CONFIRMED Minutes Audit Committee Meeting 17 March 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Government of Western Australia Department of Environment Regulation

Government of Western Australia Department of Environment Regulation NOTIFICATION OF APPLICATIONS RECEIVED FOR WORKS APPROVALS, LICENCES AND AMENDMENTS AND AVAILABLE FOR PUBLIC SUBMISSIONS AND/OR REGISTRATIONS OF INTEREST APPLICATIONS FOR WORKS APPROVALS AND NEW LICENCES Solid waste facility: Shire of Sandstone (Sandstone Refuse Site), Lot 302 on Plan 44609 Agnew Rd, Sandstone, SANDSTONE (W5625/2014/1) [*2] Class II or III putrescible landfill site: City of Busselton (Vidler Rd Class II landfill site), Western Cape Dr, Naturaliste, NATURALISTE (W5621/2014/1) [*4] Compost manufacturing and soil blending: Aussie Organics Garden Supplies Pty Ltd (Aussie Organics), Punrak Rd, Serpentine, SERPENTINE (W5626/2014/1) [*4] Livestock saleyard or holding pen: Shire of Katanning (Katanning Regional Sheep Saleyard), Katanning-Nyabing Road, Katanning 6317, KATANNING (L8814/2014/1) [*5] APPLICATIONS FOR LICENCE RENEWALS Alcoholic beverage manufacturing: Cape Mentelle Vineyards Ltd, Wallcliffe Rd, Margaret River, (L7714/2001/7) [*4] Timber preserving: Wespine Industries Pty Ltd, Moore Rd, Dardanup West, (L8357/2009/2) [*4] Timber preserving: Phillip Norman Bario & Robert Michael Bario (Minorba Grazing Co. Timber Treatment Plant), Albany Highway, Narrikup, (L7398/1999/8) [*5] Mine dewatering: Newmont Boddington Gold Pty Ltd, M70/21, Boddington (L8306/2008/2) [*4] Submissions may be forwarded to the Department of Environment Regulation Regional Office (address specified below) within 21 days of this advertisement. For Copies of applications please contact -

Aged Care Plan 2012 July, 2012 Shire of Boddington Adopted 19Th February 2013

Aged Care Plan 2012 July, 2012 Shire of Boddington Adopted 19th February 2013 Verso Consulting Pty Ltd Mail Verso Consulting PO Box 412 CLIFTON HILL VIC 3068 Telephone +61 3 9489 3233 Facsimile +61 3 9489 3244 Email [email protected] Website www.verso.com.au While Verso Consulting Pty Ltd endeavours to provide reliable analysis and believes the material it presents is accurate, it will not be liable for any claim by any party acting on such information. © Verso Consulting Pty Ltd verso is a registered Australian Trade Mark (Registration No 1142831) verso consulting pty ltd ii Executive summary Background In rural WA many Shires report that older persons are being forced to move from their local communities or are possibly refusing appropriate services for fear of being ‘removed’ from their local community and ‘put into a home’. This, in some instances, means that older persons and their family carers move from Boddington with a loss of social capital within the local community resulting in negative economic impacts into the long term. For over ten years, the Boddington community and the Shire Council have sought to address the needs of older persons in the community. Steps taken have included exploring the option for a large scale residential development; this was curtailed when it became evident that a development of this scale would not be feasable. Through a process of research and consultation, it became clear that the concept of a smaller scale village of ILUs would be sustainable and therefore this model has been explored. The Shire prepared a Positive Ageing Strategy in 2006 that further emphasised the need for more affordable housing for older people, in close proximity to health services and community facilities. -

Number of Total Fire Ban Declarations Per Fire Season

NUMBER OF TOTAL FIRE BAN DECLARATIONS PER FIRE SEASON LOCAL GOVERNMENT 2015/16 2016/17 2017/18 2018/19 2019/20 2020/21 Christmas Island 2 1 0 0 1 0 City of Albany 2 1 2 3 10 1 City of Armadale 11 4 0 5 17 18 City of Bayswater 10 1 0 1 7 6 City of Belmont 10 1 0 1 7 6 City of Bunbury 7 1 0 2 5 7 City of Busselton 6 1 0 2 5 7 City of Canning 10 1 0 1 7 6 City of Cockburn 10 1 0 1 7 6 City of Fremantle 10 1 0 1 7 6 City of Gosnells 11 4 0 5 17 18 City of Greater Geraldton 4 6 3 14 19 20 City of Joondalup 10 1 0 1 7 6 City of Kalamunda 11 4 0 5 18 18 City of Kalgoorlie-Boulder 2 8 10 14 20 9 City of Karratha 1 1 2 7 10 2 City of Kwinana 10 1 0 1 7 6 City of Mandurah 10 1 0 1 7 6 City of Melville 10 1 0 1 7 6 City of Nedlands 10 1 0 1 7 6 City of Perth 10 1 0 1 7 6 City of Rockingham 11 1 0 1 7 6 City of South Perth 10 1 0 1 7 6 City of Stirling 10 1 0 1 7 6 City of Subiaco 10 1 0 1 7 6 City of Swan 11 4 0 5 18 22 City of Vincent 9 1 0 1 7 6 City of Wanneroo 10 1 0 1 8 10 Cocos (Keeling) Islands 2 1 0 0 1 0 Indian Ocean Territories 2 1 0 0 1 0 Shire of Ashburton 1 2 4 11 11 3 Shire of Augusta Margaret River 7 1 0 0 6 3 Shire of Beverley 3 2 1 2 15 14 Shire of Boddington 6 3 1 0 7 11 Shire of Boyup Brook 6 3 0 1 6 7 Shire of Bridgetown- 6 3 0 1 6 7 Greenbushes Shire of Brookton 4 3 1 0 8 15 Shire of Broome 1 0 2 0 9 0 DFES – TOTAL FIRE BANS DECLARED PER YEAR PER LOCAL GOVERNMENT AREA Page 1 of 4 NUMBER OF TOTAL FIRE BAN DECLARATIONS PER FIRE SEASON LOCAL GOVERNMENT 2015/16 2016/17 2017/18 2018/19 2019/20 2020/21 Shire of Broomehill-Tambellup -

Dundas Woodlands Discovery Trail E

Kalgoorlie-BoulderKalgoorlie-Boulder City of Kalgoorlie-Boulder KambaldaKambalda Coolgardie-Esperance Hwy Lake Cowan CoolgardieCoolgardie Eyre Highway Shire of Coolgardie NorsemanNorseman Great Eastern Hwy SiteSite 11:11: WoodlandsWoodlands WalkWalk SiteSiteSite 10:10:10: LakeLakeLake CowanCowanCowan --- NorsemanNorsemanNorseman LookoutLookoutLookout SiteSiteSite 11:11:11: WoodlandsWoodlandsWoodlands WalkWalkWalk 1.5 4.0 4.04.04.04.04.04.04.04.0 4.04.04.04.04.04.04.04.04.04.04.04.0 4.04.04.04.04.04.04.04.04.04.04.04.0 Site 9: The Gem Fields Picnic Area 4.04.04.04.04.04.0 5.0 4.1 15.4 13.5 Site 8: The Woodland Picnic Area Lake Dundas Victoria Rock Rd Rock Victoria 20.6 Shire of Dundas 18.6 Coolgardie-Esperance Hwy 20.4 Site 7: Disappointment Rock Picnic Area 2.7 Site 6: Lake Johnston Camping Area Site 4: McDermid Rock Picnic Area 2.4 Site 5: Lake Johnston Picnic Area 18.5 Lake Johnston Holland Track Holland 13.1 Site 3: The Emily Anne Lay-By 0.4 SouthernSouthernGreat EasternCrossCross Hwy Navoria Track 19.0 Shire of Esperance Lake Hope Site 2: The Breakaways Camping Area 11.9 DundasDundas WoodlandsWoodlands DiscoveryDiscovery TrailTrail 12.8 SiteSiteSite 1:1:1: ShireShireShire BoundaryBoundaryBoundary ShireShireShire ofofof DundasDundasDundas ShireShireShireShireShireShire of of of ofofof Dundas Dundas Dundas DundasDundasDundas ShireShireShire ofofof KondininKondininKondinin ShireShireShireShireShireShire of of of ofofof Kondinin Kondinin Kondinin KondininKondininKondinin 25.4 Shire of Yilgarn Forrestania Rd Norseman-Lake King Rd 28.0 Holland Track Holland Shire of Ravensthorpe State Barrier Fence 5.0 39.0 Wave Rock Shire of Kulin 11.0 Shire of Kondinin e HydenHyden Prepared by: March 2002. -

Local Government Statistics 30/09/2020 As At

Local Government Statistics as at 30/09/2020 001 City of Albany Ward # Electors % Electors 01 Breaksea 4239 15.61% 02 Kalgan 4721 17.39% 03 Vancouver 4727 17.41% 04 West 4604 16.96% 05 Frederickstown 4435 16.34% 06 Yakamia 4421 16.29% District Total 27147 100.00% 129 City of Armadale Ward # Electors % Electors 01 Heron 6904 12.31% 02 River 7709 13.75% 03 Ranford 9016 16.08% 04 Minnawarra 7076 12.62% 05 Hills 7917 14.12% 06 Lake 9615 17.15% 07 Palomino 7842 13.98% District Total 56079 100.00% 105 Shire of Ashburton Ward # Electors % Electors 01 Ashburton 44 1.50% 03 Tom Price 1511 51.48% 04 Onslow 398 13.56% 06 Tableland 87 2.96% 07 Paraburdoo 615 20.95% 08 Pannawonica 280 9.54% District Total 2935 100.00% 002 Shire of Augusta-Margaret River Ward # Electors % Electors 00 Augusta-Margaret River 10712 100.00% District Total 10712 100.00% 130 Town of Bassendean Ward # Electors % Electors 00 Bassendean 11119 100.00% District Total 11119 100.00% Page : 1 Local Government Statistics as at 30/09/2020 003 City of Bayswater Ward # Electors % Electors 01 North 12100 25.99% 02 Central 11858 25.47% 03 West 13381 28.74% 04 South 9217 19.80% District Total 46556 100.00% 116 City of Belmont Ward # Electors % Electors 01 West 9588 37.68% 02 South 8348 32.80% 03 East 7513 29.52% District Total 25449 100.00% 004 Shire of Beverley Ward # Electors % Electors 00 Beverley 1317 100.00% District Total 1317 100.00% 005 Shire of Boddington Ward # Electors % Electors 00 Boddington 1179 100.00% District Total 1179 100.00% 007 Shire of Boyup Brook Ward # Electors -

Biosecurity Areas

Study Name Biosecurity Areas ! ! ! ! (! ! (! ! (! Warrayu!(Wyndham ! ! (! ! (! Ku(!nunurra !( M!irima !Nulleywah ! (! ! ! ! !! ! !!( ! ! !! (! (! !! ! ! ! (! Shire of !! Wyndham-East Kimberley ! (! !!(!! ! !! !! (! ! ! ! (! ! !! !! ! !(!! !! ! !(! (! (! ! ! ! (! ! !!(!! ! !!!! ! ! (! (! ! !!( ! !!!!! ! !!!!! ! ! (! (! ! ! (!!!! (!(! ! ! ( ! KIMB! ERLEY !!! ! ! ! ! ! !! ! ! ! De!(!r( by ! ! (! ! ! (! ! Shire of (! ! Derby-West Kimberley ! (! ! (!! (! ! ! ! ! (! Morrell Park!( ! ! ! ! !(!(B! roome Mallingbar ! Bilgungurr ! ! ! ! Fitzroy Crossing ( Y (! !(!(!( ! H! alls Creek !(!(! Mardiwah Loop!(!( ! Mindi Rardi ! !!( R ! !Junjuwa !! ! !! ! ! ! ! O ! Nicholson Block (! ( ! ! (! ! ( T !(! I ! ! ! ! ! ! ! R ! ! ! ! ! !!!(! R ! !( ! ! ! !! ! ! ! ! (! ! ! ! ! E ! (! ! ! Shire of Broome T ! ! (! Shire of Halls Creek (! (! (! ! N ! R E H (! T ! Port Hedland ! ! R (! O !(Tkalka Boorda ! ! N (! Karratha (! Dampier ! (! !( Roebourne C! heeditha ! City of Karratha Gooda Binya !( (! ! PILBARA ! Onslow (! Shire of East Pilbara !( Bindi Bindi ! !( I(!rrungadji Exmouth ! ! ! Shire of Ashburton Tom Price ! ! ! (! ! (! Paraburdoo Newman (! Parnpajinya !( ! (! (! Shire of Carnarvon Shire of ! Upper Gascoyne ! ! ! Carnarvon (! !( Mungullah GASCOYNE Shire of Ngaanyatjarraku ! !( Woodgamia Shire of Wiluna ! ! MID WEST Shire of Meekatharra ! ! ! ! ! ! ! ! ! Shire of (! ! ! Meekatharra !( Shark Bay Bondini Shire of Murchison ! A Shire of Cue I L ! ! A Kalbarri R T Leinster S ! ! Shire of Laverton U A Northampton Shire of Sandstone Shire of Leonora ! ! ( Shire -

Government of Western Australia Department of Environment Regulation

Government of Western Australia Department of Environment Regulation NOTIFICATION OF APPLICATIONS RECEIVED FOR CLEARING PERMITS AND AMENDMENTS AVAILABLE FOR PUBLIC SUBMISSIONS AND/OR REGISTRATIONS OF INTEREST Applications for clearing permits with a 7 day submission period 1. PA Horgan, Area Permit, Lot 661 on Deposited Plan 131668, Witchcliffe, Shire of Augusta-Margaret River, vineyard establishment, 12 native trees, (CPS 6729/1) 2. City of Albany, Area Permit, Norwood Road reserve (PIN 11748054), King River, City of Albany, road upgrades, 0.65ha, (CPS 6733/1) 3. City of Wanneroo, Purpose Permit, Lot 10823 on Deposited Plan 187676 – Reserve 11598, Spence Road reserve (PIN 1192731 and PIN 1141639), unnamed road reserve (PIN 11585469 and PIN 11751044), Pinjar, Crown Reserve 11598, Old Yanchep Road reserve (PIN 11751045), Neerabup, City of Wanneroo, road upgrades, 2.39ha, (CPS 6736/1) 4. City of Wanneroo, Purpose Permit, Lot 600 on Deposited Plan 302260, Lot 3021 on Deposited Plan 59574, Lot 2704 on Deposited Plan 89747 – Reserve 20432, Neerabup, Lot 1 on Diagram 43204, Lot 601 on Deposited Plan 302260, Old Yanchep Road reserve (PIN 11582355 and PIN 11543914), Pinjar, City of Wanneroo, road upgrades, 0.87ha, (CPS 6737/1) 5. E and G Henningheim, Area Permit, Lot 9083 on Deposited Plan 201677, Channybearup, Shire of Manjimup, re control, 4.4ha, (CPS 6751/1) 6. S and JM Payne, Area Permit, Lot 854 on Deposited Plan 134689, Walsall, City of Busselton, gravel extraction, 3.4ha, (CPS 6742/1) – readvertised for increase in clearing size by 0.4ha Applications for clearing permits with a 21 day submission period 1. -

Stakeholders Department of Commerce June 2011 Ist Quarter

Position Sponsors Karara Mining Ltd Oakajee Port and Rail Sinosteel Midwest Mid West Procurement City of Geraldton Greenough Officer Shire of Dalwallinu Quarterly Report Shire of Morawa Shire of Perenjori To Mid West Chamber of Commerce & Industry Stakeholders Department of Commerce June 2011 Ist Quarter Crossland Resources INDEX 1 Cover Page 2 Index 3 Executive Summary 4 Report against KPI’s EXECUTIVE SUMMARY – MID WEST PROCUREMENT OFFICER QUARTERLY REPORT BACKGROUND The Mid West Procurement Officer (MWPO) was appointed on the 18/1/2010 by the Mid West Chamber of Commerce and Industry as the Host agency. Following the departure of Vickie Petersen the MWCCI appointed John Evans to the MWPO position. John commenced on 28 February 2011. Funding for the position has been sourced from the following parties Karara Mining Ltd Shire of Perenjori Oakajee Port & Rail Mid West Chamber of Commerce Sinosteel Midwest and Industry City of Geraldton Greenough Shire of Dalwallinu Shire of Morawa Crosslands Resources Q1 ACTIVITY Attached is a report of activity to date against the KPI’s (KPI’s previously circulated to all stakeholders). The Industry data base is continuing in its development and is has moved from 339 businesses across the Mid West in the last report to 691 at the end of May 2011. The actual number of registered businesses is closer to 600 as many companies have multiple entries listed. Currently there are 218 Industry Categories in the database. The number of Company Profiles registered is 139 and further followup work is progressing on increasing this number. Further Business Network functions have been requested by the Shires of Dalwallinu, Morawa and Perenjori. -

Central Midlands Sub-Regional Economic Strategy

Central Midlands Sub-Regional Economic Strategy Prepared by RPS in collaboration with the Wheatbelt Development Commission Funded by Royalties for Regions, State Government of Western Australia rpsgroup.com.au Valuable support and input to the project was provided by the Central Midlands local governments including: . Shire of Chittering . Shire of Dalwallinu . Shire of Moora . Shire of Victoria Plains . Shire of Wongan-Ballidu Prepared by: Prepared for: RPS AUSTRALIA EAST PTY LTD THE WHEATBELT DEVELOPMENT COMMISSION 38 Station Street 298 Fitzgerald Street Subiaco, WA, 6008 NORTHAM WA 6401 T: +61 8 9211 1111 T: 08 9622 7222 F: +61 8 9211 1122 F: 08 9622 7406 E: [email protected] E: [email protected] W: www.wheatbelt.wa.gov.au Client Manager: Mark Wallace Report Number: 114880-1 Version / Date: FINAL rpsgroup.com.au Central Midlands Sub-Regional Economic Strategy Document Status Version Purpose of Document Orig Review Review Date WIP v1.0 WIP Report for client review SS MW 24.09.2013 DRAFT A Draft report for client review MW TC 18.03.2014 FINAL Final report for release MW TC 28.05.2014 Disclaimer This document is and shall remain the property of RPS. The document may only be used for the purposes for which it was commissioned and in accordance with the Terms of Engagement for the commission. Unauthorised copying or use of this document in any form whatsoever is prohibited. 114880-1; FINAL Page iii Central Midlands Sub-Regional Economic Strategy Summary In its current grouping The Central Midlands Sub-region is the Wheatbelt’s most diverse economy. -

Committee Attachments Wednesday, 17 August 2016

Committee Attachments Wednesday, 17 August 2016 REPORT PAGE REPORT TITLE AND ATTACHMENT DESCRIPTION NUMBER NUMBER(S) 10.1 Chittering Bushfire Advisory Committee – 12 July 2016 1 – 47 1. “Unconfirmed” draft minutes of the Chittering Bush Fire Advisory Committee meeting held on Tuesday, 12 July 2016 2. The Constitution of the Chittering Fire Service 10.2 Audit Committee – 9 August 2016 48 – 80 1. “Unconfirmed” minutes of the Audit Committee meeting held on 4 February 2015 2. Proposal from Moore Stephens Item 10.1 - Attachment 1 MINUTES OF THE CHITTERING BUSH FIRE ADVISORY COMMITTEE TUESDAY, 12 JULY 2016 Council Chambers 6177 Great Northern Highway Bindoon Commencement: 7.05pm Closure: 8.05pm Page 1 Item 10.1 - Attachment 1 These minutes will be confirmed at the Chittering Bushfire Advisory Committee to be held on 11 October 2016. SIGNED BY _____________________________________ Person presiding at the meeting at which minutes were confirmed DATE _____________________________________ Disclaimer The purpose of this Council meeting is to discuss and, where possible, make resolutions about items appearing on the agenda. Whilst Council has the power to resolve such items and may in fact, appear to have done so at the meeting, no person should rely on or act on the basis of such decision or on any advice or information provided by a member or officer, or on the content of any discussion occurring, during the course of the meeting. Persons should be aware that the provisions of the Local Government Act 1995 (section 5.25 (e)) establish procedures for revocation or rescission of a Council decision. No person should rely on the decisions made by Council until formal advice of the Council decision is received by that person. -

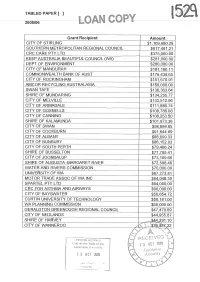

Tabled Paper [I

TABLED PAPER [I 2005/06 Grant Recipient Amount CITY OF STIRLING 1,109,680.28 SOUTHERN METROPOLITAN REGIONAL COUNCIL $617,461.21 CRC CARE PTY LTD $375,000.00 KEEP AUSTRALIA BEAUTIFUL COUNCIL (WA) $281,000.00 DEPT OF ENVIRONMENT $280,000.00 ITY OF MANDURAH $181,160.11 COMMONWEALTH BANK OF AUST $176,438.65 CITY OF ROCKINGHAM $151,670.91 AMCOR RECYCLING AUSTRALASIA 50,000.00 SWAN TAFE $136,363.64 SHIRE OF MUNDARING $134,255.77 CITY OF MELVILLE $133,512.96 CITY OF ARMADALE $111,880.74 CITY OF GOSNE LS $108,786.08 CITY OF CANNING $108,253.50 SHIRE OF KALAMUNDA $101,973.36 CITY OF SWAN $98,684.85 CITY OF COCKBURN $91,644.69 CITY OF ALBANY $88,699.33 CITY OF BUNBURY $86,152.03 CITY OF SOUTH PERTH $79,466.24 SHIRE OF BUSSELTON $77,795.41 CITY OF JOONDALUP $73,109.66 SHIRE OF AUGUSTA -MARGARET RIVER $72,598.46 WATER AND RIVERS COMMISSION $70,000.00 UNIVERSITY OF WA $67,272.81 MOTOR TRADE ASSOC OF WA INC $64,048.30 SPARTEL PTY LTD $64,000.00 CRC FOR ASTHMA AND AIRWAYS $60,000.00 CITY OF BAYSWATER $50,654.72 CURTIN UNIVERSITY OF TECHNOLOGY $50,181.00 WA PLANNING COMMISSION $50.000.00 GERALDTON GREENOUGH REGIONAL COUN $47,470.69 CITY OF NEDLANDS $44,955.87_ SHIRE OF HARVEY $44,291 10 CITY OF WANNEROO 1392527_ 22 I Il 2 Grant Recisien Amount SHIRE OF MURRAY $35,837.78 MURDOCH UNIVERSITY $35,629.83 TOWN OF KWINANA $35,475.52 PRINTING INDUSTRIES ASSOCIATION $34,090.91 HOUSING INDUSTRY ASSOCIATION $33,986.00 GERALDTON-GREENOUGH REGIONAL COUNCIL $32,844.67 CITY OF FREMANTLE $32,766.43 SHIRE OF MANJIMUP $32,646.00 TOWN OF CAMBRIDGE $32,414.72 WA LOCAL GOVERNMENT -

Repeal Local Law 2019 Published in Government Gazette 31 March

!2020048GG! WESTERN 831 AUSTRALIAN GOVERNMENT ISSN 1448-949X (print) ISSN 2204-4264 (online) PRINT POST APPROVED PP665002/00041 PERTH, TUESDAY, 31 MARCH 2020 No. 48 PUBLISHED BY AUTHORITY KEVIN J. McRAE, GOVERNMENT PRINTER AT 12.00 NOON © STATE OF WESTERN AUSTRALIA CONTENTS PART 1 Page Building Amendment Regulations (No. 2) 2020 ....................................................................... 833 City of Rockingham Repeal Local Law 2019 ............................................................................ 836 Juries Amendment Regulations 2020 ....................................................................................... 834 Liquor Commission Amendment Rules 2020 ........................................................................... 837 Terrorism (Preventative Detention) Amendment Regulations 2020 ....................................... 836 ——— PART 2 Agriculture and Food ................................................................................................................. 839 Environment .............................................................................................................................. 840 Fire and Emergency Services .................................................................................................... 842 Health ......................................................................................................................................... 845 Justice ........................................................................................................................................