Frequently Asked Questions on Repo

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Repo Haircuts and Economic Capital: a Theory of Repo Pricing Wujiang Lou1 1St Draft February 2016; Updated June, 2020

Repo Haircuts and Economic Capital: A Theory of Repo Pricing Wujiang Lou1 1st draft February 2016; Updated June, 2020 Abstract A repurchase agreement lets investors borrow cash to buy securities. Financier only lends to securities’ market value after a haircut and charges interest. Repo pricing is characterized with its puzzling dual pricing measures: repo haircut and repo spread. This article develops a repo haircut model by designing haircuts to achieve high credit criteria, and identifies economic capital for repo’s default risk as the main driver of repo pricing. A simple repo spread formula is obtained that relates spread to haircuts negative linearly. An investor wishing to minimize all-in funding cost can settle at an optimal combination of haircut and repo rate. The model empirically reproduces repo haircut hikes concerning asset backed securities during the financial crisis. It explains tri-party and bilateral repo haircut differences, quantifies shortening tenor’s risk reduction effect, and sets a limit on excess liquidity intermediating dealers can extract between money market funds and hedge funds. Keywords: repo haircut model, repo pricing, repo spread, repo formula, repo pricing puzzle. JEL Classification: G23, G24, G33 A repurchase agreement (repo) is an everyday securities financing tool that lets investors borrow cash to fund the purchase or carry of securities by using the securities as collateral. In its typical transaction form, the borrower of cash or seller sells a security to the lender at an initial purchase price and agrees to purchase it back at a predetermined repurchase price on a future date. On the repo maturity date T, the lender (or the buyer) sells the security back to the borrower. -

Informed and Strategic Order Flow in the Bond Markets

Informed and Strategic Order Flow in the Bond Markets Paolo Pasquariello Ross School of Business, University of Michigan Clara Vega Simon School of Business, University of Rochester and FRBG We study the role played by private and public information in the process of price formation in the U.S. Treasury bond market. To guide our analysis, we develop a parsimonious model of speculative trading in the presence of two realistic market frictions—information heterogeneity and imperfect competition among informed traders—and a public signal. We test its equilibrium implications by analyzing the response of two-year, five-year, and ten-year U.S. bond yields to order flow and real-time U.S. macroeconomic news. We find strong evidence of informational effects in the U.S. Treasury bond market: unanticipated order flow has a significant and permanent impact on daily bond yield changes during both announcement and nonannouncement days. Our analysis further shows that, consistent with our stylized model, the contemporaneous correlation between order flow and yield changes is higher when the dispersion of beliefs among market participants is high and public announcements are noisy. (JEL E44, G14) Identifying the causes of daily asset price movements remains a puzzling issue in finance. In a frictionless market, asset prices should immediately adjust to public news surprises. Hence, we should observe price jumps only during announcement times. However, asset prices fluctuate significantly during nonannouncement days as well. This fact has motivated the introduction of various market frictions to better explain the behavior The authors are affiliated with the Department of Finance at the Ross School of Business, University of Michigan (Pasquariello) and the University of Rochester, Simon School of Business and the Federal Reserve Board of Governors (Vega). -

Government Bonds Have Given Us So Much a Roadmap For

GOVERNMENT QUARTERLY LETTER 2Q 2020 BONDS HAVE GIVEN US SO MUCH Do they have anything left to give? Ben Inker | Pages 1-8 A ROADMAP FOR NAVIGATING TODAY’S LOW INTEREST RATES Matt Kadnar | Pages 9-16 2Q 2020 GOVERNMENT QUARTERLY LETTER 2Q 2020 BONDS HAVE GIVEN US SO MUCH EXECUTIVE SUMMARY Do they have anything left to give? The recent fall in cash and bond yields for those developed countries that still had Ben Inker | Head of Asset Allocation positive yields has left government bonds in a position where they cannot provide two of the basic investment services they When I was a student studying finance, I was taught that government bonds served have traditionally provided in portfolios – two basic functions in investment portfolios. They were there to generate income and 1 meaningful income and a hedge against provide a hedge in the event of a depression-like event. For the first 20 years or so an economic disaster. This leaves almost of my career, they did exactly that. While other fixed income instruments may have all investment portfolios with both a provided even more income, government bonds gave higher income than equities lower expected return and more risk in the and generated strong capital gains at those times when economically risky assets event of a depression-like event than they fell. For the last 10 years or so, the issue of their income became iffier. In the U.S., the used to have. There is no obvious simple income from a 10-Year Treasury Note spent the last decade bouncing around levels replacement for government bonds that similar to dividend yields from equities, and in most of the rest of the developed world provides those valuable investment government bond yields fell well below equity dividend yields. -

Repurchase Agreements, Securities Lending, Gold Swaps and Gold Loans: an Update

SNA/M2.04/26 Repurchase agreements, securities lending, gold swaps and gold loans: An update Prepared by the IMF for the December 2004 Meeting of the Advisory Expert Group on National Accounts (For information) This paper is for the information of the members of the Advisory Expert Group (AEG), regarding the currently accepted treatment of repurchase agreements, securities lending without cash collateral1, gold loans, and gold swaps2. The paper also sets out areas where work is continuing by the IMF Committee on Balance of Payments (Committee) and on which the Committee will provide further reports in due course. Repurchase agreements and securities lending without cash collateral Background A securities repurchase agreement (repo) is an arrangement involving the sale of securities at a specified price with a commitment to repurchase the same or similar securities at a fixed price on a specified future date. Margin payments may also be made3. A repo viewed from the point of view of the cash provider is called a reverse repo. When the funds are repaid (along with an interest payment) the securities are returned to the “cash taker”4. The 1 The term securities (or stock or bond) lending is sometimes used to describe both types of reverse transactions described in this note. In order to distingush between those used involving the exchange of cash and those that do not involve the exchange of cash, this note uses the term “repurchase agreements” for those involving cash and “securities lending without cash collateral” for those not involving the exchange of cash. 2 A fuller description of repurchase agreements, securities lending, gold loans and gold swaps can be found at http://www.imf.org/external/pubs/ft/bop/2001/01-16.pdf 3 “Margin” represents the value of the securities delivered that is in excess of the cash provided. -

IN the UNITED STATES DISTRICT COURT for the DISTRICT of COLORADO Judge R

Case 1:18-cv-01700-RBJ Document 38 Filed 12/06/19 USDC Colorado Page 1 of 15 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLORADO Judge R. Brooke Jackson Civil Action No. 18-cv-01700-RBJ CHERRY HILLS FARM COURT, LLC, Plaintiff, v. FIRST AMERICAN TITLE INSURANCE COMPANY, Defendant. ORDER ON MOTIONS FOR SUMMARY JUDGMENT This matter is before the Court on defendant First American Title Insurance Company (“First American”)’s motion for summary judgment [ECF No. 30] and plaintiff Cherry Hills Farm Court, LLC (“Cherry Hills”)’s motion for summary judgment [ECF No. 31]. For the reasons stated herein, First American’s motion is GRANTED and Cherry Hill’s motion is DENIED. I. BACKGROUND This case arises out of a title insurer’s decision not to cover a counterclaim made against an insured by a third party. The insured, Cherry Hills, is a land developer that purchased real property located at 2 Cherry Hills Farm Court, Englewood, Colorado 80113 (the “property”). ECF No. 3 ¶ 8. On June 23, 2015 First American issued title insurance to Cherry Hills regarding this property. ECF No. 30 ¶ 1. The title insurance policy covered loss or damage by ten specified risks, including “[a]ny defect in or lien or encumbrance on the Title.” ECF No. 30-1 at FATIC 000620. First American agreed to pay “costs, attorneys’ fees, and expenses incurred in 1 Case 1:18-cv-01700-RBJ Document 38 Filed 12/06/19 USDC Colorado Page 2 of 15 defense of any matter insured against by [the] policy, but only to the extent provided in the Conditions.” ECF No. -

DIVIDEND GROWERS DOMINATE OTHER DIVIDEND CATEGORIES June 7, 2021

DIVIDEND GROWERS DOMINATE OTHER DIVIDEND CATEGORIES June 7, 2021 Dividend growers outperformed all dividend categories for the past 48 1/4 years with less risk. This is our conclusion based on data provided by Ned Davis Research. The research focuses on dividend payers, non-dividend payers, and dividend cutters. Note that the pattern of dividend growers outperformance holds for both the entire period of analysis and each sub-period (First Table). It also holds that growers experienced lower volatility for both the entire period and each sub-period (Second Table). In this note, we address why we think this phenomenon exists and what it could mean to investors. RETURN BY DIVIDEND CATEGORY (ANNUAL) Period Increased Paid No Change Not Paid Cut 1973-79 5.9% 5.3% 4.9% 1.7% -3.9% 1980-89 17.8% 16.3% 12.8% 8.6% 8.4% 1990-99 13.2% 12.0% 9.4% 10.3% 6.3% 2000-09 3.5% 2.4% 0.3% -6.5% -12.2% 2010-19 12.9% 11.6% 7.9% 9.3% -1.1% 1973-April 21 10.6% 9.5% 7.0% 4.8% -0.8% VOLATILITY BY DIVIDEND CATEGORY (ANNUAL) Period Increased Paid No Change Not Paid Cut 1973-79 19.2% 19.5% 20.7% 25.5% 23.7% 1980-89 17.3% 17.6% 18.9% 21.2% 21.5% 1990-99 13.9% 13.9% 14.4% 18.5% 17.1% 2000-09 15.9% 18.1% 20.1% 27.2% 31.8% 2010-19 12.7% 13.4% 15.8% 16.1% 21.9% 1973-April 21 16.1% 16.9% 18.5% 22.2% 25.1% Source: Ned Davis Research; WCA WHY DIVIDEND GROWERS GENERATE SUPERIOR RISK-ADJUSTED RETURNS We believe there are five main reasons why investors should prefer dividend growers based on years of research and study. -

Use of Leverage, Short Sales, and Options by Mutual Funds

Use of Leverage, Short Sales, and Options by Mutual Funds Paul Calluzzo, Fabio Moneta, and Selim Topaloglu* This draft: March 2017 Abstract We study the use of leverage, short sales, and options by equity mutual funds. Consistent with agency-induced motives for the use of these complex instruments, we find that they are often used by poorly monitored funds, and are associated with poor outcomes for investors such as lower performance, higher idiosyncratic risk, more negative skewness, greater kurtosis, and higher fees. Consistent with moral hazard, we also find that mutual funds that use these instruments hold riskier equity positions. Mutual funds attempt to use complex instruments to reduce the risk of their portfolios but in an imperfect and costly way. JEL Classification: G11, G23 Keywords: mutual funds, leverage, short sales, options, complex instruments, fees, performance, risk * Smith School of Business, Queen's University, 143 Union Street, Kingston, Ontario K7L 3N6, Canada. Emails: [email protected], [email protected], and [email protected]. We thank George Aragon, Laurent Barras and seminar participants at the 2nd Smith-Ivey Finance Workshop and the 2016 Telfer Annual Conference on Accounting and Finance for their helpful comments. Electronic copy available at: https://ssrn.com/abstract=2938146 I can resist anything except temptation. -Oscar Wilde 1. Introduction Over the past fifteen years there has been a rise in the complexity of mutual funds as more funds are given the authority to use leverage, short sales, and options. Over this period 42.5% of domestic equity funds have reported using at least one of these instruments. -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

Housing and Real Property

ISSUE 139 | DECEMBER 2019 Malpractice Prevention Education for Oregon Lawyers LAW UPDATES Housing and Real Property RECORDING ELECTRONIC DOCUMENTS HB 2460 provides that the transferee of a tax-deferred homestead property is liable to Department of 2019 Oregon Laws Ch. 402 (HB 2425) Revenue for amounts of outstanding deferred property HB 2425 allows the county clerk to record taxes only if transferee is using the homestead more electronic documents and documents bearing an than 90 days following the death of the qualifying electronic signature. The bill provides that the taxpayer, and if the transferee is a potential recipient county clerk may charge for electronic delivery of of the homestead property under intestate succession, record or file images. by devise, from the estate of the deceased taxpayer, or by gift or assignment from the insolvent taxpayer. LIEN INFORMATION STATEMENTS HB 2460 took effect on September 29, 2019. 2019 Oregon Laws Ch. 140 (HB 2459) HOMESTEAD PROPERTY TAX HB 2459 provides that a person holding an DEFERRAL PROGRAM encumbrance against real property may request an itemized statement of the amount necessary to 2019 Oregon Laws Ch. 591 (HB 2587) pay off another encumbrance from the person that Prior to passage of this bill, the statute prohibited holds the other encumbrance on the same property. the owner of homestead tax-deferred property from The person that receives a request may provide the pledging said property as security for a reverse itemized statement without permission from the mortgage. This bill amends ORS 311.700 to provide obligor unless federal or state law requires obligor’s that real property that secures a reverse mortgage consent. -

Collateral Control Services

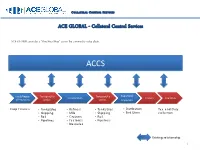

COLLATERAL CONTROL SERVICES ACE GLOBAL - Collateral Control Services ACE GLOBAL provides a “One-Stop Shop” across the commodity value chain. ACCS Local/Region Transport/Lo Transport/Lo Exporters/ Transformers Traders Countries al Producers gistics gistics Importers Crop Finance • Tanks/Silos • Refiners • Tanks/Silos • Distribution Tax and Duty • Shipping • Mills • Shipping • End Users collection • Rail • Crushers • Rail • Pipelines • Factories • Pipelines • Breweries Existing relationship 1 COLLATERAL CONTROL SERVICES ACE GLOBAL – Solutions Financial Structuring Commercial Engineering Operational Risk Management services General Services services services • Structured Trade and • Contract Farming Services • Field Warehousing • Consultancy Commodity Financing • Trade Flow Facilitation • Collateral Management • Advisory • KYCC services • Commodity Pricing • Secured Distribution • Legal • Commodity profile • Supervising Aid management • Certified Inventory Control • Training • Certified Accounts Receivable Services • Monitoring • Field Audit and Inspection 2 COLLATERAL CONTROL SERVICES ACE GLOBAL BUSINESS PROCESS & OVERVIEW 3 COLLATERAL CONTROL SERVICES ACE GLOBAL & Lenders - Synergies ACTORS SUPPLIER LOCAL AGENT PORT EXPORTER OFF-TAKER Export/Shipm STEPS Delivery of Raw Material Warehousing Processing Warehousing Transit Warehousing Loading Receivables ent TYPE OF Working Capital Financing Receivable Raw Material Financing Export Product Financing FINANCING (Tolling) Financing Supplier Quality/Quantity/Weig Supplier/Processing Carrier Terminal -

BASIC BOND ANALYSIS Joanna Place

Handbooks in Central Banking No. 20 BASIC BOND ANALYSIS Joanna Place Series editor: Juliette Healey Issued by the Centre for Central Banking Studies, Bank of England, London EC2R 8AH Telephone 020 7601 3892, Fax 020 7601 5650 December 2000 © Bank of England 2000 ISBN 1 85730 197 8 1 BASIC BOND ANALYSIS Joanna Place Contents Page Abstract ...................................................................................................................3 1 Introduction ......................................................................................................5 2 Pricing a bond ...................................................................................................5 2.1 Single cash flow .....................................................................................5 2.2 Discount Rate .........................................................................................6 2.3 Multiple cash flow..................................................................................7 2.4 Dirty Prices and Clean Prices.................................................................8 2.5 Relationship between Price and Yield .......................................................10 3 Yields and Yield Curves .................................................................................11 3.1 Money market yields ..........................................................................11 3.2 Uses of yield measures and yield curve theories ...............................12 3.3 Flat yield..............................................................................................12 -

Share-Based Payments – IFRS 2 Handbook

Share-based payments IFRS 2 handbook November 2018 kpmg.com/ifrs Contents Variety increases complexity 1 1 Introduction 2 2 Overview 8 3 Scope 15 4 Classification of share-based payment transactions 49 5 Classification of conditions 66 6 Equity-settled share-based payment transactions with employees 81 7 Cash-settled share-based payment transactions with employees 144 8 Employee transactions – Choice of settlement 161 9 Modifications and cancellations of employee share-based payment transactions 177 10 Group share-based payments 208 11 Share-based payment transactions with non-employees 257 12 Replacement awards in a business combination 268 13 Other application issues in practice 299 14 Transition requirements and unrecognised share-based payments 317 15 First-time adoption of IFRS 320 Appendices I Key terms 333 II Valuation aspects of accounting for share-based payments 340 III Table of concordance between IFRS 2 and this handbook 374 Detailed contents 378 About this publication 385 Keeping in touch 386 Acknowledgements 388 Variety increases complexity In October 2018, the International Accounting Standards Board (the Board) published the results of its research project on sources of complexity in applying IFRS 2 Share-based Payment. The Board concluded that no further amendments to IFRS 2 are needed. It felt the main issues that have arisen in practice have been addressed and there are no significant financial reporting problems to address through changing the standard. However, it did acknowledge that a key source of complexity is the variety and complexity of terms and conditions included in share-based payment arrangements, which cannot be solved through amendments to the standard.