PARTIAL DECISION and ORDER EB-2019-0018 Alectra Utilities

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ale0011152.0001

ALE0011152.0001 ORANGEVILLE St.Thomas . HYDRO energyserv1ces- DISTRIBUTION INC. NEWS RELEASE FOR IMMEDIATE RELEASE August 11, 2011 Five Ontario electric utilities to partner on solar initiative Pilot project will measure conservation impact of using solar powered attic vents COLLINGWOOD, ON - Five Ontario electricity distribution companies are getting together to partner on an initiative that will test the effectiveness of using solar powered attic vents in helping to reduce the electricity consumption required to cool homes. The announcement was made today at a project launch event on Davis Street in Collingwood where representatives from Callus Power, PowerStream, Orangevillle Hydro, St Thomas Energy, Wasaga Beach Distribution, other key stakeholders and members of the media witnessed the unveiling, on the roof of a new home, two fully-installed solar powered attic vent units that were provided by the project's supplier, International Solar Solutions. A solar powered attic vent, also referred to as a solar powered roof vent, works during the day and has a solar panel which converts energy from the sun into electricity. This electricity operates a motor that drives a fan inside the vent. Attic ventilation is an important aspect in maintaining a healthy energy-efficient home. Venting cools a roof, extends the life of roof materials and helps to reduce the load on air conditioning systems. Callus Power, PowerStream and Wasaga Beach Distribution will operate the pilot in their respective service territories using a combination of installing solar powered attic vents on new houses being built by Devonleigh Homes and retrofitting houses in older subdivisions. Orangeville Hydro and St. -

Alectra Inc. 2018 Consolidated Financial Statements

Consolidated Financial Statements (In millions of Canadian dollars) ALECTRA INC. Year ended December 31, 2018 KPMG LLP Bay Adelaide Centre 333 Bay Street, Suite 4600 Toronto, ON M5H 2S5 Canada Tel 416-777-8500 Fax 416-777-8818 INDEPENDENT AUDITORS’ REPORT To the Shareholders of Alectra Inc. Opinion We have audited the consolidated financial statements of Alectra Inc. (the Entity), which comprise: • the consolidated statement of financial position as at December 31, 2018 • the consolidated statement of income and comprehensive income for the year then ended • the consolidated statement of changes in equity for the year then ended • the consolidated statement of cash flows for the year then ended • and notes to the consolidated financial statements, including a summary of significant accounting policies (Hereinafter referred to as the “financial statements”). In our opinion, the accompanying financial statements present fairly, in all material respects, the consolidated financial position of the Entity as at December 31, 2018, and its consolidated financial performance and its consolidated cash flows for the year then ended in accordance with International Financial Reporting Standards (IFRS). Basis for Opinion We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the “Auditors’ Responsibilities for the Audit of the Financial Statements” section of our auditors’ report. We are independent of the Entity in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada and we have fulfilled our other responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. -

Discovering the Possibilities About Our Sustainability Report

2019 Annual Sustainability Report Discovering the possibilities About our sustainability report The Alectra Inc. 2019 Annual Sustainability Report provides details about Alectra’s social, environmental and economic impact, as well as issues that are of material interest to our stakeholders as validated through a third-party materiality assessment and a variety of engagement activities. Material issues include: Health and Safety/ Public Health and Safety; Infrastructure Modernization; Community Engagement; Climate Change; Customer Services; Energy Affordability; Waste and Material Management; Diversity and Inclusion; Employee Well-Being, Engagement and Development; Energy Efficiency; and Financial Performance. Commitment Our sustainability commitment As a sustainable company, Alectra is committed to meeting today’s needs and the needs of future generations by empowering our customers, communities and employees, protecting the environment, and embracing innovation. Our vision is to be Canada’s leading distribution and integrated energy solutions provider, creating a future where people, businesses and communities will benefit from energy’s full potential. Our mission is to provide customers with smart and simple energy choices, while creating sustainable value for our shareholders, customers, communities and employees. Our values are safety, respect, customer focus, excellence, and innovation. CONTENTS 2 Corporate profile 10 People 3 2019 Achievements 20 Planet 4 Message to our stakeholders 26 Performance 6 A new energy future 32 Corporate governance 8 The Alectra GRE&T Centre Corporate Profile As one of Canada’s Sustainability leading energy companies, at Alectra Alectra Inc. is shaping the Our sustainability future of energy. framework – AlectraCARES We provide safe, reliable and innovative We have embedded sustainability energy solutions to families and About Alectra principles into our core business businesses across the 17 communities strategy and operations in order to in our service territory, while maintaining Alectra Inc. -

Download the 2018 Annual Sustainability Report

SUSTAINABLE POWER Discovering the possibilities 2018 Annual Sustainability Report Sustainable power balances social responsibility and environmental accountability with economic efficiency – People, Planet and Performance. It is power that embraces innovation to improve our quality of life by providing safe and reliable energy solutions that help deliver value to our homes, workplaces and communities. Alectra is committed to helping customers and the communities we serve discover the possibilities of a new energy future for our people and our planet through our sustainable performance. This is Alectra’s second Annual Sustainability Report which highlights our achievements in 2018. Alectra’s Vision, Mission and Values Our Vision To be Canada’s leading electricity distribution and integrated energy solutions provider, creating a future where people, businesses and communities will benefit from energy’s full potential. Our Mission To provide customers with smart and simple energy choices, while creating sustainable value for our shareholders, customers, communities and employees. Our Values Our core values are safety, respect, customer focus, excellence and innovation. 2 Corporate Profile 4 Message to Stakeholders 6 Corporate Governance 8 Sustainability at Alectra 10 Stakeholder Engagement 12 Sustainability Leadership 14 People 22 Planet 30 Performance Alectra Inc. 2018 Annual Sustainability Report 1 Corporate Profile About Alectra Alectra Inc. (Alectra) is an investment holding customers, we deliver approximately company with a head office in Mississauga, 22 per cent of Ontario’s electricity. In Ontario, that owns 100 per cent of the addition to our electricity distribution common shares of each of: Alectra Utilities business, Alectra Utilities Corporation Corporation (Alectra Utilities), Alectra Energy has a non-regulated commercial rooftop Solutions Inc. -

Alectra Inc. 16X9

Exploring PSBN in Electric Utilities 1 March 26, 2019 Keith Hemingway, Manager Operational Technology Services Who We Are 2 Together we’re better • Enersource, Horizon Utilities and PowerStream merged to become Alectra Inc. on January 31, 2017; The company acquired Hydro One Brampton on February 28, and merged with Guelph Hydro on January 1, 2019. • The consolidation of the four utilities created the second largest municipally-owned electric utility by customer base in North America (second only to Los Angeles Department of Water and Power) • Alectra Inc. is the holding company for several subsidiaries including Alectra Utilities and Alectra Energy Solutions 3 Alectra’s family of companies • Alectra’s family of energy companies distributes electricity to nearly one million customers in Ontario’s Greater Golden Horseshoe area and provides innovative energy solutions to these and thousands more all across Ontario. Our employees are allies in helping customers discover the possibilities of energy conservation and new technologies for enhancing their quality of life. We create sustainable value for our customers, communities and shareholders. 4 Alectra’s family of companies 5 Our name & signature line • The Greek meaning of the name Alectra means brilliant. Our name also conveys energy... the energy of our people and the millions of customers we serve. • Alectra identifies us with the energy sector today and for the future—and sends the message that we are the customer’s ally. • Our signature line, ‘Discover the Possibilities’ is an invitation—to our customers, employees and communities—to come with us on this journey. It says we aspire to something bold for the future, but we’re also about practical choices that improve daily life. -

Alectra Utilities (“Alectra”) Serves Over One Million Customers Across 1,800 Sq

February 13, 2020 IESO Engagement Independent Electricity System Operator 1600–120 Adelaide Street West Toronto, ON M5H 1T1 To Whom it May Concern: Re: Exploring Expanded DER Participation in the IESO-Administered Markets Part 2: Options and Considerations for Enabling DER Participation On October 17, 2019 the Independent Electricity System Operator (“IESO”) released the first in its series of white papers (the “Paper”) on exploring expanded Distributed Energy Resource (“DER”) participation in the IESO Administered Markets (“IAMs”). The Paper overviewed the ways in which DERs currently participate in the IAM, concluding that only directly participating generators, Demand Response (“DR”) and aggregated non-dispatchable DR are currently able to fully participate. The Paper also examined several barriers that prevent DERs from other types or forms of participation. On January 30, 2020, the IESO hosted a webinar to provide an overview of the next DER white paper and to introduce some of its high-level ideas and options to enhance DER participation that may be explored in the next Paper. The intention of the next Paper will be to include more detailed examination of participation models and options to address barriers identified in the first Paper. The IESO is seeking feedback from stakeholders on the options presented in the webinar in order to determine or guide which should be explored further. Alectra Utilities (“Alectra”) serves over one million customers across 1,800 sq. km of service territory, spanning 17 communities in Ontario, including Alliston, Aurora, Barrie, Beeton, Brampton, Bradford, Guelph, Hamilton, Markham, Mississauga, Penetanguishene, Richmond Hill, Rockford, St. Catharines, Thornton, Tottenham and Vaughan. -

Ontario Energy Board Preliminary Filing Requirements for a Notice Of

Ontario Energy Board Preliminary Filing Requirements For a Notice of Proposal under Sections 80 and 81 Of the Ontario Energy Board Act, 1998 INSTRUCTIONS: This form applies to all applicants who are providing a Notice of Proposal to the Ontario Energy Board (the “Board”) under sections 80 and 81 of the Ontario Energy Board Act, 1998 (the “Act”), including parties who are also, as part of the same transaction or project, applying for other orders of the Board such as orders under sections 86 and 92 of the Act. The Board has established this form under section 13 of the Act. Please note that the Board may require information that is additional or supplementary to the information filed in this form and that the filing of the form does not preclude the applicant from filing additional or supplementary information. PART I: GENERAL MINIMUM FILING REQUIREMENTS All applicants must complete and file the information requested in Part I. 1.1 Identification of the Parties 1.1.1 Applicant Name of Applicant File No: (Board Use Only) Address of Head Office Telephone Number The names and contact information for the Applicants are provided in Attachment 1.1.1. Facsimile Number E-mail Address Name of Individual to Contact Telephone Number Facsimile Number E-mail Address 2 1.1.2 Other Parties to the Transaction or Project If morethan one attach list Name of Applicant File No: (Board Use Only) Address of Head Office Telephone Number The names and contact information for the other parties to the transactions are provided in Facsimile Number Attachment 1.1.2. -

Collingwood Powerstream Utility Services Corp. Current Corporate

Schedule A: Collingwood PowerStream Utility Services Corp. Current Corporate Structure Alectra Town of Collingwood 50% Owner 50% Owner Collingwood PowerStream Utility Services Corp. Collus PowerStream Corp. Collus Solutions Corp. Collus Energy Corp. (LDC) (Inactive) (Inactive) Schedule B EPCOREPCOR Utilities Inc. EPCOR Power EPCOR Ontario EPCOR Holdings EPCOR EPCOR Development Utilities Inc. East Inc. Water Services Distribution & Corporation Inc. Transmission Inc. EPCOR EPCOR Collingwood Water (USA) Inc. Distribution Corp. EPCOR Natural Gas Limited Partnership Following closing of the transaction, EPCOR Collus PowerStream Collingwood Distribution Corp. will hold all of the Utility Services Corp. issued and outstanding shares of Collus PowerStream Utility Services Corp. The name of this entity will be changed to EPCOR Collingwood Services Inc. immediately after closing. Collus Powestream Corp. will be renamed EPCOR Collus PowerStream Collingwood Local Distribution Corp. Corp. This organizational chart reflects a simplified organizational structure and indicates the EPCOR Utilities Inc. (“EUI”) subsidiaries related to the transaction and EUI’s material subsidiaries as of the date of this application. EPCOR Utilities Inc. Investor Presentation July 2017 Guy Bridgeman Senior Vice President & Chief Financial Officer Amanda Rosychuk Senior Vice President, Drainage Services Pam Zrobek Treasurer 1 Forward-Looking Information Certain information in this presentation is forward looking within the meaning of Canadian securities laws as it relates -

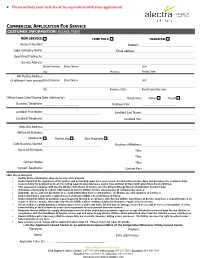

Commercial Application Form

* Please include your Articles of Incorporation with your application. COMMERCIAL APPLICATION FOR SERVICE CUSTOMER INFORMATION: PLEASE PRINT NEW SERVICE: TEMP POLE: TRANSFER: Account Number: Deposit: Legal Company Name: Email address: Operating/Trading As: Service Address: Street Number Street Name Unit City Province Postal Code Bill Mailing Address: (if different from service) Street Number Street Name Unit City Province/State Postal Code/Zip Code Official Lease Date/Closing Date (dd/mm/yy): Check One: Owner Tenant Business Telephone: Business Fax: Landlord First Name: Landlord Last Name: Landlord Telephone: Landlord Fax: Web Site Address: Nature of Business: Corporation Partnership Sole Proprietor Date Business Started: Business Affiliations: Name of Principals: Title: Title: Contact Name: Title: Contact Telephone: Contact Fax: I/We, the undersigned Certify all the information above to be true and complete; Understand that the signatures of the parties will be binding upon their successors. Vacating this premise does not discharge the customer from responsibility for payment up to and including legal closing date/lease expiry date, without written notification from Alectra Utilities; This agreement complies with Alectra Utilities Conditions of Service and the Ontario Energy Boards Distribution System Code; Authorize a third party to submit information to Alectra Utilities for the sole purpose of commencing service; Authorize the receipt and provision of account information from credit grantors, credit bureaus and suppliers of services; Understand that a deposit is required based on Alectra Utilities Security Deposit Policy. Understand that failure to maintain a good payment history in accordance with Alectra Utilities Conditions of Service may have a deposit invoiced as required. Service may be interrupted by Alectra Utilities when customer payments for power supplied are in arrears; Alectra Utilities cannot guarantee uninterrupted service and is not liable for any loss or damage incurred as a result of service interruption. -

Discovering the Possibilities

Discovering the possibilities 2020 Annual Sustainability Report About our sustainability report The Alectra Inc. 2020 Annual Sustainability Report provides details about Alectra’s social, environmental, and economic impact, as well as issues that are of significant interest to our stakeholders as validated through a third-party assessment and a variety of engagement activities. Significant issues include: Health and Safety/Public Health and Safety; Infrastructure Modernization; Community Engagement; Climate Change; Customer Services; Energy Affordability; Waste and Materials Management; Equity, Diversity and Inclusion; Employee Well-Being, Engagement and Development; Energy Efficiency; and Financial Performance. Many of these issues were brought into sharper focus as the COVID-19 pandemic affected all aspects of the corporation and the communities we serve. This report discusses the impact of these issues in detail. This is Alectra’s fourth Annual Sustainability Report. Transparently sharing our performance and progress is one way of demonstrating our commitment to the three pillars of sustainability – people, planet, and performance. Our sustainability commitment As a sustainable company, Alectra is committed to meeting the needs of current and future generations by empowering our customers, communities, and employees, protecting the environment, and embracing innovation. Our vision is to be Canada’s leading distribution and integrated energy solutions provider, creating a future where people, businesses, and communities will benefit from energy’s full potential. Our mission is to provide customers with smart and simple energy choices, while creating sustainable value for our shareholders, customers, communities, and employees. Our values are safety, respect, customer focus, excellence, and innovation. CONTENTS 2 Corporate Profile 4 2020 Highlights 6 Message to our Stakeholders 8 Response to COVID-19 10 People 18 Planet 26 Performance 36 Corporate Governance 38 Alectra Fast Facts CORPORATE PROFILE As one of Canada’s leading energy companies, Alectra Inc. -

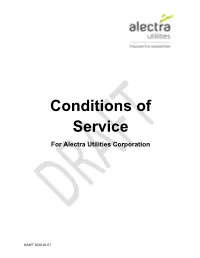

Conditions of Service for Alectra Utilities Corporation

Conditions of Service For Alectra Utilities Corporation DRAFT 2020.01.07 PREFACE CONDITIONS OF SERVICE Alectra Utilities’ Conditions of Service contains three major sections: Section 1 (Introduction): contains references to the legislation that covers the Conditions of Service, the rights of the Customer and of Alectra, and the dispute resolution process. Section 2 (General Distribution Activities): contains references to services and requirements that are common to all the Customer classes. This section covers items such as Capital Contribution, Billing, Hours of Work, Emergency Response, Power Quality and Availability Voltages. Section 3 (Customer Specific): contains references to services and requirements specific to the respective Customer class. This section covers items such as Service Entrance Requirements, Delineation of Ownership, Special Contracts, and Metering etc. Other sections include the Glossary of Terms (Section 4), and Appendices (Section 5). 2 Table of Contents 1. INTRODUCTION .............................................................................................................................. 10 1.1 IDENTIFICATION OF DISTRIBUTOR AND SERVICE AREA ......................................... 10 1.2 RELATED CODES, AND GOVERNING LAWS ................................................................. 10 1.3 INTERPRETATION ................................................................................................................. 11 1.4 AMENDMENTS AND CHANGES ........................................................................................ -

Scorecard - Alectra Utilities Corporation 10/21/2020

Scorecard - Alectra Utilities Corporation 10/21/2020 Target Performance Outcomes Performance Categories Measures 2015 2016 2017 2018 2019 Trend Industry Distributor Customer Focus New Residential/Small Business Services Connected 99.47% 99.59% 97.02% 94.57% 92.59% 90.00% Service Quality on Time Services are provided in a Scheduled Appointments Met On Time 95.97% 99.47% 99.31% 99.31% 98.75% 90.00% manner that responds to Telephone Calls Answered On Time 80.73% 80.61% 79.52% 77.67% 75.78% 65.00% identified customer preferences. First Contact Resolution 82.76% 80.86% 81.73% 86.18% 85.1% Customer Satisfaction Billing Accuracy 99.54% 99.56% 99.64% 99.59% 99.58% 98.00% Customer Satisfaction Survey Results 91.13% 90.76% 88.05% 90.89% 93% Operational Effectiveness Level of Public Awareness 78.60% 78.59% 81.27% 81.27% 82.00% 1 Safety Level of Compliance with Ontario Regulation 22/04 C C C C C C Continuous improvement in Serious Electrical Number of General Public Incidents 8 6 9 13 20 6 productivity and cost Incident Index Rate per 10, 100, 1000 km of line 0.388 0.289 0.429 0.621 0.950 0.283 performance is achieved; and Average Number of Hours that Power to a Customer is distributors deliver on system 1.00 0.83 0.80 1.04 1.07 0.91 System Reliability Interrupted 2 reliability and quality objectives. Average Number of Times that Power to a Customer is 1.23 1.09 1.11 1.33 1.26 1.26 Interrupted 2 Asset Management Distribution System Plan Implementation Progress 108.28% 96.16% 95.82% 89.01% 114% Efficiency Assessment 3 3 3 3 3 Cost Control Total Cost