Journal of the Senate

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Official Primary Election Results

Kansas Secretary of State Page 1 2014 Primary Election Official Vote Totals Race Candidate Votes Percent United States Senate D-Chad Taylor 35,067 53.2 % D-Patrick Wiesner 30,752 46.7 % R-Pat Roberts 127,089 48.0 % R-D.J. Smith 15,288 5.7 % R-Milton Wolf 107,799 40.7 % R-Alvin E. Zahnter 14,164 5.3 % United States House of Representatives 001 D-James E. Sherow 8,209 65.6 % D-Bryan R. Whitney 4,293 34.3 % R-Tim Huelskamp 42,847 54.9 % R-Alan LaPolice 35,108 45.0 % United States House of Representatives 002 D-Margie Wakefield 18,337 100.0 % R-Lynn Jenkins 41,850 69.1 % R-Joshua Joel Tucker 18,680 30.8 % United States House of Representatives 003 D-Kelly Kultala 14,189 68.5 % D-Reginald (Reggie) Marselus 6,524 31.4 % R-Kevin Yoder 47,319 100.0 % United States House of Representatives 004 D-Perry L. Schuckman 11,408 100.0 % R-Mike Pompeo 43,564 62.6 % R-Todd Tiahrt 25,977 37.3 % Governor / Lt. Governor D-Paul Davis 66,357 100.0 % R-Sam Brownback 166,687 63.2 % R-Jennifer Winn 96,907 36.7 % Secretary of State D-Jean Kurtis Schodorf 59,822 100.0 % R-Kris Kobach 166,793 64.7 % R-Scott Morgan 90,680 35.2 % Attorney General D-A.J. Kotich 58,294 100.0 % R-Derek Schmidt 220,581 100.0 % State Treasurer D-Carmen Alldritt 58,570 100.0 % R-Ron Estes 220,859 100.0 % Commissioner of Insurance D-Dennis Anderson 58,590 100.0 % R-Beverly Gossage 55,306 23.0 % R-David J. -

32Nd Annual ANGUS BULL SALE Monday, March 2Nd Manhattan, KS 115 18-Month Old Bulls Sons of Ashland, Bronc, Paycheck, Resource and More GE-Epds-Ready to Work

SALUTE THE HOLTON INSIDE HOLTON, KANSAS Holton wins Hometown of Big Seven David & Jeanie wrestling Combs Holton Recorder subscribers tourney. for 15 years. RECORDERServing the Jackson County Community for 153 years See sports pages. Volume 153, Issue 13 HOLTON, KANSAS • Monday, February 17, 2020 12 Pages $1.00 Dems’ primary set for May 2 n Presidential runoff election for GOP cancelled in Kansas By Ali Holcomb receive the state’s 47 delegates. A presidential primary elec- This is the first time the KDP tion for Democrat voters will be will hold a primary election in- held in Kansas on May 2 while stead of a caucus, it was report- the state’s Republican presiden- ed. The change is to “encourage tial primary has been cancelled, greater participation and provide it has been reported. wider accessibility for voters in State primaries and caucuses an open and transparent man- are now under way across the ner,” according to the KDP. country as members of both par- During a caucus, voters gath- ties seek nominees for president er together to determine which for the Nov. 3 general election. candidates should be supported Iowa held the first caucuses by voters raising their hands or in the country on Feb. 3, and dividing into groups based on New Hampshire held its prima- the candidate they support. ries last week. In a presidential primary, vot- So far, Democrat candidate ers cast secret ballots for their Peter Buttigieg has 22 delegates, preferred candidate. followed by Bernie Sanders with A mailing explaining how to 21, Elizabeth Warren with eight, voter in person or by advance Amy Klobuchar with seven and ballot in the Kansas Demo- Joe Biden with six. -

Candidates for the 2012 General (Official)

Candidates for the 2012 General (official) * To view the candidates' information in Excel you can "right click" on the table below then "select all." Then copy the information and paste it into an Excel document. Candidate Office District Position Division Party Ballot City Running Mate Ballot City Barack Obama / Joe Biden President / Vice President 0 0 0 Democratic Chicago, IL Wilmington, DE Mitt Romney / Paul Ryan President / Vice President 0 0 0 Republican Belmont, MA Janesville, WI Gary Johnson / James P. Gray President / Vice President 0 0 0 Libertarian El Prado, NM Newport Beach, CA Chuck Baldwin / Joseph Martin President / Vice President 0 0 0 Reform Kila, MT Union Grove, NC Tim Huelskamp United States House of Representatives 1 0 0 Republican Fowler Tobias Schlingensiepen United States House of Representatives 2 0 0 Democratic Topeka Lynn Jenkins United States House of Representatives 2 0 0 Republican Topeka Dennis Hawver United States House of Representatives 2 0 0 Libertarian Ozawkie Kevin Yoder United States House of Representatives 3 0 0 Republican Overland Park Joel Balam United States House of Representatives 3 0 0 Libertarian Overland Park Robert Leon Tillman United States House of Representatives 4 0 0 Democratic Wichita Mike Pompeo United States House of Representatives 4 0 0 Republican Wichita Thomas Jefferson United States House of Representatives 4 0 0 Libertarian Wichita Steve Lukert Kansas Senate 1 0 0 Democratic Sabetha Dennis D. Pyle Kansas Senate 1 0 0 Republican Hiawatha Marci Francisco Kansas Senate 2 0 0 Democratic Lawrence Ronald B. Ellis Kansas Senate 2 0 0 Republican Meriden Tom Holland Kansas Senate 3 0 0 Democratic Baldwin City Anthony R. -

2008 General Election Official Results

Kansas Secretary of State Page 1 2008 General Election Official Vote Totals Race Candidate Votes Percent President / Vice President D-Barack Obama 514,765 41.6 % R-John McCain 699,655 56.6 % L-Bob Barr 6,706 .5 % F-Chuck Baldwin 4,148 .3 % i-Ralph Nader 10,527 .8 % Jonathan E. Allen 2 .0 % Keith Russell Judd 1 .0 % Alan Keyes 31 .0 % Cynthia A. Mcinney 35 .0 % Frank Moore 2 .0 % United States Senate D-Jim Slattery 441,399 36.4 % R-Pat Roberts 727,121 60.0 % L-Randall L. Hodgkinson 25,727 2.1 % F-Joseph L Martin 16,443 1.3 % United States House of Representatives 001 D-James Bordonaro 34,771 13.2 % R-Jerry Moran 214,549 81.8 % L-Jack Warner 5,562 2.1 % F-Kathleen M. Burton 7,145 2.7 % United States House of Representatives 002 D-Nancy E. Boyda 142,013 46.2 % R-Lynn Jenkins 155,532 50.6 % L-Robert Garrard 4,683 1.5 % F-Leslie S. Martin 5,080 1.6 % United States House of Representatives 003 D-Dennis Moore 202,541 56.4 % R-Nick Jordan 142,307 39.6 % L-Joe Bellis 10,073 2.8 % F-Roger D. Tucker 3,937 1.0 % United States House of Representatives 004 D-Donald Betts Jr. 90,706 32.3 % R-Todd Tiahrt 177,617 63.4 % L-Steven A Rosile 5,345 1.9 % F-Susan G. Ducey 6,441 2.2 % Kansas Senate 001 D-Galen Weiland 11,017 36.3 % R-Dennis D. -

Legislative Directory 84Th Kansas Legislature 2012 Regular Session

Legislative Directory 84th Kansas Legislature 2012 Regular Session Published by Kris W. Kobach Secretary of State 2012 Legislative Directory Table of Contents United States Senators ........................................................................................................ 1 United States Representatives ............................................................................................. 2 Kansas State Officers .......................................................................................................... 4 State Board of Education .................................................................................................... 6 Legislative telephone numbers and websites ...................................................................... 8 Kansas Senate By district ..................................................................................................................... 9 Officers and standing committees .............................................................................. 11 Capitol office addresses and phone numbers ............................................................. 12 Home/business contact information .......................................................................... 14 Kansas House of Representatives By district ................................................................................................................... 24 Officers and standing committees .............................................................................. 31 Capitol office -

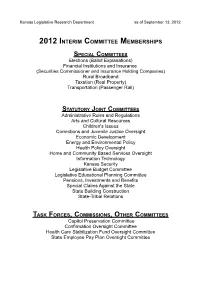

2012 Interim List

Kansas Legislative Research Department as of September 13, 2012 2012 INTERIM COMMITTEE MEMBERSHIPS SPECIAL COMMITTEES Elections (Ballot Explanations) Financial Institutions and Insurance (Securities Commissioner and Insurance Holding Companies) Rural Broadband Taxation (Real Property) Transportation (Passenger Rail) STATUTORY JOINT COMMITTEES Administrative Rules and Regulations Arts and Cultural Resources Children's Issues Corrections and Juvenile Justice Oversight Economic Development Energy and Environmental Policy Health Policy Oversight Home and Community Based Services Oversight Information Technology Kansas Security Legislative Budget Committee Legislative Educational Planning Committee Pensions, Investments and Benefits Special Claims Against the State State Building Construction State-Tribal Relations TASK FORCES, COMMISSIONS, OTHER COMMITTEES Capitol Preservation Committee Confirmation Oversight Committee Health Care Stabilization Fund Oversight Committee State Employee Pay Plan Oversight Committee SPECIAL COMMITTEES Elections Financial Institutions and Insurance Rural Broadband Taxation Transportation 2012 SPECIAL COMMITTEE ON ELECTIONS Senate House Sen. Terrie Huntington, Chairperson Rep. Scott Schwab, Vice-chairperson Sen. Pete Brungardt Rep. Randy Garber Sen. Oletha Faust-Goudeau Rep. TerriLois Gregory Sen. Carolyn McGinn Rep. Jim Howell Sen. Vicki Schmidt Rep. Ann Mah Rep. Les Osterman Rep. John Rubin Rep. Kathy Wolfe-Moore Kansas Legislative Research Department Revisor of Statutes Office Martha Dorsey Renae Jefferies Jill -

Candidates for the 2010 General (Official) Candidate Office District Position Division Party Title First Name Middle Last Name S

Candidates for the 2010 General (official) Candidate Office District Position Division Party Title First Name Middle Last Name Suffix Ballot City Running Mate Ballot City Lisa Johnston United States Senate 0 0 0 Democratic Ms. Lisa Johnston Overland Park Jerry Moran United States Senate 0 0 0 Republican Mr. Jerry Moran Hays Michael Wm. Dann United States Senate 0 0 0 Libertarian Mr. Michael Wm. Dann Baldwin City Joseph (Joe) K. Bellis United States Senate 0 0 0 Reform Mr. Joseph (Joe) K. Bellis Overland Park Alan Jilka United States House of Representatives 1 0 0 Democratic Mr. Alan Jilka Salina Tim Huelskamp United States House of Representatives 1 0 0 Republican Mr. Tim Huelskamp Fowler Jack Warner United States House of Representatives 1 0 0 Libertarian Mr. Jack Warner Wright Cheryl Hudspeth United States House of Representatives 2 0 0 Democratic Ms. Cheryl Hudspeth Girard Lynn Jenkins United States House of Representatives 2 0 0 Republican Ms. Lynn Jenkins Topeka Robert Garrard United States House of Representatives 2 0 0 Libertarian Mr. Robert Garrard Edgerton Stephene Moore United States House of Representatives 3 0 0 Democratic Mrs. Stephene Moore Lenexa Kevin Yoder United States House of Representatives 3 0 0 Republican Mr. Kevin Yoder Overland Park Jasmin Talbert United States House of Representatives 3 0 0 Libertarian Ms. Jasmin Talbert Kansas City Raj Goyle United States House of Representatives 4 0 0 Democratic Mr. Raj Goyle Wichita Mike Pompeo United States House of Representatives 4 0 0 Republican Mr. Mike Pompeo Wichita Shawn Smith United States House of Representatives 4 0 0 Libertarian Mr. -

Union Pacific Corporate Political Contributions to Candidates

Union Pacific Corporate Political Contributions to Candidates, Committees, Political Organizations and Ballot Measures for 2012 Committee State Candidate Name Committee Name Amount Committee Party Committee Office Committee District AR Allen, Fred Fred Allen Campaign Committee $1,000.00 D STATE HOUSE 33 AR Altes, Robert Robert Dennis Altes Campaign Committee $100.00 R STATE HOUSE 76 AR Barnett, Jonathan Jonathan Barnett Campaign Committee $100.00 R STATE HOUSE 87 AR Barnett, Jonathan Jonathan Barnett Campaign Committee $500.00 R STATE HOUSE 87 AR Biviano, Mark Mark Biviano for State Representative $100.00 R STATE HOUSE 46 AR Branscum, David David Branscum Campaign Committee $100.00 R STATE HOUSE 83 AR Broadaway, Mary Mary Broadaway for State Representative $100.00 D STATE HOUSE 57 AR Burris, John John Burris Campaign Committee $100.00 R STATE HOUSE 98 AR Caldwell, Ronald Ronald Caldwell for State Senate $1,000.00 R STATE SENATE 23 AR Carter, Davy Committee to Elect Davy Carter $100.00 R STATE HOUSE 43 AR Catlett, John John Catlett Campaign Committee $100.00 D STATE HOUSE 73 AR Chesterfield, Linda Linda Chesterfield Senate Campaign Committee $500.00 D STATE SENATE 30 AR Chesterfield, Linda Linda Chesterfield Senate Campaign Committee $1,000.00 D STATE SENATE 30 AR Clemmer, Ann Ann Clemmer Campaign Committee $100.00 R STATE HOUSE 23 AR Copenhaver, Harold Harold Copenhaver for State Representative $100.00 D STATE HOUSE 58 AR Cozart, Bruce Bruce Cozart Campaign Committee $100.00 R STATE HOUSE 24 AR Dale, Robert Robert E. Dale Campaign Committee -

Legislative Directory 84Th Kansas Legislature 2011 Regular Session

Legislative Directory 84th Kansas Legislature 2011 Regular Session Published by Kris W. Kobach Secretary of State 2011 Legislative Directory Table of Contents United States Senators ....................................................................................................... 1 United States Representatives ............................................................................................ 2 Kansas State Officers.......................................................................................................... 4 State Board of Education .................................................................................................... 6 Legislative telephone numbers and Web sites ................................................................... 8 Kansas Senate By district .................................................................................................................... 9 Officers and standing committees ............................................................................. 11 Capitol office addresses and phone numbers ............................................................ 12 Home/business contact information .......................................................................... 14 Kansas House of Representatives By district .................................................................................................................. 24 Officers and standing committees ............................................................................. 31 Capitol office addresses -

Candidate Ballot City Office District Tim Huelskamp Fowler United

Candidates for the 2012 Primary (OFFICIAL) Candidate Ballot City Office District Tim Huelskamp Fowler United States House of Representatives 1 Scott Barnhart Ottawa United States House of Representatives 2 Robert V. Eye Lawrence United States House of Representatives 2 Tobias Schlingensiepen Topeka United States House of Representatives 2 Lynn Jenkins Topeka United States House of Representatives 2 Kevin Yoder Overland Park United States House of Representatives 3 Esau A. Freeman Wichita United States House of Representatives 4 Robert Leon Tillman Wichita United States House of Representatives 4 Mike Pompeo Wichita United States House of Representatives 4 Steve Lukert Sabetha Kansas Senate 1 Marje A. Cochren Whiting Kansas Senate 1 Dennis D. Pyle Hiawatha Kansas Senate 1 Marci Francisco Lawrence Kansas Senate 2 Ronald B. Ellis Meriden Kansas Senate 2 Jeremy Ryan Pierce Lawrence Kansas Senate 2 Tom Holland Baldwin City Kansas Senate 3 Anthony R. Brown Eudora Kansas Senate 3 James C. "J.C." Tellefson Leavenworth Kansas Senate 3 David Haley Kansas City Kansas Senate 4 Joe Ward Kansas City Kansas Senate 4 Kelly Kultala Kansas City Kansas Senate 5 Steve Fitzgerald Leavenworth Kansas Senate 5 Mark S. Gilstrap Piper Kansas Senate 5 (Vincent) Mario Escobar Kansas City Kansas Senate 6 Pat Pettey Kansas City Kansas Senate 6 Chris Steineger Kansas City Kansas Senate 6 Kyle Russell Roeland Park Kansas Senate 7 David Harvey Mission Hills Kansas Senate 7 Kay Wolf Prairie Village Kansas Senate 7 Lisa Johnston Overland Park Kansas Senate 8 Jim Denning Overland Park Kansas Senate 8 Thomas C. (Tim) Owens Overland Park Kansas Senate 8 Merlin D. -

Sample Ballots: 2010 Primary Election

Official DEMOCRATIC Ballot-Primary Election 1/1 A State of KansasB Douglas CountyC August 3, 2010 Instructions to Voter STATE OFFICES GOVERNOR AND LIEUTENANT GOVERNOR Vote for One Pair To vote you must darken the Tom Holland oval completely. Baldwin City Kelly Kultala Use black or blue ball point Kansas City pen only. SECRETARY OF STATE To vote for persons for governor Vote for One and lieutenant governor whose Chris Biggs names are printed on the ballot, Junction City darken the oval to the left of the names of the persons running Chris Steineger together for such offices. Kansas City ATTORNEY GENERAL To vote for a person (except for Vote for One governor and lieutenant governor) Steve Six whose name is printed on the ballot Lawrence darken the oval at the left of the person's name. STATE TREASURER Vote for One Dennis McKinney Greensburg COMMISSIONER OF To vote for a person whose name INSURANCE is not printed on the ballot, write the Vote for One person's name in the blank space provided and darken the oval to the left. or write-in STATE REPRESENTATIVE 46th DISTRICT Notice: If you tear, deface or Vote for One make a mistake and wrongfully mark any ballot, Paul Davis you must return it to the Lawrence election board and receive a STATE BOARD OF new ballot or set of ballots. EDUCATION MEMBER 1st DISTRICT Vote for One NATIONAL OFFICES Janet Waugh Kansas City UNITED STATES SENATOR COUNTY OFFICES Vote for One David Haley COUNTY COMMISSIONER Kansas City 1st DISTRICT Vote for One Lisa Johnston Mike Gaughan Overland Park Lawrence PRECINCT COMMITTEEMAN Charles Vote for One Schollenberger Prairie Village Paul Jefferson Lawrence Patrick Wiesner Lawrence or write-in Robert A. -

Journal of the Senate

1140 JOURNAL OF THE SENATE Journal of the Senate FIRST DAY SENATE CHAMBER, TOPEKA, KANSAS Monday, January 13, 2020, 2:00 p.m. In accordance with the provisions of the Constitution of the State of Kansas and by the virtue of her office as President of the Senate, President Susan Wagle declared the 2020 Senate to be in session. President Wagle welcomed Reverend Cecil T. Washington, who will again serve as the Senate Chaplain. Reverend Washington delivered the invocation: Gracious Father and God of all mercies, once again, we thank You for Your faithfulness. We thank You for the summer break, for safe travel and for a new opportunity to serve. Lord, what we need as we begin this new session, in this new year and in this new decade, is a new fresh awareness of Your presence. You said in Lamentations 3:22-23, that Your love and mercies are new every day; as fresh as the morning and as sure as the sunrise. So Lord, let all that we do in this new season of serving be a reflection of Your precious renewed guidance. Now, having faith in Your unfailing support, I thank You in the Name of Jesus for how You’re going to bless this new session. Amen and Amen The Pledge of Allegiance was led by President Wagle. President Wagle introduced Heidi Farnsworth, who will serve as Reading Clerk for the 2020 Session. The roll was called with 39 senators present. Senator Suellentrop was excused. District District 1. Dennis Pyle 21. Dinah H. Sykes 2.