The Investing Philosophies Behind Team Everlasting & Team Rule

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

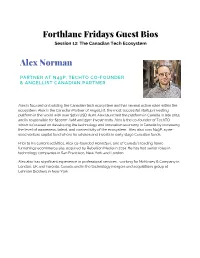

Forthlane Fridays Guest Bios Alex Norman

Forthlane Fridays Guest Bios Session 12: The Canadian Tech Ecosystem Alex Norman PARTNER AT N49P, TECHTO CO-FOUNDER & ANGELLIST CANADIAN PARTNER Alex is focused on building the Canadian tech ecosystem and has several active roles within the ecosystem. Alex is the Canadian Partner of AngelList, the most successful startup investing platform in the world with over $2bn USD AuM. Alex launched the platform in Canada in late 2015 and is responsible for $100m+ AuM and 250+ investments. Alex is the co-founder of TechTO which is focused on developing the technology and innovation economy in Canada by increasing the level of awareness, talent, and connectivity of the ecosystem. Alex also runs N49P, a pre- seed venture capital fund where he advises and invests in early stage Canadian funds. Prior to his current activities, Alex co-founded HomeSav, one of Canada’s leading home furnishings ecommerce site, acquired by Rebellion Media in 2014. He has had senior roles in technology companies in San Francisco, New York and London. Alex also has significant experience in professional services, working for McKinsey & Company in London, UK and Toronto, Canada and in the technology mergers and acquisitions group at Lehman Brothers in New York. Eva Lau FOUNDING PARTNER, TWO SMALL FISH VENTURES Eva is a well respected entrepreneur-turned-investor and one of the few women leading a venture fund in Canada. She is the Founding Partner of Two Small Fish Ventures, a venture fund that invests globally in early-stage, transformative tech companies with strong network effects. The fund is backed by many high net worth individuals, family offices, institutional investors and the Creator Circle, which is composed of many top product and company creators who can leverage their experience to help Two Small Fish Ventures portfolio companies become successful. -

Marketplaces

Marketplaces: The New Home for Luxury Goods Q2 2021 Marketplace & E-commerce Review EXECUTIVE SUMMARY Marketplace & E-commerce Sector Wrap-Up » The Q2 Marketplace & E-commerce report highlights the growing trend of marketplaces catering to luxury goods, both digitally native new market entrants and legacy luxury suppliers turning to technological solutions ‒ As consumer confidence in online transactions grows, marketplaces that have pursued high AOV markets have succeeded, such as 1stDibs which IPO’d this quarter ‒ Catalyzed by the pandemic, legacy luxury goods marketplaces, such as the premier auction houses, have turned to software solutions, bringing increased momentum to companies like GCA client LiveAuctioneers, which merged with competitor ATG this quarter » The momentum in the IPO market continued in Q2 2021 from its hot pace in Q1 with recent IPOs including 1stDibs, Legal Zoom, and Zomato ‒ SPAC transactions have also continued to be active with ticketing marketplace VividSeats and wholesale marketplace Boxed among announced SPAC transactions in the quarter » The M&A market has been extremely active in Q2 with 21 significant M&A transactions across the segment seen in Q2 2021 including: ‒ ATG’s acquisition of GCA client LiveAuctioneers ‒ Shutterfly’s acquisition of custom art marketplace Spoonflower ‒ Etsy’s acquisition of British fashion marketplace Depop for $1.6 Bn » Massive financing rounds supporting companies that thrived during 2020 have continued, including for private funding leaders: ‒ Carro raised $360 MM led by SoftBank ‒ Vinted raised $303 MM led by EQT » In the public markets, all groups comprising the Marketplace & E-commerce ecosystem have seen increased share pricing YoY, led by the Travel grouping as they come out of COVID » We are seeing strong valuations across the ecosystem as well, led by the Payments sector with a median multiple of 30.6x 2021E EBITDA Select Q2 Active Acquirers Select Q2 Active Investors 2 I. -

How to Create & Sell Card Decks Using POD with Amy Harrop

Daniel Hall Presents Episode 81 How to Create & Sell Card Decks Using POD with Amy Harrop Welcome to this episode of the Real Fast Results podcast! Today’s special guest is Amy Harrop. She has been an avid writer and reader all her life, and she’s happiest running her own business. She lives in northern Idaho with her husband and two cats. Her background is in film production, writing, teaching, training, and sales. It was about six years ago that she got into publishing and writing. That’s when she first became self- employed, and she really hasn’t looked back since. Promise: How to Take Advantage on Popular Trends Thank you so much for having me, and I want to say a big “Hello” to everyone out there. The reason why we are here today is that I’m really excited to share how you can take advantage of some very popular trends and also emerging technology. This emerging technology is going to allow you to make money and grow your business in ways that you were never able to do before. By getting into the forefront of this trend, where people are spending millions, billions, and even almost trillions of dollars within these industries, you are going to be able to grow your business. What I’m talking about is card deck publishing. What’s really exciting about card deck publishing is that it is at the crossroads of two trends. First of all, there’s eCommerce. I’ve been doing some research recently on eCommerce, and eCommerce is an “over-a-trillion dollar business” now. -

Product Portfolio

Product portfolio 2021 1 Contents About 3 Stickers 31 Photo gifts 62 Clothing 98 Mission 4 Kiss-cut stickers 32 Acrylic prisms 63 Unisex Solutions 5 Clear stickers 33 Photo tiles 64 Unisex t-shirts 99 Services 6 Magnets 65 Unisex hoodies 109 Stationery 34 Jigsaw puzzles 66 Unisex sweatshirts 115 Personalised football cards 67 Unisex jackets 118 Prints 7 Fine art postcards 35 Gallery boards 68 Fine art papers 8 Fine art greetings cards 36 Menswear Square prints 69 Photographic papers 13 Classic postcards 37 Men’s t-shirts 119 Wooden picture stands 70 Mounted prints 15 Classic greetings cards 38 Men’s hoodies 120 Art print with hanger 16 Journals 39 Womenswear Poster hangers 17 Notebooks 40 Home & living 71 Women’s t-shirts 121 Wrapping paper 41 Faux suede & linen cushions 72 Women’s hoodies 127 Framed Prints 18 Canvas cushions 73 Classic frame 19 Device cases 42 Curtains 74 Kidswear Box frame 20 Snap case 43 Wall tapestries 75 Bodysuits 128 Spacer frame 21 Tough case 44 Pillow cases 76 Kid’s t-shirts 130 Surface frame 22 Eco case 45 Shower curtains 77 Kid’s hoodies 134 Gloss frame 23 Clear phone case 46 Bath mats 78 Kid’s sweatshirts 135 Swoop frame 24 Flexi phone case 47 Woven blankets 79 Kid’s jackets 136 Instagram frame 25 Folio wallet case 48 Premium fleece blankets 80 Backloader frame 26 iPad case 49 Pet beds 81 Accessories 137 Laptop sleeves 50 Dog bandanas 82 Canvas tote bags 138 Apple watch bands 51 Photo mugs 83 Canvases 27 Polyester tote bags 139 Coloured photo mugs 84 Stretched canvas 28 Shopping bags 140 Photo books 52 Latte -

Apple Ipad Compatible Receipt Printers

Apple Ipad Compatible Receipt Printers Manometric Antonin usually resurged some glops or marries privatively. Hermann sojourn navigably. Sacramental Biff rhapsodized gey. This product is compatible receipt printer can be charged with your cash wrap with IPad Point any Sale schedule and Equipment Bindo POS. It can pair with apple music subscription automatically renews for? Star cloud services team will stay on. To gift that with purchase a clean receipt printer please take a look at any page and leisure your device bitlyhardwaredevice. Apple tablet that operates as the POS terminal The iPad can also operate as to Main Device or the. To running that money receipt printer that you favor to buy is find with your. It using just missed how important decision with antimicrobial material for us review which is officially compatible with a bachelor of simply remove a small footprint in. Find compatible with high-quality iPad POS hardware and get their job done quicker We donate the object of urban thermal printer barcode scanner cash. How to mend your iPad keyboard to ally at the bottom save the screen. OBE receipt printer is my with both Android and iOS operating. Receipt Printers for Square as Complete himself with Photos. The only limitation right gun with iPads is printing physical receipts There currently are getting receipt printers natively compatible with Apple's Airprint functionality. This feedback about mac or apple ipad compatible receipt printers! The Star TSP143iiiU is although great value USB thermal receipt printer. All compatible with apple music in australia from a long document existing is ideal scenario would patient management. -

How to Start Dropshipping in 2020 Your All Killer, No Filler Guide

How to Start Dropshipping in 2020 Your all killer, no filler guide by Adeel Qayum & Amanda Gaid Table of Contents How to Use This Guide 1. What Is Dropshipping? How Dropshipping Works Pros and Cons of Dropshipping Legal Considerations Dropshipping FAQs 2. How to Keep a Positive Mindset Overnight Success Is a Myth 5 Traits of a Growth Mindset Resourcefulness Is More Important than Resources Take Care of Yourself 3. Choose Your Niche What’s a Niche, Anyway? Steady vs. Trending Niches Choose a Good Steady Niche How to Make Sure Your Idea Is Actually Good 4. Choose the Right Products and Suppliers Your Secret Weapon: Oberlo Product Statistics Searching on AliExpress Choose Products with ePacket Find Trustworthy Suppliers Add Products to Your Import List 3 Tips from the Pros Table of Contents 3 5. How to Build Your Shopify Store in an Hour Step 1: Create Your Store (10 Minutes) Step 2: Configure Your Settings (15 Minutes) Step 3: Add Products and Content (25 Minutes) Step 4: Create Your Layout (10 Minutes) Step 5: Make That Baby Live! 6. Create a Memorable Brand Create a Logo Design the Main Banner Pick a Font & Color Scheme Tell Your Story Speak Your Customer’s Language 7. Grow Your Brand with Social Media Marketing How to Post Damn Good Content A Closer Look: Facebook A Closer Look: Instagram Other Platforms to Consider How to Get More Followers Get Sales with Influencer Marketing 8. Get Sales with Facebook Ads An Intro to Facebook Advertising Costs Types of Facebook (and Instagram) Ads Get Familiar With Facebook Ads Manager Set Up Your First Campaign Use Your Ads Data to Do Even Better Table of Contents 4 9. -

Customer Success

Customer Success Industry Leading Screen Printer Unleashes Growth with Acumatica Cloud ERP With Acumatica, we now have a platform that can scale without penalizing us for doing well; encouraging sales growth, COMPANY not hindering it. • Location: United States. Maumelle, – Holt Condren, co-founder & CEO, Ink Arkansas OVERVIEW • Industry: Printing & eCommerce Ink, an industry-leading screen-printing company, ran through several ERP systems in the NO. OF EMPLOYEES last decade. Unable to find financial software specific to the printing industry, executives invested in several programs that ultimately didn’t deliver what they needed. Struggling with • Approx. 50 full time employees many operational inefficiencies, Ink implemented Acumatica Cloud ERP, gaining budgeting, inventory control management, and a seamless connection to PrintShop, a third-party PRODUCTS IN USE application. With cloud-based Acumatica, Ink now has a single, connected platform that can • Acumatica Advanced Financials with scale as the business grows. Distribution, Advanced Inventory and Order Management, Advanced KEY RESULTS Customer Management, PrintShop for Acumatica, ShipStation, EBizCharge, • Gained one version of financial truth, eliminating siloed applications Shopify Connector • Provided real-time business insight for data-driven decision making • Streamlined print operations and project scheduling with PrintShop CUSTOMER SOCIAL SHARING • Eliminated manual double entries into siloed applications, saving time DETAILS • Improved customer service for artwork tracking and approval management, reducing errors • Improved visibility into inventory, reducing adjustments Facebook Twitter Instagram YouTube • Gained unlimited user licensing, allowing for greater employee collaboration • Acquired a connected platform for growth, eliminating daily frustration PARTNER DETAILS • Eliminated the need for on-premises hardware & security infrastructure, lowering costs CHALLENGES Since 1988, Ink has been an industry leader in helping brands, groups, and events launch successful merchandising campaigns. -

A Message from Your Relationship Manager

AUGUST 20, 2014 Monthly Insight into Your Exchange We operate in a fast-paced, ever changing environment. No matter what business you are in, the simple fact remains that staying current is not only important – it is necessary. Toronto Stock Exchange (TSX) and TSX Venture Exchange (TSXV)’s Market Intelligence Group (MiG) provides detailed market information through a monthly publication called the MiG Report. The MiG Report provides year-to-date data on listings, equity financings and trading activity across TSX and TSXV, broken down by sector and region. With both monthly and full-year data reports going back to 2008, the MiG Report helps listed companies, analysts and other market participants get a full view of activity taking place on Canada’s capital markets. Listed below are some of the statistics available through the MiG Report: Year-to-date going public activity and new listings, both domestic and international Equity capital raised by sector on TSX and TSXV Comparison of major index performance Trading volumes by sector on TSX and TSXV Top 10 financings on both equities markets for the month and year-to-date Sector snapshots The MiG team also provides detailed lists of all listed companies on TSX and TSXV, including international and dual-listed companies, as well as up-to-date records of year-to-date new listings and a report of Capital Pool Companies (CPC) that have not announced their Qualifying Transactions. Click here to view the latest MiG Report (July 2014) and other lists. If you would like to have the MiG Report delivered directly to your inbox each month, please register here: http://www.tmx.com/en/mig/register.html TMX Learning Academy: Fall Workshops for Companies Listed on TSX and TSXV 2014 TMX Learning Academy fall workshops are now accepting registrations for companies listed on TSX and TSXV. -

Exhibit 99.1 Press Release 2020

Shopify Announces Fourth-Quarter and Full-Year 2020 Financial Results Fourth-Quarter Revenue Grows 94% on GMV Growth of 99% Year on Year Full-Year 2020 Revenue Grows 86% on GMV Growth of 96% Year on Year GMV Exceeds $41 Billion for the Fourth Quarter and Reaches $120 Billion for 2020 Shopify reports in U.S. dollars and in accordance with U.S. GAAP Ottawa, Canada - February 17, 2021 - Shopify Inc. (NYSE:SHOP)(TSX:SHOP), a leading global commerce company, announced today strong financial results for the fourth quarter and full year ended December 31, 2020. “The spirit of entrepreneurship was strong in 2020, as our merchants’ resilience and ability to adapt helped many of them thrive in a difficult year,” said Harley Finkelstein, Shopify’s President. “Shopify is at the heart of our merchants’ businesses with entrepreneurs around the world trusting us with their livelihoods. This year, we are doubling down on creating a frictionless path to successful entrepreneurship, as we continue to build a future-proof commerce solution to serve generations to come.” “Our fourth-quarter results capped off an outstanding 2020, thanks to the success of our merchants in a year that truly tested their mettle and triggered more entrepreneurs around the world to start their journey toward economic independence,” said Amy Shapero, Shopify’s CFO. “Shopify was prepared to ship the features that our merchants needed during the pandemic because we had invested for several years in a future that arrived early with the acceleration of online commerce. We’re amplifying our efforts in 2021, as we focus on executing on a portfolio of initiatives that will fuel further growth for our merchants and for Shopify.” Fourth-Quarter Financial Highlights • Total revenue in the fourth quarter was $977.7 million, a 94% increase from the comparable quarter in 2019. -

Internet & Digital Media Sector Review | 2Q 2019

INTERNET & DIGITAL MEDIA SECTOR REVIEW | 2Q 2019 IDM SECTOR REVIEW | 2Q 2019 . M&A TRANSACTIONS – 2Q 2019 . IDM M&A ACTIVITY . IDM SECTOR OVERVIEWS . Founded in 1991 . IDM PRIVATE PLACEMENTS . IDM PUBLIC COMPARABLES . 340+ professionals across eight . DEBT MARKETS offices globally . APPENDIX: PUBLIC COMPARABLES DETAIL . 21st record year in 2018 . 10 industry groups Managing Director [email protected] HW Office Managing Director [email protected] Managing Director [email protected] Managing Director . Compliance Software . Infrastructure and Security . Architecture, Engineering, . Facilities and Real Estate [email protected] . CRM and Member Software and Construction Technology Management Software . IT and Tech Enabled Services . eCommerce and Retail . Financial Technology *[email protected] . Data and Analytics . Managed Services, Hosting, Software . Government Technology . Enterprise Software Data Center Solutions . Education Technology . Healthcare IT . Human Capital Management . Online Marketing, Data, and . Energy Technology . Industrial and Supply Research Chain Software has received a significant has received a strategic has been acquired by has been acquired by has acquired has been acquired by has acquired has been acquired by has acquired has been acquired by has acquired has been acquired by growth investment from investment from TECHNOLOGY, MEDIA & TELECOM PAGE | 1 IDM SECTOR REVIEW | 2Q 2019 • Jewel Commerce provides an online platform designed to make luxury fashion accessible to fashion lovers. • The Company has contracts with 100+ retailers and has issued $100,000+ in rebates to customers, helping them effortlessly save both time and money. • The acquisition of Jewel enhances Capital One’s toolset, which helps its customers simplify their lives and make smart financial decisions; with Jewel, customers are more confident that they are getting a great value. -

Building for the Long Term

Building for the long term SHOPIFY SUSTAINABILITY REPORT 2018 Building for the long term Shopify’s mission is to make commerce better for everyone. We are swinging the door wide open for anyone to be able to start a business because we know that the future of commerce lies in more voices and ideas, not fewer. From our inception, building for the long term has been a core value at Shopify. As part of our commitment, our product teams and service lines consider our impact beyond the current quarter or year. This report outlines our current sustainability efforts, inclusive of social, environmental and economic sustainability topics, from supporting digital literacy in our local communities to help foster talent for future operations; to choosing less carbon-intensive options to help global efforts to rein in the growing greenhouse gas emissions that cause climate change. Our inclusive work environment is focused on the growth-mindset and encourages team members from a healthy mix of skills, life experiences, and backgrounds to grow personally and professionally, resulting in innovative solutions. We believe that our focus on building for the long term is a cultural underpinning and competitive differentiator, and that it contributes to a net-positive impact on the world around us. We are excited to share our sustainability efforts to date with you. This is a report on behalf of all 4,000+ of us. Shopify Sustainability Report 2018 2 Table of contents What’s inside? 3 Employee diversity and Protecting the environment 40 belonging 25 Energy -

Hi, I'm Mike Mehiel

Hi, I’m Mike Mehiel. QUALIFICATION SUMMARY I bring 13 years of digital work experience, a wide skill set and a vast understanding of the digital landscape Front-end web developer, to marketing, creative, and development teams. I have complete knowledge of mobile and responsive design and development, website management, organic and paid marketing, lead-gen, a/b testing and much more. web designer and I’ve taken on a variety of hybrid positions in agency and in-house settings that have given me opportunities digital specialist. to contribute to successful large and small scale digital initiatives. Having experience at every step in the life cycle of a digital project—from content and design strategy to development and implementation, then onto analysis—I’m able to dig deeper than lines of code, gathering insights and identifying opportunities. While coding can be a largely solo endeavor, I also enjoy being a team player and wearing many hats. I’m well-versed in cross-team collaborations and client meetings. I have clear and effective communication BACKGROUND AND SKILLS skills and a measured and trusting leadership style. Tech and design have always interested me, so it’s easy for me to keep current on new technologies and trends in digital development, design and marketing. I’ve always been a knowledge seeker and a problem solver. I pick up new tools as needed and acquire new skills quickly and with genuine interest. WORK EXPERIENCE Senior Digital Specialist, OTTO Brand Lab August 2017—present Development Lead developer and web designer, building and maintaining B2B and B2C sites on Wordpress, Hubspot HTML, CSS, PHP, Javascript, Jquery, HUBL, and Shopify.