Chapter II Performance Audit 11

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Officename a G S.O Bhubaneswar Secretariate S.O Kharavela Nagar S.O Orissa Assembly S.O Bhubaneswar G.P.O. Old Town S.O (Khorda

pincode officename districtname statename 751001 A G S.O Khorda ODISHA 751001 Bhubaneswar Secretariate S.O Khorda ODISHA 751001 Kharavela Nagar S.O Khorda ODISHA 751001 Orissa Assembly S.O Khorda ODISHA 751001 Bhubaneswar G.P.O. Khorda ODISHA 751002 Old Town S.O (Khorda) Khorda ODISHA 751002 Harachandi Sahi S.O Khorda ODISHA 751002 Kedargouri S.O Khorda ODISHA 751002 Santarapur S.O Khorda ODISHA 751002 Bhimatangi ND S.O Khorda ODISHA 751002 Gopinathpur B.O Khorda ODISHA 751002 Itipur B.O Khorda ODISHA 751002 Kalyanpur Sasan B.O Khorda ODISHA 751002 Kausalyaganga B.O Khorda ODISHA 751002 Kuha B.O Khorda ODISHA 751002 Sisupalgarh B.O Khorda ODISHA 751002 Sundarpada B.O Khorda ODISHA 751002 Bankual B.O Khorda ODISHA 751003 Baramunda Colony S.O Khorda ODISHA 751003 Suryanagar S.O (Khorda) Khorda ODISHA 751004 Utkal University S.O Khorda ODISHA 751005 Sainik School S.O (Khorda) Khorda ODISHA 751006 Budheswari Colony S.O Khorda ODISHA 751006 Kalpana Square S.O Khorda ODISHA 751006 Laxmisagar S.O (Khorda) Khorda ODISHA 751006 Jharapada B.O Khorda ODISHA 751006 Station Bazar B.O Khorda ODISHA 751007 Saheed Nagar S.O Khorda ODISHA 751007 Satyanagar S.O (Khorda) Khorda ODISHA 751007 V S S Nagar S.O Khorda ODISHA 751008 Rajbhawan S.O (Khorda) Khorda ODISHA 751009 Bapujee Nagar S.O Khorda ODISHA 751009 Bhubaneswar R S S.O Khorda ODISHA 751009 Ashok Nagar S.O (Khorda) Khorda ODISHA 751009 Udyan Marg S.O Khorda ODISHA 751010 Rasulgarh S.O Khorda ODISHA 751011 C R P Lines S.O Khorda ODISHA 751012 Nayapalli S.O Khorda ODISHA 751013 Regional Research Laboratory -

District Disaster Management Plan 2018

District Disaster Management Plan 2018 2018 District Disaster Management Plan Cuttack, ODISHA Volume- I District Disaster Management Authority (DDMA) Cuttack, Odisha 6/10/2018 District Disaster Management Plan 2018 CONTENT Topic Page No. 1. Introduction 2. District Profile 3. Hazard, Risk and Vulnerability Analysis 4. Institutional Arrangement 5. Prevention and Mitigation 6. Capacity Building 7. Preparedness 8. Response 9. Restoration and Rehabilitation 10. Recovery 11. Financial Arrangement 12. Preparation and Implementation of DDMP 13. Lessons Learnt and Documentation District Disaster Management Plan 2018 ABBREVIATION DDMA- District Disaster Management Authority DDMP- District Disaster Management Plan DEOC- District Emergency Operation Centre HRVA- Hazard Risk and Vulnerability Analysis ADM -Additional District Magistrate AWC - Anganwadi Centre BDO - Block Development officer BCR - Block Control Room CCA - Climate Change Adaptation CDMO - Chief District Medical Officer CDPO - Child Development Project Officer CDVO - Chief District Veterinary Officer CMRF - Chief Ministers Relief Fund DC - District Collector DCR - District Control Room DDMP -District Disaster Management Plan DDM - District Disaster Manager DEOC - District Emergency Operation Centre DRDA - District Rural Development Agency DSWO – District Social Welfare Officer DRR - Disaster Risk Reduction GoI - Government of India District Disaster Management Plan 2018 GP - Gram Panchayat HRVA - Hazard Risk and Vulnerability Assessment IAY - Indira AawasYojana MO - Medical Officer -

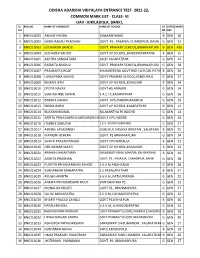

2021-22, Common Mark List

ODISHA ADARSHA VIDYALAYA ENTRANCE TEST- 2021-22, COMMON MARK LIST - CLASS- VI OAV -JOKILADOLA, BANKI, SL ROLLNO NAME OF CANDIDATE NAME OF SCHOOL GE CATEG MARK NO ND ORY ER 1 BNK216001 ABHIJIT PANDA SSM,KANTABAD B GEN 26 2 BNK216002 SARDHANJALI PRADHAN GOVT. PS , PASANIA, CHANDIPUR, BANKI G GEN 21 3 BNK216003 SUDHAKAR GHADEI GOVT. PRIMARY SCHOOL,BRAHMAPURA B GEN ABS 4 BNK216004 SESHADEV SAHOO GOVT UP SCHOOL,BAIDESWARPATNA B GEN 15 5 BNK216005 AMITRA SAMANTARA SACIE KALAPATHAR G GEN 22 6 BNK216006 RASMITA MUDULI GOVT. PRIMARY SCHOOL,BRAHMAPURA G GEN 28 7 BNK216007 PRASHANTA ROUT MAHABERENA GOVT HIGH SCHOOL PATHURIPADAB GEN 30 8 BNK216008 LAXMIPRIYA SAHOO GOVT PRIMARY SCHOOL,KENDUPALI G GEN 27 9 BNK216009 BIGYAN JETHI GOVT UP SCHOOL,KUMUSAR B GEN 24 10 BNK216010 EPSITA NAYAK GOVT HS ANWARI G GEN 14 11 BNK216011 SUBHASHREE SWAIN S.A.C.I.E,KALAPATHAR G GEN 26 12 BNK216012 BARSHA SWAIN GOVT. UPS, PARSHURAMPUR G GEN 29 13 BNK216013 SNEHA BARIK GOVT UP SCHOOL,KALAPATHAR G GEN 12 14 BNK216014 BIJAYANI BISWAL NILAKANTHA PS BAGHEI G GEN 14 15 BNK216015 ARPITA PRIYADARSINI SARDARSINGH GOVT UPS, NATERI G GEN 24 16 BNK216016 ITSHREE SUBUDHI S.S.V. M PATHURIPADA G GEN 21 17 BNK216017 ABINAS JAYASIINGH GURUKUL SIKSHYA NIKETAN , SALATARA B GEN 25 18 BNK216018 MAMUNI BEHERA GOVT. PS BRAHMAPURA G GEN 24 19 BNK216019 SHAKTI PRASAD PANDA GOVT UPS KIAPALLA B GEN 21 20 BNK216020 DEB KUMAR MAJHI GOVT UP SCHOOL,KUMUSUR B GEN 22 21 BNK216021 ABINASH SAMANTARAY SARASWATI SISHU MANDIR, KALAPATHAR B GEN 40 22 BNK216022 AMRITA PRADHAN GOVT. -

Cuttack District

NAME OF THE DISTRICT- CUTTACK PENDING LIST OF NBWs NBW STATUS AS ON-28.02.2019 Sl. NAME OF THE PS NBW Ref. Name of the Fathers name Address of the warrantee Case Ref. No. warrantee 1 2 3 4 5 6 7 1 GOVINDPUR P.S GR NO-534/2004 of Niranjan Das S/O-Lingaraj Das Vill-Govindpur U/S -304(A)/34 IPC SDJM Kamakhya PS- Govindpur Nagar Dist - Cuttack 2 GOVINDPUR P.S GR NO-1049/2013 of Sanjukta Das W/O- Banambar Das Vill-Govindpur Witness JMFC Ctc PS- Govindpur Dist - Cuttack 3 GOVINDPUR P.S GR NO-1017/2013 of Kailash Ch Sahoo S/O- Lt Birabar Vill-Balipada U/S- 47(a) B & O Excise JMFC R Ctc Sahoo PS- Govindpur Act Dist - Cuttack 4 GOVINDPUR P.S GR NO- 143/2015 of Ashoka Behera S/O-Surendra Behera Vill-Tirthapada U/S-498(A)/302/304- JMFC ( R ) Ctc PS- Govindpur B/406/34 IPC Dist - Cuttack 5 GOVINDPUR P.S GR NO- 439/2010 of Kanchu Chara Das S/O- Lt Dijabara Das Vill-Govindpur U/S-448/354/323/ JMFC ( R ) Ctc PS- Govindpur 294 IPC Dist - Cuttack 6 GOVINDPUR P.S GR NO-956/1990 Duryadhana S/O-Kanduri Behera Vill-Sirasundarpur U/S-448/294/506/ JMFC Ctc Behera PS- Govindpur 34 IPC Dist - Cuttack 7 GOVINDPUR P.S GR NO-542/2006 of Sanjukta Bhoi W/O- Rabindra Bhoi Vill-Mankha U/S-354/420 IPC JMFC Ctc PS- Govindpur Dist - Cuttack 8 GOVINDPUR P.S GR NO- Bijaya Ku Das S/O- Adikanda Das Vill-Nahalpur U/S-447/448/426/ 1629 A/1994 of PS- Govindpur 336/149 IPC SDJM S Ctc Dist - Cuttack 9 GOVINDPUR P.S GR NO- Bijaya Ku Das S/O- Adikanda Das Vill-Nahalpur U/S-394/435/436 IPC 1630 A /1994 of PS- Govindpur SDJM S Ctc Dist - Cuttack 10 GOVINDPUR P.S GR NO-1449/2005 of -

GENERAL ELECTION to Pris - 2017 DIST.- CUTTACK SL

GENERAL ELECTION TO PRIs - 2017 DIST.- CUTTACK SL. Name of the Grama Name of the elected Block Name NO. Panchayats Sarpanch 1 Tigiria Achalkot Gourahari Pradhan 2 Gadadharpur Sarat Kumar Swain 3 Jemadeipur Saida Begum 4 Nizigarh Bhabani Prasad Pattnaik 5 Nuapatna Sabita Kundu 6 Panchagaon Nirupama Dash 7 Puruna Tigiria Ranjana Sahoo 8 Badanauput Sashmita Rout 9 Baliput Puspalata Jena 10 Bindhanima Ajit Rout 11 Bhiruda Premranjan Mahamansingh 12 Bhogoda Sarmila Nayak 13 Sompada Rebati Behera 14 Hatamal Prasanna Bhoi 15 Badamba Abhimanpur Ramesh Dehury 16 Badabarsingh Nayana Sahoo 17 Badakambilo Droupadi Naik 18 Badambagarh Sudhanshu Kishore Mohanty 19 Banamalipur Ushamani Sahoo 20 Bangerisingha Archhana Naik 21 Beliapal Bichitrananda Panda 22 Bhattarika Basanti Behera 23 Dasarathipur Ritarani Arukh 24 Diniary Manaswini Behera 25 Gadapokhari Pravakar Mallick 26 Gopalpur Batakrushna Attabudhhi 27 Gopamathura Pravati Nayak 28 Gopapur Narasingh Sahoo 29 Gopinathpur Minati Sahoo 30 Janisahi Khetrabasi Biswal 31 Jhajia Sujata Pani 32 Jodumu Bidulata Jethi 33 Krushnachandrapur Anita Barada 34 Kankadajodi Rabindra Kumar Sahoo 35 Karadibandha Ananda Chandra Rout 36 Kasikiary Jayanti Sethi 37 Khuntakata Sridhar Behera 38 Koleswar Amiya Kumar Panigrahi 39 Kuanarpal Sasmita Pallei 40 Mahulia Laxmipriya Sethi 41 Malati Priyambada Mohanty 42 Manapur Sailabala Dalei 43 Mangarajpur Umakanta Swain 44 Maniabandha Prasanta Debata 45 Mugagahira Kartik Choudhury 46 Parajapada Chintamani Samal 47 Ragadipada Santosh Kumar Maharana 48 Ratapat Durgapriya Dalabehera -

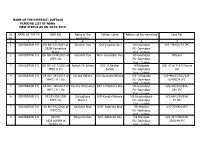

Advancetour Programme of Mvu Tangi Choudwar Block

ADVANCETOUR PROGRAMME OF MVU TANGI CHOUDWAR BLOCK FROM JANUARY-MARCH-2020 NAME OF THE SCHEME : Mobile Veterinary Unit NAME OF THE DISTRICT :cuttack NAME OF THE BLOCK :Tangi choudwar NAME OF THE BVO & CONTACT NO : Dr Antaryami Khuntia, 9437202313 NAME OF THE BVO & CONTACT NO. OF MVU STAFF : VETERINARY OFFICER-VACANT LIVESTOCK ASSISTANT-GORACHAND SETHI ATTENDANT-VACANT MVU VEHICLE REGISTRATION NO.: OD05AP8022 NAME & CONTACT ADDRESS OF VEHICLE OWNER : Kabita Rout, 9853045075 NAME & CONTACT NO OF AVAS- VACANT ADVANCE TOUR PROGRAMME OF MVU OF TANGI-CHOUDWAR BLOCK FOR THE MONTH OF JANUARY-2020 Sl no Date GP Village Distance 1 02/1/20 Uchhapada Nischinta,Damaka,Hosinabad 50 2 03/1/20 choudwar Paikaraipur,Mandapada,Daulatabad 60 3 06/1/20 Mangarajpur, Amblijari, Ramachandrapur 60 4 07/1/20 Sankarpur Bantua,Shankarpur 50 5 08/1/20 Slagaon Madhapur,Kharipadia,Bamboori 40 6 09/1/20 Slagaon Chatabar,Guali,Guali 60 7 10/1/20 Gobindpur Karuala,Rudrapur 50 8 13/1/20 Badasamantrapur Badasamantpur,Badapadagaon 60 9 14/1/20 Safa Abhaypur,Haridaphal,Karanji 50 10 15/1/20 Kahneipur Barpada,Anjua 40 11 16/1/20 Kayalpada Kayalpda,Nuapatna,Similihand 50 12 17/1/20 Mangarajpur Kochilanuagaon,Berena 70 13 20/1/20 Indranipatna Banipada,Goukhana,Devinagar 50 14 21/1/20 Safa Haripur,Kusunpur 50 15 22/1/20 Gobindpur Magura Dhanmandal,Gobindpur 50 16 24/1/20 Napanga,Harianta Itua,Tantira,Tiranpada 50 17 27/1/20 Safa,Sankarpur Machhapangi,Dudhianali,Kankali 50 18 28/1/20 D.B Pur Kanjia,Kamanga 40 19 29/1/20 Garudgaon Kanpur,Chandanpur 40 20 31/1/20 Gobindpur Adambaru,Badadebili -

![8`Ge F Gvz]D C'= Tc ^` Vezdrez` A]R](https://docslib.b-cdn.net/cover/7130/8-ge-f-gvz-d-c-tc-vezdrez-a-r-2377130.webp)

8`Ge F Gvz]D C'= Tc ^` Vezdrez` A]R

/ 0 !"#$ %&'! !"#$" !"#$% &' 1+''1 41 56 $+1 !23 -%#/! 5 1 / 2 (0 7/ ( ( 1 5 81 4 / 5 / ( ( 56 2 3 4 2 &(& )*+ , -'& $$ ( )(*) +)) ,', ,-,' Q estimated value corresponds to 14 per cent of the proposed outlay for Centre under the National Infrastructure Pipeline (43 lakh crore). s India is engaged in a big New Delhi: Amid deepening The end objective of this Arescue operation to bring crisis in Afghanistan after the initiative is to enable “infra- out its citizens from strife- Taliban took over the war- structure creation through torn Afghanistan, External torn nation, a large number of monetisation” wherein the Affairs Minister S Jaishankar Afghan refugees in India vocif- public and private sector col- will brief Parliamentary lead- erously protested in front of the laborate, each excelling in their ers of various political parties UNHCR office here on core areas of competence, so as on August 26 about the situ- Monday demanding release of to deliver socio-economic ation there. “support letters” from the UN inance Minister Nirmala growth and quality of life to the This forthcoming all- agency to migrate to other FSitharaman on Monday country’s citizens, she added. party interaction comes at $$ $# countries for better opportu- announced an ambitious 6 In the railways sector, as the direction of Prime *" + #( $ % nities. lakh crore National many as 400 railway stations, Minister Narendra Modi, Monetisation Pipeline (NMP) 90 passenger trains, 741-km Parliamentary Affairs Minister of Parliamentary Sources said first ever brief- aimed at unlocking value in Konkan Railways and 15 rail- Minister Pralhad Joshi said Affairs @JoshiPralhad will be ing of this sort is expected to infrastructure assets across way stadiums and colonies are here on Monday. -

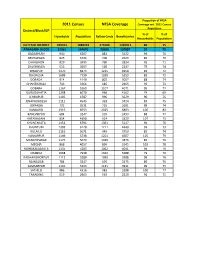

Proportion of NFSA Coverage Wrt. 2011 Census

Proportion of NFSA 2011 Census NFSA Coverage Coverage wrt. 2011 Census Population District/Block/GP % of % of Houeholds Population Ration Cards Beneficiaries Households Population CUTTACK DISTRICT 429454 1888423 371006 1420911 86 75 ATHAGARH BLOCK 31361 144670 28698 107857 92 75 BADABHUIN 940 4267 881 3222 94 76 BENTAPADA 825 3734 700 2623 85 70 CHHAGAON 829 3995 760 2824 92 71 DALABHAGA 656 3037 520 2237 79 74 DHAIPUR 1470 6873 1225 4958 83 72 DHURUSIA 1609 7730 1339 5553 83 72 DORADA 914 4149 802 3057 88 74 GHANTIKHALA 743 3364 685 2465 92 73 GOBARA 1167 5269 1107 4071 95 77 GURUDIJHATIA 1298 6070 966 4162 74 69 ICHHAPUR 1105 4787 996 3629 90 76 JENAPADADESH 1112 4545 928 3424 83 75 JORANDA 732 3531 725 2601 99 74 KANDAREI 1915 8553 2025 6803 106 80 KANDARPUR 684 3247 599 2493 88 77 KATAKIASAHI 854 4398 914 3320 107 75 KHUNTAKATA 1452 6794 1361 5147 94 76 KHUNTUNI 1303 6120 1211 4440 93 73 KULAILO 1116 5071 949 3750 85 74 KUMARPUR 1149 5738 1201 4507 105 79 MANCHESWAR 1175 5079 1049 3876 89 76 MEGHA 868 4057 896 3145 103 78 MOHAKALABASTA 1135 5283 1062 4041 94 76 ORANDA 1668 7930 1322 5588 79 70 RADHAKISHORPUR 1112 5280 1099 3998 99 76 RAJNAGAR 784 3247 699 2475 89 76 SAMSARPUR 1141 5243 1131 3911 99 75 SATHILO 986 4316 983 3308 100 77 TARADING 619 2963 563 2229 91 75 Proportion of NFSA 2011 Census NFSA Coverage Coverage wrt. 2011 Census Population District/Block/GP % of % of Houeholds Population Ration Cards Beneficiaries Households Population BADAMBA 35635 149797 33551 120705 94 81 ABHIMANPUR 1241 5541 1097 4155 88 75 BADABARSING -

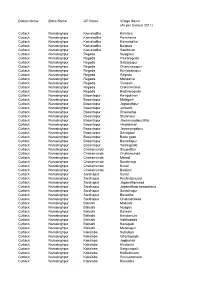

District Name Block Name GP Name Village Name (As Per Census 2011)

District Name Block Name GP Name Village Name (As per Census 2011) Cuttack Narasinghpur Kamaladiha Kaintara Cuttack Narasinghpur Kamaladiha Panchama Cuttack Narasinghpur Kamaladiha Kamaladiha Cuttack Narasinghpur Kamaladiha Baliputa Cuttack Narasinghpur Kamaladiha Ranibhuin Cuttack Narasinghpur Regeda Nuagaon Cuttack Narasinghpur Regeda Paikaregeda Cuttack Narasinghpur Regeda Satyajaypur Cuttack Narasinghpur Regeda Dhanurjayapur Cuttack Narasinghpur Regeda Kunjabanapur Cuttack Narasinghpur Regeda Regeda Cuttack Narasinghpur Regeda Mandania Cuttack Narasinghpur Regeda Talasahi Cuttack Narasinghpur Regeda Chikankhandi Cuttack Narasinghpur Regeda Badhiaregeda Cuttack Narasinghpur Basantapur Kainpokhari Cuttack Narasinghpur Basantapur Mahigarh Cuttack Narasinghpur Basantapur Jaganathpur Cuttack Narasinghpur Basantapur Janisahi Cuttack Narasinghpur Basantapur Dhanadhip Cuttack Narasinghpur Basantapur Shyampur Cuttack Narasinghpur Basantapur Jayamangalpur(Ka) Cuttack Narasinghpur Basantapur Hinjalakhal Cuttack Narasinghpur Basantapur Jayamangalpur Cuttack Narasinghpur Basantapur Sanagaon Cuttack Narasinghpur Basantapur Bada gaon Cuttack Narasinghpur Basantapur Basantapur Cuttack Narasinghpur Basantapur Tolakapatia Cuttack Narasinghpur Chakamunda Sisupathar Cuttack Narasinghpur Chakamunda Chakamunda Cuttack Narasinghpur Chakamunda Marudi Cuttack Narasinghpur Chakamunda Barabhaya Cuttack Narasinghpur Chakamunda Kusal Cuttack Narasinghpur Chakamunda Balikiari Cuttack Narasinghpur Sardhapur Sukat Cuttack Narasinghpur Sardhapur Krishnaprasad Cuttack -

Puri District, Odisha

कᴂ द्रीय भूमि जल बो셍ड जल संसाधन, नदी विकास और गंगा संरक्षण विभाग, जल शक्ति मंत्रालय भारि सरकार Central Ground Water Board Department of Water Resources, River Development and Ganga Rejuvenation, Ministry of Jal Shakti Government of India AQUIFER MAPPING AND MANAGEMENT OF GROUND WATER RESOURCES PURI DISTRICT, ODISHA दक्षक्षण पूिी क्षेत्र, भुिने�िर South Eastern Region, Bhubaneswar Government of India Ministry of Jal Shakti DEPARTMENT OF WATER RESOURCES, RIVER DEVELOPMENT & GANGA REJUVENATION AQUIFER MAPPING AND MANAGEMENT PLAN OF PURI DISTRICT ODISHA BY CHIRASHREE MOHANTY (SCIENTIST-C) CENTRAL GROUND WATER BOARD South Eastern Region, Bhubaneswar July – 2018 HYDROGEOLOGICAL FRAMEWORK, GROUND WATER DEVELOPMENT PROSPECTS & AQUIFER MANAGEMENT PLAN IN PARTS OF PURI DISTRICT, ODISHA CONTRIBUTORS PAGE Data Acquisition : Sh. D. Biswas, Scientist-‘D’ Sh Gulab Prasad, Scientist-‘D’ Smt. C. Mohanty, Scientist-‘C’ Shri D. N.Mandal, Scientist-‘D’ Shri S.Sahu- Scientist-‘C’ Data Processing : Smt. C. Mohanty, Scientist-‘C’ Shri D. Biswas, Scientist-‘D’ Dr. N. C. Nayak, Scientist-‘D’ Data Compilation & Editing: Smt. C. Mohanty, Scientist-‘C’ Dr. N. C. Nayak, Scientist-‘D’ Data Interpretation : Smt. C. Mohanty, Scientist-‘C’ Dr. N. C. Nayak, Scientist-‘D’ GIS : Smt. C. Mohanty, Scientist-‘C’ Dr. N. C. Nayak, Scientist-‘D’ Shri P. K. Mohapatra, Scientist-‘D’ Report Compilation : Smt. C. Mohanty, Scientist-‘C’ Technical Guidance : Shri P. K. Mohapatra, Scientist-‘D’ Shri S. C. Behera, Scientist-‘D’ Dr. N. C. Nayak, Scientist-‘D’ Overall Supervision : Dr Utpal Gogoi, Regional Director Shri D. P. Pati, ex-Regional Director Dr. N. C. -

UNITED BANK of INDIA Head Office 11, Hemanta Basu Sarani Kolkata – 700 001

id721812 pdfMachine by Broadgun Software - a great PDF writer! - a great PDF creator! - http://www.pdfmachine.com http://www.broadgun.com UNITED BANK OF INDIA Head Office 11, Hemanta Basu Sarani Kolkata – 700 001 Request for Proposal Data Archival and Retrieval Suite (DAR) Tender : 07/2009 Release Date : 11/05/2009 Version : Final Submission Details- Particulars Deadline th Last date of requesting any clarifications 16 May, 2009, 1300 hrs th Date of Pre Bid Conference 18 May, 2009, 1430 hrs th Last date of submission of the Technical 11 June, 2009, 1400 hrs and Commercial bid th Date of opening of the Technical Bid 11 June, 2009, 1430 hrs Date of opening of the Commercial Bid Will be intimated separately to technically qualified bidders. RFP for Data Archival and Retrieval Project Tender 07/2009 Table of Contents 1. Bank Introduction and Purpose: ________________________________________________ 5 2. Project Details ______________________________________________________________ 7 2.1 Project Overview ________________________________________________________ 7 2.2 Project Scope ___________________________________________________________ 8 2.3 Project Timelines _______________________________________________________ 11 2.4 Proposed DAR Project plan up to UAT and Pilot Implementation. _________________ 12 3. Terms & Conditions _________________________________________________________ 13 3.1 Terms & Conditions _____________________________________________________ 13 3.1.1 General ____________________________________________________________ 13 -

The Odisha G a Z E T T E

The Odisha G a z e t t e EXTRAORDINARY PUBLISHED BY AUTHORITY No. 766 CUTTACK, TUESDAY, MAY 6, 2014/BAISAKHA 16, 1936 REVENUE & DISASTER MANAGEMENT DEPARTMENT NOTIFICATION The 23rd April 2014 S.R.O. No. 183/2014—In supersession of the Notification No. 12242—S-13/2013-R & DM., dated the 6th April 2013 and in exercise of powers conferred under sub-section (1) of Section 3 of the Odisha Special Survey and Settlement Act, 2012, read with sub-rule (1) of Rule 4 of Odisha Special Survey and Settlement Rules, 2012 (Odisha Act 5 of 2012), the State Government do hereby notify 1890 number of villages of Cuttack District as at Schedule-A for taking up further proceedings relating to survey and preparation of record of rights simultaneously with respect to all lands lying in the areas comprised within the limits of villages as per the schedule annexed herewith. The settlement of rent with respect to above said areas shall be dertermined as per the prevailing guidelines issued by Revenue & Disaster Management Department. [ No. 11772—NLRMP-06/2014-R & DM. ] By order of the Governor S. SUKLA Joint Secretary to Government DISTRICT : CUTTACK, (RURAL) Name of the Name of the Name of the Village Name of the Sl. No. Name of the Tahasil PS No. District Sub-Division Odiya English PS 1 CUTTACK ATHAGARH ATHAGARH ‚¨¥Þ ISARA ‹”‹ ª›¥ 50 2 CUTTACK ATHAGARH ATHAGARH „›¤ýÇÚ¥›¦ UDAYAPURDALA ‹”‹ ª›¥ 63 3 CUTTACK ATHAGARH ATHAGARH „›¤ýÇڥᛨ UDAYAPURDESA ‹”‹ ª›¥ 64 4 CUTTACK ATHAGARH ATHAGARH ‹Äꪥ KANSARA ¡ß–ÍÞåÞªß 2 5 CUTTACK ATHAGARH ATHAGARH ‹˜Ø᥂ KANDERAI ¡ß–ÍÞåÞªß