Executive Remuneration in the 100 Largest Companies Listed in Switzerland (Summary Version)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Media Release

CREDIT SUISSE AG Paradeplatz 8 Tel. +41 844 33 88 44 P.O. Box Fax +41 44 333 88 77 CH-8070 Zurich [email protected] Switzerland Rating Overview of Swiss Companies Company CS Rating CS Outlook Changes since June 2009 S&P Moody's ABB Low A Stable A–, Stable A3, Stable Adecco Mid BBB Negative Outlook changed from Stable to Negative BBB–, Stable Baa3, Stable AFG Low BBB Stable Outlook changed from Negative to Stable n.r. n.r. Alpiq High A Stable n.r. n.r. Aryzta High BBB Stable Coverage initiation n.r. n.r. Axpo Low AA Stable n.r. n.r. Bâloise Low A Stable A–, Stable1 n.r. BKW Low AA Stable n.r. n.r. –1 notch, outlook changed from Negative to Bobst Group Low BBB Stable n.r. n.r. Stable Bucher Industries High BBB Stable n.r. n.r. CKW n.r. n.r. Drop coverage Clariant High BB Stable BBB–, Stable Ba1, Stable Coop Low A Stable n.r. n.r. –1 notch, outlook changed from Stable to Edipresse High BB Negative n.r. n.r. Negative –1 notch, outlook changed from Negative to EGL Low A Stable n.r. n.r. Stable EMS Chemie Low A Stable Outlook changed from Negative to Stable n.r. n.r. Energiedienst Low A Stable n.r. n.r. EOS n.r. n.r. Drop coverage Flughafen Zurich Mid BBB Stable BBB+, Positive n.r. Forbo Mid BBB Stable n.r. n.r. Geberit High BBB Stable A–, Stable n.r. -

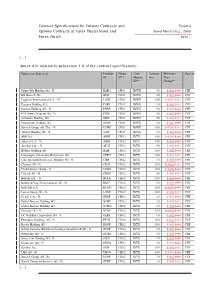

Contract Specifications for Futures Contracts and Eurex14 Options Contracts at Eurex Deutschland and Stand March 2831, 2008 Eurex Zürich Seite 1

Contract Specifications for Futures Contracts and Eurex14 Options Contracts at Eurex Deutschland and Stand March 2831, 2008 Eurex Zürich Seite 1 [....] Annex A in relation to subsection 1.6 of the contract specifications: Futures on Shares of Produkt- Group Cash Contract Minimum Currency ID ID** Market- Size Price ID** Change* Julius Bär Holding AG - N. BAEG CH01 XSWX 50 0.0010.01 CHF BB Biotech AG BIOF CH01 XSWX 50 0.0010.01 CHF Logitech International S.A. - N. LOGF CH01 XSWX 100 0.00010.01 CHF Pargesa Holding S.A. PARF CH01 XSWX 10 0.0010.01 CHF Sonova Holding AG - N. PHBF CH01 XSWX 50 0.0010.01 CHF PSP Swiss Property AG - N. PSPF CH01 XSWX 50 0.0010.01 CHF Schindler Holding AG SINF CH01 XSWX 50 0.0010.01 CHF Straumann Holding AG STMF CH01 XSWX 10 0.0010.01 CHF Swatch Group AG, The - N. UHRF CH01 XSWX 100 0.00010.01 CHF Valiant Holding AG - N. VATF CH01 XSWX 10 0.0010.01 CHF ABB Ltd. ABBF CH02 XVTX 100 0.00010.01 CHF Adecco S.A. - N. ADEF CH02 XVTX 100 0.0010.01 CHF Actelion Ltd. - N. ATLG CH02 XVTX 50 0.0010.01 CHF Bâloise Holding AG BALF CH02 XVTX 100 0.0010.01 CHF Compagnie Financière Richemont AG CFRH CH02 XVTX 100 0.0010.01 CHF Ciba Spezialitätenchemie Holding AG - N. CIBF CH02 XVTX 10 0.0010.01 CHF Clariant AG - N. CLNF CH02 XVTX 100 0.00010.01 CHF Credit Suisse Group - N. CSGG CH02 XVTX 100 0.00010.01 CHF Geberit AG - N. -

Swiss Opportunity Fund

January 2021 Swiss Opportunity Fund FACT SHEET January 2021 / PERFORMANCE 0.19% After stocks ended 2020 with a such a strong performance, a The Swiss Opportunity Fund kept pace with its relevant bench- bumpy start to the new year could be expected. There was a raft mark and crept 0.19% higher. There was no clear trend among of economic news with few upside surprises. Political develop- the portfolio positions. Logitech (8.08%) and Zur Rose (44.7%) ments in the US captured the world's attention. The assault on continued to drive performance, as did some cyclical positions the Capitol Building, the formal confirmation of President-Elect such as Zehnder (10.15%), SIG (3.31%) and Sulzer (3.54%). Mean- Joe Biden’s win and the Democratic sweep of the Georgia run-off while, the rather defensive plays such as Sonova (-6.35%), Strau- election giving them control of the US Senate all happened dur- mann (-4.06%) and Vifor Pharma (-12.81%) hurt overall perfor- ing the space of 48 hours. Observers of these events may have mance. Turning to transaction activity, we opened a position in held their breath, but financial markets hardly reacted. That was Stadler Rail (10.34%) and sharply reduced our position in Zur attributable, in our opinion, to the prospect of more fiscal stimu- Rose as its share price surged on frothy sentiment. So where do lus and to statements from the relevant central banks in which we stand now after the opening month of the new year? Obvi- they pledged to keep monetary policy ultra-expansive. -

2019 Switzerland Spencer Stuart Board Index

2019 Switzerland Spencer Stuart Board Index About Spencer StuArt Spencer Stuart has had an uninterrupted presence in Switzerland since 1959, when it opened its Zurich office. Spencer Stuart is one of the world’s leading executive search consulting firms. We are trusted by organisations around the world to help them make the senior-level leadership decisions that have a lasting impact on their enterprises. Through our executive search, board and leadership advisory services, we help build and enhance high-performing teams for select clients ranging from major multinationals to emerging companies to nonprofit institutions. Privately held since 1956, we focus on delivering knowledge, insight and results though the collaborative efforts of a team of experts — now spanning more than 60 offices, over 30 countries and more than 50 practice specialties. Boards and leaders consistently turn to Spencer Stuart to help address their evolving leadership needs in areas such as senior-level executive search, board recruitment, board effectiveness, succession planning, in-depth senior management assessment and many other facets of organisational effectiveness. For more information on Spencer Stuart, please visit www.spencerstuart.com. Social Media @ Spencer Stuart Stay up to date on the trends and topics that are relevant to your business and career. @Spencer Stuart © 2020 Spencer Stuart. All rights reserved. For information about copying, distributing and displaying this work, contact: [email protected]. 1 spencer stuart Contents 3 Foreword -

FTSE Developed Europe

2 FTSE Russell Publications 19 August 2021 FTSE Developed Europe Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 1&1 AG 0.01 GERMANY Avast 0.03 UNITED Cnp Assurance 0.02 FRANCE 3i Group 0.14 UNITED KINGDOM Coca-Cola HBC AG 0.06 UNITED KINGDOM Aveva Group 0.05 UNITED KINGDOM A P Moller - Maersk A 0.1 DENMARK KINGDOM Coloplast B 0.19 DENMARK A P Moller - Maersk B 0.15 DENMARK Aviva 0.19 UNITED Colruyt 0.03 BELGIUM A2A 0.03 ITALY KINGDOM Commerzbank 0.07 GERMANY Aalberts NV 0.05 NETHERLANDS AXA 0.43 FRANCE Compagnie Financiere Richemont SA 0.55 SWITZERLAND ABB 0.51 SWITZERLAND B&M European Value Retail 0.06 UNITED Compass Group 0.33 UNITED KINGDOM ABN AMRO Bank NV 0.04 NETHERLANDS KINGDOM BAE Systems 0.21 UNITED Acciona S.A. 0.03 SPAIN Continental 0.14 GERMANY KINGDOM Accor 0.06 FRANCE ConvaTec Group 0.05 UNITED Baloise 0.06 SWITZERLAND Ackermans & Van Haaren 0.03 BELGIUM KINGDOM Banca Mediolanum 0.02 ITALY ACS Actividades Cons y Serv 0.06 SPAIN Covestro AG 0.1 GERMANY Banco Bilbao Vizcaya Argentaria 0.36 SPAIN Adecco Group AG 0.09 SWITZERLAND Covivio 0.04 FRANCE Banco Santander 0.58 SPAIN Adevinta 0.04 NORWAY Credit Agricole 0.14 FRANCE Bank Pekao 0.03 POLAND Adidas 0.63 GERMANY Credit Suisse Group 0.22 SWITZERLAND Bankinter 0.03 SPAIN Admiral Group 0.08 UNITED CRH 0.35 UNITED Banque Cantonale Vaudoise 0.02 SWITZERLAND KINGDOM KINGDOM Barclays 0.35 UNITED Adyen 0.62 NETHERLANDS Croda International 0.12 UNITED KINGDOM KINGDOM Aegon NV 0.06 NETHERLANDS Barratt Developments 0.09 UNITED Cts Eventim 0.03 GERMANY Aena SME SA 0.1 SPAIN KINGDOM Cyfrowy Polsat SA 0.02 POLAND Aeroports de Paris 0.03 FRANCE Barry Callebaut 0.07 SWITZERLAND Daimler AG 0.66 GERMANY Ageas 0.09 BELGIUM BASF 0.64 GERMANY Danone 0.37 FRANCE Ahold Delhaize 0.26 NETHERLANDS Bayer AG 0.53 GERMANY Danske Bank A/S 0.1 DENMARK AIB Group 0.02 IRELAND Bechtle 0.04 GERMANY Dassault Aviation S.A. -

Notice N19 2019

Swiss Instruments to be delisted from CLXNz CH0011115703 Crealogix Holding AG LEHNz CH0022427626 LEM Holding SA SFZNz CH0014284498 Siegfried Holding AG UBS MTF effective 1 July CMBNz CH0225173167 Cembra Money Bank AG LEONz CH0190891181 Leonteq AG SGKNz CH0011484067 St Galler Kantonalbank AG CONz CH0244017502 Conzzeta AG LHNz CH0012214059 LafargeHolcim Ltd SGSNz CH0002497458 SGS SA COTNz CH0360826991 Comet Holding AG LINNz CH0001307757 Bank Linth LLB AG SIGNz CH0435377954 SIG Combibloc Group AG Symbol ISIN Issuer CPENz CH0048854746 Castle Private Equity Ltd LISNz CH0010570759 Chocoladefabriken Lindt & Spruengli AG SIKAz CH0418792922 Sika AG ABBNz CH0012221716 ABB Ltd CPHNz CH0001624714 CPH Chemie & Papier Holding AG LISPz CH0010570767 Chocoladefabriken Lindt & Spruengli AG SIMAz CH0014420878 UBS CH Property Fund - Swiss Mixed Sima ADENz CH0012138605 Adecco Group AG CSGNz CH0012138530 Credit Suisse Group AG LLQz CH0033813293 Lalique Group SA SLHNz CH0014852781 Swiss Life Holding AG ADVNz CH0008967926 Adval Tech Holding AG DAEz CH0030486770 Daetwyler Holding AG LOGNz CH0025751329 Logitech International SA SNBNz CH0001319265 Schweizerische Nationalbank ADXNz CH0029850754 Addex Therapeutics Ltd DCNz CH0008531045 Datacolor AG LONNz CH0013841017 Lonza Group AG SOONz CH0012549785 Sonova Holding AG AEVSz CH0478634105 AEVIS VICTORIA SA DESNz CH0020739006 Dottikon Es Holding AG LUKNz CH0011693600 Luzerner Kantonalbank AG SPCEz CH0009153310 Spice Private Equity AG AIREz CH0010947627 Airesis SA DKSHz CH0126673539 DKSH Holding AG MBTNz CH0108503795 -

Notice N19 2019

UBS MTF Market Notice Swiss Market Removal 28 June 2019 Dear Member, Following the announcement of the Swiss Federal Department of Finance on June 24 (FDF prepared to activate measure to protect Swiss stock exchange infrastructure), and further to our notice of the same date, UBS MTF will remove all instruments issued by companies with registered offices in Switzerland which are listed on Swiss trading venues. This update will take effect from 1 July. Our daily Stock Universe file, published on our website at https://www.ubs.com/global/en/investment- bank/ib/multilateral-trading-facility/reference-data.html and by SFTP, will reflect the removal of these instruments as of this date. Instruments not subject to the Swiss measure are unaffected; a list of affected instruments is attached to this notice. If you have any queries regarding this notice please contact the UBS MTF Supervisors at +44 207 568 2052 or [email protected]. UBS MTF Management Notice N19 2019 UBS MTF Notices and documentation are available at https://www.ubs.com/mtf. If you have any queries regarding this notice, or comments on the above, please contact the UBS MTF Supervisors at +44 20 7568 2052 or [email protected]. UBS MTF is operated by UBS AGLB which is authorised by the Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and Prudential Regulation Authority. UBS AG is a public company incorporated with limited liability in Switzerland domiciled in the Canton of Basel-City and the Canton of Zurich respectively registered at the Commercial Registry offices in those Cantons with Identification No: CHE-101.329.561 as from 18 December 2013 (and prior to 18 December 2013 with Identification No: CH-270.3.004.646-4) and having respective head offices at Aeschenvorstadt 1, 4051 Basel and Bahnhofstrasse 45, 8001 Zurich, Switzerland and is authorised and regulated by the Financial Market Supervisory Authority in Switzerland. -

FTSE Publications

2 FTSE Russell Publications FTSE Developed Europe ex UK ex 19 August 2021 Controversies ex CW Index Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 1&1 AG 0.02 GERMANY BMW 0.41 GERMANY Engie 0.27 FRANCE A P Moller - Maersk A 0.14 DENMARK BMW AG Pref 0.06 GERMANY Eni 0.37 ITALY A P Moller - Maersk B 0.2 DENMARK BNP Paribas 0.81 FRANCE Epiroc A 0.17 SWEDEN A2A 0.04 ITALY Boliden 0.13 SWEDEN Epiroc B 0.09 SWEDEN Aalberts NV 0.06 NETHERLANDS Bollore 0.06 FRANCE EQT Partners AB 0.1 SWEDEN ABB 0.69 SWITZERLAND Bouygues 0.09 FRANCE Equinor ASA 0.24 NORWAY ABN AMRO Bank NV 0.06 NETHERLANDS Brenntag AG 0.17 GERMANY Ericsson A 0.01 SWEDEN Acciona S.A. 0.04 SPAIN Bureau Veritas S.A. 0.11 FRANCE Ericsson B 0.45 SWEDEN Accor 0.08 FRANCE Buzzi Unicem 0.03 ITALY Erste Group Bank 0.12 AUSTRIA Ackermans & Van Haaren 0.04 BELGIUM CaixaBank 0.16 SPAIN EssilorLuxottica 0.65 FRANCE ACS Actividades Cons y Serv 0.08 SPAIN Campari 0.08 ITALY Essity Aktiebolag B 0.24 SWEDEN Adecco Group AG 0.12 SWITZERLAND Capgemini SE 0.36 FRANCE Eurazeo 0.05 FRANCE Adevinta 0.05 NORWAY Carl Zeiss Meditec 0.08 GERMANY Eurofins Scienti 0.17 FRANCE Adidas 0.85 GERMANY Carlsberg (B) 0.22 DENMARK Euronext 0.11 FRANCE Adyen 0.84 NETHERLANDS Carrefour 0.14 FRANCE Evolution AB 0.3 SWEDEN Aegon NV 0.09 NETHERLANDS Casino Guichard Perrachon 0.02 FRANCE Evonik Industries AG 0.08 GERMANY Aena SME SA 0.14 SPAIN Castellum 0.08 SWEDEN Evotec 0.08 GERMANY Aeroports de Paris 0.04 FRANCE CD Projekt SA 0.04 POLAND Exor NV 0.1 ITALY Ageas 0.12 BELGIUM Cellnex Telecom SAU 0.46 SPAIN Fastighets AB Balder B 0.08 SWEDEN Ahold Delhaize 0.35 NETHERLANDS Chr. -

Swiss Prime Site Annual Report 2019

2019ANNUAL REPORT Reporting 2019 This year, Swiss Prime Site is publishing an integrated report for the first time. The report is based on the Inte- grated Reporting (<IR>) Framework of the International Integrated Reporting Council (IIRC) and follows the Glob- al Reporting Initiative (GRI) standards. Swiss Prime Site is reporting for the first time on climate-related risks us- ing the guidelines of the Task Force on Climate-related Financial Disclosures (TCFD). Reporting consists of the online report (www.sps. swiss/reporting) and the separate sub-reports (PDF download). For reasons of sustainability, only the short report is available as a printed version. Contents Integrated Report Corporate Governance Report Compensation Report Financial Report 2019INTEGRATED REPORT Integrated Report 4 Key figures 5 Our strengths 6 Foreword by the Chairman 8 Interview with the CEO 14 Interview with the CEO Immobilien 18 Board of Directors 19 Executive Board 20 Success story 22 Our markets 24 Risk management 26 Strategy 28 Property portfolio 30 Project pipeline Value creation 32 Assuming responsibility 36 Stakeholder engagement 38 Materiality analysis 42 Sustainability goals and roadmap 48 Business model 50 Integrated value creation 53 Value creation group companies 58 Reduction pathway 64 TCFD Report Notes 70 GRI Report 100 Key figures of group companies 106 GRI Content Index 110 Independent Limited Assurance Report on selected GRI Disclosures Reporting structure 113 Information policy Reporting consists of the online report (sps.swiss/en/reporting) -

UBS Underlyings-Offering on Swiss DOTS

Public Distribution June 2014 Switzerland UBS underlyings-offering on Swiss DOTS A D I ABB Ltd. Daimler AG IBM Corporation Actelion Ltd. DAX® Infineon Technologies AG Adecco SA Dell Inc. Intel Corporation Advanced Micro Devices Inc. Deutsche Bank AG AFG Arbonia-Forster-Holding AG Deutsche Lufthansa AG J Alcatel-Lucent SA Deutsche Telekom AG Johnson & Johnson Alcoa Inc. DKSH Holding Ltd. JPMorgan Chase & Co. Allianz SE Dow Chemical Co. Julius Baer Group Ltd. Alpiq Holding AG Dow Jones Industrial Average K Amazon.com Inc. Dufry AG K+S AG Amgen Inc. Kaba Holding AG AMS AG E Kudelski SA Apple Inc. E.ON SE Kühne + Nagel International AG Aryzta AG eBay Inc. Kuoni Reisen Holding AG AXA SA EFG International AG EUR/CHF L B EUR/USD Lilly (Eli) & Co. BAIDU Inc. Euro STOXX 50® Index Logitech International SA Bâloise Holding AG Exxon Mobil Corporation Lonza Group AG Bank of America Corporation LVMH Moët Hennessy Louis Vuitton Barrick Gold Corporation F Barry Callebaut AG Facebook, Inc. M BASF SE First Solar Inc. McDonald’s Corporation Basilea Pharmaceutica AG Forbo Holding AG MDAX® BKW AG Freeport McMoRan Copper & Gold Inc. Merck & Co BNP Paribas S.A. Meyer Burger Technology AG Boeing Co. G Micronas Semiconductor Holding AG Bucher Industries Ltd Galenica AG Microsoft Corporation GAM Holding AG C Gategroup Holding AG N Caterpillar Inc. Geberit AG Nasdaq 100® Index Cembra Money Bank AG General Electric Company Nestlé SA Charles Vögele Holding AG General Motors Company Netflix Chesapeake Energy Corp. Georg Fischer AG Newmont Mining Corporation Chevron Corp. Givaudan SA Nobel Biocare Holding AG Cisco Systems, Inc. -

Zmonthly December 16

Swiss Small & Mid Cap Fund Class A zMonthly December 16 2016 closes on an upbeat note Performance since Launch (as of 30/12/2016) The Swiss equities market moved higher at the end of the year in the wake of US stock markets, with the blue chips in the SMI outperforming for once. In the small and mid cap segment, cy- clical stocks and securities with above-average short-selling po- sitions attracted the strongest demand. The market followed the pattern of ignoring negative news flow – such as the “No” vote in Italy’s referendum on constitutional reform – and focusing in- stead on positive news. The ECB left interest rates at rock bot- tom and extended its bond-purchasing programme at least until December 2017. This move pushed the euro down to a new re- zCapital Swiss Small & Mid Cap Fund A SPI Extra® (indexed) cord low against the US dollar. After months of prevarication, the Fed finally announced a 0.25 percentage point increase in interest rates, long since priced in by the markets, and also sig- Performance (as of 30/12/2016) nalled another three hikes over the course of 2017. There were YTD (Fund / Benchmark) 9.3% / 8.5% several noteworthy company announcements as well. Lonza is 1 year 9.3% / 8.5% acquiring the US capsule manufacturer Capsugel for USD 5.5 3 years p.a. 12.4% / 10.3% billion. Market players felt the acquisition was expensive and 5 years p.a. 16.1% / 14.3% marked down Lonza’s share price. The share price of Leonteq, Since launch p.a. -

Vontobel Fund (CH) - Vescore Swiss Equity Multi Factor A

Asset Management / Monthly Factsheet as at 30/11/2020 Vontobel Fund (CH) - Vescore Swiss Equity Multi Factor A Approved for Wholesale/Retail investors in: CH. Investment objective Fund Data This equity fund aims to achieve attractive long-term returns compared Investment manager Vontobel Asset Management AG to traditional Swiss equity market indices weighted by market capitaliza- Custodian RBC Investor Services Bank S.A. tion. Management company Vontobel Fonds Services AG Fund domicile Switzerland Key features The fund actively invests in around 50 of the largest equities listed in Fund currency CHF Switzerland, measured by market capitalization. Based on quantitative Share class currency CHF models, the fund tactically adjusts the weights of its positions to maintain Swinging Single Pricing Yes adequate exposure to the fundamental factor premia driving equity re- Net asset value 152.95 turns, such as Value, Momentum, Quality, and Minimum Volatility. Fund volume in mln 722.44 CHF Management fee 1.000% Approach TER (per 31/08/2020) 1.01% Vescore's proven investment process amalgamates outstanding propriet- Launch date 26/01/2016 ary models, cutting-edge technology, and active management. For this Launch price 100.00 fund, the highly experienced investment team uses their models to con- tinuingly assess the attractiveness of each fundamental factor premium End of fiscal year 28. February and make the corresponding investment decisions without emotional bi- Last distribution 2.00 / June ases, while ensuring systematic risk control at all times. ISIN CH0311188863 Valor 31118886 Bloomberg VESEMFA SW Distribution policy Distributing As of 31.10.2020 Net Performance of A Share (in CHF and %)** Net Performance of A Share in CHF** 3 y.