % % % % % % % % Headline Voting Intention [Excluding Don't knows and Wouldn't votes] Con 33 100 0 0 0 76 5 13 35 32 32 30 31 40 35 31 30 39 32 33 22 Lab 38 0 100 0 0 3 87 30 37 40 34 42 40 34 36 40 46 26 40 48 35 Lib Dem 9 0 0 100 0 1 1 33 9 10 15 11 8 7 11 7 7 13 7 6 12 Other 20 0 0 0 100 19 6 23 20 19 19 17 22 19 18 22 16 22 21 12 32 Other Parties Voting Intention UKIP 12 0 0 0 100 18 3 10 13 11 6 7 16 13 10 15 9 17 12 10 5 SNP / PCY 3 0 0 0 0 0 2 3 3 3 1 4 2 3 3 2 0 0 2 0 21 Green 3 0 0 0 0 1 0 7 2 4 5 5 3 1 3 2 5 4 3 1 2 BNP 1 0 0 0 0 0 0 1 1 1 3 1 1 0 1 1 2 0 2 1 1 Respect 0 0 0 0 0 0 0 0 0 0 3 0 0 0 0 0 0 0 0 0 3 Other 1 0 0 0 0 0 1 1 1 1 1 0 0 2 0 1 0 0 2 1 1 Non Voters Would Not Vote 8 0 0 0 0 3 3 4 7 9 17 11 7 3 8 9 8 12 6 7 4 Don't know 17 0 0 0 0 13 10 25 9 25 22 18 13 21 15 21 18 18 19 17 15 Sep Sep 11-12 12-13 Do you approve or disapprove of the Government's record to date? Approve 31 31 81 5 49 16 62 9 23 37 24 26 29 31 33 33 27 33 33 31 27 25 Disapprove 56 54 8 86 38 73 26 80 62 53 54 41 50 57 57 51 56 52 50 53 56 63 Don't know 13 16 11 8 13 12 13 11 15 10 22 33 20 12 10 15 17 15 17 15 17 12 1 © 2013 YouGov plc. -

Citizens Advice Camden, GOSH Information Sheet 4: the Benefit Cap 020 7829 8896

Citizens Advice Camden, GOSH Information Sheet 4: The Benefit Cap 020 7829 8896 Take home message • The Benefit Cap is intended as a maximum amount of benefit that anyone will be able to get • There are exemptions, e.g. for people who get disability benefits or work full-time and claim Working Tax Credit • The Benefit Cap mainly affects large families and families living in London What is the Benefit Cap? • The Benefit Cap is the maximum amount a person should receive in benefits. The cap depends on each claimant’s circumstances. • The Cap works by adding up a person’s total benefit income. Note that not all benefits are counted in this. If the total income is above the Cap, then their Housing Benefit (HB) or Universal Credit (UC) will be reduced to bring their income to the level of the Cap. • It only applies if a person is getting HB or UC. • It mainly affects families in London where rents are high. What are the ways around it? • The Cap does not apply if: • A member of the household is working full-time and has claimed Working Tax Credit (WTC). This applies even if they earn too much to actually get WTC. • If someone has stopped working having worked 50 weeks of the past 52, then the Cap will not be applied for 39 weeks. • If someone in the household gets a disability benefit such as Disability Living Allowance (DLA – see Sheet 1). This applies even if DLA payments stop because the child is an inpatient. • Someone affected can claim discretionary housing payments from their council, though such help is not guaranteed or indefinite. -

Benefits Rates and Income/Savings Thresholds

alzheimers.org.uk Benefits rates and income/ savings thresholds This factsheet provides details of benefits rates and savings thresholds as of April 2016. It is designed to be used in conjunction with various Alzheimer’s Society factsheets about benefits and how to apply for them, especially factsheet 413, ‘Benefits’ (see list in ‘Further reading’ section at the end of this factsheet.) Care and mobility benefits Attendance allowance Higher rate £82.30 weekly Lower rate £55.10 weekly Disability living allowance Personal care component Higher rate £82.30 weekly Middle rate £55.10 weekly Lower rate £21.80 weekly Mobility component Higher rate £57.45 weekly Lower rate £21.80 weekly 1 Personal independence payment Personal independence payment (PIP) has replaced Disability living allowance for all new claims after June 2013. Daily living component Enhanced rate £82.30 weekly Standard rate £55.10 weekly Mobility component Enhanced rate £57.45 weekly Standard rate £21.80 weekly Paying for care NHS-funded nursing care The standard rate in England is £112.00 per week. In Wales, the rate is £140.90 per week. In Northern Ireland, the rate is £100 per week. Payment of home care and care home fees Upper savings threshold in England (above which the person has to pay all their costs) is £23,250. Lower savings threshold in England (below which a person’s savings are no longer taken into account, although all other income including benefits and pensions is still counted) is £14,250. In Wales, the upper savings threshold is £24,000. There is no lower savings threshold. -

Evaluation of Removal of the Spare Room Subsidy

Evaluation of Removal of the Spare Room Subsidy Final Report December 2015 Research Report No 913 A report of research carried out by by the Cambridge Centre for Housing and Planning Research and Ipsos MORI on behalf of the Department for Work and Pensions. Views expressed in this report are not necessarily those of the Department for Work and Pensions or any other government department. © Crown copyright 2015. You may re-use this information (not including logos) free of charge in any format or medium, under the terms of the Open Government Licence. To view this licence, visit http://www.nationalarchives.gov.uk/doc/open-government-licence/ or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: [email protected]. This document/publication is also available on our website at: https://www.gov.uk/government/organisations/department-for-work-pensions/about/ research#research-publications If you would like to know more about DWP research, please email: [email protected] First published December 2015. ISBN 978 1 911003 14 4 Views expressed in this report are not necessarily those of the Department for Work and Pensions or any other Government Department. Evaluation of Removal of the Spare Room Subsidy – Final Report Summary This report presents findings from the evaluation of the Removal of the Spare Room Subsidy (RSRS) undertaken by Ipsos MORI and the Cambridge Centre for Housing and Planning Research. The fieldwork was carried out over the first 20 months of implementation, from April 2013 until November 2014. An interim report was published in July 2014. -

The Benefit Cap

BRIEFING PAPER Number 06294, 20 July 2015 By Wendy Wilson The Benefit Cap Inside: 1. Background 2. Rationale 3. Numbers & characteristics of affected households 4. Reaction and comment 5. Reducing the cap threshold www.parliament.uk/commons-library | intranet.parliament.uk/commons-library | [email protected] | @commonslibrary Number 06294, 20 July 2015 2 Contents Summary 3 1. Background 4 Rolling out the benefit cap 4 Setting the level of the cap 4 Calculating the cap: included and excluded benefits 4 Applying the cap 6 2. Rationale 7 3. Numbers & characteristics of affected households 8 4. Reaction and comment 12 Supported and temporary accommodation 15 The cap and affordable rent tenure 19 The Welfare Reform Bill in the House of Lords 20 Secondary Legislation Scrutiny Committee – 10th Report 2012 23 Assessment by the Equality and Human Rights Commission (EHRC) 24 Legal challenge 25 One year review of the cap 26 5. Reducing the cap threshold 30 Comment 31 Cover page image copyright: Money UK British pound coins by hitthatswitch. Licensed under CC BY 2.0 / image cropped. 3 The Benefit Cap Summary As part of the October 2010 Spending Review the Coalition Government announced an intention to cap total household benefits at £500 per week for a family (£26,000 per year) and £350 per week (£18,200 per year) for a single person with no children. Households with income from benefits in excess of these caps experience a reduction in their Housing Benefit entitlement. Measures to introduce the cap were included in sections 96 and 97 of the Welfare Reform Act 2012 and the Benefit Cap (Housing Benefit) Regulations 2012. -

Carers UK Briefing on Housing Benefit Size Criteria Rules the Bedroom Tax

Policy Briefing Housing Benefit size criteria rules: the ‘bedroom tax’ January 2013 Summary Housing Benefit is changing and a restriction is being introduced on the number of rooms in a socially rented home which will be covered by Housing Benefit. The new size criteria could have a major impact on certain groups of carers and some families may be unable to cover the shortfall putting them at risk of having to move. Carers UK is particularly concerned that couples where one person is disabled, only one bedroom will be allowed under Housing Benefit rules. This means that a couple who need an extra bedroom for equipment or are unable to sleep in the same room, not be given enough Housing Benefit to cover the extra rent costs of having this room to retain this room. Many homes have been specially adapted, often at a considerable financial cost to local authorities or families themselves. If these families are forced to move, this would be not only distressing for families and disruptive to care arrangements but could risk a greater long-term cost as adaptations need to be replaced in new homes. This note summarises the new rules and looks ahead to further changes on the introduction of Universal Credit later next year. Size criteria rules: what are they? The size criteria rules, have restricted Housing Benefit for private sector tenants for some years. From 1 April 2013 they will also be applied to social sector tenants (people with housing association or local council tenancies for instance). This is commonly referred to as the ‘Bedroom Tax’.