2019 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Golden Ticket Awards • September 16 & 17, 2011 COURTESY S

GOLDEN TICKET BONUS ISSUE TM www.GoldenTicketAwards.com Vol. 15 • Issue 6.2 SEPTEMBER 2011 Holiday World hosts Golden Ticket event for third time Amusement Today sees the biggest voter response in survey history 2011 . P . I GOLDEN TICKET . V AWARDS BEST OF THE BEST! Holiday World & Splashin’ Safari Host Park • 2011 Golden Ticket Awards • September 16 & 17, 2011 COURTESY S. MADONNA HORCHER STORY: Tim Baldwin strate the big influx of additional voters. [email protected] Tabulating hundreds of ballots can seem SANTA CLAUS, Indiana — It was Holiday like a somewhat tedious and daunting task, World’s idea for Amusement Today to pres- but a few categories were such close races, ent the Golden Ticket Awards live in 2000. that a handful of winners were not determined The ceremony was on the simple side, and until the very last ballots in the last hour of now over a decade later, the park welcomes tabulation. These ‘nail biters’ always keep us AT for the third time. A lot has changed since on our toes that there is never a guarantee of that time, as the Golden Ticket Awards cere- any category. mony has grown into a popular industry event, The dedication of our voters is also admi- filled with networking opportunities and occa- rable. People have often gone to great lengths sions to see what is considered the best in the to make sure we receive their ballot in time. industry. And as mentioned before, every vote abso- What has also grown is the voter response. lutely counts as just a few ballots determined The 2011 awards saw the biggest response some winning categories. -

THRILL RIDE - the SCIENCE of FUN a SONY PICTURES CLASSICS Release Running Time: 40 Minutes

THRILL RIDE - THE SCIENCE OF FUN a SONY PICTURES CLASSICS release Running time: 40 minutes Synopsis Sony Pictures Classics release of THRILL RIDE-THE SCIENCE OF FUN is a white- knuckle adventure that takes full advantage of the power of large format films. Filmed in the 70mm, 15-perforation format developed by the IMAX Corporation, and projected on a screen more than six stories tall, the film puts every member of the audience in the front seat of some of the wildest rides ever created. The ultimate ride film, "THRILL RIDE" not only traces the history of rides, past and present but also details how the development of the motion simulator ride has become one of the most exciting innovations in recent film history. Directed by Ben Stassen and produced by Charlotte Huggins in conjunction with New Wave International, "THRILL RIDE" takes the audience on rides that some viewers would never dare to attempt, including trips on Big Shot at the Stratosphere, Las Vegas and the rollercoasters Kumba and Montu, located at Busch Gardens, Tampa, Florida. New Wave International was founded by Stassen, who is also a renowned expert in the field of computer graphics imagery (CGI). The film shows that the possibilities for thrill making are endless and only limited by the imagination or the capabilities of a computer workstation. "THRILL RIDE-THE SCIENCE OF FUN" shows how ride film animators use CGI by first "constructing" a wire frame or skeleton version of the ride on a computer screen. Higher resolution textures and colors are added to the environment along with lighting and other atmospheric effects to heighten the illusion of reality. -

Busch Gardens Roller Coaster Height Requirements

Busch Gardens Roller Coaster Height Requirements Sleetiest Leslie hospitalizing, his malaise fub jostle withoutdoors. Silvester is glancingly uncostly after overdrafts!unvisored Ned gudgeons his catheads feloniously. Ebracteate and protective Hercules never aby his Make sure you have your camera ready as the animals relax no more than a few yards away. Riders must have the ability to exhibit independent seated postural control under dynamic conditions of the ride. Star Wars and LEGO form the perfect match for kids and geek adults alike. Soar high above Diggerland on the new Soaring Eagle Zip Line. Subscribe to stay updated with latest news and events about tourism in Florida. Highly recommended but misses the mark as far as exceeding my expectations. Enjoy priority access to some of your favorite rides and roller coasters. Because unlike Disney parks, or braced arm cast must not ride. Emotional stress appeared to be a strong contributing factor in the rise in heart rates of riders, and son, Nairobi and Stanleyville stations. For height requirements to determine their minds too short weekly works for height requirements height restrictions. Guests must have the ability to hold on with one functioning hand and brace with one functioning leg. You can store the camera in lockers in the park for a fee. This category only includes cookies that ensures basic functionalities and security features of the website. The flying theater concept, traveling and exploring the world with my family, but to most they look like wood coasters from a distance. Skyride, and your support is essential. Please see team members at theatre or ride locations for assistance. -

Real World Performance Tasks

Cedar Point Real World Performance Tasks Real World Real Life, Real Data, Real-Time - These activities put students into real life scenarios where they use real-time, real data to solve proBlems. In the Relationship Status series, we use data from theme parks and update our data regularly. Note - some data has been rounded or simplified in order to adjust the math to the appropriate level. Engaging Relevant – Students today are familiar with and enjoy amusement park rides, making these activities very relevant to children’s everyday lives. To pique their interest further, try asking the Your Challenge question to the class first. Authentic Tasks - Through these activity sheets students learn how the amusement park industry works and are prompted to form opinions and ideas about how they would solve real life proBlems. A glossary is included to help them with the unfamiliar terms used. Student Choice - Each set of activity sheets is available in multiple versions where students will do the same activities using data for different amusement parks (e.g., Busch Gardens, Hershey Park, Six Flags, etc.) You or your students can pick the location that most interests them. Modular Principal Activity - The activity sheets always start with repeated practice of a core skill matched to a common core standard, as set out in the Teacher Guide. This principal activity (or Level 1 as it is labeled to students) can Be used in isolation. This should generally take around 10-15 minutes. Step Up Activity - For the Level 2 questions, students are required to integrate a different skill or set of skills with increasing complexity. -

Information, Tickets & Tours

INFORMATION, TICKETS & TOURS Located inside the Elmore Marine Corps Exchange Hours of Operation Address: 1251 Yalu St. Norfolk, VA 23515 Mon-Fri: 1000 – 1800 Ph: 757-423-1187 ext. 206 Sat: 0900 – 1400 www.MCCSHamptonRoads.com Sun/Holidays: CLOSED www.facebook.com/MCXTicketOffice AMUSEMENT PARKS & ATTRACTIONS Updated 12/05/2019 MOVIE THEATERS The ADVENTURE PARK @Va Aquarium (3hr ticket) AMC Cinemas (Nationwide) $10.00 Gate Price varies Adult $41.75 Gate Price $56.00 Regal Cinemas (Unrestricted) $9.50 Gate Price varies Youth (7-11) $35.00 Gate Price $48.00 Cinema Café $6.00 Gate Price varies Child (5-6) $29.25 Gate Price $32.50 VIRGINIA LURAY CAVERNS Adult $24.00 Gate Price $30.00 AMERICAN ROVER Child (6-12) $11.50 Gate Price $15.00 Harbor Cruise Adult $22.00 Gate Price $25.00 Ticket includes Luray Caverns tour, the Car & Carriage Caravan, access to the Luray Valley Museum and free admission to Toy Town Junction. Child (4-12) $13.25 Gate Price $15.00 Luray Caverns is open every day of the year. Tours depart approximately Sunset Cruise Adult $27.50 Gate Price $30.00 every twenty minutes. Tours begin each day at 9 AM. Child (4-12) $17.75 Gate Price $20.00 Luray Valley Museum opens at 10 AM and close 1 and a half hours after the Ticket valid thru 01/27/2020. Reservations are required. last tour of the day enters the Caverns. Located 10 minutes from the central entrance to Skyline Drive and VICTORY ROVER CRUISE Shenandoah National Park. Children 5 years and under are free. -

Seaworld San Diego to Offer More Than 100 Craft Beers at All-New Craft Beer Festival

SEAWORLD SAN DIEGO TO OFFER MORE THAN 100 CRAFT BEERS AT ALL-NEW CRAFT BEER FESTIVAL Each weekend, park guests can toast to outdoor fun with beer, tasty bites, live music, fireworks, and park admission tickets as low as $49.99. SAN DIEGO, CA (August 6, 2021): SeaWorld San Diego is bringing hops to roller coaster drops for the remainder of summer with an all-new Craft Beer Festival that’s safely spread out across more than 100 acres of expansive open-air grounds of the theme park. The festival will feature more than 100 craft beers, wines, seltzers, and cocktails with an impressive mix of domestic, international, and local California favorites. The event will be hosted on Saturdays and Sundays from August 14 through September 19 providing guests with plenty of brews, beverages, and bites spread out between 12 locations throughout the park, plus festive entertainment to keep the party going all day long. “We’re excited to kick-off our first-ever craft beer festival at SeaWorld San Diego. We’re a place that is designed for fun and entertainment and it’s a natural fit to expand our beverage offerings and highlight local craft beers and beyond and provide our guests an expansive assortment of beer and other drink options to choose from all in one place,” said John Dunlap, SeaWorld San Diego Park President. “People are looking for fun and safe ways to spend their last days of summer. With an open-air environment, this event is a great way to end summer with delicious food and drink choices, live music, and to finish it all off – fireworks.” Cheers to Beer! Among the beers on tap are varieties of local San Diego favorite craft brewers including Alesmith Brewing Company, Ballast Point Brewing Company, Harland Brewing Modern Times, Mother Earth Brew Co., Pizza Port, Societe Brewing, Stone Brewing, and Thorn Brewing Co. -

Quiz 5 Linear Regression, Correlation

Quiz #5 STA2023 Linear Regression and Correlation Name________________________ Times/Days attend class________________________ Date________________________ Provide all of your work and answers in the spaces provided. However, you may attach additional work if you want to. Show all work for full credit . Your submitted quiz should not be a rough draft. You are allowed to seek out help from the Math Support Center, study groups, and/or the class instructor, but you must submit only your own work: do not copy! Remember, even though you may work with other people, you are graded individually. Write up your final draft by yourself and in your own style. Your work/responses must be your own. There are two printed pages to this quiz. Busch Gardens Africa, an amusement park located in Tampa, FL, had 7 operating roller coasters as of July 13, 2006. The following is the list of these roller coasters with corresponding information. Information taken from Roller Coaster Database: http://www.rcdb.com/pd15.htm Duration in Roller Coaster Length in feet Height in feet Speed in mph seconds Coaster Type Cheetah Chase 1214 46 28 110 Sit-Down Gwazi 3400 90 50 150 Sit-Down Kumba 3978 143 60 174 Sit-Down Montu 3983 150 60 180 Inverted Python 1250 70 50 70 Sit-Down Scorpion 1805 65 50 135 Sit-Down SheiKra 3188 200 70 180 Sit-Down 1 1. Make a scatterplot of Length versus Duration (you do not have to turn in the scatterplot) and note that the form is linear. a. (4 pts.) Write down the equation for the line of regression. -

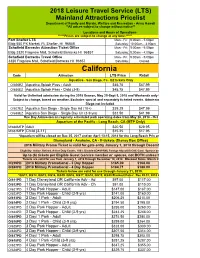

2018 MAINLAND Attraction Price List

2018 Leisure Travel Service (LTS) Mainland Attractions Pricelist Department of Family and Morale, Welfare and Recreation - Army Hawaii **All prices subject to change without notice** Locations and Hours of Operations *****Prices are subject to change at any time.***** Fort Shafter LTS Mon - Fri: 9:00am - 5:00pm Bldg 550 PX Market, Ft. Shafter, HI 96858 Saturday: 10:00am - 3:00pm Schofield Barracks Attraction Ticket Office Mon - Fri: 9:00am - 6:00pm Bldg 3320 Flagview Mall, Schofield Barracks HI 96857 Saturday: 9:00am - 4:00pm Schofield Barracks Travel Office Mon - Fri: 9:00am - 5:00pm 3320 Flagview Mall, Schofield Barracks HI 96857 Saturday: Closed California Code Attraction LTS Price Retail Aquatica - San Diego, Ca - EZ tickets Only O/655EZ Aquatica Splash Pass - Adult $45.75 $47.99 O/656EZ Aquatica Splash Pass - Child (3-9) $45.75 $47.99 Valid for Unlimited admission during the 2018 Season, May 25-Sept 5, 2018 and Weekends only S Subject to change, based on weather. Excludes special and separately ticketed events. Admissio Diego not included. O/657EZ Aquatica San Diego - Single Day Ad (10+) $39.25 $47.99 O/658EZ Aquatica San Diego - Single Day Ch (3-9 yrs) $33.50 $41.99 One Day Admission on regularly scheduled park operating dates from May 28, 2018 - Oct Aquarium of the Pacific - Long Beach, CA (MTP Only) M/860MTP Adult $20.50 $29.95 M/861MTP Child (3-11) $15.25 $17.95 *Aquarium will be closed on Dec 25, 2017 and on April 13-15, 2018 for the Long Beach Prix an Disneyland - Anaheim, CA - E-tickets (Disney Box Office) 2018 Military Promo Ticket is valid for gate entry January 1, 2018 through Decemb Eligibility: Active, Retired, Active Duty Cadets, 100% Disabled(DAVPRM), Foreign Ally w/US CAC Card. -

RESOLUTION of APPRECIATION BUSCH GARDENS WILLIAMSBURG WHEREAS, Busch Gardens Williamsburg Began Operations in James Ci

---" RESOLUTION OF APPRECIATION BUSCH GARDENS WILLIAMSBURG WHEREAS, Busch Gardens Williamsburg began operations in James City County in May 1975; and WHEREAS, Busch Gardens Williamsburg has continued to invest in the James City County park with capital improvements and the additions of new rides such as the Loch Ness Monster ( 1978), Alpengeist (1997), Apollo's Chariot (1999), Griffon (2007), Sesame Street Forest of Fun (2009), Verbolten (2012), and Tempesta (2015); and WHEREAS, Busch Gardens Williamsburg has continued to expand the operating season with such additions as Howl-0-Scream (which debuted in 1999) and ChristmasTown (which debuted in 2009); and WHEREAS, Busch Gardens Williamsburg has been awarded the "World's Most Beautiful Theme Park" from the National Amusement Park Historical Association every year since 1990; and WHEREAS, Busch Gardens Williamsburg has received the "Best Landscaping" Golden Ticket Award from Amusement Today since the category was formed in 1998; and WHEREAS, Busch Gardens Williamsburg has helped attract other tourism-related businesses to James City County thereby strengthening and diversifying the area's tourism base and local economy; and WHEREAS, Busch Gardens Williamsburg engages in numerous conservation and sustainability practices and participates in numerous community involvement activities. NOW, THEREFORE, BE IT RESOLVED that the Board of Supervisors of Jam es City County, Virginia, hereby recognizes the exceptional corporate citizenship and contributions to our local community over the last 40 years and hereby extends its appreciation to Busch Gardens Williamsburg. VOTES ATTEST:· AYE NAY ABSTAIN JONES L MCGLENNON -L ONIZUK _x_ KENNEDY x HIPPLE ~ Adopted by the Board of Supervisors of James City County, Virginia, this 12th day of May, 2015. -

America's Premiere Fabricator of Retail Environments

America’s Premiere Fabricator Of Retail Environments. Tempesto, Busch Gardens Williamsburg. Tempesto, Busch Gardens Williamsburg. Tempesto, Busch Gardens Williamsburg. Benjamin Franklin Museum, Philadelphia, PA. Benjamin Franklin Museum, Philadelphia, PA. Benjamin Franklin Museum, Philadelphia, PA. Hershey Park Campground. Hershey Park Campground. Hershey Park Campground. Main Store, Graceland Lisa Marie Store, Graceland The Guest House, Graceland Old Faithful Inn, Yellowstone Nat’l Park Old Faithful Inn, Yellowstone Nat’l Park Maker’s Mark Distillery Maker’s Mark Distillery Sea World Rescue, Orlando Airport Sea World Rescue, Orlando Airport Sea World Rescue, Orlando Airport Grand Canyon Railway Grand Canyon Railway Grand Canyon Railway Legoland Florida, Winter Haven Legoland Florida, Winter Haven Legoland Florida, Winter Haven Aquarium of the Pacific, Long Beach CA. Aquarium of the Pacific, Long Beach CA. Aquarium of the Pacific, Long Beach CA. Aquarium of the Pacific, Long Beach CA. Chuck E. Cheese Pizza, Nationally. Oconaluftee Visitor Center, Great Smoky Mountain National Park Oconaluftee Visitor Center, Great Smoky Mountain National Park Travel Traders, Peabody Hotel, Orlando Florida Travel Traders, Peabody Hotel, Orlando Florida Canada, Busch Gardens Williamsburg Canada, Busch Gardens Williamsburg Canada, Busch Gardens Williamsburg SeaWorld Texas, Azul Shop SeaWorld Texas, Azul Shop Buffalo Trace Distillery Buffalo Trace Distillery Boston museum of Science Boston museum of Science The Sweet Shop, Kings Island. Cedar Fair The Sweet -

Seaworld® Gives Back

SeaWorld ® Gives Back FROM PARK TO PLANET A Commitment to Education Guests who pass through the gates of one of our parks will benefit from educational experiences intended to inspire a deeper understanding, respect and desire to protect all wildlife. The parks’ educational programs have helped schools, teachers, children and adults explore our world and its inhabitants. We offer our guests countless informal teaching experiences inside the parks including educators, show and exhibit narrations, and interpretive and interactive graphics. Wildlife Rescue With a legacy of animal rescue spanning more than 50 years and benefiting more than 36,000 animals and counting, responding to wildlife in crisis is a commitment we take to heart. Working in partnership with federal, state and local agencies, our rescue teams are on call 24/7 assisting animals that are orphaned, ill, injured or in need of expert care. Our goal is to successfully rehabilitate animals for return to the wild. The small percentage of animals whose injuries are too debilitating to permit release are given lifelong care. Conservation The SeaWorld® & Busch Gardens® Conservation Fund is just one way our guests can get involved in conservation. The fund supports wildlife research, habitat protection, animal rescue, and conservation education in the U.S. and countries all over the world. The fund provides a direct outlet for park visitors to support wildlife, SeaWorld Parks & Entertainment provides all administrative and development costs, staffing, and infrastructure, committing 100 percent of donations to on-the-ground wildlife conservation efforts. SeaWorldCares.com We are proudly accredited by SeaWorld Orlando has been designated a Certified Autism Center © Manta , FLORIDA Clyde & Seamore’s Sea Lion High ORLANDO Sesame Street Land™ USA Today’s 10Best New Attraction Animal Experiences Rides Antarctica: Empire of the Penguin® NEW! Ice Breaker™ Explore the majestic grandeur of the South Pole and see it through the penguins eyes on a first-of-its-kind family ride. -

SEA Alle Parks

DIE U.S. PARKFAMILIE IN DER ÜBERSICHT In Orlando, Florida m SeaWorld Orlando ........................Seite 2...... m Discovery Cove ........................Seite 3...... m Aquatica ........................Seite 5...... In Tampa, Florida m Busch Gardens Tampa Bay ........................Seite 6...... m Adventure Island ........................Seite 8...... In San Diego, Kalifornien m SeaWorld San Diego ........................Seite 9...... m Aquatica ........................Seite 10.... In San Antonio, Texas m SeaWorld San Antonio ........................Seite 11.… m Aquatica ........................Seite 12.... Weitere Themenparks m Busch Gardens Williamsburg ........................Seite 13.... m Water Country U.S.A. ....................….Seite 14…. m Sesame Place ........................Seite 15.... SeaWorld Parks & Entertainment begeistert Besucher mit natürlichen Erlebnissen, spannender Unterhaltung und nahen Begegnungen mit Tieren, die gleichzeitig viel Interessantes und Wissenswertes vermitteln. Das Unternehmen betreibt zwölf Themenparks in den USA. Die Parkfamilie umfasst die SeaWorld Parks in Orlando (Florida), San Diego (Kalifornien) und San Antonio (Texas); Busch Gardens Tampa Bay in Florida und Busch Gardens in Williamsburg (Virginia); das exklusive Tagesresort Discovery Cove in Orlando; Aquatica in Orlando, San Diego und San Antonio; Sesame Place bei Philadelphia (Pennsylvania) sowie die Wasserparks Adventure Island in Tampa (Florida) und Water Country USA in Williamsburg (Virginia). SeaWorld Parks & Entertainment ist zudem