Impact 2008-2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CHRISTOWN SPECTRUM MALL Bethany Home Rd & 19Th Ave - Southeast Corner Phoenix, Arizona

CHRISTOWN SPECTRUM MALL Bethany Home Rd & 19th Ave - Southeast Corner Phoenix, Arizona PROPERTY HIGHLIGHTS SITE PLAN / AVAILABILITY AERIAL CONTACT DEMOGRAPHICS Brian Gast Brian Harpel Brad Ranly A 602.682.8155 602.682.8150 602.682.8120 [email protected] [email protected] [email protected] Project CHRISTOWN SPECTRUM MALL Bethany Home Rd & 19th Ave - Southeast Corner Phoenix, Arizona ANCHOR SPACE & SHOPS AVAILABLE Property Highlights Traffic Counts Bethany Home Rd 35,980 CPD • Dominant Central Phoenix Shopping Center 19th Ave 21,350 CPD Total 57,330 CPD • Total GLA: 844,955 SF on 71.73 Acres Demographics 1 mi 3 mi 5 mi Estimated Population 24,764 214,436 494,474 • Over 57,000 Cars per Day drive by the site Med Household Income $48,058 $52,725 $53,409 Estimated Households 9,964 83,088 190,534 • Shops Space Available Daytime Population 6,907 68,846 242,995 Source: SitesUSA • Rental Rate: Call to Discuss Nearby Tenants PROPERTY HIGHLIGHTS SITE PLAN / AVAILABILITY AERIAL CONTACT DEMOGRAPHICS Brian Gast Brian Harpel Brad Ranly A 602.682.8155 602.682.8150 602.682.8120 [email protected] [email protected] [email protected] Project CHRISTOWN SPECTRUM MALL Bethany Home Rd & 19th Ave - Southeast Corner Phoenix, Arizona K5 Available 55,332 33 Harkins Theatres 62,322 K58 Olive Garden 7,700 34 Costco 154,809 1 Ulta 8,992 35 Bath & Body Works 2,532 2 Carter’s 4,020 36 Modluxx 1,230 3 America’s Best 3,500 37 GameStop 1,140 4 Bright Now! Dental 3,337 38 GNC 1,040 5 Dollar Tree 10,740 -

Orangewood Apartments

Orangewood Apartments 2020 WEST ORANGEWOOD AVENUE // PHOENIX, AZ OFFERING SUMMARY PROPERTY NAME Orangewood Apartments ADDRESS 2020 West Orangewood Avenue CITY, STATE Phoenix, Arizona 85021 PARCEL NUMBER 157–19–141 ZONING R–4, Phoenix Orangewood TOTAL UNITS 27 YEAR BUILT 1986 Apartments TOTAL SQUARE FEET 13,758 PARCEL SIZE 0.94 AC DENSITY 27.72 Units per Acre Orangewood Apartments Marcus & Millichap is pleased to announce the opportunity to acquire PRICE $2,400,000 Orangewood Apartments, a 27–unit multifamily community located in Phoenix, Arizona. Situated a block west of 19th Avenue and a half mile south UNITS 27 of Northern Avenue in the Christown submarket, where multifamily renovation and development is burgeoning. Anchoring the neighborhood is PRICE PER UNIT $88,889 the 1 million square foot Christown Spectrum Mall with its 50+ stores including Costco, Walmart, Target and many others. Within walking distance TOTAL SQUARE FEET 13,758 is Albertsons as well as Fry’s grocers. PRICE PER SQUARE FOOT $174.44 Listed at $2,400,000 Orangewood offers an investor the ability to pay a below–market price in an up–and–coming submarket. Built in 1986, the unit mix is comprised of (24) studios, (2) one bedroom–one bath units and (1) Phoenix metro will experience faster job growth than the two bedroom–one bath townhome style unit. The tenants enjoy large mature national rate during the next five years. shade trees, grass–covered open spaces as well as a gated pool and lounge area. Deliveries pick up in 2019 as Phoenix receives 10,600 new Within walking distance to the property is the Northern/19th Avenue Phoenix units. -

Christown Spectrum Pud 1

CHRISTOWN SPECTRUM PUD 1 PRINCIPALS AND DEVELOPMENT TEAM Property Owner: Christown 1755, LLC A Delaware Limited Liability Company Managed by Kimco Realty Corporation. Developer: Kimco Realty Corporation 2429 Park Avenue Tustin, CA 92782-2705 Contact: Mark Wendel Director of Development | Western Region Phone: (949) 252-3870 E-mail: [email protected] Architect: Streetsense / TBD 3 Bethesda Metro, #140 Bethesda, MD 20814 Contacts: Stephen Miller, Project Designer John Huntzinger, Senior Director of Planning Phone: (240) 479-7201 E-mail: [email protected] E-mail: [email protected] Attorney: Earl & Curley, PC 3101 North Central Avenue, Suite #1000 Phoenix, AZ 85012 Attorney: Taylor Earl Principal Planner: Ricardo Toris Phone: (602) 265-0094 E-mail: [email protected] E-mail: [email protected] Civil Engineering and Landscape Architecture: Kimley-Horn and Associates, Inc 1001 West Southern Ave, Suite 131 Mesa, AZ 85210 Contact: Heather Roberts, PE Phone: (623) 552-3171 Contact: Chuck Wright, PE Phone: (602) 944-5500 Contact: Anne DeBoard, PLA Phone: (602) 906-1106 E-mail: [email protected] E-mail: [email protected] E-mail: [email protected] 2 PLANNED UNIT DEVELOPMENT DISCLAIMER Regulatory Provisions This PUD has been prepared pursuant to Section 671 of the Zoning Ordinance of City of Phoenix, Arizona (Planned Unit Development) to establish the regulatory framework for the Christown Spectrum PUD development by utilizing the City of Phoenix Zoning Ordinance Chapter 13, Walkable Urban Code (“WU”), Transect District: T5:5 development standards to fit future development(s) within the context of the area. This PUD is a stand-alone document comprised of project specific zoning regulations, including permitted uses, conditions/limitations, development standards, building heights, landscaping, outdoor storage, parking (e.g., bicycle and automobile) standards, and signage. -

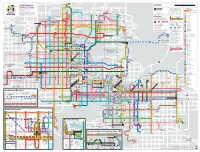

SYSTEM MAP Scale Is Approximate

Happy Valley Rd Happy Valley 0 1 2 3 4 5 R I- LEGEND Miles SYSTEM MAP Scale is approximate. MAPA DEL SISTEMA Pinnacle Peak Rd 17 Transit Center Valley Metro Rail Local Buses Light Rail, Local, Express Phoenix-Deer Valley Municipal Airport Frequent and reliable all-day rail Main bus route 29th Ave Park-and-Ride Regular service Deer Valley Dr E Marriott Dr and RAPID Bus Routes 19th Ave 27th Ave 27th Ave 23rd service operating 365 days a year Select trips only Barry Point of Interest linking Phoenix, Tempe and Mesa Limited service Deer Valley Rd Eective/Validez 10.28.2019 Goldwater Direction of Travel with connections to Sky Harbor High School R SR Central Avenue Honeywell Airport and many bus routes. Rose Garden Ln Rose Garden Ln Desert Ridge Marketplace St 73rd 602.253.5000 | valleymetro.org Pima Fwy Scottsdale Healthcare Dr Washington Agua Fria Fwy 7th Ave 101 Rail line is on 101 E Mayo Blvd Thompson Peak Pkwy this street Train stops only at Van Buren HonorHealth Scottsdale Beardsley Rd Beardsley Rd 51 RAPID Bus light rail stations Glendale Thompson Peak 7th Street Foothills Library Fast and frequent bus service from Apache Blvd Behrend Dr Yorkshire Dr park-and-rides to downtown Phoenix 7th Avenue Utopia Rd Blvd Tatum Abrazo Arrowhead Hospital E on weekdays 5–8 a.m. and 3–6 p.m. Union Hills Dr Rd Creek Cave Light rail line Roosevelt Union Hills Dr E 56th St Mayo Clinic See light rail map on reverse for details. Phoenix Campus E Foothills Paradise Valley 101 R I-E 12th Street Aquatics Center Ave 27th 17 Community College RAPID stops only at these RAPID route(s) Buckeye Road 59th Ave 59th Arrowhead Ave 57th points and at transit centers. -

Employee Shop Phoenix 2012.Indd

Shop Phoenix! Regional Malls/Power Centers & Retail Warehouses Regional Malls Metrocenter Mall 9617 N. Metro Parkway West Outlets At Anthem 4250 W. Anthem Way Desert Ridge Marketplace 21001 N. Tatum Boulevard Scottsdale 101 7000 E. Mayo Boulevard CityNorth 20250 N. 56th Street Kierland Commons 15054 N. Scottsdale Road Paradise Valley Mall 4568 E. Cactus Road Christown Spectrum Mall 1703 W. Bethany Home Road Biltmore Fashion Park 2470 E. Camelback Road Desert Sky Mall 7611 W. Thomas Road Power Centers Happy Valley Towne Center 2501 W. Happy Valley Road Bell Towne Centre 16806 N. Seventh Street Desert Sky Palms Center 7502 W. Thomas Road Ahwatukee Foothills Towne Center 4710 E. Ray Road Camelback Colonnade 1919 E. Camelback Road Tuscano Towne Center 7575 W. Lower Buckeye Road Arcadia Crossing 4535 E. Thomas Road Desert Palms Power Center 3883 E. Thomas Road The Shops at Norterra 2460 W. Happy Valley Road Retail Warehouse Sam’s Club Sam’s Club Center 1525 W. Bell Road Sam’s Club Center 8340 W. McDowell Road Costco Costco Plaza 3801 N. 33rd Avenue Christown/Spectrum 1646 W. Montebello Arcadia Crossing 4502 E. Oak Street Paradise Valley Mall 4570 E. Cactus Road Costco Center 19001 N. 27th Avenue Cave Creek Market Place 2450 E. Beardsley Best Buy Ahwatukee Foothills Towne Center 5051 E. Ray Road Metro North 2727 W. Thunderbird Road Village Fair 12645 N. 48th Street Camelback Colonnade 1949 E. Camelback Road Fry’s Electronics Fry’s Electronics 3035 W. Thunderbird Road Shop Phoenix! Auto Dealerships Home Repair & Appliance Distributors East Camelback Road Lowe’s ABC Nissan, Inc. -

Contact Information Retail Locations Fares

AUGUST 2013 RETAIL LOCATIONS CONTACT INFORMATION BUS / LIGHT RAIL There are nearly 800 retail locations where you can Customer Service: 602.253.5000 purchase your pass before boarding. Purchase TTY: 602.251.2039 (for the hearing impaired) passes at most valley-wide locations of the following stores: Customers can obtain information about various transit services by using our automated phone • 7-Eleven system 24 hours a day, 365 days a year. Hablamos • Circle K español. • Corner Store (formerly Valero) RIDE • Food City (select locations only) Customer Service Business Hours • Fry's Food Store • Weekdays, 6 am - 8 pm • PLS Check Cashers • Saturdays, 7 am - 7 pm • Safeway GUIDE • Sundays and designated holidays, 8 am - 5 pm • Walgreens • Closed New Year’s Day, Memorial Day, Passes can also be purchased at participating: Independence Day, Labor Day, Thanksgiving Day and Christmas Day • APS locations • Public libraries Lost and Found Information: 602.253.5000. • Transit centers Use the automated system for help. When prompted, say “Lost and Found” and provide the route number. Not all pass types are sold at every location. Follow provided instructions. Please contact the location prior to traveling to check availability of passes and types of payment Transit Watch. Help improve transit safety and accepted. security by reporting any and all suspicious activities to Valley Metro Customer Service. In case of For a complete list of retail locations, visit emergencies, call 911. valleymetro.org or call 602.253.5000. Local bus/light rail/ LINK Reduced** Express/ RAPID FARES 1-Ride* $2.00 $1.00 $3.25 Local bus, light rail and LINK share the same fare structure and pass All-Day $4.00 $2.00 $6.50 types. -

Valley Metro System Map April 2017

35 Happy Valley Rd Happy Valley 0 1 2 3 4 5 I-17 LEGEND Miles SYSTEM MAP Scale is approximate. Pinnacle Peak Rd 17 MAPA DEL SISTEMA 19 Transit Center Valley Metro Rail Local Buses Light Rail, Local, Express Phoenix-Deer Valley Municipal Airport Frequent and reliable all-day rail 29th Ave Main bus route Deer Valley Dr Park-and-Ride E Marriott Dr 136 and RAPID Bus Routes 19th Ave 27th Ave 27th Ave 23rd service operating 365 days a year 44 Select trips only Barry 7 Point of Interest linking Phoenix, Tempe and Mesa 27 Deer Valley Rd Eective/Validez 04.24.2017 Goldwater Direction of Travel with connections to Sky Harbor High School SR 51 0 Central Avenue Honeywell Airport and many bus routes. Rose Garden Ln 27 Rose Garden Ln 90 Desert Ridge Marketplace 72 St 73rd 602.253.5000 | valleymetro.org Pima Fwy Scottsdale Healthcare Dr 1 Washington Agua Fria Fwy 7th Ave 101 Rail line is on 101 575 Mayo Blvd Thompson Peak Pkwy this street Train stops only at 3 Van Buren HonorHealth Scottsdale Beardsley Rd Beardsley Rd 51 RAPID Bus light rail stations 575 Thompson Peak 7 7th Street Utopia Rd Fast and frequent bus service from Apache Blvd Behrend Dr Yorkshire Dr Glendale Foothills Library park-and-rides to downtown Phoenix 8 7th Avenue Utopia Rd Blvd Tatum 575 on weekdays 5–8 a.m. and 3–6 p.m. Union Hills Dr Rd Creek Cave Light rail line 10 Roosevelt Union Hills Dr 43 186 16 39 186 56th St Mayo Clinic See light rail map on reverse for details. -

Welcome to the Desert

Phoenix UpTowne Casa Phoenix Welcome to the Desert Thank you for taking time in life to schedule some FUN! Whether you are here just for relaxation, business, or school we hope you and your guests have a great time. Our goal is to exceed your expectations while staying at Phoenix UpTowne Casa and your time in Phoenix. Please bring this welcome packet with you to ensure a smooth arrival and check in. Property Address: 5310 N 15th Dr Phoenix, AZ 85015 Parking Instructions: Parking available by front door in the 2 carport spaces or across from the pool. Please DO NOT park in the roadway as you could be towed. Check-in Time: 4:00 p.m. Front Door code-last 4 digits of your cell phone as was on your application Internet – WiFi Password—4454e2a9 Pool Key in hall storage closet Local Contact Dave 480 232 5477 Pat / Ed 703 928 5833 307-363-0504 [email protected] House Rules No Smoking No Parties or Overnight guests not listed in reservation packet Departure: Please leave the pool key on the Dining Room table on your departure day by 11 AM Sleeping: There is a king bed in the rear bedroom, 2 twins in the front bedroom as well as a pullout double sleeper sofa in the living room and a plush rollaway twin stored in the master bedroom closet-sleeps 6. Extra linens and towels are in the hall entry closet. What’s Up In Phoenix? https://www.azcentral.com/things-to-do/events/ http://www.phoenixnewtimes.com/calendar What’s Up In Scottsdale? https://www.eventbrite.com/things-to-do/az--scottsdale/this-weekend/ https://www.tripadvisor.com/Attractions-g31350-Activities-Scottsdale_Arizona.html- -

The Edge on Seventeen

THE EDGE ON SEVENTEEN 2501 W. OCOTILLO ROAD | PHOENIX, AZ | 85017 52-UNIT MULTIFAMILY INVESTMENT OPPORTUNITY OFFER SOLICITATION PROCESS PROPERTY VISITATION Prospective purchasers will have the opportunity to visit the property via pre-scheduled property tours. These tours will include access to a representative sampling of units and access to maintenance and other similar facilities. In order to accommodate the property’s ongoing operations, property visitation will require advance notice and scheduling. OFFER SUBMISSION Offers should be presented in the form of a non-binding Letter of Intent, spelling out the significant terms and conditions of Purchasers’ offers including, but not limited to (1) asset pricing, (2) due diligence and closing time frame, (3) earnest money deposit, and (4) qualifications to close. The purchase terms shall require all cash to be paid at closing. Offers should be delivered to the attention of Ryan Ash and Mike Woodrick using the email or fax number information listed below. CONTACT INFORMATION Ryan Ash Senior Managing Director Tel: 602-852-3784 [email protected] Mike Woodrick Director Tel: 602-852-3789 [email protected] ARA - Phoenix 2398 E. Camelback Road Suite 950 Phoenix, Arizona 85016 Tel: 602-252-4232 Fax: 602-252-4236 www.ARAnewmark.com 2 TABLE OF CONTENTS 03 EXECUTIVE SUMMARY 07 PROPERTY OVERVIEW 12 VALUATION SUMMARY 16 COMPARABLE SALES 22 AREA OVERVIEW 33 CONTACT EXECUTIVE SUMMARY DOWNTOWN PHOENIX CAMELBACK CORRIDOR CENTRAL CORRIDOR THE EDGE ON SEVENTEEN 4 THE OPPORTUNITY INVESTMENT HIGHLIGHTS The Edge on Seventeen is a 54-unit apartment community located in Phoenix, AZ. The property has great visibility and frontage just west of the Interstate-17 which provides residents convenient • Majority 2 Bedroom Units access to Downtown Phoenix just 10 minutes to the south. -

2017 Graduation Information

2017 GRADUATION INFORMATION Graduates and Families, Our 2017 Graduation Ceremony is almost here! DATE: Friday, July 7, 2017 at 3 p.m. LOCATION: Grand Canyon University ADDRESS: 3300 W. Camelback Rd. Phoenix, AZ 85017 Please review the following information about the ceremony, which includes directions to Grand Canyon University, an area map, a list of local hotels and restaurants, frequently asked questions and helpful post-graduation information. All graduates must arrive between 11 a.m - 12:15 p.m. to check in. Cap and gown distribution will also take place during this time for students who have not already recieved these items. A rehearsal and final review of event details by our staff will begin at 12:15 p.m. for all graduates that are partcipating in the ceremony. Please arrive at the scheduled time to ensure that we can rehearse and begin the ceremony on time. Guests will be seated once the Arena doors are opened at approximately 2 p.m. The ceremony will begin promptly at 3 p.m., so we ask that all guests find their seats prior to this time. If you have any questions regarding the ceremony, please email us at [email protected] or contact your guidance counselor. We look forward to celebrating this special occasion with you—what an accomplishment! Sincerely, Primavera Faculty and Staff 2471 N. Arizona Ave PHONE 480.456.6678 Chandler, AZ 85225 TOLL FREE 877.877.4628 ChoosePrimavera.com FAX 480.355.2100 2017 Graduation Information DIRECTIONS GRAND CANYON UNIVERSITY ARENA 3300 W Camelback Rd, Phoenix, AZ 85017 gcuarena.com Directions from Interstate 17: N 43RD N 35TH EXIT on Camelback WEST on Camelback NORTH on 29th Ave or 33rd Ave 60 PARKING on left MISSOURI CAMELBACK Directions from Airport: INDIAN SCHOOL EXIT AIRPORT onto I-10 West CONTINUE to I-17 Interchange THOMAS NORTH on I-17 EXIT at Camelback (exit 143A) WEST on Camelback 60 NORTH on 29th Ave or 33rd Ave PARKING on left See detailed parking map on next page >>> 2471 N. -

Local Resources

Local Resources Grocery Stores/Pharmacies *Safeway Money - Orders .69 cents Phoenix Public Market 340 E McDowell Rd 14 E Pierce St Phoenix, AZ 85004 Phoenix, AZ 85004 (602) 252-4538 (602) 254-1799 2 mins / 0.25 miles 2 mins / 0.84 miles Los Altos Ranch Market *Safeway Money Orders .69 cents 1602 E Roosevelt St 520 W Osborn Rd Phoenix, AZ 85006 Phoenix, AZ 85013 (602) 254-7201 (602) 274-7422 4 mins / 1.6 miles 6 mins / 2.46 miles AJ’s Fine Foods *Fry’s Food & Drug 5017 N Central Ave - Money Orders .50 cents Phoenix, AZ 85012 744 W Camelback Rd (602) 230-7490 Phoenix, AZ 85013-2207 7 mins / 3.44 miles (602) 279-9001 12 mins / 4.4 miles Sprouts Whole Foods 2824 E Indian School Rd 4701 N 20th St Phoenix, AZ 85016 Phoenix, AZ 85016 (602) 553.3131 (602)761-4750 11 mins / 5.22 miles 7 mins/ 5.24 miles Trader Joes 4821 N 20th St Phoenix, AZ 85016 (602) 912-9022 8 mins / 5.39 miles *Denotes a Pharmacy on site Local Resources Grocery Stores/Pharmacies CVS Walgreen’s 1525 N Central Ave 705 E McDowell Rd Phoenix, AZ 85004 Phoenix AZ 85006 (602) 256-2124 (602) 258-4865 2 mins / 0.39 miles 2 mins / 0.46 miles Avella Specialty Pharmacy Walgreen’s Apothecary Shop 3402 N Central Ave 1101 N Central Ave #102 Phoenix AZ 85012 Phoenix AZ 85004 (602) 265-4781 (602) 257-1134 5 mins / 2.22 miles 5 mins / .6 miles CVS Food City 711 E Indian School Rd 2124 E McDowell Rd. -

Kimco Realty 2015 Annual Report

2020 VISION REALTY 2015 ANNUAL REPORT ABOUT THE COMPANY Kimco Realty Corporation (NYSE: KIM) is a real estate investment trust (REIT) headquartered in New Hyde Park, N.Y., that is North America’s largest publicly traded owner and operator of open-air shopping centers. As of December 31, 2015, the company owned interests in 564 open-air shopping centers comprising 90 million square feet of leasable space across 38 U.S. states and Puerto Rico. Letter from the Chairman 2 2015 Operating Review 4 Form 10-K 21 Shareholder Information 128 Corporate Directory IBC Dania Pointe, Dania Beach, FL MSA: Miami - Fort Lauderdale - West Palm Beach (FL) KIMCO’S 2020 VISION Over the past five years, Kimco has transformed its business and created additional shareholder value by successfully executing on the Company’s Back to Basics and TSR+ (Transform, Simplify, Redevelop, Plus) strategies. As we look ahead to the next five years, Kimco’s 2020 Vision is focused on three key objectives: QUALITY Major Metro Focused SIMPLICITY Transparent and Efficient STRENGTH Balance Sheet 1 CHAIRMAN’S LETTER Our talented team has managed the successful transformation of our business with a clear and focused vision on future growth. Dear Fellow Shareholders and Associates During this past winter when a record-breaking storm ren- resiliency. Many of our top tenants are grocers and off-price dered me snowbound for a few days, I had a chance to retailers, and over 85% of our Annualized Base Rent comes reflect on our sector and our Company. I loved the open air from sites anchored by one or more of these operators.