Eften Real Estate Fund III AS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

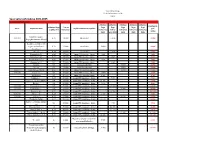

Erihoolekande Teenusekohtade Tabel 01.11.2017.Xlsx

Tegevusloa omaja Tegevuskoha aadress Kontaktandmed Telefon Andmed tegevusloa kohta Tegevusloa Riigieelarveli Tegevusloa Riigieelarvelis Halduslepingu (teenuse osutaja) E-post / veebiaadress (erihoolekandeteenus) number ste kohtade kehtivusaeg te täidetud kehtivusaeg arv kohtade arv 01.11.2017 seisuga HARJUMAA AS Hoolekandeteenused Merimetsa tee 1 [email protected] 6 771 250 igapäevaelu toetamine SEH000162 28 Tegevusloa Riigieelarveliste 29.02.2020 10614 Tallinn www.hoolekandeteenused.ee töötamise toetamine SEH000168 194 kehtivusaeg kohtade arv toetatud elamine SEH000169 8 tegevuskohta tegevuskohtad kogukonnas elamine SEH000161 237 de lõikes e lõikes erinev ööpäevaringne erihooldusteenusSEH000174 1430 erinev (vt (vt allpool allpool olevast tabelist) ööpäevaringne erihooldusteenus 220 olevast sügava liitpuudega isikule tabelist) ööpäevaringne erihooldusteenus 104 kohtumäärusega paigutatud isikule Ööpäevaringne erihooldusteenus 6 kohtumäärusega paigutatud isikule (alaealised) AS Hoolekandeteenused Valkla Kodu Valkla küla [email protected] 6 066 301 ööpäevaringne erihooldusteenus SEH000174 104 tähtajatu 88 Kuusalu vald www.hoolekandeteenused.ee/valkla kohtumäärusega paigutatud isikule 74630 Harjumaa AS Hoolekandeteenuse Vääna-Viti Kodu Viti küla 1 [email protected] 6 742 127 kogukonnas elamine SEH000161 1 tähtajatu 1 Harku vald http://www.hoolekandeteenused.ee/vaan ööpäevaringne erihooldusteenus SEH000174/10 87 tähtajatu 86 76910 Harjumaa a/ AS Hoolekandeteenused Kehra Kodu Lehtmetsa küla Anija [email protected] -

Ispa Project Estonia

FICHA INFORMATIVA ISPA nº 2003/EE/16/P/PA/011 Título de la medida Asistencia técnica para el plan piloto de gestión de recursos hidráulicos de la subcuenca del distrito de Harju en Estonia Organismo responsable de la aplicación Nombre: Ministerio de Medio Ambiente Dirección: 24 Toompuiestee, 15127 Tallin, Estonia Correo electrónico: [email protected] Descripción El Ministerio de Medio Ambiente ha identificado la necesidad de asistencia técnica (AT) para la preparación del Plan de Gestión de Recursos Hidráulicos de la subcuenca del distrito de Harju como plan piloto de gestión de cuencas fluviales. En Estonia está prevista la ejecución de ulteriores planes de este tipo. Este proyecto de AT se ha iniciado con la finalidad de aplicar la Directiva marco sobre política de aguas 2000/60/CE. Se refiere a la elaboración de un plan de gestión de recursos hidráulicos para la subcuenca del distrito de Harju, que incluye cinco subprogramas (agua potable, aguas subterráneas, aguas superficiales, ecosistema acuático y aguas costeras). El plan establecerá una lista de medidas potenciales e inversiones concretas en el sector del agua. El proyecto comprende 7 ciudades (Tallinn, Maardu, Kehra, Paldiski, Keila, Saue y Tapa) y 38 municipios (Aegviidu, Albu, Ambla, Anija, Harku, Jõelähtme, Juuru, Kadrina, Kaiu, Kehtna, Keila, Kernu, Kiili, Kohila, Kose, Kõue, Kuusalu, Lehtse, Loksa, Nissi, Nõva, Noarootsi, Oru, Padise, Paide, Raasiku, Rae, Rapla, Risti, Roosna-Alliku, Saksi, Saku, Saue, Taebla, Tamsalu, Väätsa, Vasalemma y Viimsi). Objetivos El objetivo global es desarrollar un plan integral de gestión de recursos hidráulicos basado en la Directiva marco sobre política de aguas 2000/60/CE. -

Kõrvalmaantee Nr 11162 Riisipere Riisipere-Nurme Km

Registrikood 10171636 Riia 35, Tartu 50410 Tel 7300 310 [email protected] TÖÖ NR 20182018----179179179179 Alguspunkti a sukoha l igikaudsed koordinaadid (L -Est’97) X 65539 80 Y 51754 6 KÕRVALMAANTEE NR 11162 RIISIPERERIISIPERE----NURMENURME KM 0,000,00----2,802,80 REKONSTRUEERIMISEGA KAASNEVA KESKKONNAMÕJU HINDAMISE EELHINNANG Objekti aadress: HARJU MAAKOND , SAUE VALD , RIISIPERE ALEVIK Tellija: TINTER -PROJEKT OÜ Töö täitja: Kobras AS Juhataja: URMAS URI Juhtekspert: URMAS URI Vastutav täitja: NOEELA KULM Kontrollis: ENE KÕND Oktoober 201 8 TARTU Kõrvalmaantee nr 11162 Riisipere-Nurme km 0,00-2,80 rekonstrueerimisega kaasneva keskkonnamõju hindamise EELHINNANG Üldinfo TÖÖ NIMETUS: Kõrvalmaantee nr 11162 Riisipere-Nurme km 0,00-2,80 rekonstrueerimisega kaasneva keskkonnamõju hindamise eelhinnang OBJEKTI ASUKOHT: Harju maakond, Saue vald, Riisipere alevik TÖÖ EESMÄRK: Kõrvalmaantee nr 11162 Riisipere-Nurme km 0,00-2,80 rekonstrueerimise projektiga kavandatava tegevuse keskkonnamõju hindamise eelhinnangu koostamine selgitamaks välja keskkonnamõju strateegilise hindamise algatamise ja koostamise vajalikkus. Projekti eesmärk on riigitee 11162 Riisipere - Nurme km 0,00 – 2,80 lõigu põhiprojekti koostamine, mille alusel on võimalik teostada kõnealuse maanteelõigu rekonstrueerimine. Eesmärk on lõigu rekonstrueerimise järgselt liiklusohutuse ja liikluse sujuvuse parandamine, liiklusmüra leevendamine ja kergliikluse eraldamine autoliiklusest, samuti uude asukohta Riisipere – Turba raudtee ja riigitee ristumise projekteerimine. TÖÖ LIIK: Keskkonnamõju -

VALLAJUHTIDE OOTUSED NOORTEKESKUSELE IDA-VIRU MAAKONNA NÄITEL Lõputöö

TARTU ÜLIKOOLI VILJANDI KULTUURIAKADEEMIA Kultuurhariduse osakond Huvijuht-loovtegevuse õpetaja eriala Merle Harjo VALLAJUHTIDE OOTUSED NOORTEKESKUSELE IDA-VIRU MAAKONNA NÄITEL Lõputöö Juhendaja: Urmo Reitav, MA Kaitsmisele lubatud ……………………. Viljandi 2013 SISUKORD SISUKORD ..................................................................................................................................... 1 SISSEJUHATUS ............................................................................................................................. 3 1. TEEMA LÄHTEALUSED...................................................................................................... 5 1.1 Töös kasutatavaid mõisted ................................................................................................ 5 1.2 Ootus ja ootuste teooria .................................................................................................... 6 1.3 Kohalik omavalitsus ......................................................................................................... 7 1.4 Avatud noorsootöö – noortele, noortega ja noorte heaks ................................................. 9 1.5 Noortekeskused Eestis .................................................................................................... 12 1.6 Noorsootöö Ida-Virumaal ............................................................................................... 14 2. UURIMISMETOODIKA ..................................................................................................... -

Muudatused Elektrivõrgus Vastavalt Elektrilevi

1 Lisa 8. Muudatused elektirvõrgus vastavalt Elektrilevi OÜ ja Elering AS tegevuskavadele Elektrilevi OÜ olemasolevad ja uued 35–110 kV liinid Olemasolevad uuendatavad 35-110 kV liinid Jrk. nr. Omavalitsus Liini nimetus Nimipinge/ märkused 35 kV üleviimine 110 kV 1 Nissi ja Märjamaa Ellamaa - Märjamaa õhuliiniks 35 kV üleviimine 110 kV 2 Nissi Ellamaa - Riisipere õhuliiniks 35 kV üleviimine 110 kV 3 Nissi ja Kernu Riisipere - Haiba õhuliiniks 35 kV üleviimine 110 kV 4 Kernu ja Kohila Haiba - Kohila õhuliiniks 35 kV üleviimine 110 kV 5 Nissi Ellamaa - Riisipere õhuliiniks 35 kV üleviimine 110 kV 6 Nissi ja Kernu Riisipere - Laitse õhuliiniks 35 kV üleviimine 110 kV 7 Kernu, Saue, Keila Laitse - Keila õhuliiniks 35 kV üleviimine 110 kV 8 Saku ja Kohila Kiis - Kohila õhuliiniks 35 kV üleviimine 110 kV 9 Vasalemma ja Padise Rummu - Padise õhuliiniks 35 kV üleviimine 110 kV 10 Padise Padise - Suurküla õhuliiniks 35 kV üleviimine 110 kV 11 Padise ja Keila Suurküla - Klooga õhuliiniks 35 kV üleviimine 110 kV 12 Keila Klooga - Keila õhuliiniks 35 kV üleviimine 110 kV 13 Keila v. ja Keila linn Keila - Elevaatori õhuliiniks 35 kV üleviimine 110 kV 14 Keila Keila - Keila-Joa õhuliiniks 2 35 kV üleviimine 110 kV 15 Keila ja Harku Keila - Keila-Joa õhuliiniks 35 kV üleviimine 110 kV 16 Keila ja Saue Keila - Saue õhuliiniks 35 kV üleviimine 110 kV 17 Saue ja Tallinn Saue - Pääsküla õhuliiniks 35 kV üleviimine 110 kV 18 Saue ja Tallinn Laagri - Pääsküla õhuliiniks 35 kV üleviimine 110 kV 19 Saku Kiisa - Saku õhuliiniks 35 kV üleviimine 110 kV 20 Saku -

Tree-Ring Dating in Estonia

University of Helsinki Faculty of Science Department of Geology View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Helsingin yliopiston digitaalinen arkisto TREE-RING DATING IN ESTONIA ALAR LÄÄNELAID HELSINKI 2002 Doctoral dissertation to be defended in University of Helsinki, Faculty of Science To be presented, with the permission of the Faculty of Science of the University of Helsinki, for public criticism in Auditorium E204, Physicum, Kumpula, Gustaf Hällströmin katu 2, University of Helsinki, on November 29th, at 2 o'clock in the afternoon. Custos: Prof. Matti Eronen, Department of Geology, Faculty of Science of University of Helsinki, Finland Opponent: Prof. Dieter Eckstein, Institute for Wood Biology of University of Hamburg, Germany Reviewers: Dr. Tomasz Wazny, Dendrochronological Laboratory, Faculty of Conservation and Restoration of Academy of Fine Arts, Warsaw, Poland Prof. Olavi Heikkinen, Department of Geography of University of Oulu, Finland © Alar Läänelaid, 2002 Tartu Ülikooli Kirjastuse trükikoda Tiigi 78, Tartu 50410 ISBN 9985–78–740–4 Tellimus nr. 488 2 CONTENTS LIST OF ORIGINAL PUBLICATIONS ...................................................... 4 PREFACE ..................................................................................................... 5 1. INTRODUCTION ................................................................................... 6 1.1. What is tree-ring dating? .................................................................. 6 1.2. Briefly about the -

Saue Valla Teehoiukava 2021-2025

Saue Vallavolikogu 29.10.2020 määrus nr 28 Lisa 1 Saue valla teehoiukava 2021-2025 Saue valla teed ja tänavad ehitatava ehitatava ehitatava ehitatava ehitatava investeerin- ehitatava lõigu 1 km ca lõigu lõigu lõigu lõigu lõigu tee nr tee/tänava nimi vajaliku teehoiutöö kirjeldus gud ca pikkus km maksumus maksu-mus maksu- maksumus maksumus maksumus kokku 2021 mus 2022 2023 2024 2025 Kooli tn(Laagri) 7270163 0,15 72 000 uus a/b kiht 10800 10800 Riigigümnaasiumi kõrval Koidu tee ja Hämariku riigitee mahasõitude 0,15 72 000 uus a/b kiht 10800 10800 laiendused Sae tn 0,24 72 000 uus a/b kiht 17280 17280 Vanasilla tn L1 0,05 37 000 kuum PIN mustkatte ehitus 1850 1850 Nõlvaku tn L2 0,22 37 000 kuum PIN mustkatte ehitus 8140 8140 Veskitammi tn L3 0,05 37 000 kuum PIN mustkatte ehitus 1850 1850 Avamaa tn L2 0,1 29 000 kuum PIN mustkatte ehitus 2900 2900 Hoiu tn 0,6 72 000 roopa parandustööd 95000 43200 Vae tn 0,3 72 000 roopa parandustööd 55000 21600 7270277 Kaasiku tee(Alliku) 0,56 29 000 kuum PIN mustkatte ehitus 16240 16240 7270226 Vatsla tee 0,3 72 000 kuum PIN mustkatte ehitus 21600 21600 Jõeääre tee 0,3 29 000 kuum PIN mustkatte ehitus 8700 8700 Jahimaja tee 0,25 29 000 kuum PIN mustkatte ehitus 7250 7250 Jõe tee L1 ja L3(Hüüru) 0,4 29 000 kuum PIN mustkatte ehitus 11 600 11600 Kivi tee 0,2 29 000 kuum PIN mustkatte ehitus 5 800 5800 7270244 Vanamõisa tee 0,3 37 000 kuum PIN mustkatte ehitus 11 100 11100 7270254 Kapsaküla tee 1,387 29 000 kuum PIN mustkatte ehitus 20 000 40 000 Pagavere tee 0,37 29 000 kuum PIN mustkatte ehitus 10 730 10 -

KORRALDUS 16.11.2018 Nr 1-3/18/220

KORRALDUS 16.11.2018 nr 1-3/18/220 Projekteerimistingimuste andmine Riigitee nr 11162 Riisipere-Nurme km 0,00 – 2,80 lõigu põhiprojekt koostamiseks ja ehitusprojektiga kavandavate tegevuste keskkonnamõju hindamise algatamata jätmine Ehitusseadustiku (EhS) § 99 lõigete 1 ja 2 alusel algatas Maanteeamet projekteerimistingimuste andmise menetluse riigitee nr 11162 Riisipere-Nurme km 0,00 – 2,80 lõigu põhiprojekti koostamiseks. Projekteerimistingimuste menetluse ese (11162 Riisipere-Nurme km 0,00 – 2,80) paikneb riigi transpordimaa kinnisasjal Riisipere alevikus, Saue valla territooriumil. Tulenevalt EhS § 31 lõikest 3 kaasas Maanteeamet pädeva asutusena projekteerimistingimuste menetlusse Lisas 2 loetletud menetluse eseme kinnisasjaga piirnevate kinnisasjade omanikud. Tulenevalt EhS § 31 lõike 4 punktist 1 esitas Maanteeamet projekteerimistingimuste eelnõu kooskõlastamiseks asutustele, kelle seadusest tulenev pädevus on seotud projekteerimistingimuste menetluse esemega: Põllumajandusamet (registrikood 70000071) Terviseamet (registrikood 70008799) Muinsuskaitseamet (70000958) Tulenevalt EhS § 31 lõike 4 punktist 2 esitas Maanteeamet projekteerimistingimuste eelnõu arvamuse avaldamiseks asutusele või isikule, kelle õigusi või huve võib taotletav ehitis või ehitamine puudutada: Maa-amet (registrikood 70003098) Saue Vallavalitsus (registrikood 77000430) Telia Eesti AS (registrikood 10283074) Elektrilevi OÜ (registrikood 11050857) Connecto Eesti AS (registrikood 10722319) Võttes aluseks EhS § 26 lõike 5 teavitas Maanteeamet projekteerimistingimuste -

LETHAIA Ordovician of Estonia: Two Ichnogenera Produced by a Single Maker, a Case of Host Morphology Control

BoringsBlackwell Publishing Ltd in trepostome bryozoans from the Ordovician of Estonia: two ichnogenera produced by a single maker, a case of host morphology control PATRICK N. WYSE JACKSON AND MARCUS M. KEY, JR. Wyse Jackson, P.N. & Key, M.M., Jr. 2007: Borings in trepostome bryozoans from the LETHAIA Ordovician of Estonia: two ichnogenera produced by a single maker, a case of host morphology control. Lethaia, Vol. 40, pp. 237–252. The evolution of borings has shown that the morphology of borings is a function of both the borer and its substrate. This study investigated the effect of bryozoan internal skeletal morphology on the dimensions and distribution of borings. One hundred and forty-three trepostome colonies from the Middle and Upper Ordovician strata of northern Estonia were examined. Of these, 80% were matrix entombed, longitudinally sectioned ramose and hemispherical colonies, and 20% were matrix-free hemispherical colonies that allowed examination of the colony surfaces. Seventy-one percent of the ramose colonies were bored, whereas 88% of the hemispherical colonies were bored. On average, only 8% of colony surface areas were bored out. Borings were more ran- domly oriented in the hemispherical colonies. In contrast in the ramose colonies, the borings tended to more restricted to the thin-walled endozone and thus parallel to the branch axis. This is interpreted to be a function of the thick-walled exozones con- trolling to some extent where the borer could bore. Based on morphology, the borings in the hemispherical colonies are referred to Trypanites and those in the ramose colonies to Sanctum. Sanctum is revised to include two possible openings and to recognize that boring shapes were inherently constrained by the thick-walled exozones of the host bryozoan colonies. -

International Geological Congress, XXVII Session, Estonian Soviet Socialist Republic, Excursions: 027, 028 Guidebook

INTERNATIONAL GEOLOGICAL CONGRESS XXVII SESSION ESTONIAN SOVIET SOCIAL1ST REPUBLIC Excursions: 027, 028 Guidebook 021 A +e \ \ �� Dz \ _(,/ \ POCCHHCKAR Ct/JCP\ RUSsiAN SFSR \ y n] Dt (. - � v$&.1/ATBHHCKA f1 CCP LATV/AN SSR 02 • 3 INTERNATIONAL GEOLOGICAL CONGRESS XXVII SESSION USSR MOSCOW 1984 ESTONIAN SOVIET SOCIAL1ST REPUBLIC Excursions: 027 Hydrogeology of the Baltic 028 Geology and minerai deposits of Lower Palaeozoic of the Eastern Baltic area Guidebook Tallinn, 1984 552 G89 Prepared for the press by Institute of Geology, Academy of Sciences of the Estonian SSR and Board of Geology of the Estonian SSR Editorial board: D. Kaljo, E. Mustjõgi and I. Zekcer Authors of the guide: A. Freimanis, ü. Heinsalu, L. Hints, P. Jõgar, D. Kaljo, V. Karise, H. Kink, E. Klaamann, 0. Morozov, E. Mustjõgi, S. Mägi, H. Nestor, Y. Nikolaev, J. Nõlvak, E. Pirrus, L. Põlma, L. Savitsky, L. Vallner, V. Vanchugov Перевод с русского Титул оригинала: Эстонская советехая сочиалистичесхая Республика. Экскурсии: 027, 028. Сводный путеводителъ. Таллии, 1984. © Academy of Sciences of the Estonian SSR, 1984 INTRODUCTION The geology of the Estonian Soviet Socialist Republic (Estonia) has become the object of excursions of the International Geo logical Congress for the second time. It happened first in 1897 when the excursion of IGC visited North Estonia (and the ter ritory of the present Leningrad District) under the guidance of Academician F. Schmidt. Such recurrent interest is justi fied in view of the classical development of the Lower Pa laeozoic in our region and the results of investigations ohtained by geological institutions of the republic. The excursions of the 27th IGC are designed, firstly, to provide a review of the stratigraphy, palaeontology and lithology of the Estonian Early Palaeozoic and associated useful minerals in the light of recent investigations (excursion 028), and, secondly, to give a survey of the problerus and some results of hydrogeology in a mare extensive area of the northwestern part of the Soviet Union (excursion 027). -

The Price List of Services of the Academic Library of Tallinn University

APPROVED by the decree no 12 of the Director of the Library on 07. July 20 21 The Price List of Services of the Academic Library of Tallinn University User registration Information d esk, telephone +372 6659 439 Price in Euros, Service incl VAT User reg istration with ID card free User registration for the Tallinn University students and staff free User registration for others (without Estonian ID card) 2.00 Duplicate of the library card 4.00 One - time visitor card 0.50 Duplicate to replace a stolen c ard (in case there is official proof of the theft being reported to police) free Copy and Print Services Information desk, telephone +372 6659 439 Price in Euros, Service Unit incl VAT Copy (A4, B/W, one side / double sided)* page 0.10 / 0.19 Copy (A4 , colour, one side / double sided)* page 0.60 / 1.19 Copy (A3, B/W, one side / double sided)* page 0.17 / 0.33 Copy (A3, colour, one side / double sided)* page 1.20 / 2.39 Copy of a bound newspaper (A4)* page 0.20 Copy of a bound newspaper (A3)* page 0 .38 Search and copy* page 0.30 Printout (A4, B/W, one side / double sided)** page 0.10 / 0.19 Printout (A4, colour, one side / double sided)** page 0.60 / 1.19 Printout (A3, B/W, one side / double sided)** page 0.17 / 0.33 Printout (A3, colour, one si de / double sided)** page 1.20 / 2.39 * The service is only for making copies of library collection items. Making copies while you wait, max 20 pages. -

JOBS CREATED out of TALLINN HAVE NOT Reduced

THE BALTIC JOURNAL OF ROAD AND BRIDGE ENGINEERING 2013 8(1): 58–65 JOBS CREATED OUT OF TALLINN HAVE NOT REDUCED COMMUTING Roland Mäe1 , Dago Antov2, Imre Antso3 Dept of Transportation, Tallinn University of Technology, Ehitajate tee 5, 19086 Tallinn, Estonia E-mails: [email protected]; [email protected]; [email protected] Abstract. Although urban sprawl is relatively new process for Estonia which has not revealed itself to the full extent, in many European cities urban sprawl is recognised as a major challenge to quality of life. Due to the above mentioned negative aspects of urban sprawl in some countries the efforts are determined to restrain urban sprawl. Many studies have been undertaken to research the financial, ecological, cultural and social cost of urban sprawl in most of developed countries. This is the main reason, why declared in the majority of studies the theses, especially in the field of traffic and transportation, cannot be applied to assess situation in our country. Estonia has many geographical, economical, social and cultural peculiarities, which influence its traffic and transportation patterns as well as its urban sprawl rates. Economical crisis has shown the exigency to reduce drastically non-productive expenses and optimize productivity of labour. Thus the reduction of losses in traffic and transportation could be one of all possible solutions. In this article the commuting caused by urban sprawl has been analyzed. The second task is to find out in which range public databases are used to determine the demand of mobility. Keywords: urban sprawl, commuting, traffic volume, mobility, territorial planning, public databases.