Cardiff Office Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Attached List Shows Those Planning Applications Received by the Council During the Stated Week

CARDIFF COUNTY COUNCIL PLANNING APPLICATIONS RECEIVED DURING THE WEEK ENDING 9TH FEBRUARY 2016 The attached list shows those planning applications received by the Council during the stated week. These applications can be inspected during normal working hours at the address below: STRATEGIC PLANNING, HIGHWAYS, TRAFFIC & TRANSPORTATION COUNTY HALL CARDIFF CF10 4UW Any enquiries or representations should be addressed to the CHIEF STRATEGIC PLANNING, HIGHWAYS, TRAFFIC & TRANSPORTATION OFFICER at the above address. In view of the provisions of the Local Government (Access to Information) Act 1985, such representations will normally be available for public inspection. The following dates have been confirmed for future meetings of the Planning Committee: 15 March 2017 Total Count of Applications: 57 ADAMSDOWN 17/00171/MJR Outline Planning Permission Expected Decision DEL Received: 03/02/2017 Ward: ADAMSDOWN Case Officer: Justin Jones Applicant: Amos Projects Ltd , , , Agents: C2J Architects & Town Planners, UNIT 1A COMPASS BUSINESS PARK, PACIFIC ROAD, OCEAN PARK Proposal: PROPOSED DEMOLITION OF EXISTING BUILDING AND CONSTRUCTION OF RESIDENTIAL DEVELOPMENT OF 17 X 1BED AND 1 X 2 BED APARTMENTS, PARKING, CYCLE, REFUSE AND AMENITY FACILITIES At: THE CITADEL, PEARL STREET/SPLOTT ROAD, ADAMSDOWN, CARDIFF. CF24 1HD BUTETOWN 17/00159/MJR Full Planning Permission Expected Decision DEL Received: 26/01/2017 Ward: BUTETOWN Case Officer: Lawrence Dowdall Applicant: - Rightacres Property Company Limited, , , Agents: Nathaniel Lichfield and Partners, Helmont -

BBC Cymru Wales Apprenticeship Role: Sound Apprentice Location: Roath Lock Studios, Cardiff

Sound Apprentice - Drama Company: BBC Cymru Wales Apprenticeship Role: Sound Apprentice Location: Roath Lock Studios, Cardiff About the Organisation BBC Cymru Wales is the nation's broadcaster, providing a wide range of English and Welsh language content for audiences across Wales on television, radio and on our websites Roath Lock, is the BBC's state of the art centre of excellence for Drama, a place brimming with new energy and talent. When the first productions moved into Roath Lock in September 2011, they fulfilled a BBC commitment to create a centre of excellence for Drama in Cardiff. Located in Porth Teigr, Cardiff Bay, the 170,000 square foot facility, including nine studios and equivalent in length to three football pitches, is now the permanent, purpose-built home of four flagship BBC dramas - Casualty, Pobol y Cwm, Doctor Who - as well as new productions in the future. Job Description Sound Assistants are a member of the Production Sound Crew and provide general back up and support to the Production Sound Mixer and the Boom Operator. They are responsible for checking all stock, microphones and batteries and making sure that the sound department runs as smoothly as possible. Although the work is physically demanding, the hours are long and are sometimes performed on location in extreme terrain and/or severe weather the work can be very rewarding. Sound Assistants usually begin work early arriving on set half at least an hour before call time, with the rest of the Sound Crew. They help to unload the sound van, and working with the Boom Operator, check that all equipment is prepared and fully operational. -

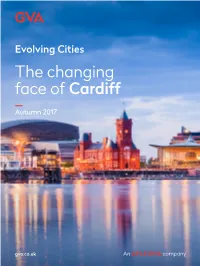

The Changing Face of Cardiff

Evolving Cities The changing face of Cardiff Autumn 2017 gva.co.uk Evolving cities The UK’s cities are The Changing Face of Cardiff is one of our series of reports looking at how undergoing a renaissance. the UK’s key cities are evolving and Large scale place making the transformational change that is schemes are dramatically occurring, either in terms of the scale improving how they are of regeneration activity or a shift in perception. perceived, making them more desirable places to For each city, we identify the key locations where such change has live and work, and better occurred over the last 10 years, able to attract new people and the major developments that and businesses. continue to deliver it. We then explore the key large scale regeneration opportunities going forward. Cardiff today Cardiff is the capital Cardiff’s city status and wealth The city has become a popular The city’s transport links are international location for businesses was primarily accrued from its tourist location which has been undergoing significant improvement. is supported by the city’s ability to and focal point of Wales. coal exporting industry, which led underpinned by major investments At Cardiff Central Station, Network Rail offer high quality office stock within Historically the city to the opening of the West Bute in leisure, sports and cultural venues. has recently added a new platform, Central Square, Callaghan Square flourished, becoming Dock and transformed Cardiff’s The construction of Mermaid Quay facilities and a modern entrance to and Capital Quarter. Key occupiers the world’s biggest coal landscape. -

Economic Events Diary November 2010 -December 2011

Welsh Economic Review Economic Events Diary November 2010 -December 2011 November 2010 In a deal reportedly worth billions of pounds to the UK, China of the six sector external panel chairs were announced Aviation Supplies Holding Company (CAS) substantially as: Sir Chris Evans (life sciences); Gareth Jenkins (advanced expanded its order from Airbus to 102 aeroplanes. Final materials and manufacturing); Chris Nott (financial and wing assembly for Airbus is carried out at its Broughton, professional services); Kevin McCullough (energy and Flintshire facility. environment); Thomas Kelly (ICT); and Ron Jones (creative industries). Japanese company Sharp PV announced a £35m investment at its solar panel production facility in Wrexham. The new March 2011 rd investment will fund three new assembly lines and double Following a referendum which took place on March 3 , the production capacity. In early 2011 the company revealed people of Wales voted for the National Assembly to have law- details of an expansion in jobs at the site, which exports making powers in 20 policy areas excluding defence, throughout Europe (see Comings & Goings section). foreign affairs, fiscal, monetary and economic policy, broadcasting, social security, immigration, employment law, The Welsh Assembly Government announced the closure of policing and criminal law. Wales can follow different pathways six out of the ten Technium innovation centres in Wales. from the rest of the UK in education, health and economic In a statement from the Deputy Minister for Science, development. Innovation & Skills, Lesley Griffiths, it was noted that a review of the centres (which provide incubation support, such The Wales Manufacturing Forum unveiled its manufacturing as office space, for new and growing businesses) had found Strategy for Wales . -

Dev-Plan.Chp:Corel VENTURA

On Track for the 21st Century A Development Plan for the Railways of Wales and the Borders Tua’r Unfed Ganrif ar Ugain Cynllun Datblygu Rheilffyrdd Cymru a’r Gororau Railfuture Wales 2nd Edition ©September 2004 2 On Track for the 21st Century Section CONTENTS Page 1 Executive summary/ Crynodeb weithredol ......5 2 Preface to the Second Edition .............9 2.1 Some positive developments . 9 2.2 Some developments ‘in the pipeline’ . 10 2.3 Some negative developments . 10 2.4 Future needs . 10 3 Introduction ..................... 11 4 Passenger services .................. 13 4.1 Service levels . 13 4.1.1 General principles .............................13 4.1.2 Service levels for individual routes . ................13 4.2 Links between services: “The seamless journey” . 26 4.2.1 Introduction .................................26 4.2.2 Connectional policies ............................27 4.2.3 Through ticketing ..............................28 4.2.4 Interchanges .................................29 4.3 Station facilities . 30 4.4 On-train standards . 31 4.4.1 General principles .............................31 4.4.2 Better trains for Wales and the Borders . ...............32 4.5 Information for passengers . 35 4.5.1 Introduction .................................35 4.5.2 Ways in which information could be further improved ..........35 4.6 Marketing . 36 4.6.1 Introduction .................................36 4.6.2 General principles .............................36 5 Freight services .................... 38 5.1 Introduction . 38 5.2 Strategies for development . 38 6 Infrastructure ..................... 40 6.1 Introduction . 40 6.2 Resignalling . 40 6.3 New lines and additional tracks / connections . 40 6.3.1 Protection of land for rail use ........................40 6.3.2 Route by route requirements ........................41 6.3.3 New and reopened stations and mini-freight terminals ..........44 On Track for the 21st Century 3 Section CONTENTS Page 7 Political control / planning / funding of rail services 47 7.1 Problems arising from the rail industry structure . -

194 ADAM Appnum Register

Applications decided by Delegated Powers between 01/01/2010 and 31/01/2010 Total Count of Applications: 194 ADAM AppNum Registered AppName Proposal Location Days taken <= 56 Dcn DcnDate 45 True PER 04/01/2010 09/02032/C 20/11/2009 Khan CONVERSION FROM FIVE SELF 12 PIERCEFIELD PLACE, CONTAINED RESIDENTIAL UNITS ADAMSDOWN, CARDIFF, INTO EIGHT SELF CONTAINED CF24 0LD RESIDENTIAL UNITS WITH A THREE STOREY SIDE EXTENSION 53 True PER 05/01/2010 09/02021/C 13/11/2009 Cardiff Community Housing AssociationDEMOLITION Ltd AND REBUILDING OF 28 DIAMOND STREET, EXISTING DWELLING ADAMSDOWN, CARDIFF, CF24 1NQ 46 True PER 05/01/2010 09/02043/C 20/11/2009 Cardiff Council NEW SHOPFRONT & ROLLER 143 CLIFTON STREET, SHUTTERS ADAMSDOWN, CARDIFF, CF24 1LZ 41 True PER 05/01/2010 09/02082/C 25/11/2009 Cardiff Community Housing AssociationDEMOLITION Ltd AND REBUILDING OF 27 SAPPHIRE STREET, EXISTING DWELLING ADAMSDOWN, CARDIFF, CF24 1PY 41 True PER 05/01/2010 09/02083/C 25/11/2009 Cardiff Community Housing AssociationDEMOLITION Ltd AND REBUILDING OF 22 RUBY STREET, EXISTING DWELLING ADAMSDOWN, CARDIFF, CF24 1LN 41 True PER 06/01/2010 09/02102/C 26/11/2009 Mr Caesar Lucius CHANGE OF USE FROM RETAIL TO 11 CLIFTON STREET, BEAUTY SPA ADAMSDOWN, CARDIFF, CF24 1PX 50 True PER 07/01/2010 09/02053/C 18/11/2009 Mr Arif Khan FIRST FLOOR REAR EXTENSION 14 RICHARDS TERRACE, AND REINSTATEMENT OF GROUND ROATH, CARDIFF, CF24 FLOOR FRONT BAY 1RU 47 True PER 25/01/2010 09/02169/C 09/12/2009 Mr Brain James Ash PROPOSED REAR GROUND FLOOR 79 BROADWAY, EXTENSION AND THE RELOCATION -

The Social Services Bill for Wales & Promoting Well-Being

The Social Services Bill for Wales & promoting well-being 150,000 young, old and disabled people receive help each year from Wales’ Social Services. Many of these services are delivered in partnership between organisations from the housing, health and education sectors. The Welsh Government is intending to develop legislation that maintains and enhances the wellbeing of people in need. A duty to that effect will form part of the Bill. Our key concern has been the need to make Social Services in Wales sustainable. Our strategy for this was set out in Sustainable Social Services for Wales: A Framework for Action. The central purpose for this Bill is to provide the legislative framework to enable us to deliver that strategy. Providing appropriate services often requires intervention at an earlier stage and reflects a key principle of the Welsh Government’s approach to sustainable development. Part of the Social Services (Wales) Bill will encourage the promotion of preventative strategies and access to support that will result in better outcomes for people; which we hope will save on more costly interventions at a later stage. The legislation aims to give individuals a stronger voice and real control of the services they use, enabling them to understand how care and support can help them. It will also place a duty on social services and the NHS to collaborate in how they deliver integrated services. WG15470 own Copyright 2012 © Cr The Sustainable Development framework is thinking long-term The Welsh Local Government Association, through their Sustainable Development Framework have been encouraging local authorities and Local Service Boards to develop techniques and approaches to long term thinking for their strategies and partnerships. -

Year 8 Summer Learning Year 8 Summer Learning

Year 8 Summer Learning Year 8 Summer Learning Wednesday 24th June Thursday 25th June Friday 26th June Sense of Wales Wonderful Welsh Weekend Monmouthshire Trails Conference Challenge • Visit a site of cultural significance in • Spend the day at the Wyastone • Choose a local peak or trail to Wales Estate, just outside of Monmouth walk • You choose where to visit •Work in form bases around the • Different degrees of difficulty • Linked to the ‘Wonderful Welsh estate as well as spending time in the • Challenge yourself! Weekend’ project stunning concert hall. • Celebrate after with food at • Information collected will be used the • Information from the previous day Skenfrith Castle following day will be used during the day. Discover Wales Gather Information Using Information Physical Challenge Celebrate Together Sense of Wales Wednesday 24th June • You are going to have the opportunity to visit a site of cultural significance in Wales on the Wednesday of Summer Learning Week • You will choose your preferred site to visit • You will be expected to gather information and data from your visit to be used the following day during Summer Learning. National Museum Cardiff (30 places) www.museumwales.ac.uk/en/cardiff Discover art, archaeology, natural history and geology. With a busy programme of exhibitions and events, the National Museum has something to amaze everyone, whatever your interest. The art collection is one of Europe's finest. Five hundred years of magnificent paintings, drawings, sculpture, silver and ceramics from Wales and across the world, including one of Europe's best collections of Impressionist works. Prepare for a 4,600 million-year voyage accompanied by meteorites, moon rock and fossils on a journey bringing you face to face with dinosaurs and woolly mammoths. -

The Attached List Shows Those Planning Applications Received by the Council During the Stated Week

CARDIFF COUNTY COUNCIL PLANNING APPLICATIONS RECEIVED DURING WEEK ENDING 10TH OCTOBER 2019 The attached list shows those planning applications received by the Council during the stated week. These applications can be inspected during normal working hours at the address below: PLANNING, TRANSPORT AND ENVIRONMENT COUNTY HALL CARDIFF CF10 4UW Any enquiries or representations should be addressed to the CHIEF STRATEGIC PLANNING, HIGHWAYS, TRAFFIC & TRANSPORTATION OFFICER at the above address. In view of the provisions of the Local Government (Access to Information) Act 1985, such representations will normally be available for public inspection. Future Planning Committee Dates are as follows: 16 October 2019 20 November 2019 18 December 2019 22 January 2020 19 February 2020 18 March 2020 22 April 2020 20 May 2020 24 June 2020 22 July 2020 19 August 2020 Total Count of Applications: 39 BUTETOWN 19/02681/MJR Discharge of Condition(s) Expected Decision Level: DEL Received: 04/10/2019 Ward: BUTETOWN Case Officer: Richard Cole Applicant: Holland Morgan Sindall, Cae Gwyrdd, Greenmeadow Springs Business Park, Cardiff Agents: Chetwoods, 32, Frederick Street, Birmingham, , B1 3HH Proposal: DISCHARGE OF CONDITIONS 9 (FUME EXTRACTION) AND 15 (CYCLE SPACES) OF 18/00792/MJR At: HMS CAMBRIA, CARGO ROAD, CARDIFF BAY, CARDIFF, CF10 4RP 19/02699/MJR Discharge of Condition(s) Expected Decision Level: DEL Received: 09/10/2019 Ward: BUTETOWN Case Officer: Amanda Sutcliffe Applicant: Ms Thomas Platform Cardiff, , , Agents: RPS Planning & Development, Park House, Greyfriars Road, Cardiff, , CF10 3AF Proposal: DISCHARGE OF CONDITION 9 (LANDSCAPING) OF 18/02383/MJR At: FORMER BROWNING JONES AND MORRIS, DUMBALLS ROAD, BUTETOWN, CARDIFF A/19/00126/MNR Advertisement Expected Decision Level: DEL Received: 04/10/2019 Ward: BUTETOWN Case Officer: Clare Beaney Applicant: Holland Morgan Sindall, Cae Gwyrdd, Greenmeadow Springs Business Park, Cardiff Agents: Chetwoods, 32, Frederick Street, Birmingham, , B1 3HH Proposal: X2 FASCIA SIGNS TO NORTH AND SOUTH ELEVATIONS. -

Cardiff Council Cyngor Caerdydd Cabinet Meeting

CARDIFF COUNCIL CYNGOR CAERDYDD CABINET MEETING: 15 FEBRUARY 2018 INDOOR ARENA INVESTMENT & DEVELOPMENT (COUNCILLOR RUSSELL GOODWAY) AGENDA ITEM:9 REPORT OF DIRECTOR OF ECONOMIC DEVELOPMENT Appendices 1, 3 and 4 are not for publication as they contain exempt information of the description contained in paragraphs 14 and 21 of Schedule 12A of the Local Government Act 1972. Reason for this Report 1. To present the results of a site options appraisal exercise to identify the preferred location for delivery of the indoor arena project following the administration’s recent announcement in their strategic policy statement Capital Ambition that delivery of a new indoor arena is one of two key strategic regeneration priorities for the city’s core employment zone. 2. To seek authority to prepare a detailed delivery strategy based on the preferred location to include full financial implications for the Council and to report back to a future meeting of Cabinet for authority to proceed. Background 3. Delivery of a new Multi-purpose Arena has been a long standing priority for the city. Since the turn of the millennium, a number of reports have been presented to successive Cabinets outlining the strategic importance of securing a ‘top-tier’ facility. 4. In 2013, the ‘Rebuilding Momentum’ Green Paper consultation identified the lack of a ‘top-tier’ arena as a key weakness in the city’s business and cultural offer. Since then the Council has included actions in its Corporate Plan to progress delivery of the project. 5. In September 2013 Cabinet agreed to a market testing exercise to help develop a specification for a new facility and to gauge private sector interest. -

Doctor Who 1 Doctor Who

Doctor Who 1 Doctor Who This article is about the television series. For other uses, see Doctor Who (disambiguation). Doctor Who Genre Science fiction drama Created by • Sydney Newman • C. E. Webber • Donald Wilson Written by Various Directed by Various Starring Various Doctors (as of 2014, Peter Capaldi) Various companions (as of 2014, Jenna Coleman) Theme music composer • Ron Grainer • Delia Derbyshire Opening theme Doctor Who theme music Composer(s) Various composers (as of 2005, Murray Gold) Country of origin United Kingdom No. of seasons 26 (1963–89) plus one TV film (1996) No. of series 7 (2005–present) No. of episodes 800 (97 missing) (List of episodes) Production Executive producer(s) Various (as of 2014, Steven Moffat and Brian Minchin) Camera setup Single/multiple-camera hybrid Running time Regular episodes: • 25 minutes (1963–84, 1986–89) • 45 minutes (1985, 2005–present) Specials: Various: 50–75 minutes Broadcast Original channel BBC One (1963–1989, 1996, 2005–present) BBC One HD (2010–present) BBC HD (2007–10) Picture format • 405-line Black-and-white (1963–67) • 625-line Black-and-white (1968–69) • 625-line PAL (1970–89) • 525-line NTSC (1996) • 576i 16:9 DTV (2005–08) • 1080i HDTV (2009–present) Doctor Who 2 Audio format Monaural (1963–87) Stereo (1988–89; 1996; 2005–08) 5.1 Surround Sound (2009–present) Original run Classic series: 23 November 1963 – 6 December 1989 Television film: 12 May 1996 Revived series: 26 March 2005 – present Chronology Related shows • K-9 and Company (1981) • Torchwood (2006–11) • The Sarah Jane Adventures (2007–11) • K-9 (2009–10) • Doctor Who Confidential (2005–11) • Totally Doctor Who (2006–07) External links [1] Doctor Who at the BBC Doctor Who is a British science-fiction television programme produced by the BBC. -

Gloworks Café, Retail & Office Units To

PorthTeigr GloWorks Café, Retail & Office Units To Let porthteigr.com/gloworks The Café, Retail and Office units are located on the ground GloWorks floor of Gloworks the new creative industries centre in the heart of Porth Teigr in Cardiff Bay. Overlooking the water Gound Floor and adjacent to the BBC studios in an area frequented by Retail Units cyclists, walkers and leisure tourists. Unit 1 Terms A A3 / restaurant / café unit, overlooking The units are available on new Roath Basin with an outside seating area. full repairing and insuring leases via a service charge. Unit 2 A studio/office unit. Full details and rent available from the marketing agents. EPC The property has an EPC rating of B31. Schedule of Accommodation Net Internal Areas m2 ft2 Unit 1 (incorporating office 294 3170 meeting room) Unit 2 66 710 Unit 2 Unit 1 Reception Office (1) Pierhead Senedd — National Assembly for Wales Mermaid Quay Norwegian Church Doctor Who Experience Outer Lock Crossing GloWorks BBC Roath Lock Studios porthteigr.com/gloworks Gloworks together with BBC Cymru Wales’s Roath Lock studios is a hub for Wales’ dynamic creative sector. The Roath Lock Studios – the BBC’s 170,000 sq. ft. drama production studio complex is home to flagship BBC productions including Doctor Who, Casualty and Pobol y Cwm. Porth Teigr forms part of the Cardiff Bay area and is in close proximity to The Welsh Millennium Centre, The Senedd, Mermaid Quay and the existing vibrant residential and office communities. Porth Teigr is a joint venture between Igloo and Welsh Government and Gloworks comprises 38 acres of prime waterfront development in Cardiff Bay.