Wolverhampton City Council OPEN EXECUTIVE DECISION ITEM (AMBER)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

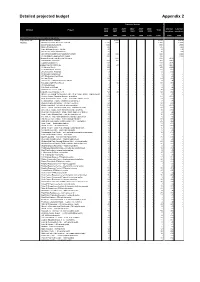

Detailed Projected Budget Appendix 2

Detailed projected budget Appendix 2 Projected budget 2019- 2020- 2021- 2022- 2023- 2024- Internal External Division Project Total 2020 2021 2022 2023 2024 2025 resources resources £000 £000 £000 £000 £000 £000 £000 £000 £000 General Revenue Account capital programme City Assets and Disabled Facilities Grants - 2,215 - - - - 2,215 - (2,215) Housing Mandatory Disabled Facilities Grants 1,500 800 - - - - 2,300 - (2,300) Small Adaptations Grants 800 - - - - - 800 - (800) Stair Lift Maintenance 25 - - - - - 25 - (25) Care & Repair Fees re: DFG's 70 - - - - - 70 - (70) Social Care Minor Adaptations 30 - - - - - 30 - (30) Discretionary Bathrooms Adaptations Grant 50 450 - - - - 500 - (500) Rehabilitation Equipment 2019-2020 165 - - - - - 165 - (165) Housing General Fund General Schemes - 215 - - - - 215 (215) - Small Works Assistance 160 182 - - - - 342 (342) - Capitalised Salaries 118 - - - - - 118 (118) - Empty Properties Strategy 69 178 - - - - 247 (247) - 19 Chester Street 100 - - - - - 100 (100) - 14 Selwyn Road, Bilston 60 - - - - - 60 (60) - 29 Lime Street, Penfields 13 - - - - - 13 (13) - 99 Milfields Road Bilston 5 - - - - - 5 (5) - 473 Birmingham New Road 3 - - - - - 3 (3) - 14 Lane Road 69 - - - - - 69 (69) - Land between 44 and 48 Showell Road 4 - - - - - 4 (4) - Two and a half Clifford Street - 80 - - - - 80 (80) - 30 Victoria Road 2 - - - - - 2 (2) - 182 Castlecroft Road 4 - - - - - 4 (4) - All Saints Development Fees 35 - - - - - 35 (35) - Corporate Asset Management 62 20 - - - - 82 (82) - Graiseley Learning Technology Centre -

The Case for a New Hertfordshire Village WELWYN HATFIELD BOROUGH COUNCIL LOCAL PLAN CONSULTATION 23 JANUARY- 19 MARCH 2015 CONTENTS

The Case for a new Hertfordshire Village WELWYN HATFIELD BOROUGH COUNCIL LOCAL PLAN CONSULTATION 23 JANUARY- 19 MARCH 2015 CONTENTS INTRODUCTION: THE ENGLISH VILLAGE 4 SECTION 1: THE HISTORY AND EVOLUTION OF THE ENGLISH VILLAGE 6 SECTION 2: THE IDEALISATION OF THE ENGLISH VILLAGE 13 SECTION 3: PLANNING POLICY AND THE ENGLISH VILLAGE 17 APPENDIX 1: HERTFORDSHIRE VILLAGES TODAY 28 APPENDIX 2: ENGLISH MODEL VILLAGES 35 APPENDIX 3: SCOTTISH MODEL VILLAGE 54 INTRODUCTION Although close to London, Hertfordshire still enjoys significant and types of village and how they have provided a variety of Hertfordshire has a rich tradition of creative town and country they have developed. A village will typically fall into one of the areas of predominantly rural landscape character. The landscape different responses to these fundamental aims and objectives. planning including two of the most important garden cities. following three categories: the organic village characterised of Hertfordshire is naturally friendly, green and gently rolling. Hertfordshire also can also draw upon its experiences of the by incremental growth; the estate village laid out by private These rural areas are not just characterised by the natural The 21st Century has brought new pressures on housing New Towns – Stevenage, Hatfield and Hemel Hempstead are landowners and; the industrial village planned and executed landscape but also a whole series of villages. In many cases numbers, a fresh debate about green belt and how best to now all mature settlements. In all cases there were lessons to for a new elite, the wealthy entrepreneur. Current planning these are typical of archetypal English villages. -

WMCA Wellbeing Board

WMCA Wellbeing Board Date 24 January 2020 Report title West Midlands on the Move Portfolio Lead Cllr Izzi Seccombe – Wellbeing Accountable Chief Deborah Cadman OBE, West Midlands Executive Combined Authority email: [email protected] Tel: (0121) 214 7800 Accountable Simon Hall Physical Activity Policy & Delivery Employee Lead Email: [email protected] Tel: 0121 214 7093 Report has been Sean Russell, Wellbeing Director, WMCA considered by Recommendation(s) for action or decision: The WMCA Wellbeing Board is recommended to: 1. To note the progress in the delivery of current priorities. 2. To approve the strategy refresh by Summer 2020. 1. Purpose 1.1 This paper outlines the progress and next steps in the delivery of the WMCA’s West Midlands on the Move Strategic Framework and seeks the Wellbeing’s support for this work. 2. Background 2.1 In delivering its strategic framework, the WMCA’s focus has been on convening the collaborative space for physical activity and working with stakeholders to influence and address some of the barriers preventing people being active. 1 3. Progress Headlines Collaborative Engagement and Evaluating Impact. 3.1. On 9 January 2020, 25 physical activity stakeholders launched the West Midlands physical activity sector collaborative engagement programme, a yearlong programme to strengthen how we work together to make the West Midlands the best it can be in getting more people active. 3.2. This programme is being led by the University of Birmingham’s Institute of Leadership and the Leadership Centre working with Local Authorities, Active Partnerships and regional and national organisations such as Transport for the West Midlands and the Public Health England, will develop shared principles and values, explore shared accountability, priorities as well as applying learning from different practice. -

West Midlands Police Freedom of Information 18/05/2021 138A/21 I

West Midlands Police Freedom of Information I would like to know the following information under the Freedom of Information Act (FOIA) for your police force area between 01/01/2011 and 31/12/2015 (both inclusive): 1) The precise date of the respective incident (if not available, then the date of reporting). 2) The statistical ward and town or LSOA and town of each established homicide (that is incidents of murder, manslaughter or infanticide). Offence Town and District / Date Committed Total MANSLAUGHTER MURDER VICTIM UNDER 1 YR OLD MURDER-VICTIM 1 YR OLD OR OVER BIRMINGHAM 5 2 80 87 ACOCKS GREEN 0 0 1 1 25/04/2015 0 0 1 1 ALUM ROCK 0 0 2 2 19/11/2012 0 0 1 1 13/06/2013 0 0 1 1 ASTON 1 0 1 2 26/02/2013 0 0 1 1 05/01/2015 1 0 0 1 BALSALL HEATH 0 0 1 1 01/01/2015 0 0 1 1 BARTLEY GREEN 0 0 2 2 21/09/2012 0 0 1 1 02/08/2015 0 0 1 1 BILLESLEY 0 1 1 2 01/06/2013 0 1 1 2 BORDESLEY GREEN 0 0 1 1 20/05/2015 0 0 1 1 CASTLE BROMWICH 0 0 1 1 20/02/2013 0 0 1 1 18/05/2021 138A/21 West Midlands Police Freedom of Information CHELMSLEY WOOD 0 0 2 2 20/11/2011 0 0 1 1 11/11/2012 0 0 1 1 CITY CENTRE 0 0 3 3 12/05/2012 0 0 1 1 11/01/2013 0 0 2 2 DIGBETH 0 0 2 2 10/08/2013 0 0 1 1 03/10/2015 0 0 1 1 DRUIDS HEATH 0 0 2 2 12/02/2012 0 0 1 1 05/04/2012 0 0 1 1 EDGBASTON 0 0 6 6 21/06/2011 0 0 1 1 05/11/2012 0 0 1 1 07/03/2013 0 0 1 1 02/05/2013 0 0 1 1 12/01/2014 0 0 1 1 07/08/2015 0 0 1 1 ERDINGTON 0 0 6 6 18/12/2011 0 0 1 1 03/05/2012 0 0 1 1 07/05/2012 0 0 1 1 13/12/2012 0 0 1 1 28/12/2012 0 0 1 1 22/07/2014 0 0 1 1 FRANKLEY 1 0 0 1 01/07/2013 1 0 0 1 GREAT -

Heathfield Park Historic Characterisation Study

Heathfield Park Neighbourhood Plan Historic Characterisation Study Paul Quigley Landscape Archaeologist Black Country Archaeology Service June 2013 THIS PAGE IS LEFT INTENTIONALLY BLANK Characterisation Study –Heathfield Park Neighbourhood Plan Area version 2-0 Page 2 CONTENTS 1.0 INTRODUCTION .................................................................................................. 5 2.0 METHODOLOGY ................................................................................................. 7 MAP OF CHARACTER ZONES ............................................................. 11 3.0 CORONATION ROAD CHARACTER ZONE ........................................................ 12 4.0 FISHES ESTATE CHARACTER ZONE ................................................................ 18 5.0 HEATH TOWN ESTATE CHARACTER ZONE ..................................................... 20 6.0 HEATH TOWN PARK CHARACTER ZONE ........................................................ 26 7.0 NEW CROSS CHARACTER ZONE ..................................................................... 32 8.0 NEW PARK VILLAGE CHARACTER ZONE ........................................................ 34 9.0 NORTHERN CHARACTER ZONE ...................................................................... 39 10.0 POWELL STREET CHARACTER ZONE ............................................................. 44 11.0 RAILWAYS & CANAL CHARACTER ZONE ........................................................ 53 12.0 SPRINGFIELD CHARACTER ZONE .................................................................. -

Stafford Road Corridor Area Action Plan Publication Document

Agenda Item: 5B Wolverhampton City Council OPEN EXECUTIVE DECISION ITEM (AMBER) CABINET Date 22 MAY 2013 Portfolio COUNCILLOR P BILSON/ ECONOMIC REGENERATION AND PROSPERITY Originating Service Group(s) EDUCATION AND ENTERPRISE Contact Officer(s)/ TOM PODD IAN CULLEY Key Decision: Yes Telephone Number(s) 5638 5636 Forward Plan: Yes Title/Subject Matter STAFFORD ROAD CORRIDOR AREA ACTION PLAN PUBLICATION DOCUMENT Recommendation 1. That the Stafford Road Corridor Area Action Plan Publication Document (the AAP) be approved and published for the purposes of consultation. 2. That in the event of no representations being made to the consultation that may challenge the soundness of the AAP resulting in significant changes, the Cabinet Member for Economic Regeneration and Prosperity is authorised to approve any further amendments of a technical nature to the document prior to submission. 3. That the AAP be referred to Council for approval and submission to the Secretary of State for Communities and Local Government. 4. That if significant changes are required to the AAP prior to submission, a further report be submitted to Cabinet to consider these proposed changes. 5. The Cabinet approve the designation of extensions to the Wolverhampton Locks Conservation Area and additions to the Local List as specified in paragraphs 5.1 and 5.3 of this report and agree minor amendments to the Wolverhampton Locks Conservation Area Appraisal and Management proposals. 1 1. Purpose 1.1 To note the progress on the Stafford Road Corridor Area Action Plan (AAP). 1.2 To consider and seek approval to publish the AAP for consultation. 1.3 To consider and seek approval for the Wolverhampton Lock Conservation Area designation and additions to the Local List. -

West Midlands Key Route Network Stourbridge to WEST BROMW CH North of Wolverhampton

L CHF ELD STAFFORDSH RE WALSALL WOLVERHAMPTON West Midlands Key Route Network Stourbridge to WEST BROMW CH North of Wolverhampton DUDLEY BRMNGHAM WARW CKSH RE WORCESTERSH RE SOL HULL COVENTRY Figure 1 12 A5 A38, A38(M), A47, A435, A441, A4400, A4540, A5127, B4138, M6 L CHF ELD Birmingham West Midlands Cross City B4144, B4145, B4148, B4154 11a Birmingham Outer Circle A4030, A4040, B4145, B4146 Key Route Network A5 11 Birmingham to Stafford A34 Black Country Route A454(W), A463, A4444 3 2 1 M6 Toll BROWNH LLS Black Country to Birmingham A41 M54 A5 10a Coventry to Birmingham A45, A4114(N), B4106 A4124 A452 East of Coventry A428, A4082, A4600, B4082 STAFFORDSH RE East of Walsall A454(E), B4151, B4152 OXLEY A449 M6 A461 Kingswinford to Halesowen A459, A4101 A38 WEDNESF ELD A34 Lichfield to Wednesbury A461, A4148 A41 A460 North and South Coventry A429, A444, A4053, A4114(S), B4098, B4110, B4113 A4124 A462 A454 Northfield to Wolverhampton A4123, B4121 10 WALSALL A454 A454 Pensnett to Oldbury A461, A4034, A4100, B4179 WOLVERHAMPTON Sedgley to Birmingham A457, A4030, A4033, A4034, A4092, A4182, A4252, B4125, B4135 SUTTON T3 Solihull to Birmingham A34(S), A41, A4167, B4145 A4038 A4148 COLDF ELD PENN B LSTON 9 A449 Stourbridge to Wednesbury A461, A4036, A4037, A4098 A4123 M6 Stourbridge to A449, A460, A491 A463 8 7 WEDNESBURY M6 Toll North of Wolverhampton A4041 A452 A5127 UK Central to Brownhills A452 WEST M42 A4031 9 A4037 BROMW CH K NGSTAND NG West Bromwich Route A4031, A4041 A34 GREAT BARR M6 SEDGLEY West of Birmingham A456, A458, B4124 -

Response to Request for Information

[NOT PROTECTIVELY MARKED] Response to Request for Information Reference FOI 002702 Date 28 August 2018 Entertainment Licence Request: I would like to obtain or purchase a list of venues, pubs and establishments which are licenced for live entertainment which may provide entertainment by three or more musicians constituting a band. With reference to your above request, please see our response provided from page 2 onwards. Polish Catholic Club Polish Catholic Centre Stafford Road Wolverhampton West Midlands WV10 6DQ Hurst Hill Methodist Church Hall Hurst Hill Methodist Church Hall Hurst Road Lanesfield Wolverhampton West Midlands WV14 9EU Gorgeous 34-36 School Street Town Centre Wolverhampton WV1 4LF Divine Bar 77 Darlington Street City Centre Wolverhampton WV1 4LY R.A.F.A. Club Royal Air Force Association 26 Goldthorn Road Wolverhampton West Midlands WV2 4PN The Gunmakers Arms 63 Trysull Road Merry Hill / Bradmore Wolverhampton WV3 7JE Dartmouth Arms Dartmouth Arms Public House 47 Vicarage Road Parkfield Wolverhampton WV2 1DF Grand Station Grand Station Conference And Banqueting Centre Sun Street Wolverhampton West Midlands WV10 0BF The Lakshmi Restaurant 190-210 Dudley Road Blakenhall Wolverhampton WV2 3DY Wolverhampton Racecourse Dunstall Park Centre Gorsebrook Road Whitmore Reans Wolverhampton, West Midlands WV6 0PE The Robin R'n'B Club 2 26-28 Mount Pleasant Bilston Wolverhampton WV14 7LT The Cobra Lounge 30 Queen Street City Centre Wolverhampton WV1 3JW Ujamaa Limited Street Record Clifford Street Wolverhampton West Midlands Northwood -

Black Country Core Strategy Appendix 2 Detailed Proposals for Regeneration Corridors and Strategic Centres Adopted February 2011 Key

Black Country Core Strategy Appendix 2 Detailed Proposals for Regeneration Corridors and Strategic Centres Adopted February 2011 Key Regeneration Corridor Transport Employment Major Roads Metro Line Local Eployment Retained Proposed Metro Station Potential High Quality Proposed Rapid Transit Existing High Quality Passenger Rail Proposed Housing/ Freight Rail Local Employment Mixed Area * Motorway Office Location Bus Showcase Office Growth Corridor Major Highway Improvements Housing Rail Stations Environment Housing growth Area Housing Renewal Hub Black Country Landscape Beacons Town Centres Environmental Assets (SSIs, SACs, NNRs) Canal Strategic Centres Green Infastructure Improvements Town/Large District Centres Major Parks/Open Space District and Local Centres Existing Quarries Major New Retail Scheme Existing Strategic Waste Management Sites Tourist Hub Potential Strategic Waste Management Site Historic Centre Facility and Mineral Infastructure Site Brick Works/Tile Works/Other Clay User Community Fireclay Stockpile Health Hub Other E Education Hub Leisure/Sports Hub Black Country Local Authority Boundaries AAP Boundaries Green Belt * Areas where there will be both substantial housing development and retention of employment land. The delineation of boundaries within the diagrams and the figures provided are illustrative to give a broad indication of the scale of change. Appendix 2 This Appendix sets out the detailed proposals for the transformation of the Regeneration Corridors and Strategic Centres, including figures for housing and employment, infrastructure requirements and delivery mechanisms. The delineation of boundaries within the diagrams and the figures provided are illustrative to give a broad indication of the scale of change. Detailed boundaries and exact figures will be defined in lower tier Development Plan Documents such as site allocation documents and Area Action Plans. -

Hitchmoughs Black Country Pubs

HITCHMOUGH’S BLACK COUNTRY PUBS WEDNESFIELD (Inc. Ashmore Park, Fallings Park, Heath Town, Moseley Village) 2nd. Edition - © 2012 Tony Hitchmough. All Rights Reserved www.longpull.co.uk ALBION Lichfield Road / Stubby Lane, WEDNESFIELD OWNERS Mitchells and Butlers Ltd. [1988] Sizzling Pub Co. [2004] LICENSEES Graham Perry [1985] – [1988] Richard Thomas King [2005] NOTES Advert 1988 [1982] It was locally listed. Graham Perry was married to Frances. It was renovated in 1988 at a cost of £300,000. [2012] Check New Street. 2007 2012 ALBION 18, (8), New Street, Heath Town, WEDNESFIELD OWNERS LICENSEES John Tonks [1841] – [1870] Samuel Palmer Emery [1871] – [1872] John Leeding [1873] Samuel Palmer Emery [1874] Eli Charlton [1881] John Brookes [1891] – [1900] Frederick G ‘Fred’ White [1901] – [1912] Mrs. Maria White [1916] Harry White [1921] NOTES 8, New Street [1861] 18, New Street [1871] It had a beerhouse license. John Tonks = John Tonkes John Tonkes, beer retailer, Wednesfield. [1841] John Tonks was also a steel trap maker. [1845], [1849], [1861] He was described as a beer retailer and vermin trap maker, New Street. [1864], [1865] 1861 Census 8, New Street – ALBION INN [1] John Tonks (61), widower, publican and trap maker, born Willenhall; [2] Mary A. Tonks (22), daughter, waitress, born Willenhall; [3] Lavinia Tonks (16), daughter, house servant, born Willenhall; [4] Ellen Tonks (15), daughter, house servant, born Willenhall; [5] Mark Tonks (12), son, scholar, born Willenhall: 1871 Census 18, New Street [1] Samuel P. Emery (41), publican, born Willenhall; [2] Mary Emery (38), wife, born Wolverhampton; [3] Catherine A. Emery (16), daughter, born Wednesfield; [4] Elizabeth Emery (15), daughter, born Wednesfield; [5] William J. -

Response to Request for Information

[NOT PROTECTIVELY MARKED] Response to Request for Information Reference FOI 0615129 Date 23 June 2015 Alcohol Licensing Request: I’m emailing you to request information which I’m hoping you can assist with under the Freedom of Information Act 2000, around alcohol licensing. Please could you supply the following information: • How many primary/junior schools (up to and including 11 years old) in the Wolverhampton City Council area have applied for a Temporary Event Notice (TEN) between 01 April 2013 and 31 March 2014 to sell/serve alcohol to adults at events where children will be present? For example, school fetes and school discos • Of those who applied during that time period, how many schools were granted TEN licences and how many were rejected? • Between 01 April 2013 and 31 March 2014, how many Temporary Event Notices (TENs) have been requested by primary/junior schools (pupils up to and including 11 years old) in the Wolverhampton City Council area wanting to sell/serve alcohol to adults at events where children will be present? For example, school fetes and school discos • Of those applications received, how many were granted and how many were rejected? • Could you also provide the same information for the time between 01 April 2014 and 31 March 2015. Response: In response to your request please find below our response to the number of Temporary Event Notices issued to Primary/Junior School between April 2013 to March 2015. In regards to how many schools/applications were rejected, we can confirm that Temporary Event Notices are rarely rejected. They are objected to and would go to a subcommittee and our current records show that none [schools] have gone to subcommittee hearings for the period mentioned. -

Heathfield Park Draft Neighbourhood Plan 2014-2026

Your Plan Your Future HEATHFIELD PARK DRAFT NEIGHBOURHOOD PLAN 2014-2026 Local People Working Towards a Neighbourhood Plan for HeathTown, Springfield and New Park Village Version 9.2– updated 10.7.13 A Dedication to the People of Heathfield Park Heathfield Park Neighbourhood Planning Forum would like to dedicate the Neighbourhood Plan to all who live, work, study, worship and do business in Heath Town, Springfield and New Park Village. 2 Acknowledgements Heathfield Park Neighbourhood Forum consists of a group of local volunteers, some local individuals, others representing a number of organisations based in the Heath Town, Springfield and New Park Village area (see appendix 1 for list of members). Those volunteers have no background in planning, but a deep passion for the place where they live or volunteer. Without their enthusiasm, humour and determination, the Neighbourhood Plan would not have come to fruition. The Neighbourhood Forum would like to thank Wolverhampton City Council for the support provided in preparing the Plan, particularly the North East Neighbourhood Services Team for their role in assisting the Local Neighbourhood Partnership to become the designated Neighbourhood Forum for the area and ensuring that good quality consultation, planning and engagement has taken place with local residents. We would also like to thank Wolverhampton City Council’s Planning Team for their expertise, guidance and support at the crucial stages of preparing the draft Neighbourhood Plan. We pay tribute to the host of local residents, volunteers, organisations and local businesses who have taken part in preparing the draft Neighbourhood Plan, including those who have taken part in the Household and Business Survey and various stakeholder, consultation and workshop events over the last 18 months.