Report of the Select Committee on Port St Mary Commissioners

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GD No 2017/0037

GD No: 2017/0037 isle of Man. Government Reiltys ElIan Vannin The Council of Ministers Annual Report Isle of Man Government Preservation of War Memorials Committee .Duty 2017 The Isle of Man Government Preservation of War Piemorials Committee Foreword by the Hon Howard Quayle MHK, Chief Minister To: The Hon Stephen Rodan MLC, President of Tynwald and the Honourable Council and Keys in Tynwald assembled. In November 2007 Tynwald resolved that the Council of Ministers consider the establishment of a suitable body for the preservation of War Memorials in the Isle of Man. Subsequently in October 2008, following a report by a Working Group established by Council of Ministers to consider the matter, Tynwald gave approval to the formation of the Isle of Man Government Preservation of War Memorials Committee. I am pleased to lay the Annual Report before Tynwald from the Chair of the Committee. I would like to formally thank the members of the Committee for their interest and dedication shown in the preservation of Manx War Memorials and to especially acknowledge the outstanding voluntary contribution made by all the membership. Hon Howard Quayle MHK Chief Minister 2 Annual Report We of Man Government Preservation of War Memorials Committee I am very honoured to have been appointed to the role of Chairman of the Committee. This Committee plays a very important role in our community to ensure that all War Memorials on the Isle of Man are protected and preserved in good order for generations to come. The Committee continues to work closely with Manx National Heritage, the Church representatives and the Local Authorities to ensure that all memorials are recorded in the Register of Memorials. -

Brochure Template

01624 662820 20 Cronk Reayrt Glenfaba Park, Peel £174,950 A 2 Bed Semi Detached House Conveniently Located To All Local Amenities and Schools Entrance Porch Lounge, Separate Dining Room Recently Modernised Kitchen with Built in Oven and Hob Small Utility Room Two Double Bedrooms Bathroom Comprises of Shower, Wash Basin and Toilet 2 Car Drive Front and Rear Garden With Patio and Shed Gas Fired Central Heating uPVC Glazing Throughout **Perfect For First Time Buyers** No Onward Chain Whilst all particulars are believed to be correct, neither Property Wise Limited, or their clients guarantee their accuracy nor are they intended to form part of any contract. Floorplans are for illustrative purposes only. Decorative finishes, fixtures, fittings and furnishings do not represent the current state of the property. Measurements are approximate and not to scale. Directions:Heading Out Of Peel On The Patrick to Glen Maye Road Take The 6th Turning On The Left Onto Creggans Avenue Then Bear Right into Cronk Reayrt The Property Can Be Found Just As The Road Bends Clearly Identified By Our For Sale Board Rateable value: £ Rates payable: £ (Inc Water Rates) Inclusions: to be confirmed Services: All Mains Services Connected Whilst all particulars are believed to be correct, neither Property Wise Limited, or their clients guarantee their accuracy nor are they intended to form part of any contract. Floorplans are for illustrative purposes only, decorative finishes, fixtures, fittings and furnishings do not represent the current state of the property. Measurements are approximate and not to scale. Property Wise Limited,14b Village Walk, Onchan Isle of Man, IM3 4BE. -

Grid Export Data

Accommodation for Guest Required to Self-Isolate February 2021 Accommodation Name Classification Type Address 1 Address 2 Town Post Code Email Address Main Phone Bedrooms Bedspaces Rating 1 Barnagh Barns Self Catering 1 Barnagh Barns Rhencullen Kirk Michael IM6 2HB [email protected] 07624 480803 2 4 4 Star Gold 13 Willow Terrace Self Catering 13 Willow Terrace Douglas IM1 3HA [email protected] 07624 307575 2 4 Rating Pending Apartment 1 - Derby Court Self Catering Flat 1 Derby Court 42 The Promenade Castletown IM9 1BG [email protected] 07624 493181 2 4 4 Star Arrandale Apartments - Flat 1 Self Catering 24 Hutchinson Square Douglas IM2 4HP [email protected] 01624 674907 1 2 3 Star Arrandale Apartments - Flat 2 Self Catering 24 Hutchinson Square Douglas IM2 4HP [email protected] 01624 674907 1 2 3 Star Arrandale Apartments - Flat 3 Self Catering 24 Hutchinson Square Douglas IM2 4HP [email protected] 01624 674907 2 3 3 Star Arrandale Apartments - Flat 4 Self Catering 24 Hutchinson Square Douglas IM2 4HP [email protected] 01624 674907 1 2 3 Star Arrandale Apartments - Flat 5 Self Catering 24 Hutchinson Square Douglas IM2 4HP [email protected] 01624 674907 1 2 3 Star Arrandale Apartments - Flat 6 Self Catering 24 Hutchinson Square Douglas IM2 4HP [email protected] 01624 674907 1 2 3 Star Arrandale Apartments - Flat 7 Self Catering 24 Hutchinson Square Douglas IM2 4HP [email protected] 01624 674907 1 2 3 Star At Caledonia Guest House Caledonia 17 Palace Terrace Douglas IM2 4NE [email protected] 01624 624569 20 50 -

Doing Business in the Isle of Man

DOING BUSINESS IN THE ISLE OF MAN CONTENTS 1 – Introduction 3 2 – Business environment 4 3 – Foreign Investment 7 4 – Setting up a Business 8 5 – Labour 13 6 – Taxation 16 7 – Accounting & reporting 21 8 – UHY Representation in the Isle of Man 23 DOING BUSINESS IN THE ISLE OF MAN 3 1 – INTRODUCTION UHY is an international organisation providing accountancy, business management and consultancy services through financial business centres in over 100 countries throughout the world. Member firms work together through the network to conduct transnational operations for clients as well as offering specialist knowledge and experience within their own national borders. Global specialists in various industry and market sectors are also available for consultation. This detailed report providing key issues and information for users considering business operations in the Isle of Man has been provided by the office of UHY representatives: UHY CROSSLEYS LLC PO Box 1 Portland House Station Road Ballasalla Isle of Man, IM99 6AB British Isles Phone +44 (0) 1624 822816 Website www.crossleys.com Email [email protected] You are welcome to contact Andrew Pennington ([email protected]) or Nigel Rotheroe ([email protected]) for any enquiries you may have. Information in the following pages has been updated so that it is effective at the date shown, but inevitably it is both general and subject to change and should be used for guidance only. For specific matters, users are strongly advised to obtain further information and take professional advice before making any decisions. This publication is current at August 2021. We look forward to helping you do business in the Isle of Man. -

Buchan School Magazine 1971 Index

THE BUCHAN SCHOOL MAGAZINE 1971 No. 18 (Series begun 195S) CANNELl'S CAFE 40 Duke Street - Douglas Our comprehensive Menu offers Good Food and Service at reasonable prices Large selection of Quality confectionery including Fresh Cream Cakes, Superb Sponges, Meringues & Chocolate Eclairs Outside Catering is another Cannell's Service THE BUCHAN SCHOOL MAGAZINE 1971 INDEX Page Visitor, Patrons and Governors 3 Staff 5 School Officers 7 Editorial 7 Old Students News 9 Principal's Report 11 Honours List, 1970-71 19 Term Events 34 Salvete 36 Swimming, 1970-71 37 Hockey, 1971-72 39 Tennis, 1971 39 Sailing Club 40 Water Ski Club 41 Royal Manx Agricultural Show, 1971 42 I.O.M, Beekeepers' Competitions, 1971 42 Manx Music Festival, 1971 42 "Danger Point" 43 My Holiday In Europe 44 The Keellls of Patrick Parish ... 45 Making a Fi!m 50 My Home in South East Arabia 51 Keellls In my Parish 52 General Knowledge Paper, 1970 59 General Knowledge Paper, 1971 64 School List 74 Tfcitor THE LORD BISHOP OF SODOR & MAN, RIGHT REVEREND ERIC GORDON, M.A. MRS. AYLWIN COTTON, C.B.E., M.B., B.S., F.S.A. LADY COWLEY LADY DUNDAS MRS. B. MAGRATH LADY QUALTROUGH LADY SUGDEN Rev. F. M. CUBBON, Hon. C.F., D.C. J. S. KERMODE, ESQ., J.P. AIR MARSHAL SIR PATERSON FRASER. K.B.E., C.B., A.F.C., B.A., F.R.Ae.s. (Chairman) A. H. SIMCOCKS, ESQ., M.H.K. (Vice-Chairman) MRS. T. E. BROWNSDON MRS. A. J. DAVIDSON MRS. G. W. REES-JONES MISS R. -

Common Law Courts Act 1796

c i e AT 1 of 1796 COMMON LAW COURTS ACT 1796 Common Law Courts Act 1796 Index c i e COMMON LAW COURTS ACT 1796 Index Section Page 1 Glanfaba Sheading .......................................................................................................... 5 2 Garff Sheading ................................................................................................................ 5 3 Middle Sheading ............................................................................................................. 5 4 [Repealed] ........................................................................................................................ 6 5 and 6 [Repealed] ............................................................................................................. 6 7 [Repealed] ........................................................................................................................ 6 ENDNOTES 7 TABLE OF ENDNOTE REFERENCES 7 c AT 1 of 1796 Page 3 Common Law Courts Act 1796 Section 1 c i e COMMON LAW COURTS ACT 1796 Received Royal Assent: 15 July 1796 Promulgated: 12 September 1796 Commenced: 12 September 1796 AN ACT for the better Regulation of the Court of Common Law. Island divided into Districts, etc Whereas the present Mode of holding the Court of Common Law for the whole Island, at one particular Time and Place, hath been found to be very inconvenient to the Public. And it is thought expedient that the Island should be divided into two Districts for the Purpose of holding a Court of Common Law within each -

Eight Hour Coastal Tour

Eight Hour Coastal Tour To start this coastal tour, you will be picked up at the Sea Terminal and driven north along Douglas Promenade, around Onchan Head and along the coast road to Groudle Glen. Groundle Glen After a short time spent relaxing, walking in the Glen and taking in the sea views, we drive on towards Laxey. Laxey After spending a little while wandering around Laxey’s quaint waterfront, we set off North along the coastal road stopping at Dhoon Glen. Dhoon Glen Dhoon Glen is picturesque but the walk down to the sea is very steep. Some people may find it too difficult to walk back, so if you are a little unsteady on your feet or prone to get tired on steep walks you may wish to stay on the higher level of the Glen. For those who are a little fitter, the walk down to the sea has its rewards. The Glen is only small but very beautiful and boasts a small waterfall. When we leave Doon Glen, we carry on north toward Ramsey, passing through Glen Mona village and the parish of Margould. Ramsey Ramsey is the second largest town on the Isle of Man and has quite a nice choice of shops. You may wish to spend a little time here browsing through the many small shops along the high Street (Parliament Street). You will also get the chance for a little refreshment in one of the town’s cafes or pubs. When we leave Ramsey, we travel further north to the Point of Ayre Lighthouse. -

The Runic and Other Monumental Remains of the Isle of Man

Vy. < THE RUNIC AND OTHER MONUMENTAL REMAINS OF THE ISLE OF MAN. CHI8W1CK PRESS:—PKINTBD BY C. WHITTIKOHAM, TOOK8 COURT, CHANCERY LANE. n XXE K.VXIC /^ Of r/yf ^4/ or ,V^ ^44^ By the Uev? J. G. Gumming, M. A. F. G. S Head Master of the Grammar School , Lichf/eld. LONDON Bell atitd Daldy, tleet street. Lonifur XicfvfieUl. Kerrutsh k\l^rieale^ Daicgl/LS . lOAN STACK TO THE HONOURABLE AND RIGHT REVEREND HORACE POWYS, D.D. Bishop of Sodor and Man. My Lord, The earliest Monumental Remains noticed in the present work were pro- bably erected when your Lordship's ancestors were Kings of Man. The names of the Bishops contemporary with Merfyn Frych and Roderic Mawr have not been handed down to posterity, but the oldest Manx Chronicle assures us that this has never been to the there was a true succession j and interrupted present office in the most ancient ex- day, when your Lordship is adorning the Episcopal isting See of the British Isles. in the which I therefore deem myself peculiarly privileged permission your of the Lordship has afforded me to dedicate to you these few pages descriptive remarkable Memorials, erected in your Diocese through a long series of years, to those who have died in the faith of Christ. With the deepest respect, I beg leave to subscribe myself. Your Lordship's Very faithful and obedient servant, J. G. GUMMING. Lichfield, June 1st, 1857. 891 PREFATORY NOTE. T THINK it right to state that the following work is primarily an endeavour to exhibit in its rude character the ornamentation on the Scandinavian Crosses in the Isle of Man. -

Grid Export Data

Visit Isle of Man Registered Accommodation List April 2021 Accommodation Name Classification Type Address 1 Address 2 Address 3 Town Post Code Email Address Main Phone 1 Barnagh Barns Self Catering 1 Barnagh Barns Rhencullen Kirk Michael IM6 2HB [email protected] 07624 480803 1 Mews Cottages Self Catering 1 Mews Cottages Factory Lane Peel IM5 1HF [email protected] 07624 373032 13 Willow Terrace Self Catering 13 Willow Terrace Douglas IM1 3HA [email protected] 07624 307575 2 Sunnyside Terrace Self Catering 2 Sunnyside Terrace Minorca Hill Laxey IM4 7EE [email protected] 07747 610150 24 Milner Park Self Catering 24 Milner Park Port Erin IM9 6DH [email protected] 07624 413608 4 Mews Cottages Self Catering 4 Mews Cottages Factory Lane Peel IM5 1HF [email protected] 07817 720597 4 Shore Road Self Catering 4 Shore Road Peel IM5 1AH [email protected] 01624 830200 49 Piccadilly Court Self Catering Apartment 49 Piccadilly Court Queens Promenade Douglas IM2 4NS [email protected] 07783 374383 5 Mews Cottages Self Catering Beach Street Factory Lane Peel IM5 1HF [email protected] 01277822433 5 Strathallan Apartments - First Floor Self Catering Flat 1 5 Strathallan Crescent Douglas IM2 4NR [email protected] 01624 626646 5 Strathallan Apartments - Ground Floor Self Catering Flat 2 5 Strathallan Crescent Douglas IM2 4NR [email protected] 01624 626646 8 Links Close Self Catering 8 Links Close Port Erin IM9 6LT [email protected] 07624 269650 Aalin Thie - Apartment 1 Self -

Brochure Template

01624 662820 26 Glenfaba Road Peel £259,950 A Well Presented 4 Bed Mid-Terrace Town House Located In The Heart Of Peel Within Walking Distance to All Of Peels Local Amenities Entrance Porch With Stairs To First Floor Large Lounge Into Dining Area New Fitted Kitchen With Built In Washing Machine, Dishwasher, Electric Oven And Gas Hob Downstairs WC and Wash Basin First Floor Comprises Family Bathroom With Bath and Separate Shower, Toilet and Wash Basin 2 Double Bedrooms One With Fitted Wardrobes Second Floor with Double Bedroom and Single Bedroom Outside with Decked and Paved Area With Views Out To Peel Hill Stone Built Store With Central Heating Boiler Oil Fired Central Heating Upvc Double Glazing Throughout Decorated and Maintained to a High Standard Throughout Whilst all particulars are believed to be correct, neither Property Wise Limited, or their clients guarantee their accuracy nor are they intended to form part of any contract. Floorplans are for illustrative purposes only. Decorative finishes, fixtures, fittings and furnishings do not represent the current state of the property. Measurements are approximate and not to scale. Directions: Travelling Out of Peel Towards Patrick and Glen Maye, Follow Patrick Street Onto Glenfaba Road. The Property Can Be Located On The Right Hand Side. Clearly Identified By Our For Sale Board Rateable value: £76 Rates payable: £731.68 (Inc Water Rates) Inclusions: to be confirmed Services: All Mains Services Connected Whilst all particulars are believed to be correct, neither Property Wise Limited, or their clients guarantee their accuracy nor are they intended to form part of any contract. -

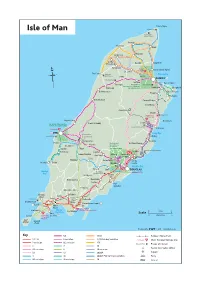

Isle of Man Bus Map.Ai

Point of Ayre Isle of Man Lighthouse Point of Ayre Visitor Centre Smeale The Lhen Bride Andreas Jurby East Jurby Regaby Dog Mills Threshold Sandygate Grove Grand Island Hotel St. Judes Museum The Cronk Ballaugh Ramsey Bay Old Church Garey Sulby RAMSEY Wildlife Park Lezayre Port e Vullen Curraghs For details of Albert Tower bus services in Ramsey, Ballaugh see separate map Lewaigue Maughold Bishopscourt Dreemskerry Hibernia Ballajora Kirk Michael Corony Bridge Glen Mona SNAEFELL Dhoon Laxey Wheel Dhoon Glen & Mines Trail Knocksharry Ballaragh Laxey For details of bus services Cronk-y-Voddy in Peel, see separate map Laxey Woollen Mills Old Laxey Peel Castle PEEL Laxey Bay Tynwald Mills Corrins Folly Tynwald Hill Ballabeg Ballacraine Baldrine Patrick For details of Halfway House Greeba bus services St. John’s in Douglas, Gordon Hope see separate map Groudle Glen and Railway Glenmaye Crosby Onchan Lower Foxdale Strang Governors Glen Vine Bridge Eairy Foxdale Union Mills Derby Niarbyl Dalby Braddan Castle NSC Douglas Bay Braaid Cooil DOUGLAS Niarbyl Rest Home Bay for Old Horses St. Mark’s Quines Hill Ballamodha Newtown Santon Port Soderick Orrisdale Silverdale Glen Bradda Ballabeg West Colby Level Cross Milners Tower Four Ballasalla Bradda Head Ways Ronaldsway Airport Port Erin Shore Hotel Castle Rushen Cregneash Bay ny The Old Grammar School Carrickey Castletown 03miles Port Scale Sound Cregneash St. Mary 05kilometres Village Folk Museum Calf Spanish of Man Head Produced by 1.9.10 www.fwt.co.uk Key 5/6 17/18 Railway / Horse Tram 1,11,12 6 variation 17/18 Sunday variation Peel Castle Manx National Heritage Site 2 variation 6C variation 17B Tynwald Mills Places of interest 3 7 19 Tourist Information Office 3A variation 8 19 variation X3 13 20/20A Airport 4 16 20/20A Point of Ayre variation Ferry 4A variation 16 variation 29 Seacat. -

Food Business Register JK 1 V19/11 ED

Food Business Register Registration Date Trading As Address of Business Licensee Number Registered 419 1 Cambridge 1 Cambridge Terrace, Douglas, IM1 3LL Ms J Porter 23/05/2012 714 14 Highfield Crescent B&B 14 Highfield Crescent, Birchill, Onchan, IM3 3BH Ms L Strickett & Mr M Strickett 21/03/2014 111 14 North 14 North Quay, Douglas, IM1 4LE Mr P Taylor 30/04/2010 1360 1886 Bar, Grill and Cocktail Lounge 6 Regents Street Mr A Hardy 27/03/2019 808 1st Class Nursery 19 Hawarden Avenue, Douglas, IM2 3BA Ms C Wiggins 02/03/2015 38 1st Class Pre-School Nursery 19 Hawarden Avenue, Douglas, IM1 4BP Ms C Wiggins 15/04/2015 120 2 Brookfield 2 Brookfield, Little Mill Road, Onchan, IM4 5BF Mr C Cain 19/05/2010 1295 21 Christian Road 21 Christian Road, Douglas, IOM 03/10/2018 45 3 Meadow Court 3 Meadow Court, Ballasalla, IM9 2DW Ms R Keggin 05/06/2009 752 6 Peveril Terrace 6 Peveril Terrace, Peel, IM5 1PH Ms L Kavanagh 13/07/2014 747 7th Wave Rock View, Strand Road, Port Erin, IM9 6HF Mrs J M Kneale 16/06/2014 77 A & J Quality Butchers Ltd. Unit 5a, Middle River Industrial Estate, Douglas, IM2 1AL Mr J O'Connell 03/12/2012 329 A & J Quality Butchers Ltd. 2 Cushag Road, Douglas, IM2 2BN Mr T Wright 03/12/2012 145 A and L Catering New Swimming Pool, Mooragh Promenade, Ramsey, IM8 3AB Mrs L Hall 13/11/2018 1332 A Little Piece of Hope Candy Floss Belmont, Maine Road, Port Erin Helen Walmsley 08/02/2019 1022 A W Teare Ballakelly Farm, Andreas, IM7 3EJ Mr A Teare 06/05/2016 177 Abbeylands B&B Southfields, Abbeylands, Onchan, IM4 5EG Mr P Nash & Mrs J Nash 12/04/2011 404 Abbotswood Nusing Home Abbotswood Court, Ballasalla, IM9 3DZ Ms J Usher 02/05/2012 205 Abfab Cakes Highland Park, Saddle Road, Douglas, IM2 1HG Ms A Dorling 27/07/2011 131 Adelphi Guest House 15 Stanley View, Douglas Luan Yi 23/08/2019 1135 Adorn Domicilary Care Ltd.