Audit Report on the Accounts of District Government Charsadda Audit Year 2017-18 Auditor General of Pakistan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Road ID Division Road Name Pavementtype Avg Right of Way

Road ID Division Road Name PavementType Avg Right of Way BT Width Shoulder Type ShoulderWidth Length in KM Executive Peshawar-Charsadda-Mardan-Swabi-Topi 1 Center Road(Peshawar,Charsadda Road (Dual carriage Asphalt Concrete 21.3-45.7 7.30 Gravel 2 29.10 PKHA Way)) Peshawar-Charsadda-Mardan-Swabi-Topi 2 Center Asphalt Concrete 21.3-45.7 7.30 Gravel 2 27.00 PKHA Road(Charsadda , Mardan Road) Peshawar-Charsadda-Mardan-Swabi-Topi 3 Center Asphalt Concrete 21.3-45.7 9.40 Gravel 2 69.30 PKHA Road(Mardan, Swabi Road) Peshawar-Charsadda-Mardan-Swabi-Topi Road(Baja 4 Center Asphalt Concrete 18.2 7.30 Gravel 2 3.50 PKHA By pass) Naguman- Shabqadar- Pir Qilla Road(Naguman - 5 Center Asphalt Concrete 7.30 Gravel 2.5 5.00 PKHA shabqadar -pirqilla) Naguman- Shabqadar- Pir Qilla Road(Naguman - 6 Center Asphalt Concrete 7.30 Gravel 2.5 12.00 PKHA shabqadar -pirqilla) Mardan Eastern &Western Bypass Road(Eastern By 7 Center Asphalt Concrete 30.47 7.30 Gravel 2 17.00 PKHA pass) Mardan Eastern &Western Bypass Road(Western 8 Center Asphalt Concrete 46 7.30 Gravel 2 16.00 PKHA Bypass) Timergara-Munda-Khar-Nawagai-Ghallanai-Pir Qilla- 9 Center Peshawar Road(Peshawar to Pir Balla (Dual Carriage Asphalt Concrete 15.24-21.3 7.30 Gravel 2 6.60 PKHA Way)) Timergara-Munda-Khar-Nawagai-Ghallanai-Pir Qilla- 10 Center Asphalt Concrete 15.24-21.3 6.10 Gravel 2 24.90 PKHA Peshawar Road(Pir Balla to Pir Qilla) Timergara-Munda-Khar-Nawagai-Ghallanai-Pir Qilla- 11 Center Asphalt Concrete 15.24-21.3 7.30 Gravel 2 5.50 PKHA Peshawar Road(Pir Qilla to Yakka Ghund) Swabi-Jehangira-Khairabad-Nizampur-Khushalgarh -

![[Khyber Pakhtunkhwa] Highways Ordinance, 1959](https://docslib.b-cdn.net/cover/3014/khyber-pakhtunkhwa-highways-ordinance-1959-423014.webp)

[Khyber Pakhtunkhwa] Highways Ordinance, 1959

1 | P a g e THE 1[KHYBER PAKHTUNKHWA] HIGHWAYS ORDINANCE, 1959. CONTENTS Preamble. Sections. CHAPTER-I PRELIMINARY 1. Short title and extent. 2. Definitions. CHAPTER-II HIGHWAY AUTHORITIES 3. Highway Authorities. 4. Transfer of control from one Highway Authority to another. CHAPTER-III POWERS OF HIGHWAY AUTHORITIES 5. General power of Highway Authorities. 6. Encroachments. 7. Certain works on highways. 8. Restrictions on ribbon development on certain highways. 9. Adoption of restrictions of section 8 in respect of other highways. 10. Compensation. 1. For the words “West Pakistan” the words “North-West Frontier Province”, Subs. by Khyber Pakhtunkhwa OrdNo.X of 1984 and then Subs vide Khyber Pakhtunkhwa Act No.IV of 2011. 2 | P a g e 11. Construction of access to road buildings on areas subject to restrictions under section 8 or section 9. 12. Temporary closure of highways. 13. Permanent closure of highways. 14. Interference or damage resulting from works on highways. 15. Regulation of classes or vehicles of animals using a highway. CHAPTER-IV IMPROVEMENT OF HIGHWAYS 16. Determination of building line. 17. Construction of buildings, etc., between highway and building line. 18. Acquisition of land. CHAPTER-V DUTIES OF HIGHWAYS USERS 19. Conformity with rules, signs and directions of officer regulating traffic. 20. Vehicles and animals to be stopped in certain cases. 21. Driving of vehicles and animals. 22. Adequate control and care of vehicles and animals. 23. Power to arrest without warrant. CHAPTER-VI PROCEDURE AND PENALTIES 24. Cognizance of offences. 25. Penalties. 3 | P a g e CHAPTER-VII MISCELLANEOUS PROVISIONS 26. -

F Government of Khyber Pakhtunkhwa

GOVERNMENT OF KHYBER PAKHTUNKHWA COMMUNICATION & WORKS DEPARTMENT No. SOR/V-39/W&S/03/Vol-II Dated: 25/05/2021 To, The Chief Engineer (Centre), Communication & Works, Peshawar. SUBJECT: 2ND REVISED ADMINISTRATIVE APPROVAL FOR THE SCHEME "CONSTRUCTION OF TECHNICALLY & ECONOMICALLY FEASIBLE 198 KM ROADS IN PESHAWAR DIVISION" ADP NO.1702/200247 (2020-21). In exercise of the powers delegated vide Part-I Serial No.5 Second Schedule of the Delegation of Powers under the Financial Rules and Powers of Re-appropriation Rules, 2018, the Khyber Pakhtunkhwa Provincial Government is pleased to accord the 2" Revised Administrative Approval for the implementation of the scheme under ADP NO.1702/200247 (2020-21)"Construction of Technically & Economically Feasible 198 KM Roads in Peshawar Division" ADP No.1702/200247 (2020-21)for the period of 26 months from (2020-21) to (2022-23) at a total cost of Rs. 4456.033 million (four thousand four hundred fifty six and thirty three thousand) as per detail given below: S.No. Name of work Total Cost (Rs in M) District Charsadda A Construction / Improvement and Widening of Road from Hassanzai to Munda Head (I) Works and Matta Mughal Khel via Katozai of Road from Shabqadar Chowk to Battagram, From Sokhta to Kotak and Dalazaak Bypass Dalazak Village District Charsadda 1 Construction/improvement and widening of Hassanzai road 3.00 km 69.92 2 Construction/Improvement and Widening of road from Shabqadar Chowk Battagram road (3.70km) 80.00 3 Advertisement charges 0.08 Total 150.00 (II) Construction / Improvement and -

FATA and Khyber Pakhtunkhwa

Nutrition Presence of Partners - F.A.T.A. and Khyber Pakhtunkhwa 29 November 2010 Legend CHITRAL Provincial Boundar Kalam Utror District Boundary Number of Implementing Partners KOHISTAN Balakot 1 2 SWAT Mankyal UPPER DIR Bahrain 3 Gowalairaj Madyan PESHAWAR Beshigram Beha Sakhra Bar Thana Fatehpur Gail Maidan Zaimdara Asharay Darangal Baidara Bishgram ShawarChuprial Miskana Shalpin Urban-4 Lal Qila Tall Arkot Shahpur Usterzai Samar Bagh Lijbook Jano/chamtalai Muhammad Zai Mayar Kala Kalay Alpuri Kuz Kana Urban-3 Koto Pir Kalay Munjai Shah DehraiDewlai Urban-5 Mian Kili Balambat Bara Bandai SHANGLADherai Opal Rabat Totano Bandai Kech Banda Togh Bala Munda QalaKhazanaBandagai HazaraKanaju Malik Khel Chakesar Urban-6 Kotigram Asbanr Puran Ganjiano Kalli Raisan Shah Pur Bahadar Kot 1 LOWER DIRMc Timargara Koz Abakhel Kabal BATAGRAM Khanpur Billitang Ziarat Talash Aloch HANGU Ouch Kokarai Kharmatu Bagh Dush Khel Chakdara Islampur Kotki KOHAT Khadagzai AbazaiBadwan Sori Chagharzai Gul BandaiBehlool Khail Kota Dhoda Daggar Batara MALAKAND Pandher Rega MANSEHRA BUNER Krapa Gagra Norezai KARAK MARDAN CHARSADDA Kangra Rajjar IiShakho KYBER PAKHTUNKHWA Hisar Yasinzai Dosahra Nisatta Dheri Zardad SWABI ABBOTTABAD Mohib Banda ChowkaiAman Kot M.c Pabbi HARIPUR PESHAWAR NOWSHERA Shah Kot Usterzai Urban-4 Kech Banda Urban-6Togh Bala Raisan Khan Bari Shah Pur Kotki KharmatuBillitang KOHAT HANGU Dhoda Muhammad Khawja This map illustrates the presence of organisations working in the sector of Nutrition in Khyber Pakhtunkhwa and FATA as reported by relief -

Pdf | 497.71 Kb

LOWER INITIAL DAMAGE ASSESSMENT FOR DIR MONSOON FLOOD - 2010 SWAT BAJAUR C h i n a Malakand FANA KHYBER BUNER PAKHTUNKHWA MALAKAND Dargai Afghanistan FATA Kharki Kohi Bermol Qasmi PUNJAB Alo MOHMAND Mian Issa Babozai BALOCHISTAN Koz Behram Dheri II n n d d i i a a Shergarh Makori II r r a a n n Dherai Likpani Shamozai Bazar Hathian SINDH Lund Khawar Show Dag Gandera Hari Chand Palo Dheri Katlang-1 Pir Saddo Jalala Kati Garhi Sawal Dher 1 Parkho Arabian Sea Mandani Dherai Katlang-2 Ghalanai Abazai Rustam Sawal Dher 2 Kata Khat Hisara Nehri Madey Baba Tangi Jamal Garhi MARDAN Chargalli Legend Katuzai Takkar Kot Jungarah Dakki Machi Matta Gujrat Daman-e-koh Fathma Bakhshali WFP Assisted Camp Affected HH (%) Mughal CHARSADA Ziam Khel Sher Pao Narai Pat Baba Garyala Humanitarian Hub 7% - 15% Chindro Dag Seri Bahlol Bala Mirzadher Jehangir Abad Garhi Mira Umarzai Behlola Babini Shahbaz Garhi Early Recovery Delivery Point 16% - 30% Hassan Saro Shah Panjpad Batgram Umar Zai Sarki Titara Gujar Garhi Sange Zai Marmar Baghicha Mohib CP Distribution Point 31% - 60% Tarnab Khan Mahi Baghdada Kot Daulatzai Dheri Shabqadar Turang Zai Muhammad Chamtar Par Hoti Banda Kangra Daulatpura Nari Khazana Mardan Sikandari Koroona Humanitarian Logistics Base 61% - 80% Rashkai Mardan Rural Garhi Daulatzai Utmanzai Manga Dheri Bijli Ghar Bari Cham Chak Hoti Hissara Razar-II Muslimabad Dargai Hoti Garhi Ismailzai Major Town 81% - 100% Jogani Yasinzai Bagh-e-iram Haji Zai Mayar Razar-I Ghunda Rorya Shamatpur Karkana Guli Bagh Highway UC Boundary Anam Khatki Charsadda -

PAK102 Revision 2 for Approval 16September 2010

SECRETARIAT 150 route de Ferney, P.O. Box 2100, 1211 Geneva 2, Switzerland TEL: +41 22 791 6033 FAX: +41 22 791 6506 www .actalliance.org Appeal Pakistan Pakistan Floods Emergency (PAK102) – Rev. 2 Appeal Target: US$ 12,441,347 Balance Requested: US$ 6,478,821 Geneva, 17 September 2010 Dear colleagues, Since 21 July 2010, heavy monsoon rains have led to the worst flooding in Pakistan’s history. Please see the ACT website ( www.actalliance.org/resources/alertsandsitreps ) for the latest ACT Situation Reports from Pakistan on this fast changing emergency. The members of the ACT Pakistan Forum, Church World Service- Pakistan/Afghanistan (CWS-P/A), Norwegian Church Aid (NCA), and Diakonie Katastrophenhilfe (DKH) continue to distribute urgent relief assistance to the flood-affected communities with the financial, material aid and personnel support of many international ACT members, their national constituencies and institutional donors, as well as other supporters from around the world. This ACT appeal was first issued on 4 August and then replaced by a revised version issued on 11 August to include the proposed responses of DKH and NCA, as well as a scaled-up version of the CWS-P/A programme. This second revision of the appeal significantly scales-up the entire proposed programme from a previous funding target of US $4,101,731 to US$ 12,441,347. CWS P/A is increasing the number of operational areas to include Sukkur and Thatta Districts in Sindh Province and Muzaffargarh District in Punjab Province. CWS P/A is now working with an additional partner – the Church of Pakistan (CoP) Diocese of Raiwind. -

Technical Assistance Layout with Instructions

Initial Environmental Examination December 2014 PAK: Pakistan Power Transmission Enhancement Program Tranche-IV (220 kV Chakdarra Grid Station and Allied Transmission Line) Prepared by Environment and Social Impact Cell (ESIC), NTDC for the Asian Development Bank. 220 kV Chakdarra Grid Station and Allied Transmission Line IEE TABLE OF CONTENTS EXECUTIVE SUMMARY i 1. INTRODUCTION 1 1.1 Overview 1 1.2 Background 1 1.3 Scope of the IEE Study and Personnel 2 2. POLICY LEGAL AND ADMINISTRATIVE FRAMEWORK 4 2.1 Statutory Framework 4 2.1.1 Pakistan Environmental Protection Act, 1997 4 2.1.2 Pakistan Environmental Protection Agency Review of IEE and EIA Regulations, 2000 4 2.1.3 National Environmental Quality Standards (NEQS) 6 2.1.4 Other Relevant Laws 6 2.2 Structure of Report 6 3. DESCRIPTION OF THE PROJECT 8 3.1 Type of Project 8 3.2 Categorization of the Project 8 3.3 Need for the Project 8 3.4 Location and Scale of Project 9 3.5 Analysis of Alternatives 11 3.5.1 Do Nothing Scenario 11 3.5.2 Alternative Construction Methods 11 3.5.3 Alternative Geometry 11 3.6 Proposed Schedule for Implementation 11 3.7 Construction Material 11 4. DESCRIPTION OF ENVIRONMENTAL AND SOCIAL BASELINE CONDITIONS 13 4.1 Project Area 13 4.1.1 General Characteristics of Project Area 13 4.1.2 Affected Administrative Units 13 4.2 Physical Resources 13 4.2.1 Topography, Geography, Geology, and Soils 13 4.2.2 Climate, Temperature and Rainfall 14 4.2.3 Groundwater and Water Supply 15 4.2.4 Surface Water 15 i 220 kV Chakdarra Grid Station and Allied Transmission Line IEE 4.2.5 Air Quality 16 4.2.6 Noise 16 4.3 Biological Resources 16 4.3.1 Wildlife, Fisheries and Aquatic Biology 16 4.3.2 Terrestrial Habitats, Forests and Protected Species 17 4.3.3 Protected areas / National Sanctuaries 17 4.4 Economic Development 17 4.4.1 Agriculture, Livestock and Industries 17 4.4.2 Energy Sources 18 4.5 Social and Cultural Resources 18 4.5.1 Population Communities and Employment 18 4.5.2 Education and Literacy 19 4.5.3 Cultural Heritage and Community Structure 19 5. -

List of Unclaimed Dividends and Shares

Ferozsons Laboratories Limited List of Unclaimed Dividend & Bonus Amount of No. of Unclaimed S.No Folio Name Address CNIC Unclaimed Dividend Shares (Rupees) 1 0005 Mr. Abdul Hamid Khan C/O Ferozsons Limited 60 The Mall, Lahore. 00000-0000000-0 499 117,337 2 0011 Mr. Mohammad Javid Khan, Pak International Printers 118 - G. T. Road Lahore. 00000-0000000-0 8 3,806 3 0012 Begum Abdul Majid Khan C/O Pakistan International Printers,118-G.T.Road, Lahore. 00000-0000000-0 718 308,023 4 0017 Miss Kaukab Sadiq 64 / E - 1, Gulberg - III Lahore. 00000-0000000-0 1724 301,856 5 0019 Imtiaz Begum Sahiba 64 / E - 1, Gulberg - III Lahore. 00000-0000000-0 143 24,882 6 0028 Mr. Abdul Razzaq H.No.815,St.64, G-9/4 Islamabad 00000-0000000-0 902 156,010 7 0035 Mr. Shams-ul-Hassan Khawaja Pharmaceutical Section Ministry of Health Al-Riyadh 00000-0000000-0 236 40,960 8 0043 Mrs. Shujaat Parveen Vill: & P. O.Toru Mardan. 00000-0000000-0 1056 1,292,201 9 0050 Mrs. Khawar Kazi L - 102, D. H. A. Lahore Cantt. 35201-8757810-4 0 2,029 10 0059 Mr. Tahir Ali Khan H.No.280,St.38, G-9/1, Islamabad 00000-0000000-0 4423 759,766 11 0060 Mr. Abdul Qadir Khan Retd.Veterinary Doctor Kacha Gojra Faisalabad. 00000-0000000-0 1874 323,753 12 0063 Mr. Said Ahmed Shah House # 64 Biket Ganj Street Mardan. 00000-0000000-0 210 318,085 13 0065 Dr. Mrs. Farrakh Iqbal A-572 Block 5, Gulshan-e-Iqbal, Karachi 75300 42201-5619562-0 0 11,332 14 0066 Mr. -

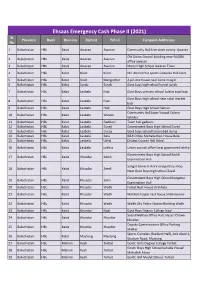

UPDATED CAMPSITES LIST for EECP PHASE-2.Xlsx

Ehsaas Emergency Cash Phase II (2021) Sr. Province Bank Division Distrcit Tehsil Campsite Addresses No. 1 Balochistan HBL Kalat Awaran Awaran Community Hall Live stock colony Awaran Old Union Council building near NADRA 2 Balochistan HBL Kalat Awaran Awaran office awaran 3 Balochistan HBL Kalat Awaran Awaran Model High School Awaran Town 4 Balochistan HBL Kalat Kalat Kalat Mir Ahmed Yar sports Complex Hall kalat 5 Balochistan HBL Kalat Kalat Mangochar A private house near Jame masjid 6 Balochistan HBL Kalat Surab Surab Govt boys high school hostel surab 7 Balochistan HBL Kalat Lasbela Hub Govt Boys primary school Adalat road hub Govt Boys high school near sabzi market 8 Balochistan HBL Kalat Lasbela Hub hub 9 Balochistan HBL Kalat Lasbela Hub Govt Boys High School Sakran Community Hall Jaam Yousuf Colony 10 Balochistan HBL Kalat Lasbela Winder Winder 11 Balochistan HBL Kalat Lasbela Gaddani Town hall gaddani 12 Balochistan HBL Kalat Lasbela Dureji Government Boys High School Dureji 13 Balochistan HBL Kalat Lasbela Dureji Govt boys school hasanabad dureji 14 Balochistan HBL Kalat Lasbela Bela B&R Office Mohalla Rest House Bela 15 Balochistan HBL Kalat Lasbela Uthal District Council Hall Uthal 16 Balochistan HBL Kalat Lasbela Lakhra Union council office local goverment lakhra Government Boys High School Karkh 17 Balochistan HBL Kalat Khuzdar Karkh Examination Hall Sangat General store and poltary shop 18 Balochistan HBL Kalat Khuzdar Zeedi Near Govt Boys high school Zeedi Government Boys High School Norgama 19 Balochistan HBL Kalat Khuzdar Zehri Examination Hall 20 Balochistan HBL Kalat Khuzdar Wadh Forest Rest House Drakhala 21 Balochistan HBL Kalat Khuzdar Wadh Mohbat Faqeer rest house Shahnoorani 22 Balochistan HBL Kalat Khuzdar Wadh Wadh City Police Station Building Wadh 23 Balochistan HBL Kalat Khuzdar Naal Govt Boys Degree College Naal Social Welfare Office Hall, Hazari Chowk 24 Balochistan HBL Kalat Khuzdar Khuzdar khuzdar. -

(TENDER ENQUIRIES).Docaaaaa

C:\Users\TAHIR~1.BAI\AppData\Local\Temp\notesD3FF90\16 (TENDER ENQUIRIES).docAAAAA Ref: DEV/PSR/TENDER/16-CHD/122020 Date: 03.11.2020 GENERAL MANAGER (IT/MIS) Sui Northern Gas Pipelines Limited Head Office Lahore FAX NO. 091-9217758 INVITATION TO BID (DITCHING, BACKFILLING, WELDING JOINTS, TRANSPORTATION & ALLIED SERVICES FOR LAYING OF (MS & PE) PIPELINES AT VARIOUS VILLAGES / LOCALITIES OF (NA-23) & (NA-24) DIST: CHARSADDA (JOB NOS. 21/35/011325, 21/35/011425, 21/35/011525, 21/35/011625, 21/35/011725, 21/35/011825, 21/35/011925, 21/35/012025) TENDER ENQUIRY# DEV/PSR/TENDER/16-CHD/122020 Dear Sir, 1. Sui Northern Gas Pipelines Limited, a Gas Transmission & Distribution Company, invites sealed bids from the original Pre-Qualified contractors of Peshawar Region. The Pre-Qualified contractors desirous of quoting for above tenders are required to provide a copy of valid NTN / Income Tax Certificate, KPRA Certificate and latest professional tax certificate along with their request for purchase of tender documents. SUB ITEM NO. BRIEF DESCRIPTION QTY.(METERS) ITEM NO. Ditching, Backfilling & Allied Services for Laying of MS Pipelines at Various Localities of (NA-23) Dist: Charsadda i) (Attaki Kallay Shabqadar) (PORTION – I) 4” Φ x 1152 Mtrs Item-I (Job No. 21/35/011325) 2” Φ x 3000 Mtrs Transportation of MS Pipelines from Regional Store Peshawar to respective sites in 1” Φ x 2748 Mtrs Various Localities of (NA-23) Dist: Charsadda ii) (Attaki Kallay Shabqadar) (PORTION – I) (Job No. 21/35/011325) Ditching, Backfilling & Allied Services for Laying of MS Pipelines at Various Localities of (NA-23) Dist: Charsadda i) (Attaki Kallay Shabqadar) (PORTION – II) 4” Φ x 1152 Mtrs Item-II (Job No. -

ADP 2021-22 Planning and Development Department, Govt of Khyber Pakhtunkhwa Page 1 of 446 NEW PROGRAMME

ONGOING PROGRAMME SECTOR : Agriculture SUB-SECTOR : Agriculture Extension 1.KP (Rs. In Million) Allocation for 2021-22 Code, Name of the Scheme, Cost TF ADP (Status) with forum and Exp. upto Beyond S.#. Local June 21 2021-22 date of last approval Local Foreign Foreign Cap. Rev. Total 1 170071 - Improvement of Govt Seed 288.052 0.000 230.220 23.615 34.217 57.832 0.000 0.000 Production Units in Khyber Pakhtunkhwa. (A) /PDWP /30-11-2017 2 180406 - Strengthening & Improvement of 60.000 0.000 41.457 8.306 10.237 18.543 0.000 0.000 Existing Govt Fruit Nursery Farms (A) /DDWP /01-01-2019 3 180407 - Provision of Offices for newly 172.866 0.000 80.000 25.000 5.296 30.296 0.000 62.570 created Directorates and repair of ATI building damaged through terrorist attack. (A) /PDWP /28-05-2021 4 190097 - Wheat Productivity Enhancement 929.299 0.000 378.000 0.000 108.000 108.000 0.000 443.299 Project in Khyber Pakhtunkhwa (Provincial Share-PM's Agriculture Emergency Program). (A) /ECNEC /29-08-2019 5 190099 - Productivity Enhancement of 173.270 0.000 98.000 0.000 36.000 36.000 0.000 39.270 Rice in the Potential Areas of Khyber Pakhtunkhwa (Provincial Share-PM's Agriculture Emergency Program). (A) /ECNEC /29-08-2019 6 190100 - National Oil Seed Crops 305.228 0.000 113.000 0.000 52.075 52.075 0.000 140.153 Enhancement Programme in Khyber Pakhtunkhwa (Provincial Share-PM's Agriculture Emergency Program). -

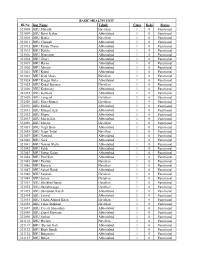

Class Beds Status 321008 BHU Mujaith Havelian 1 0 Functional

BASIC HEALTH UNIT S.NoID.No Inst Name Tehsil/ Class Beds Status 321008 BHU Mujaith Havelian 1 0 Functional 321009 BHU Berot Kalan Abbottabad 1 0 Functional 321010 BHU Bodla Havelian 1 0 Functional 321011 BHU Chamali Abbottabad 1 0 Functional 321012 BHU Pando Thana Abbottabad 1 0 Functional 321013 BHU Dalola Abbottabad 1 0 Functional 321016 BHU Dhamtour Abbottabad 1 0 Functional 321018 BHU Ghori Abbottabad 1 0 Functional 321019 BHU Harno Abbottabad 1 0 Functional 321020 BHU Jabrain Abbottabad 1 0 Functional 321021 BHU Kakul Abbottabad 1 0 Functional 321023 BHU Kalu Maire Havelian 1 0 Functional 321024 BHU Kangar Bala Abbottabad 1 0 Functional 321025 BHU Kokal Barseen Havelian 1 0 Functional 321026 BHU Kokmang Abbottabad 1 0 Functional 321027 BHU Kothiala Abbottabad 1 0 Functional 321028 BHU Langrial Havelian 1 0 Functional 321029 BHU Mera Rumal Havelian 1 0 Functional 321030 BHU Malkot Abbottabad 1 0 Functional 321031 BHU Mangal Azir Abbottabad 1 0 Functional 321032 BHU Mipur Abbottabad 1 0 Functional 321033 BHU Mochi Kot Abbottabad 1 0 Functional 321036 BHU Moolia Havelian 1 0 Functional 321037 BHU Nagri Bala Abbottabad 1 0 Functional 321038 BHU Nagri Totial Havelian 1 0 Functional 321039 BHU Nammal Abbottabad 1 0 Functional 321040 BHU Nara Abbottabad 1 0 Functional 321041 BHU Nawan Shehr Abbottabad 1 0 Functional 321042 BHU Palak Abbottabad 1 0 Functional 321043 BHU Pattan Kalan Abbottabad 1 0 Functional 321044 BHU Phal Kot Abbottabad 1 0 Functional 321045 BHU Phallah Havelian 1 0 Functional 321046 BHU Rajoyia Havelian 1 0 Functional