Techtronic Industries Strong Growth Momentum to Continue

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hand Tools Market

+44 20 8123 2220 [email protected] Hand Tools Market - Global Outlook and Forecast 2020-2025 https://marketpublishers.com/r/H0D6A08854D7EN.html Date: September 2020 Pages: 312 Price: US$ 3,500.00 (Single User License) ID: H0D6A08854D7EN Abstracts In-depth Analysis and Data-driven Insights on the Impact of COVID-19 Included in this Global Hand Tools Market Report The global hand tools market by revenue is expected to grow at a CAGR of over 4% during the period 2019–2025. The global hand tools market is expected to grow 1.3X times during the forecast period. The market is expected to witness a considerable growth post-2020. Rapid industrialization and increasing applications in household and commercial sectors are primarily driving the market. Automobile, aerospace, construction, electronics, and shipbuilding are the major end-use of these devices. The tool industry landscape is moving toward sophistication and customization that can determine market leadership in a competitive scenario. Advancements in technology and the extensive usage of battery-driven devices have fueled the adoption of cordless power tools and related accessories that are light and durable. This growth factor for the substitutes is expected to challenge the potential of hand tools. The DIY culture can be one of the major drivers for these devices in the coming years with a high scope for penetration in growing economies. The global hand tools market suffered a downfall during the COVID-19 crisis as most economic activities were halted during Q1 and Q2 in 2020. Most major revenue- generating end-users such as construction, automotive, commercial renovation, and home improvement activities were affected, leading to a decline in the market sales. -

Original Filed in Clerk's Office

Case 1:09-cv-03308-RWS Document 1 Filed 11/24/09 Page 1 of 12 ORIGINAL FILED IN CLERK'S OFFICE NOV 2 4 2009 IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF GEORGIA s . , ATLANTA DIVISION HITACHI KOKI CO ., LTD ., Plaintiff, V. Civ' Action No. : TEexTRONZC INDUSTRIES CO. LTD., .~ . ~ n , TECHTRONIC INDUSTRIES NORTH O9c!- AMERICA,- INC ., ONE WORLD TECHNOLOGIES, INC ., OWT INDUSTRIES INC ., MILWAUKEE ELECTRIC TOOL CORPORATION, and RYOBI TECHNOLOGIES, INC., Defendants. COMPLAINT FOR PATENT INFRINGEMENT Plaintiff, Hitachi Koki Co ., Ltd., by its undersigned attorneys, complains of Defendants, Techtronic Industries Co . Ltd., Techtronic North America, Inc ., One World Technologies, Inc ., OWT Industries Inc., Milwaukee Electric Tool Corporation, and Ryobi Technologies, Inc ., and shows the Court as follows : NATURE OF LAWSUIT 1 . This is a claim for patent infringement arising under the patent laws of the United States, Title 35 of the United States Code . Case 1:09-cv-03308-RWS Document 1 Filed 11/24/09 Page 2 of 12 PARTIES AND PATENTS 2 . Hitachi Koki Co., Ltd. ("Hitachi Koki") is a foreign corporation organized and existing under the laws of Japan having a principal place of business at Shinagawa Intercity Tower A, 20`t' Floor, 15-1, Konan 2-chome, Minato-ku, Tokyo 108-6020, Japan . 3 . Hitachi Koki owns all right, title and interest in the following United States Patents : U. S . Pat. No. 7,207,251 entitled "Cutter With Laser Generator That Irradiates Cutting Position On Workpiece To Facilitate Alignment Of Blade With Cutting Position" ("the `251 patent"), and U. S . Pat. -

Stanley Black and Decker Techtronic Industries Co Ltd (TTI) Chevron

Who Owns What? Andrew Davis May, 2019 This is a redacted version of an article II found on protoolreviews.com. I remember growing up when General Motors offered different brands at different price points (until they all the brands started to overlap before GM collapsed) – Cadillac at the top end, followed by Oldsmobile, Buick, Pontiac, and Chevy. We have a similar situation in woodworking tools (also in kitchen appliances) except that in the case of tools, the multi-brand company is more often a case of acquisitions rather than organic development. Anyway, for those readers interested in the business side of tools, this column, which is a departure from my usual thread, may be of interest. Stanley Black and Decker Stanley Black & Decker (SBD) turned heads when it bought Craftsman Tools in 2017 after Sears closed 235 stores in 2015. Dating back to 1843 with a man named Frederick Stanley, the company merged in 2010 with Black and Decker. As of 2017, the company maintains a $7.5 billion business in tools & storage alone. SBD brands include: DeWalt Stanley Black + Decker Bostitch Craftsman Vidmar Mac Tools Irwin Lenox Proto Porter-Cable Powers Fasteners Lista Sidchrome Emglo USAG Techtronic Industries Co Ltd (TTI) TTI owns Milwaukee Tool and a host of other power tool companies. It also licenses the RIDGID and RYOBI names for cordless power tools (Emerson actually owns RIDGID and makes the red tools). Founded in 1985 in Hong Kong, TTI sells tools all over the world and employs over 22,000 people. TTI had worldwide annual sales of over US$6 billion in 2017. -

BRIEF in OPPOSITION —————♦————— Jason C

No. 19-1299 In the Supreme Court of the United States —————♦————— THE CHAMBERLAIN GROUP, INC., Petitioner, v. TECHTRONIC INDUSTRIES CO., TECHTRONIC INDUSTRIES NORTH AMERICA, INC., ONE WORLD TECHNOLOGIES, INC., OWT INDUSTRIES, INC., RYOBI TECHNOLOGIES, INC., Respondents. —————♦————— On Petition For A Writ Of Certiorari To The United States Court Of Appeals For The Federal Circuit —————♦————— BRIEF IN OPPOSITION —————♦————— Jason C. White William R. Peterson Michael J. Abernathy Counsel of Record Sanjay K. Murthy MORGAN, LEWIS & BOCKIUS LLP Nicholas A. Restauri 1000 Louisiana St., Ste. 4000 MORGAN, LEWIS & BOCKIUS LLP Houston, TX 77002 77 W. Wacker Drive, Ste. 500 (713) 890-5188 Chicago, IL 60601 william.peterson (312) 324-1000 @morganlewis.com Julie S. Goldemberg Sean C. Cunningham MORGAN, LEWIS & BOCKIUS LLP Erin P. Gibson 1701 Market Street Stanley J. Panikowski Philadelphia, PA 19103 DLA PIPER LLP (US) (215) 963-5095 401 B Street, Suite 1700 San Diego, CA 92101 (619) 699-2700 Counsel for Respondents i QUESTION PRESENTED Petitioner The Chamberlain Group (“Chamber- lain”) received a patent covering the idea of wirelessly transmitting information about a garage door opener. Its claims recite a garage door opener (mobile barrier operator), a controller (found in any electric device), and a wireless transmitter—“a handful of generic * * * components configured to implement [this abstract] idea.” Alice Corp. Pty. Ltd. v. CLS Bank Int’l, 573 U.S. 208, 226-27 (2014). At trial, Chamberlain argued that its patent cov- ered all garage door openers with integrated transmit- ters that could communicate with smartphones. In the words of its expert, there are no “acceptable non-in- fringing alternatives.” The Federal Circuit, considering the claims as a whole, concluded that they were directed to the ab- stract idea of wirelessly transmitting information. -

In the United States Court of Appeals for the Federal Circuit

Case: 16-2713 Document: 50-1 Page: 1 Filed: 11/14/2016 No. 16-2713 In the United States Court of Appeals For the Federal Circuit THE CHAMBERLAIN GROUP, INC., Plaintiff – Appellee, v. TECHTRONIC INDUSTRIES CO. LTD., ET TECHNOLOGY (WUXI) CO. LTD., Defendants, TECHTRONIC INDUSTRIES NORTH AMERICA, INC., ONE WORLD TECHNOLOGIES, INC., OWT INDUSTRIES, INC., RYOBI TECHNOLOGIES, INC., Defendants – Appellants. On Appeal from the United States District Court for the Northern District of Illinois, Eastern Division Case No. 1:16-CV-06097, Hon. Harry D. Leinenweber NONCONFIDENTIAL JOINT APPENDIX Volume I, Pages Appx1 to Appx2776 William R. Peterson Jason C. White Nicholaus E. Floyd Michael J. Abernathy MORGAN, LEWIS & BOCKIUS LLP Sanjay K. Murthy 1000 Louisiana St., Ste. 4000 Nicholas A. Restauri Houston, TX 77005 MORGAN, LEWIS & BOCKIUS LLP (713) 890-5188 77 W. Wacker Drive, Ste. 500 (713) 890-5001 (Fax) Chicago, IL 60601 (312) 324-1000 Julie S. Goldemberg (312) 324-1001 (Fax) MORGAN, LEWIS & BOCKIUS LLP 1701 Market Street Philadelphia, PA 19103 (215) 963-5095 (215) 963-5001 (Fax) Counsel for Appellants (For continuation of appearances see inside cover) Case: 16-2713 Document: 50-1 Page: 2 Filed: 11/14/2016 Katherine Vidal Benjamin C. Elacqua FISH & RICHARDSON P.C. Michael R. Rueckheim 500 Arguello Street, Suite 500 FISH & RICHARDSON P.C. Redwood City, CA 94063 1221 McKinney Street, Suite 2800 (650) 839-5070 Houston, TX 77010 (650) 839-5071 (Fax) (713) 654-5300 (713) 652-0109 (Fax) Counsel for Appellees Case: 16-2713 Document: 50-1 Page: 3 Filed: 11/14/2016 TABLE OF CONTENTS Description Final Page No(s). -

Thdf Ar08.Pdf

Photo by Chris Gaythen/Getty Images 2008 FOUNDATION Total giving in cash Supported housing Planted or restored Awarded more and in-kind exceeded development more than 200,000 than $1.2 million to $50 million to more organizations with community trees support community than 5,100 nonprofit grants of $15.5 million, through grants volunteer projects organizations which produced and totaling $2.6 million through the Housing preserved 14,734 Impact Grant program affordable housing units, built responsibly THE importance OF HOMES At The Home Depot Foundation, we understand that affordable, healthy homes are essential to strong families, thriving neighborhoods and sustainable cities. The stability provided by living in a home that is affordable over the long-term positively impacts the family’s financial status, health and overall quality of life. And the benefits don’t stop there – they extend throughout the community and the economy. Home is where “ During the last two years, the Foundation has helped build or renovate more than 27,000 homes for families across the country. While the issues “one starts from. around the increasing number of mortgage defaults and foreclosures and the rippling effect on entire cities and regions have attracted much T.S. ELIOT attention in this time, we have partnered with nonprofit organizations and local leaders to help families move into homes that they can afford to live in for years to come. This means that the mortgage or rent is manageable, but that’s just the beginning. We also work to ensure that the home is efficient so utility bills are affordable; that the location is close to schools, stores and jobs so transportation costs are low and commutes are short; and that the community includes parks and trees so residents can enjoy healthy, safe places outdoors. -

Techtronic Industries Company Limited

[For Immediate Release] Techtronic Industries Introduces Complete Line of Professional Power Tools Marketed Under the RIDGID® Brand* in North America * * * 35 Tools in Industrial Supply Channels and The Home Depot (HONG KONG, 13 August 2003) –Techtronic Industries Co. Ltd. (“TTI”) (stock code: 669, ADR symbol: TTNDY), today announced the introduction of a new, comprehensive line of 35 RIDGID®* handheld corded, cordless, benchtop and stationary power tools for professional contractors, builders and woodworkers. In designing the new line of RIDGID tools, thousands of hours were spent talking with and working along side contractors, builders and woodworkers to understand how they work, the challenges they encounter, and their power tool needs. This was then designed and engineered into tools that boost productivity, enhance user comfort, and offer exceptional power and durability. The line will be available nationally in industrial supply channels and The Home Depot (the world’s largest home improvement specialty retailer) in the United States and Canada beginning October 1. Mr. Horst Pudwill, Chairman and CEO of TTI, said, “We are very excited about this new product launch as we have successfully expanded the product range into handheld corded and cordless tools in addition to the benchtop and stationary power tools. This innovative range of RIDGID branded tools is a result of intensive research and development. The launch positions TTI as a strong competitor in the professional power tool segment in North America, expanding on our leading position in the power tool category.” *RIDGID® is a registered trademark of Ridgid, Inc., part of Emerson Professional Tools, a business of St. -

Techtronic Industries Co. Ltd. Announcement Of

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. TECHTRONIC INDUSTRIES CO. LTD. 創 科 實 業 有 限 公 司 (Incorporated in Hong Kong with limited liability) (Stock code: 669) ANNOUNCEMENT OF RESULTS FOR THE YEAR ENDED DECEMBER 31, 2019 Highlights 2019 2018 US$’ US$’ million million Changes Revenue 7,667 7,021 +9.2% Gross profit margin 37.7% 37.2% +50 bps EBIT 673 607 +10.9% Profit attributable to Owners of the Company 615 552 +11.3% Basic earnings per share (US cents) 33.67 30.16 +11.6% Dividend per share (approx. US cents) 13.26 11.33 +17.0% ▪ Net profit grew 11.3% and sales expanded 9.2% ▪ Gross margin improved for the eleventh consecutive year ▪ Flagship Milwaukee Tool business continues to grow 20%+ in local currency ▪ RYOBI cordless sales delivered double-digit sales growth The board of directors (the “Directors” or the “Board”) of Techtronic Industries Company Limited (“TTI” or the “Company”) is pleased to announce the audited consolidated results of the Company and its subsidiaries (together, the “Group”) for the year ended December 31, 2019 together with the comparative figures in 2018. TTI is pleased to announce our 2019 performance achieved record profits marking a decade of revenue growth. We built on our strong first half performance by delivering record second half results, driven by the development of new products and expansion across all categories, verticals and geographies. -

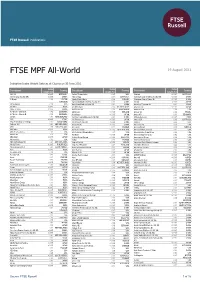

MPF All-World

2 FTSE Russell Publications 19 August 2021 FTSE MPF All-World Indicative Index Weight Data as at Closing on 30 June 2021 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) 1&1 AG <0.005 GERMANY Agilent Technologies 0.07 USA Alumina <0.005 AUSTRALIA 360 Security (A) (SC SH) <0.005 CHINA AGL Energy 0.01 AUSTRALIA Aluminum Corp of China (A) (SC SH) <0.005 CHINA 3i Group 0.02 UNITED Agnico Eagle Mines 0.02 CANADA Aluminum Corp of China (H) <0.005 CHINA KINGDOM Agricultural Bank of China (A) (SC SH) 0.01 CHINA Amada <0.005 JAPAN 3M Company 0.18 USA Agricultural Bank of China (H) 0.02 CHINA Amadeus IT Group SA 0.05 SPAIN 3M India <0.005 INDIA Ahold Delhaize 0.05 NETHERLANDS Amano Corp <0.005 JAPAN 3SBio (P Chip) <0.005 CHINA AIA Group Ltd. 0.23 HONG KONG Amazon.Com 2.28 USA A P Moller - Maersk A 0.02 DENMARK AIB Group <0.005 IRELAND Ambev SA 0.02 BRAZIL A P Moller - Maersk B 0.03 DENMARK Aica Kogyo <0.005 JAPAN Ambu A/S 0.01 DENMARK a2 Milk 0.01 NEW ZEALAND Aier Eye Hospital Group (A) (SC SZ) 0.01 CHINA Ambuja Cements <0.005 INDIA A2A <0.005 ITALY Ain Pharmaciez <0.005 JAPAN Amcor CDI 0.03 AUSTRALIA AAC Technologies Holdings 0.01 HONG KONG Air China (A) (SC SH) <0.005 CHINA Amdocs 0.02 USA Aalberts NV 0.01 NETHERLANDS Air China (H) <0.005 CHINA Ameren Corp 0.03 USA ABB 0.09 SWITZERLAND Air Liquide 0.12 FRANCE America Movil L 0.03 MEXICO ABB India <0.005 INDIA Air New Zealand <0.005 NEW ZEALAND American Airlines Group 0.01 USA Abbott Laboratories 0.31 USA Air Products & Chemicals Inc -

TTI: Tooling up for Asia

S UST 1015-046 KRISTIAAN HELSEN JEROEN VAN DEN BERG ARMAND GHIEUW TTI: Tooling up for Asia The way we differentiate ourselves from competitors is by developing breakthrough products that outperform our competition and that is why we are winning. […] We believe we will be the global leader in cordless [power tools] for years and decades to come. Joe Galli, CEO TTI1 On 19 August 2015, Techtronic Industries (TTI), a leading manufacturer of tools, outdoor products and vacuum cleaners, announced record revenues and profits for the first half of 2015. According to Joe Galli, the company CEO, TTI’s success could be attributed to the continuous roll-outs of innovative products; investments in productivity and automation; and highly targeted geographic expansion.2. Even though TTI’s star had been shining brightly its executives would not rest. They were always looking for methods to sustain the company’s growth in the global market. They predicted that in the next 10 years, Asia could become an important market for TTI. 3 Given the large number of possible entry markets, the company wanted to rank the Asian countries by level of market attractiveness. For those markets that seemed to offer the most attractive opportunity a range of other issues had to be addressed. What would the most suitable market entry strategy? A one size fits all approach was probably not workable. 1 Joe Galli, interview by Shery Ahn, Earnings Edge, Bloomberg, 20 August 2015. 2 Ibid. 3 Joe Galli, interview by author, Hong Kong, 11 August 2015. Jeroen van den Berg and Armand Ghieuw prepared this case under the supervision of Professor Kristiaan Helsen solely as a basis for class discussion. -

Techtronic Industries Company Limited

[For Immediate Release] TechTronic Industries Named “Innovator of the Year” and “Vendor of the Year” By The Home Depot for Ryobi Brand Products (HONG KONG, 16 October 2002) – TechTronic Industries Company Limited’s (“TTI”) (HKEx stock code 669; ADR symbol: TTNDY) partnership with The Home Depot (NYSE:HD) reached new highs as the world’s largest home improvement chain hailed TTI’s US subsidiary, Ryobi Technologies, Inc. (“Ryobi”), as “Vendor of the Year” and its first ever “Innovator of the Year”. In a special ceremony held at The Home Depot’s world headquarters in Atlanta, USA, Mr. Jerry Edwards, Executive Vice President of Merchandising of The Home Depot, singled out Ryobi’s 4-piece Super Combo as the most innovative product marketed by The Home Depot. Ryobi becomes the first ever winner of this new annual award. The 18-volt Super Combo combines a 5-1/2-in. circular saw, 1/2-in. drill, reciprocating saw, swiveling-head flashlight, two batteries, a charger and a sturdy plastic carrying case. For the past year, the kit has been sold at The Home Depot for US$199. “The innovation, price, performance and packaging really helped this product to stand out from the thousands of new products we evaluated this year,” said Mr. Jerry Edwards. “The 4-Piece Super Combo is a direct result of the close working relationship TTI has enjoyed with Home Depot,” said Mr. Bob Freitag, Ryobi’s Executive Vice President Sales and Business Development. “Our experience in engineering, coupled with Home Depot’s retail savvy, has turned out to be an incredibly synergistic relationship. -

The World's Most Active Consumer Goods Professionals

The USA's Most Active Consumer Goods Professionals on Social - July 2021 Industry at a glance: Why should you care? So, where does your company rank? Position Company Name LinkedIn URL Location Employees on LinkedIn No. Employees Shared (Last 30 Days) % Shared (Last 30 Days) 1 ECRM https://www.linkedin.com/company/ecrm_2/United States 219 57 26.03% 2 Oregon Tool https://www.linkedin.com/company/oregon-tool/United States 301 77 25.58% 3 Nutrabolt https://www.linkedin.com/company/nutraboltcorp/United States 300 73 24.33% 4 Oreck Corporation https://www.linkedin.com/company/oreck-corporation/United States 322 77 23.91% 5 C.A. Fortune https://www.linkedin.com/company/c-a-fortune-food-broker/United States 265 49 18.49% 6 Arrow International https://www.linkedin.com/company/arrow-international-inc-/United States 200 36 18.00% 7 Thrasio https://www.linkedin.com/company/thrasio/United States 907 156 17.20% 8 Boxed https://www.linkedin.com/company/boxed-com/United States 204 32 15.69% 9 BARK https://www.linkedin.com/company/bark-thedogcompany/United States 618 96 15.53% 10 Rad Power Bikes https://www.linkedin.com/company/rad-power-bikes/United States 341 46 13.49% 11 Glossier https://www.linkedin.com/company/glossier/United States 406 52 12.81% 12 Aprilaire https://www.linkedin.com/company/aprilaire/United States 360 45 12.50% 13 Gemline https://www.linkedin.com/company/gemline/United States 217 26 11.98% 14 Cresco Labs https://www.linkedin.com/company/cresco-labs/United States 920 110 11.96% 15 Greenworks Tools https://www.linkedin.com/company/greenworkstools/United