Vernon Parish School Board Leesville, Louisiana

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Tables

Louisiana MFP Accountability Report JUNE 2014 STATE BOARD OF ELEMENTARY AND SECONDARY EDUCATION For further information, please contact: Mr. Charles E. Roemer Mr. Jay Guillot Allen Schulenberg President 5th BESE District Office of Administrative Support 6th BESE District Division of Information Technology Services Mr. James D. Garvey, Jr. Ms. Carolyn Hill Phone: 225.342.2292 Vice President 8th BESE District E-mail: [email protected] 1st BESE District Ms. Holly Boffy Ms. Jane Smith Secretary/Treasurer Member-at-Large This public document was printed at a cost of $48.51. Five (5) copies of this document were printed in this first printing at a cost of $48.51. This 7th BESE District document package was printed by the Louisiana Department of Education, Office of Administrative Support, Division of Information Technology Ms. Kira Orange Jones Dr. Judy Miranti Services; P.O. Box 94064; Baton Rouge, LA 70804-9064. This material was printed in accordance with the standards for printing by State Agencies 2nd BESE District Member-at-Large established pursuant to R.S. 43:31. Ms. Lottie P. Beebe Ms. Connie Bradford The mission of the Louisiana Department of Education (LDOE) is to ensure equal 3rd BESE District Member-at-Large access to education and to promote equal excellence throughout the state. The LDOE is committed to providing Equal Employment Opportunities and is committed to ensuring that all of its programs and facilities are accessible to all members of the public. The LDOE does not discriminate on the basis of age, color, disability, Mr. Walter Lee Ms. Heather Cope national origin, race, religion, sex, or genetic information. -

LSU Supplier List K-12 Schools

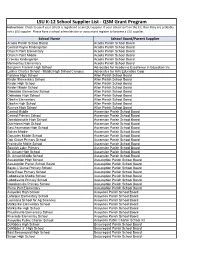

LSU K-12 School Supplier List - QSM Grant Program Instructions: Check to see if your school is registered as an LSU supplier. If your school isn't on the list, then they are probably not a LSU supplier. Please have a school administrator or accountant register to become a LSU supplier. School Name School Board/Parent Supplier Acadia Parish School Board Acadia Parish School Board Central Rayne Kindergarten Acadia Parish School Board Church Point Elementary Acadia Parish School Board Church Point Middle Acadia Parish School Board Crowley Kindergarten Acadia Parish School Board Mermentau Elementary Acadia Parish School Board Benjamin Franklin High School Advocates for Academic Excellence in Education Inc Lusher Charter School - Middle/High School Campus Advocates for Arts Education Corp Fairview High School Allen Parish School Board Kinder Elementary School Allen Parish School Board Kinder High School Allen Parish School Board Kinder Middle School Allen Parish School Board Oakedale Elementary School Allen Parish School Board Oakedale High School Allen Parish School Board Oberlin Elementary Allen Parish School Board Oberlin High School Allen Parish School Board Reeves High School Allen Parish School Board Central Middle Ascension Parish School Board Central Primary School Ascension Parish School Board Donaldsonville High School Ascension Parish School Board Dutchtown High School Ascension Parish School Board East Ascension High School Ascension Parish School Board Galvez Middle Ascension Parish School Board Gonzales Middel School Ascension Parish School Board Oak Grove Primary School Ascension Parish School Board Prairieville Midlle School Ascension Parish School Board Spanish Lake Primary Ascension Parish School Board St. Amant High School Ascension Parish School Board St. -

Vernon Parish School Board Leesville, Louisiana

^O'/l Vernon Parish School Board Leesville, Louisiana Comprehensive Annual Financial Report fop the year ended June 30, 2012 Under provisions of state law. this repoa is a public documeni Acopy of the report has baen submitted to the entity and other appropriate public ofiicials The report is avaiSabie for public inspection at the Baton Rouge OV{\ZQ of the Legislative Auditor and. where appropriate, at the office of the parish clerk of court „ , n . FEB 0 6 2013 Release Date VERNON PARISH SCHOOL BOARD Leesville, Louisiana COMPREHENSIVE ANNUAL FINANCIAL REPORT AS OF AND FOR THE YEAR ENDED JUNE 30,2012 Mike Perkins Jackie Self President Superintendent Tim Ward Director of Finance Prepared by the Department of Finance Vernon Parish School Board Table of Contents Page INTRODUCTORY SECTION Transmittal Letter 11-14 GFOA Certificate of Achievement for Excellence in Financial Reporting 15 ASBO Certificate of Excellence in Financial Reporting 17 Organization Chart 19 Elected Officials 20 Selected Administrative Officials 21 FINANCUL SECTION Statement Independent Auditors* Report 25-26 Required Supplementary Information 27 Management's Discussion and Analysis (MD&A) 28-40 Basic Financial Statements Government-wide Financial Statements (GWFS) 41 Statement of Net Assets A 42 Statement of Activities B 43 Fund Financial Statements (FFS) 44 Governmental Funds Balance Sheet C 45 Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Assets D 47 Statement of Revenues, Expenditures, and Changes in Fund Balances E 48-49 Reconciliation -

LOUISIANA- Other Identified School (PDF)

Reading Reading Math Elementary/ Middle Math Proficiency Graduation Rate State Name LEA Name LEA NCES ID School Name School NCES ID Proficiency Participation Participation School Other Academic State Defined School Improvement Status Title I School Target Target Target Target Target Indicator Target LOUISIANA Louisiana School For Math Science & the Arts 2200017 Louisiana School for Math Science & the Arts 220001701975 All Status 5 Missing LOUISIANA LSU Laboratory School 2200022 LSU Laboratory School 220002201922 All All All All Status 5 Missing LOUISIANA Southern University Lab School 2200023 Southern University Lab School 220002301921 All All All All Status 3 Title I schoolwide school LOUISIANA New Vision Learning Academy 2200025 New Vision Learning Academy 220002501000 All All Not All All All Status 3 Title I schoolwide school LOUISIANA Acadia Parish 2200030 Armstrong Middle School 220003000001 All All All All All Status 2 Title I schoolwide school LOUISIANA Acadia Parish 2200030 Branch Elementary School 220003000002 All All All All All Status 5 Title I schoolwide school Title I schoolwide eligible LOUISIANA Acadia Parish 2200030 Church Point High School 220003000004 Not All All Not All All Status 3 school-No program LOUISIANA Acadia Parish 2200030 Church Point Middle School 220003000005 Not All All All All All Status 2 Title I schoolwide school Title I schoolwide eligible LOUISIANA Acadia Parish 2200030 Crowley High School 220003000006 Not All All Not All All Status 3 school-No program LOUISIANA Acadia Parish 2200030 Crowley Middle -

Alumni Columns, an Incomplete List of Past Student Government Presidents Was Printed

— -1— ce years and was dedicated this president Dr. Rene J. Bienvenu. Bienvenu served NSU for 32 biological sciences building at Northwestern was formally NSU The 1983. in memory of former president from 1978 through 1982. He died in spring as the Rene J. Bienvenu Hall for Biological Sciences NSU Biological Sciences Building Dedicated In Memory of Former University President and Louisiana Board of successful in industry and in academic conducted Feb. 8 the former research scientist, depart- Natchitoches, Ceremonies were and medical schools." chairman, dean and NSU Trustees for Colleges and Universities Northwestern State University to ment at J. Barkate noted, "Dr. Bienvenu was in were held executive director Dr. William Rene J. Bienvenu president who died 1983, formally dedicate the an outstanding teacher who left you with the 59th annual Junkin Jr. for Biological Sciences. in conjunction Hall the ceremonies for with the feeling that this fellow was meeting of the Louisiana Academy of Responding to The naming of the three-story person as a the family was the late NSU president's interested in you as a and biological sciences building, which Sciences. and he wanted to son, Shreveport pediatrician Dr. Steve microbiologist, was approved this Guest speakers were distinguished opened in 1970, was dean of the produce the very best students of Alumnus Dr. John Barkate, Bienvenu. His father winter by the Louisiana Board NSU he felt it would College of Science and Technology possible, because State Colleges and associate director of the U.S. Trustees for building reflect on his character." Department of Agriculture's Southern when the biological sciences Universities. -

TOPS Schools Processed on 6-30-16

NAME ABBEVILLE HIGH SCHOOL ACADEMIC RECOVERY OMBUDSMAN ACADEMY OF OUR LADY (GIRLS) (C ACADEMY OF THE SACRED HEART (G ACADEMY OF THE SACRED HEART (G ACADIANA HIGH SCHOOL AIRLINE HIGH SCHOOL ALBANY HIGH SCHOOL ALEXANDRIA SENIOR HIGH SCHOOL ALFRED M. BARBE HIGH SCHOOL AMITE HIGH SCHOOL ANACOCO HIGH SCHOOL ANGELS ACADEMY ARCADIA HIGH SCHOOL ARCHBISHOP CHAPELLE HIGH SCHOO ARCHBISHOP HANNAN HIGH SCHOOL( ARCHBISHOP RUMMEL SR. HIGH SCH ARCHBISHOP SHAW SR. HIGH SCHOO ARLINGTON PREPARATORY ACADEMY ASCENSION CHRISTIAN HIGH SCHOO ASCENSION DIOCESAN REGIONAL SC ASCENSION EPISCOPAL SCHOOL (AS ASSEMBLY CHRISTIAN SCHOOL (AG) ASSUMPTION HIGH SCHOOL ATLANTA SCHOOL AVOYELLES HIGH SCHOOL BAKER HIGH SCHOOL BASILE HIGH SCHOOL BASTROP HIGH SCHOOL BATON ROUGE INTERNATIONAL SCHOOL BATON ROUGE MAGNET HIGH SCHOOL BEAU CHENE HIGH SCHOOL BEEKMAN CHARTER SCHOOL BELAIRE HIGH SCHOOL BELL CITY HIGH SCHOOL BELLE CHASSE HIGH SCHOOL BENJAMIN FRANKLIN HIGH SCHOOL BEN'S FORD CHRISTIAN SCHOOL (B BENTON HIGH SCHOOL BERCHMANS ACADEMY OF THE SACRED HEART (C) BERWICK HIGH SCHOOL BETHANY CHRISTIAN SCHOOL BETHEL CHRISTIAN SCHOOL BETHEL CHRISTIAN SCHOOL (B) BISHOP MCMANUS SCHOOL BLOCK HIGH SCHOOL BOGALUSA HIGH SCHOOL BOLTON HIGH SCHOOL BONNABEL MAGNET ACADEMY HIGH S BOOKER T. WASHINGTON NEW TECHN BOSSIER HIGH SCHOOL BREAUX BRIDGE HIGH SCHOOL BRIARFIELD ACADEMY BRIGHTER HORIZON SCHOOL OF BAT BRIGHTON SCHOOL BROADMOOR SENIOR HIGH SCHOOL BROTHER MARTIN SR. HIGH SCHOOL BRUSLY HIGH SCHOOL BUCKEYE HIGH SCHOOL BUNKIE HIGH SCHOOL C.E. BYRD HIGH SCHOOL CABRINI HIGH SCHOOL (GIRLS) (C CADDO -

2011-2012 Top Gains Schools

Louisiana Believes 2011-2012 TOP GAINS SCHOOLS For the 2011-2012 school year, 440 schools were designated as Top Gains schools, which are schools that improved their School Performance Score by or beyond a pre-determined growth goal. The following Top Gains schools will receive $8,500 each for educational purposes within the school: Acadia Parish Church Point High School Richard Elementary School Egan Elementary School South Crowley Elementary School Mermentau Elementary School South Rayne Elementary School Midland High School Iota High School Morse Elementary School Allen Parish Elizabeth High School Oakdale High School Fairview High School Oberlin Elementary School Kinder Elementary School Oberlin High School Kinder High School Reeves High School Oakdale Elementary School Kinder Middle School Ascension Parish Donaldsonville High School Galvez Primary School Dutchtown Middle School Lake Elementary School East Ascension High School Dutchtown Primary Schoolh Galvez Middle School St. Amant Primary School Prairieville Middle School Pecan Grove Primary School St. Amant Middle School Prairieville Primary School St. Amant High School Central Primary School Dutchtown High School Spanish Lake Primary School Assumption Parish Assumption High School Pierre Part Primary School Belle Rose Primary School Napoleonville Primary School Louisiana Believes Beauregard Parish DeRidder High School Singer High School East Beauregard High School South Beauregard High School Merryville High School Bienville Parish Gibsland-Coleman High School Ringgold High School Bossier Parish Airline High School T.L. Rodes Elementary School Benton High School Stockwell Place Elementary School Curtis Elementary School Benton Middle School Haughton High School Princeton Elementary School Parkway High School Legacy Elementary School Platt Elementary School W.T. -

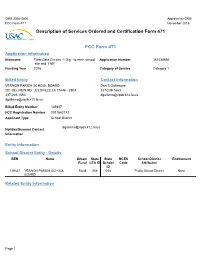

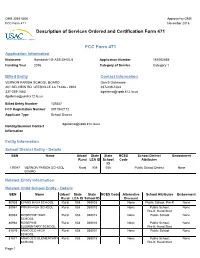

Description of Services Ordered and Certification Form 471 FCC Form

OMB 3060-0806 Approval by OMB FCC Form 471 November 2015 Description of Services Ordered and Certification Form 471 FCC Form 471 Application Information Nickname Fiber Data Circuits -1 Gig - to each school Application Number 161038692 site and 1 NIF Funding Year 2016 Category of Service Category 1 Billed Entity Contact Information VERNON PARISH SCHOOL BOARD Don S Gallemore 201 BELVIEW RD LEESVILLE LA 71446 - 2904 337-239-1663 337-239-1663 [email protected] [email protected] Billed Entity Number 139347 FCC Registration Number 0011542172 Applicant Type School District [email protected] Holiday/Summer Contact Information Entity Information School District Entity - Details BEN Name Urban/ State State NCES School District Endowment Rural LEA ID School Code Attributes ID 139347 VERNON PARISH SCHOOL Rural 058 058 Public School District None BOARD Related Entity Information Page 1 Related Child School Entity - Details BEN Name Urban/ State State NCES Code Alternative School Attributes Endowment Rural LEA ID School ID Discount 80938 EVANS HIGH SCHOOL Rural 058 058003 None Public School; Pre-K None 80961 PITKIN HIGH SCHOOL Rural 058 058010 None Public School; None Pre-K; Head Start 80963 ROSEPINE HIGH Rural 058 058012 None Public School None SCHOOL 80964 ROSEPINE Rural 058 058016 None Public School; None ELEMENTARY SCHOOL Pre-K; Head Start 81876 ANACOCO HIGH Rural 058 058001 None Public School None SCHOOL 81877 ANACOCO ELEMENTARY Rural 058 058018 None Public School; None SCHOOL Pre-K; Head Start 81913 HORNBECK HIGH Rural 058 058005 -

2019 Teacher Leaders Summit

2019 Teacher Leaders Summit - Day 3 June 28, 2019 Attendee Last Name First Name Email Status Job Title Company Southwest Louisiana Charter Aaron Devonte [email protected] Checked In Teacher Academy Abbott Jessica [email protected] Checked In New Teacher Coach Caddo Parish Public Schools St. Charles Parish Public Abdin Tanesha [email protected] Checked In Dr. Tanesha Abdin Schools Abdol Hedaaya [email protected] Checked In Math Teacher Success at Thurgood Marshall Abernathy Joy [email protected] Checked In Abney Madora [email protected] Checked In Assistant Principal Apollo Elementary School Abraham Erin [email protected] Checked In Facilitator Teaching Lab Accardo Alexis [email protected] Checked In Achor Krista [email protected] Checked In teacher Plaquemines Livingston Parish Public Achord Gabrielle [email protected] Checked In Educator Schools Acosta Jeanna [email protected] Checked In Assistant Director Carousel Preschool Director of Educational Adamek Joey [email protected] Checked In Partnerships Agile Mind Adams Blanche [email protected] Checked In Field Supervisor iTeachLouisiana Adams Donna [email protected] Checked In Teacher Vernon Parish School Board [email protected] Adams Johnnie m Checked In Principal Central High Tangipahoa Parish School Adams Valerie [email protected] Checked In Teacher Board Ouachita Parish School Adams Melinda [email protected] Checked In Master Teacher System Adams Vanessa [email protected] Checked In Curriculum Franklin Parish School Board Adams Kim [email protected] Checked In Principal Caldwell Parish School System Algiers Charter Landry Walker Adams Igenue [email protected] Checked In Master Teacher HS Adams- Graves Ashley [email protected] Checked In teacher West Carroll School District Adcock Stacy [email protected] Checked In Data Coordinator Richland Parish School Board St. -

Statewide Student Profile System System Specifications

Statewide Student Profile System System Specifications August 25, 2003 BoR Statewide Student Profile System Specifications Page 2 LOUISIANA BOARD OF REGENTS Statewide Student Profile System July 15, 2003 Memorandum to Users Due to the development and implementation timeline of the Student Transcript System (Louisiana high school transcript data), the following data elements for academic year 2003-04 (Fall, Winter, or Spring): 1) High School Grade Point Average, 2) High School Percentile Rank, and 3) Board of Regents' Core Flag will: a) NOT be required for in-state students and b) be OPTIONAL for out-of-state students. These elements will become active and required in Fall 2004. Regents' Staff BoR Statewide Student Profile System Specifications Page 3 LOUISIANA BOARD OF REGENTS Statewide Student Profile System Systems Specifications Due Date: Fall Semester/Quarter January 15 Winter Quarter March 15 Spring Semester/Quarter June 15 Summer Semester/Quarter September 15 Report Scope: 14th class day (or equivalent) census of current term enrollment, but collected at the end of term to facilitate the compilation of student level term outcomes. Reporting Medium: (1) The preferred reporting medium is via electronic File Transfer Protocol (FTP). An FTP site has been set up for this purpose. You will need the following information to access the site: Logon ID: anonymous Password: call (225) 342-4253 to obtain current password Format: ASCII with CR+LF following each record IP Address: as400.regents.state.la.us or 198.176.252.98 Filename: SPSINPUT.SPXXYZZ Where; XX = BoR Institution Code Y = Semester/Term ZZ = Academic Year Begin (exclude century) NOTE: After the file has been transmitted, send e-mail to [email protected] indicating the successful upload of the file. -

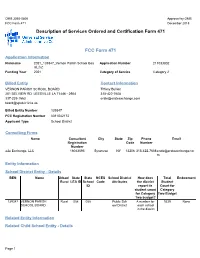

Description of Services Ordered and Certification Form 471 FCC Form

OMB 3060-0806 Approval by OMB FCC Form 471 November 2015 Description of Services Ordered and Certification Form 471 FCC Form 471 Application Information Nickname Hornbeck-1G-ASE30HGL5 Application Number 161052485 Funding Year 2016 Category of Service Category 1 Billed Entity Contact Information VERNON PARISH SCHOOL BOARD Don S Gallemore 201 BELVIEW RD LEESVILLE LA 71446 - 2904 337-239-1663 337-239-1663 [email protected] [email protected] Billed Entity Number 139347 FCC Registration Number 0011542172 Applicant Type School District [email protected] Holiday/Summer Contact Information Entity Information School District Entity - Details BEN Name Urban/ State State NCES School District Endowment Rural LEA ID School Code Attributes ID 139347 VERNON PARISH SCHOOL Rural 058 058 Public School District None BOARD Related Entity Information Related Child School Entity - Details BEN Name Urban/ State State NCES Code Alternative School Attributes Endowment Rural LEA ID School ID Discount 80938 EVANS HIGH SCHOOL Rural 058 058003 None Public School; Pre-K None 80961 PITKIN HIGH SCHOOL Rural 058 058010 None Public School; None Pre-K; Head Start 80963 ROSEPINE HIGH Rural 058 058012 None Public School None SCHOOL 80964 ROSEPINE Rural 058 058016 None Public School; None ELEMENTARY SCHOOL Pre-K; Head Start 81876 ANACOCO HIGH Rural 058 058001 None Public School None SCHOOL 81877 ANACOCO ELEMENTARY Rural 058 058018 None Public School; None SCHOOL Pre-K; Head Start Page 1 BEN Name Urban/ State State NCES Code Alternative School Attributes Endowment -

Description of Services Ordered and Certification Form 471 FCC Form

OMB 3060-0806 Approval by OMB FCC Form 471 December 2018 Description of Services Ordered and Certification Form 471 FCC Form 471 Application Information Nickname 2021_139347_Vernon Parish School Boa Application Number 211033802 rd_C2 Funding Year 2021 Category of Service Category 2 Billed Entity Contact Information VERNON PARISH SCHOOL BOARD Tiffany Bullion 201 BELVIEW RD LEESVILLE LA 71446 - 2904 315-422-7608 337-239-1663 [email protected] [email protected] Billed Entity Number 139347 FCC Registration Number 0011542172 Applicant Type School District Consulting Firms Name Consultant City State Zip Phone Email Registration Code Number Number e2e Exchange, LLC 16043595 Syracuse NY 13206 315-422-7608 [email protected] m Entity Information School District Entity - Details BEN Name Urban/ State State NCES School District How does Total Endowment Rural LEA ID School Code Attributes the district Student ID report its Count for student count Category for Category Two Budget Two budget? 139347 VERNON PARISH Rural 058 058 Public Sch A number for 9239 None SCHOOL BOARD ool District each school in the district Related Entity Information Related Child School Entity - Details Page 1 BEN Name Urban/ State State NCES Alternative School Attributes Total Endowment Rural LEA ID School ID Code Discount Students for C2 Budget 80938 EVANS HIGH SCHOOL Rural 058 058003 None Pre-K; Public School 382 None 80961 PITKIN HIGH SCHOOL Rural 058 058010 None Head Start; Pre- 512 None K; Public School 80963 ROSEPINE HIGH SCH Rural 058 058012 None Public School