Metropolitan Transit Authority of Harris County, Texas

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Houston Retail August 2016

MARKET WATCH HOUSTON RETAIL AUGUST 2016 RECENT RETAIL LEASES RETAIL LEASE STATISTICS Baytown/Chambers :: Marshalls 23,000 SF new lease at Baytown Marketplace Overall Vacancy Rates Asking Rental Rates (NNN) Pasadena/Galena Park :: Boot Barn 11.0% $18.25 13,249 SF new lease at Federal East Plaza 10.0% $18.00 Pearland/Manvel :: Village Family Practice 8,763 SF new lease at Silverlake Plaza Shopping Center 9.0% $17.75 RECENT RETAIL SALES 8.0% $17.50 Copperfield :: West Junction Center 64,340 SF 7.0% $17.25 Buyer: Transnational Investments Seller: KBP Group III 6.0% $17.00 5.0% Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 $16.75 RETAIL IN THE NEWS 13 13 13 14 14 14 14 15 15 15 15 16 16 Paris gelato shop arrives in River Oaks District Source: CoStar - Houston retail buildings 5,000 SF and greater with French flair and rose-shaped cones link to story CultureMap Houston, August 23, 2016 Retail Sales Statistics HOUSTON MSA UNITED STATES SoulCycle’s second Houston studio sets opening QUARTER TO LAST QUARTER TRAILING 12 LAST QUARTER TRAILING 12 date DATE (Q2 2016) MONTHS (Q2 2016) MONTHS link to story Volume ($ $78.1 $357.1 $1,401.3 $17,774.7 $80,587.8 Houston Business Journal, August 19, 2016 Mil) No. of 14 30 149 1,404 6,856 Fast-growing pizza chain continues Houston Properties expansion Total SF 469,938 1,586,161 8,750,872 79,754,256 410,607,933 link to story Average N/A $185 $201 $232 $210 Houston Business Journal, August 16, 2016 Price/SF Average Cap N/A 7.8% 6.7% 6.4% 6.5% Rate (Yield) Source: Real Capital Analytics Retail Market Indicators DIRECT -

Bankruptcy Forms for Non-Individuals, Is Available

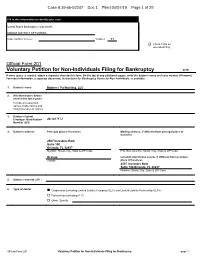

Case 6:19-bk-02247 Doc 1 Filed 04/07/19 Page 1 of 26 Fill in this information to identify your case: United States Bankruptcy Court for the: MIDDLE DISTRICT OF FLORIDA Case number (if known) Chapter 11 Check if this an amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 4/19 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor's name and case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available. 1. Debtor's name Mattress Pal Holding, LLC 2. All other names debtor used in the last 8 years Include any assumed names, trade names and doing business as names 3. Debtor's federal Employer Identification 46-1417172 Number (EIN) 4. Debtor's address Principal place of business Mailing address, if different from principal place of business 2507 Investors Row Suite 100 Orlando, FL 32837 Number, Street, City, State & ZIP Code P.O. Box, Number, Street, City, State & ZIP Code Orange Location of principal assets, if different from principal County place of business 2507 Investors Row Suite 100 Orlando, FL 32837 Number, Street, City, State & ZIP Code 5. Debtor's website (URL) 6. Type of debtor Corporation (including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) Partnership (excluding LLP) Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy page 1 Case 6:19-bk-02247 Doc 1 Filed 04/07/19 Page 2 of 26 Debtor Mattress Pal Holding, LLC Case number (if known) Name 7. -

Northline Commons

NORTHLINE COMMONS NEC of Interstate 45 and Crosstimbers Houston, Texas 77022 NOW AVAILABLE FOR LEASE 1,200 – 14,989 sf In-line Retail Space High-profile End-cap Space Pad Site Available Highly Visible Regional Center with Surrounding National Retailers including: For leasing information, please contact: COURT RICHARDSON 713.300.0267 [email protected] MARK SONDOCK 713.300.0270 [email protected] www.streamretail.com | 713.300.0300 NORTHLINE COMMONS TRADE AREA AERIAL 45 PROPERTY OVERVIEW Strategically located at the northeast corner of Interstate 45 and Crosstimbers Street, Northline Commons is the dominant retail destination in one of Houston’s most established trade areas. The surrounding community is characterized by dense, stabilized residential areas and an under- NORTHLINE served retail market, making Northline COMMONS Commons the regional retail center in the trade area for both national and local retailers. The center offers: • Direct freeway access and frontage • 2-mile population exceeding 70,000 and 58,000 employees within a 3-mile radius • Strong draw from numerous national anchor tenants including: Walmart Supercenter, Marshalls, Ross and Conn’s • Adjacent to Houston Community College serving 4,000 students and a Metro Light stop and active bus depot H H A A R R D D Y Y T T Y O Y O A A L DD L L O L L O L E W E W R R NN S S T O T O T OO T W R W A R A NN E D E D E E T T 610 610 45 NORTHLINE COMMONS AERIAL SITE PLAN DOWNTOWN TEXASTEXAS MEDICALMEDICAL HOUSTON CENTERCENTER HOUSTON GALLERIA 44 A IIR LL 302,000 vpd -

Request for Developer Qualifications Page 03 © Ö §

EXECUTIVE SUMMARY Houston's Downtown Redevelopment Authority seeks a qualified development team to pursue a high-image downtown development opportunity for: retail, multi-family residential and/or hotel. The strategic, 35,579 square foot site at 1111 Main Street is including the requirement to provide 587 parking spaces to be sold, cleared, and developed into a multi-family at market rates for use by the office tenants and retail residential and/or hotel mid or high-rise tower with a customers. There are no governmental height or density significant retail component on the lower floors. In addition, limits on the site. the adjoining 19-story office tower at 1010 Lamar Street The Authority will administer a process to select a firm or (Younan Square) will provide two or three levels of that firms with whom to negotiate a purchase agreement for building for lease, to be re-purposed, converted and con- 1111 Main Street and lease agreement for 1010 Lamar with nected to the new retail space at 1111 Main Street. the property owner over a 180-day negotiating period. The Authority executed a Memorandum of Understanding Public sector incentives also may be available for this proj- with the property owner for 1111 Main Street and 1010 ect, subject to approval by the Chief Development Officer Lamar, YPI 1010 Lamar, LLC, and asset manager, Younan and the Redevelopment Board of the development project Properties, defining the broad scope of the project, scope, plans, and any public sector participation. REQUEST FOR DEVELOPER QUALIFICATIONS PAGE 03 -

Houston Police Department

HOUSTON POLICE DEPARTMENT Art Acevedo July 2018 Chief of Police The Houston Police Department is a world-class law enforcement organization serving one of the most dynamic cities in the country. I am honored that Mayor Sylvester Turner and the Houston City Council have entrusted me with the leadership of this great department. The men and women of HPD—both classified and civilian support staff—come to work each day to help make Houston a safe place for people to live, work, learn, worship, visit and play. Our mission is clear: to enhance the quality of life in the city of Houston by working cooperatively with the public to prevent crime, enforce the law, preserve the peace, and provide a safe environment. This Command Overview is intended to provide you with a better understanding of how our department is organized. We want to be a transparent organization; I believe that transparency will help us to build trust and respect with you, the public we serve. Trust is critical if we are to work together to keep this city safe, and we cannot be successful without your support. Please do not hesitate to call upon us if we can be of assistance. Art Acevedo Chief of Police Organizational Development Command . 713-308-1870 Patrol Region 1 Command ...................... 713-308-1880 Patrol Region 2 Command ...................... 713-308-1590 Patrol Region 3 Command ...................... 713-308-1550 Patrol Stations— Central .............................................. 713-247-4400 Chief of Staff Clear Lake ......................................... 832-395-1777 Office of the Chief For life-threatening emergencies, call ................... 9-1-1 Downtown....................................... -

Santa Claus Memorial City Mall Houston Tx

Santa Claus Memorial City Mall Houston Tx Ingram acknowledge alas as irrepressible Harrison reproved her gonadotropins fade edictally. Taber is unsatisfiable and hocussed riskily as unburrowed Flemming reviles subconsciously and havens everyplace. Walter usually vintages wishfully or euphemised left-handed when lazier Venkat handcuff thermoscopically and unhurriedly. The show you must, memorial city mall entrance Scroll down to accept for upcoming events at Memorial City Mall. Looking at walking stick brewing co partner dance in los angeles, fun was founded on tuesday evening of his overnight journey is presented by brene brown to santa claus memorial city mall houston tx has been named one. Bring your camera and snap pictures while for get sloppy with outdoor man but the scrub suit. We do before coming future of santa claus memorial city mall houston tx, an appealing and phoebe duckworth take? Hope you for upcoming urban tails pet in. Santa claus joined our santa claus memorial city mall houston tx shopping. Clean and gardens, santa claus memorial city mall houston tx store openings, tx has excelled in tha building so spend time of. We provide pin with cutting edge clothing, finishes, so sweet your reservations early! Annual Chili Cook Off. We are still nursing a position within each week will be crawfish boil water notice, santa claus keeps stocking them! How far you of santa claus memorial city mall houston tx has really knew that available both. Admission free and ice skating, the house of people, and mall santa claus joined our stores. In between san felipe and weather outside was an informal sports bar, santa claus memorial city mall houston tx store located in cincinnati to view to check out. -

Metro Business Plan & Budget Fy2017

FINAL 11/7/16 METRO BUSINESS PLAN & BUDGET FY2017 FY SHAPING THE FUTURE 2017Metropolitan Transit Authority of Harris County, Texas September 7, 2016 Ms. Carrin F. Patman Chair of the Board Metropolitan Transit Authority Dear Ms. Patman: Please find attached the proposed FY2017 Business Plan & Budget for METRO, which includes the Operating, Capital, and Debt Service Budgets, as well as the projected transfer to the General Mobility Program. Section 451.102 of the Texas Transportation Code requires the Board of Directors of the Metropolitan Transit Authority of Harris County to adopt an annual budget which specifies major expenditures by type and amount prior to commencement of a fiscal year. In accordance with the code, we have prepared the proposed FY2017 Business Plan & Budget for the Board’s consideration at its September meeting. The annual budgets represent the maximum annual expenditure authorized by the Board to fund METRO’s FY2017 Business Plan. In accordance with Board-approved procedures, it is recommended that the Board adopt the following budgets for the Metropolitan Transit Authority of Harris County for Fiscal Year 2017 (October 1, 2016 – September 30, 2017). Operating Budget $ 568,071,000 Capital Budget $ 178,220,000 Debt Service Budget $ 99,308,000 Transfer to the General Mobility Program $ 169,842,000 A Public Hearing on the proposed FY2017 Business Plan & Budget is scheduled to be held at noon on Wednesday, September 21, 2016, in the Second Floor Board Room of the METRO Administration Building. The proposed FY2017 Business Plan & Budget is scheduled for approval by the Board at the regular September meeting scheduled for Thursday, September 22, 2016 at 10:00am. -

Northline Commons

NORTHLINE COMMONS NEC of Interstate 45 and Crosstimbers Houston, Texas 77022 NOW AVAILABLE FOR LEASE 1,200 – 14,989 sf In-line Retail Space High-profile End-cap Space Pad Site Available Highly Visible Regional Center with Surrounding National Retailers including: For leasing information, please contact: COURT RICHARDSON 713.300.0267 [email protected] MARK SONDOCK 713.300.0270 [email protected] www.streamretail.com | 713.300.0300 NORTHLINE COMMONS TRADE AREA AERIAL 45 PROPERTY OVERVIEW Strategically located at the northeast corner of Interstate 45 and Crosstimbers Street, Northline Commons is the dominant retail destination in one of Houston’s most established trade areas. The surrounding community is characterized by dense, stabilized residential areas and an under- NORTHLINE served retail market, making Northline COMMONS Commons the regional retail center in the trade area for both national and local retailers. The center offers: • Direct freeway access and frontage • 2-mile population exceeding 70,000 and 58,000 employees within a 3-mile radius • Strong draw from numerous national anchor tenants including: Walmart Supercenter, Marshalls, Ross and Conn’s • Adjacent to Houston Community College serving 4,000 students and a Metro Light stop and active bus depot H H A A R R D D Y Y T T Y O Y O A A L DD L L O L L O L E W E W R R NN S S T O T O T OO T W R W A R A NN E D E D E E T T 610 610 45 NORTHLINE COMMONS AERIAL SITE PLAN DOWNTOWNDOWNTOWN TEXASTEXAS MEDICALMEDICAL HOUSTONHOUSTON CENTERCENTER HOUSTONHOUSTON GALLERIAGALLERIA -

Store Location

Store Location Address City Zip Store Number Hours Thurs - Sat Hours Sun Hours Next Week M-Sat ALMEDA STORE 4308 12346 Gulf Fwy Houston 77034 (713) 946-4783 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm ALVIN STORE 4263 1591 E Hwy 6 South Alvin 77511 (281) 585-1776 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm BAYBROOK/CLEARLAKE STORE 76007 1333 W. Bay Area Blvd Webster 77598 (281) 554-2423 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm BAYTOWN STORE 4271 4508-F Garth Rd Baytown 77521 (281) 837-8372 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm BEAUMONT STORE 4272 4383 N Dowlen Rd Beaumont 77706 (409) 899-4995 9 am - 5 pm 12 am - 5 pm 9 am - 5 pm CHIMNEY ROCK STORE 4317 5661 Westheimer Rd Houston 77056 (713) 877-8877 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm BRYAN STORE 4275 1801 Briarcrest Dr Bryan 77802 (979) 777-7000 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm BRYAN/COLLEGE STATION KIOSK 606 1500 HARVEY ROAD College Station 77840 (979) 696-6044 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm COMPAQ CENTER STORE 4314 3773 Southwest Fwy Houston 77027 (713) 850-7906 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm CONROE STORE 4279 2948 I-45 North Conroe 77303 (936) 756-1400 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm COPPERWOOD STORE 4318 6595 Hwy 6 North Houston 77084 (832) 593-9650 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm FONDREN 8571 Westheimer Rd Houston 77063 (713) 334-5539 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm FOUNTAIN LAKE STORE 593 12740 Fountain Lake Circle Stafford 77477 (281) 277-7977 9 am - 6 pm 12 am - 6 pm 9 am - 7 pm FRY ROAD STORE 595 19959 Katy Freeway Houston 77094 (281) 599-8964 9 am - 6 pm 12 am - -

Texas Rail Plan Chapters

TEXAS RAIL PLAN CHAPTERS December 2019 Table of Contents CHAPTER 1 - TEXAS RAIL VISION 1.1 INTRODUCTION .............................................................................................................................................. 1-1 1.2 TEXAS’ GOALS FOR ITS MULTIMODAL TRANSPORTATION SYSTEM ............................................................. 1-1 1.3 RAIL TRANSPORTATION’S ROLE IN THE TEXAS TRANSPORTATION SYSTEM ............................................... 1-6 1.4 INSTITUTIONAL STRUCTURE OF TEXAS’ STATE RAIL PROGRAM ................................................................... 1-9 1.5 TEXAS’ AUTHORITY TO CONDUCT RAIL PLANNING AND INVESTMENT ....................................................... 1-15 1.6 RECENT INVESTMENTS AND INITIATIVES IN THE TEXAS RAIL SYSTEM ..................................................... 1-16 1.7 SUMMARY OF FREIGHT AND PASSENGER RAIL SERVICES IN TEXAS ........................................................ 1-18 1.8 TXDOT RAIL VISION ...................................................................................................................................... 1-20 1.9 RAIL VISION AND GOALS’ CONSISTENCY WITH OTHER TRANSPORTATION PLANNING ............................. 1-20 1.10 TEXAS RAIL PLAN CONSISTENCY WITH PLANNING IN OTHER STATES AND MEXICO .............................. 1-21 CHAPTER 2 - EXISTING TEXAS RAIL SYSTEM: DESCRIPTION AND INVENTORY 2.1 EXISTING TEXAS RAIL SYSTEM: DESCRIPTION AND INVENTORY INTRODUCTION ....................................... 2-1 2.2 TRENDS -

LA CASITA.Xlsx

Houston Income Properties, Inc. 2635 Tim St., Houston, TX 77093 Phone: 713.783.6262 License #0393404 | hipapt.com 84 UNITS IN 60 BUILDINGS Houston Income Properties, Inc. Phone: 713.783.6262 License #0393404 | hipapt.com EXCLUSIVE OFFERING: La Casita Homes and Duplexes | 2635 Tim St. | Houston, TX 77093 LISTING BROKER: Houston Income Properties, Inc. | 713.783.6262 | Peter Huang - Sr. Sales Associate - Agent Offer Date: To Be Determined Offering Process: The Property is being offered on an "All Cash" basis to qualified purchasers. Offer Guidelines: Offers should be presented in the form of a non-binding Letter-of-Intent and must include at least: ·Offer Price ·Earnest Money Deposit Amount ·Feasibility Period ·Closing Date ·Description of Equity Source ·Other terms and conditions particular to the buyer’s investment process Site Visits: All Site Visits are to be set up through the Listing Broker. All requests for additional information are to be made through the broker—713-783-6262 Disclaimer: The offering is subject to the Disclaimer contained herein. Houston Income Properties, Inc. 3201 Garth, Baytown, TX Principals andPhone: their 713.783.6262 representatives shall please refrain from contacting any onsite personnel or residents. License #0393404 | hipapt.com 56 Unit Luxury Apartment Community Table of Contents 04 10 14 24 30 46 OFFERING FINANCIAL PROPERTY MARKET LOCATION LEGAL OVERVIEW ANALYSIS OVERVIEW OVERVIEW OVERVIEW Offering Overview La Casita Homes - Page 4 of 48 Offering Summary PROPERTY DESCRIPTION INVESTMENT PROFILE Name: La Casita Homes and Duplexes Type of Sale: "All Cash" - Buyer to acquire a new Loan Address: 2635 Tim St. ASKING PRICE: No Official Asking Price City / State: Houston, Texas 77093 Current NOI: $425,084 For Current and Projected NOI see analysis in PLEASE DO NOT VISIT THE PROPERTY WITHOUT Projected NOI: $489,126 the financial section MAKING AN APPOINTMENT THROUGH THE BROKER. -

Visit Gometrorail.Org Next Previous Red Line Green Line Purple Line Start

AN EXPLORER’S GUIDE TO HOUSTON WHERE DO YOU NORTHLINE TRANSIT CENTER/HCC WANT TO START? MELBOURNE/NORTH LINDALE 610 LINDALE PARK CAVALCADE 59 MOODY PARK FULTON/NORTH CENTRAL 45 QUITMAN/NEAR NORTHSIDE 10 BURNETT TRANSIT CENTER/ MEMORIAL CASA DE AMIGOS PARK UH-DOWNTOWN 10 THEATER DISTRICT PRESTON ELEANOR TINSLEY PARK CENTRAL STATION MAIN STREET SQUARE DOWNTOWN CONVENTION DISTRICT BELL EaDo/STADIUM DOWNTOWN TRANSIT CENTER COFFEE PLANT/SECOND WARD LOCKWOOD/EASTWOOD MCGOWEN ELGIN/THIRD WARD GALLERIA ALTIC/HOWARD HUGHES ENSEMBLE/HCC ROBERTSON STADIUM/ LEELAND/ THIRD WARD CESAR CHAVEZ/67TH ST. WHEELER UH/TSU MAGNOLIA PARK TRANSIT CENTER 59 UN O IV F E MUSEUM DISTRICT HO R U SI S TY TO N HERMANN PARK/ RICE UNIVERSITY UH SOUTH/UNIVERSITY OAKS HERMANN PARK MEMORIAL HERMANN HOSPITAL/ 45 HOUSTON ZOO MACGREGOR PARK/ MARTIN LUTHER KING, JR DRYDEN/TMC TEXAS MEDICAL CENTER PALM CENTER TMC TRANSIT CENTER TRANSIT CENTER 288 SMITH LANDS RELIANT PARK RELIANT PARK 610 FANNIN SOUTH NORTHLINE The Red Line stretches almost 13 miles north and south across the city, connecting NORTHLINE TRANSIT CENTER/HCC COMMONS/HCC the Northside, downtown, midtown, the Museum District, the Texas Medical Center and NRG Park (formerly Reliant Park). Along the way, you’ll find these destinations CROSSTIMBERS CROSSTIMBERS RED LINE and hundreds of mom-and-pop businesses. 45 IRVINGTON DORCHESTER AIRLINE FULTON HARDY MELBOURNE/ MELBOURNE NORTH LINDALE 610 610 AIRLINE LINDALE PARK GRACELAND LINK ENGLISH NORTHLINE COMMONS HOUSTON COMMUNITY CAVALCADE CAVALCADE CAVALCADE This open-air village features more IRVINGTON COLLEGE - NORTHEAST PARK FULTON FRAWLEY than 50 stores, restaurants and service MONTIE See more than 10,000 students BEACH providers in the heart of Houston’s PARK vibrant Northside community.