Regional PC Hardware Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ASUSTEK COMPUTER INC. NON-CONSOLIDATED FINANCIAL STATEMENTS December 31, 2007 and 2006 with Report of Independent Auditors

ASUSTEK COMPUTER INC. NON-CONSOLIDATED FINANCIAL STATEMENTS December 31, 2007 and 2006 With Report of Independent Auditors The reader is advised that these financial statements have been prepared originally in Chinese. In the event of a conflict between these financial statements and the original Chinese version or difference in interpretation between the two versions, the Chinese language financial statements shall prevail. English Translations of Financial Statements Originally Issued in Chinese ASUSTEK COMPUTER INC. NON-CONSOLIDATED BALANCE SHEETS DECEMBER 31, 2007 AND 2006 (Expressed in New Taiwan Thousand Dollars) ASSETS Notes 2007 2006 LIABILITIES AND STOCKHOLDERS' EQUITY Notes 2007 2006 CURRENT ASSETS CURRENT LIABILITIES Cash and cash equivalents II, IV.1 $9,174,219 $10,791,836 Notes and accounts payable $80,372,075 $109,230,069 Financial assets at fair value through profit or loss-current II, IV.2 7 ,257,169 4,218,719 Notes and accounts payable -affiliated companies V 837,669 9,007,117 Notes and accounts receivable-Net II, IV.3 61 ,863,244 80,950,232 Income tax payable II, IV.19 5,795,472 3,558,780 Accounts receivable-affiliated companies-Net II, IV.3, V 45 ,747,118 21,152,900 Accrued expenses II, IV.12, V 31,771,898 21,553,421 Other receivables-Net II,V 5 ,069,634 1,627,107 Other payables V 771,563 469,653 Inventories-Net II, IV.4 53 ,643,865 72,627,961 Receipts in advance V 2,412,198 2,502,732 Prepayments V 121 ,788 162,382 Bonds payable-current portion IV.11 - 6,613,377 Other current assets 101 ,863 - Other current liabilities -

Inventec Corporation

(English Translation of Pro Forma Financial Report Originally Issued in Chinese) PEGATRON CORPORATION AND ITS SUBSIDIARIES PRO FORMA CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2008 AND 2007 (With Independent Auditors’ Report Thereon) Address: 5F., No.76, Ligong St., Beitou District, Taipei City 112, Taiwan Telephone: 886-2-8143-9001 - 1 - TABLE OF CONTENTS Contents Page Cover Page 1 Table of Contents 2 Independent Auditors’ Report 3 Pro Forma Consolidated Balance Sheets 4 Pro Forma Consolidated Statements of Income 5 Pro Forma Consolidated Statements of Changes in Stockholders’ Equity 6 Pro Forma Consolidated Statements of Cash Flows 7 Notes to Pro Forma Consolidated Financial Statements (1) Organization and Business 8 (2) Summary of Significant Accounting Policies 8-28 (3) Reasons for and Effects of Accounting Changes 28 (4) Summary of Major Accounts 28-49 (5) Related-Party Transactions 50-56 (6) Pledged Assets 56 (7) Significant Commitments and Contingencies 57-58 (8) Significant Catastrophic Losses 59 (9) Significant Subsequent Events 59 (10) Others 59 (11)Additional Disclosures 60-61 (12)Segment Information 61-62 - 2 - (English Translation of Financial Report Originally Issued in Chinese) PEGATRON CORPORATION AND ITS SUBSIDIARIES PRO FORMA CONSOLIDATED BALANCE SHEETS DECEMBER 31, 2008 AND 2007 (All Amounts Expressed in Thousands of New Taiwan Dollars, Except for Share Data) December 31, 2008 December 31, 2007 Amount % Amount % ASSETS Current Asset: Cash (Notes 2 and 4(1)) $ 27,065,987 12 26,294,882 9 Financial assets reported -

Taiwan's Top 50 Corporates

Title Page 1 TAIWAN RATINGS CORP. | TAIWAN'S TOP 50 CORPORATES We provide: A variety of Chinese and English rating credit Our address: https://rrs.taiwanratings.com.tw rating information. Real-time credit rating news. Credit rating results and credit reports on rated corporations and financial institutions. Commentaries and house views on various industrial sectors. Rating definitions and criteria. Rating performance and default information. S&P commentaries on the Greater China region. Multi-media broadcast services. Topics and content from Investor outreach meetings. RRS contains comprehensive research and analysis on both local and international corporations as well as the markets in which they operate. The site has significant reference value for market practitioners and academic institutions who wish to have an insight on the default probability of Taiwanese corporations. (as of June 30, 2015) Chinese English Rating News 3,440 3,406 Rating Reports 2,006 2,145 TRC Local Analysis 462 458 S&P Greater China Region Analysis 76 77 Contact Us Iris Chu; (886) 2 8722-5870; [email protected] TAIWAN RATINGS CORP. | TAIWAN'S TOP 50 CORPORATESJenny Wu (886) 2 872-5873; [email protected] We warmly welcome you to our latest study of Taiwan's top 50 corporates, covering the island's largest corporations by revenue in 2014. Our survey of Taiwan's top corporates includes an assessment of the 14 industry sectors in which these companies operate, to inform our views on which sectors are most vulnerable to the current global (especially for China) economic environment, as well as the rising strength of China's domestic supply chain. -

Summary of Investments by Type

COMMON INVESTMENT FUNDS Schedule of Investments March 31, 2017 SUMMARY OF INVESTMENTS BY TYPE Cost Market Value Fixed Income Investments $ $ Short-term investments 42,653,484 42,653,484 Bonds 175,482,352 175,327,122 Mortgage-backed securities 22,199,796 21,785,061 Emerging markets debt 9,619,817 10,899,147 Bank loans - high income fund 20,985,176 23,595,337 Total Fixed Income Investments 270,940,624 274,260,151 Equity-Type Investments Mutual funds Domestic 9,234,353 12,420,750 International 18,849,681 18,688,379 Common stocks Domestic 152,833,551 187,487,257 International 216,167,277 227,850,648 Total Equity-Type Investments 397,084,862 446,447,034 Alternative Investments Funds of hedge funds 38,264,990 46,247,453 Real estate trust fund 6,876,041 10,104,141 Total Alternatives Investments 45,141,031 56,351,594 TOTAL INVESTMENTS 713,166,517 777,058,779 Page 1 of 32 COMMON INVESTMENT FUNDS Schedule of Investments March 31, 2017 SUMMARY OF INVESTMENTS BY FUND Cost Market Value Fixed Income Fund $ $ Short-term investments 13,092,627 13,092,627 Bonds 143,036,345 143,362,214 Mortgage-backed securities 21,372,523 20,977,317 Emerging markets debt 9,619,817 10,899,147 Bank loans - high income fund 20,985,176 23,595,337 208,106,487 211,926,642 Domestic Core Equity Fund Short-term investments 9,127,791 9,127,791 Common stocks 134,983,626 165,021,220 Futures - (5,950) Private placement 4,150 4,150 144,115,567 174,147,211 Small Cap Equity Fund Short-term investments 2,937,066 2,937,066 Mutual funds 9,234,353 12,420,750 Common stocks 17,845,775 22,467,836 -

Chapter 2 Hon Hai/Foxconn: Which Way Forward ?

Chapter 2 Hon Hai/Foxconn: which way forward ? Gijsbert van Liemt 1 1. Introduction Hon Hai/Foxconn, the world's leading contract manufacturer, assembles consumer electronics products for well-known brand-names. It is also a supplier of parts and components and has strategic alliances with many other such suppliers. Despite its size (over a million employees; ranked 32 in the Fortune Global 500) and client base (Apple, HP, Sony, Nokia), remarkably little information is publicly available on the company. The company does not seek the limelight, a trait that it shares with many others operating in this industry. Quoted on the Taiwan stock exchange, Hon Hai Precision Industry (HHPI) functions as an ‘anchor company’ for a conglomerate of companies. 2 As the case may be, HHPI is the sole, the majority or a minority shareholder in these companies and has full, partial or no control at all. Many subsidiaries use the trade name Foxconn and that is why this chapter refers to the company as Hon Hai/Foxconn. Among its many subsidiaries and affiliates are Ambit Microsystems, Cybermart, FIH Mobile, Fu Taihua Industrial, Hong Fujin Precision and Premier Image. After a near hundredfold increase in sales in the first decade of this century Hon Hai/Foxconn's sales growth slowed down drastically. The company is facing several challenges: slowing demand growth in its core (electronics) business; a weakening link with Apple, its main customer; rising labour costs and a more assertive labour force in China, its main production location; and pressure from its shareholders. 1. Copyright 2015 Gijsbert van Liemt. -

Pegatron Corporation and Subsidiaries

1 Stock Code:4938 (English Translation of Consolidated Financial Statements and Report Originally Issued in Chinese) PEGATRON CORPORATION AND SUBSIDIARIES Consolidated Financial Statements With Independent Accountants’ Review Report For the Three Months Ended March 31, 2018 and 2017 Address: 5F., No.76, Ligong St., Beitou District, Taipei City 112, Taiwan Telephone: 886-2-8143-9001 The auditors’ review report and the accompanying consolidated financial statements are the partial English translation of the Chinese version prepared and used in the Republic of China. If there is any conflict between, or any difference in the interpretation of the English and Chinese language auditors’ review report and consolidated financial statements, the Chinese version shall prevail. 2 Table of contents Contents Page 1. Cover Page 1 2. Table of Contents 2 3. Independent Accountants’ Review Report 3 4. Consolidated Balance Sheets 4 5. Consolidated Statements of Comprehensive Income 5 6. Consolidated Statements of Changes in Equity 6 7. Consolidated Statements of Cash Flows 7 8. Notes to the Consolidated Financial Statements (1) Company history 8 (2) Approval date and procedures of the consolidated financial statements 8 (3) Application of new standards, amendments and interpretations 8~15 (4) Summary of significant accounting policies 16~50 (5) Significant accounting assumptions and judgments, and major sources 50 of estimation uncertainty (6) Explanation of significant accounts 51~90 (7) Related-party transactions 90~91 (8) Pledged assets 91 (9) Significant -

AQR TM Emerging Multi-Style Fund June 30, 2021

AQR TM Emerging Multi-Style Fund June 30, 2021 Portfolio Exposures NAV: $685,149,993 Asset Class Security Description Exposure Quantity Equity A-Living Services Ord Shs H 2,001,965 402,250 Equity Absa Group Ord Shs 492,551 51,820 Equity Abu Dhabi Commercial Bank Ord Shs 180,427 96,468 Equity Accton Technology Ord Shs 1,292,939 109,000 Equity Acer Ord Shs 320,736 305,000 Equity Adani Enterprises Ord Shs 1,397,318 68,895 Equity Adaro Energy Tbk Ord Shs 2,003,142 24,104,200 Equity Advanced Info Service Non-Voting DR 199,011 37,300 Equity Advanced Petrochemical Ord Shs 419,931 21,783 Equity Agricultural Bank of China Ord Shs A 288,187 614,500 Equity Agricultural Bank Of China Ord Shs H 482,574 1,388,000 Equity Al Rajhi Bank Ord Shs 6,291,578 212,576 Equity Alibaba Group Holding ADR Representing 8 Ord Shs 33,044,794 145,713 Equity Alinma Bank Ord Shs 1,480,452 263,892 Equity Ambuja Cements Ord Shs 305,517 66,664 Equity Anglo American Platinum Ord Shs 174,890 1,514 Equity Anhui Conch Cement Ord Shs A 307,028 48,323 Equity Anhui Conch Cement Ord Shs H 1,382,025 260,500 Equity Arab National Bank Ord Shs 485,970 80,290 Equity ASE Technology Holding Ord Shs 2,982,647 742,000 Equity Asia Cement Ord Shs 231,096 127,000 Equity Aspen Pharmacare Ord Shs 565,696 49,833 Equity Asustek Computer Ord Shs 1,320,000 99,000 Equity Au Optronics Ord Shs 2,623,295 3,227,000 Equity Aurobindo Pharma Ord Shs 3,970,513 305,769 Equity Autohome ADS Representing 4 Ord Shs Class A 395,017 6,176 Equity Axis Bank GDR 710,789 14,131 Equity Ayala Land Ord Shs 254,266 344,300 -

QS-9000 on Customer Satisfaction

國立中山大學 管理學院 國際高階經營碩士學程碩士在職專班 碩士論文 Impact of the Implementation of QS-9000 on Customer Satisfaction in Taiwan’s Auto-parts Manufacturing Industry 探討臺灣汽車零件製造業實施 QS-9000 品保系統 與客戶滿意度之關係 研究生:楊森鴻 撰 指導教授:周泰華博士 中華民國 九十二年六月 中文致謝詞 i 中文致謝詞 隨著時間邁入 2003 年,我在國立中山大學國際高階經營碩士學程也將逐漸 進入終點。對我個人而言,離開學校已經超過 20 年了,如果中山沒有提供 IEMBA 這個學程,自己也不可能有這個機會再接觸到管理這方面的專業知識。我們生長 在這個劇變的時代。全球化,知識經濟等等理論不斷被提出,在在都推翻了以前 既有的概念,如果不求新知,很容易就被潮流淹沒。 本論文的完成,首先要感謝指導教授周泰華博士,他淵博的學識及耐心的指 導,尤其在關鍵時刻的引導,使得撰寫過程遇到瓶頸時,都能否極泰來。當然口 試委員李清潭博士,郭倉義博士的指導及高見,使得本篇論文也增色不少。 在論文訪談時,一些認識或不認識的朋友的大力協助,使得個案公司的資料 能順利取得,實在令我永生難忘。他們包括我在 IEMBA 2 同學敦揚科技趙處長瑞 君兄,金利公司總經理室特助楊日竹經理,瑞興發公司林焜瑞專員,繼茂公司品 保部陳志慶副理,他們的熱心協助實在令人難忘。 2002 年底正逢服務公司全力開發 253 Ministick 及推行 QS9000 品保系統認證 的緊要關頭,但我在臺灣博士電子公司品保處的部門秘書吳惠娟小姐,仍不厭其 煩替我整理圖表,中文報告的繕打等等額外的工作,對我完成碩士課程也發揮莫 大的助力,在此也一併致上十二萬分的謝意。 也要感謝內人林照娟女士,在這二年沒有個人時間也沒有家庭時間的充電學 習過程中,如果沒有她的諒解及全力照顧家庭,是不能使我順利完成學業。在人 生的道路上能有這一段再充電的生命歷程,實在是既豐富且又充滿無限的感恩, 讓人永遠的懷念。 最後要感謝中山管院副院長徐守德博士及全體授課的老師,和 IEMBA 2 的 全體同學,及我在博士電子公司品保處的蔡和良課長,如果沒有大家互相的扶 持,鼓勵和幫忙,這段路會走的更艱辛!謝謝你們! 臺灣博士電子公司品保處處長 楊森鴻 于西子灣 國立中山大學 2003 年 6 月 Acknowledgement ii Acknowledgement “Tempus Fugit”, the time is approaching fast that my graduate study, International Executive MBA program at National Sun Yat-sen University will be coming to an end. I graduated from National Central University more than twenty years ago. If NSYSU had not provided this IEMBA program, I might not have had the opportunity to return to campus to further my studies in the management field. Over the past decade, globalization and economic knowledge concepts have been introduced to the industry, and past experiences and knowledge have fallen by the wayside. We live in a fast paced, fast changing, highly demanding and competitive global market environment. The train of economic change and knowledge is leaving the station, we better be on it or we will be left behind. I would like to thank my advisor – Professor Tai-Hwa Chow for his patience and instruction for my thesis writing. -

Ken Sean Industries Co., Ltd

Ken Sean Industries Co., Ltd. Taiwan Ken Sean in Taiwan Locations: Plant 1(HQ) & Plant 2 Plant 1(HQ) ◇ Founded on 1950 Founder:Wen-Chin, Chuang Chairman:Joe Juang Plant area:Plant 1→23,200 ㎡ 彰化交流道 Plant 2 →37,584 ㎡ Factory area :Plant 1→15,126 ㎡ Plant 2 →9,653 ㎡ ◇ Product s & Maximum capacity 4W rear view mirror(1.5M PRS/YEAR) 2W rear view mirror(5M PRS/YEAR) Mirror plate(10Mft2/YEAR) Plant 2 Others (indicators, electronic parts, bicycle mirror) -2- Biography •K Source Being audited • Hanoi as a GM supplier. Vietnam founded •Certified by •Silver Mirror Plant •Started to ship ISO/TS to Volkswagen. 2011 2014 •K Source 16949:2002 2008 2010 . Vietnam founded •Awarded 2005 for TPM Xiamen K K Source • Excellence • Source Mirror Inc. in U.S.A. Industry 2015 founded founded 2001 •R&D Building 2006 2013 •Started producing 1995 2003 automotive mirrors •Awarded for • Start to •Offshore Special Award 1994 rebuild the Company - for TPM 1996 Achievement 」 plants 1992 Ken Sean 2000Group Co., •Awarded for •Awarded for Ltd. founded Industrial 1969 1988 National Sustainable • Certified by Excellence Started producing Quality • •Technical ISO 14001 Award motorcycle mirrors Award Agreement with • Established •Started to ship Murakami Electronics electronic 1960 Corporation Technical •Started 1972 • R&D Division interior mirrors producing Agreement to Porsche • FORD Supply bicycle mirrors with Honda Lock Mfg. 1957 1965 •Ken Sean factory •CSR: Wen- founded Jing Lecture 1950 •Ken Sean founded •Main Product: Make- Up Mirrors -3- Ken Sean Industries Ken Sean Group KenSean KenSean U.S.A Vietnam (HQ ,R&D) Group K Source K Source(TA) U.S.A. -

2020 Annual Report

AUGUST 31, 2020 2020 Annual Report iShares, Inc. • iShares MSCI Hong Kong ETF | EWH | NYSE Arca • iShares MSCI Japan Small-Cap ETF | SCJ | NYSE Arca • iShares MSCI Malaysia ETF | EWM | NYSE Arca • iShares MSCI Pacific ex Japan ETF | EPP | NYSE Arca • iShares MSCI Singapore ETF | EWS | NYSE Arca • iShares MSCI Taiwan ETF | EWT | NYSE Arca • iShares MSCI Thailand ETF | THD | NYSE Arca Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of each Fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. You may elect to receive all future reports in paper free of charge. Ifyou hold accounts throughafinancial intermediary, you can follow the instructions included with this disclosure, if applicable, or contact your financial intermediary to request that you continue to receive paper copies ofyour shareholder reports. Please note that not all financial intermediaries may offer this service. Your election to receive reports in paper will apply to all funds held with your financial intermediary. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive electronic delivery of shareholder reports and other communications by contactingyour financial intermediary. -

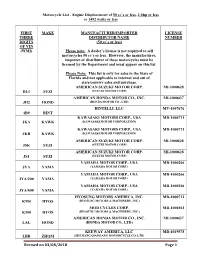

Motorcycle List - Engine Displacement of 50 Cc’S Or Less, 2 Bhp Or Less Or 1492 Watts Or Less

Motorcycle List - Engine Displacement of 50 cc’s or less, 2 bhp or less or 1492 watts or less FIRST MAKE MANUFACTURER/IMPORTER LICENSE THREE DISTRIBUTOR NAME NUMBER DIGITS (50 cc’s or less) OF VIN (WMI) Please note: A dealer’s license is not required to sell motorcycles 50 cc’s or less. However, the manufacturer, importer or distributor of these motorcycles must be licensed by the Department and must appear on this list. Please Note: This list is only for sales in the State of Florida and not applicable to internet and out of state/country sales and purchase. AMERICAN SUZUKI MOTOR CORP. MI-1000628 DL1 SUZI (SUZUKI MOTOR CORP) AMERICAN HONDA MOTOR CO., INC. MI-1000437 JH2 HOND (HONDA MOTOR CO., LTD) BINTELLI, LLC MV-1057676 4B9 BINT KAWASAKI MOTORS CORP., USA MD-1000711 JKA KAWK (KAWASAKI MOTOR CORPORATION) KAWASAKI MOTORS CORP., USA MD-1000711 JKB KAWK (KAWASAKI MOTOR CORPORATION) AMERICAN SUZUKI MOTOR CORP. MI-1000628 JSK SUZI (SUZUKI MOTOR CORP) AMERICAN SUZUKI MOTOR CORP. MI-1000628 JS1 SUZI (SUZUKI MOTOR CORP) YAMAHA MOTOR CORP., USA MD-1000266 JYA YAMA (YAMAHA MOTOR CORP.) YAMAHA MOTOR CORP., USA MD-1000266 JYA/200 YAMA (YAMAHA MOTOR CORP.) YAMAHA MOTOR CORP., USA MD-1000266 JYA/600 YAMA (YAMAHA MOTOR CORP.) HYOSUNG MOTORS AMERICA, INC. MD-1000712 KM4 HYOS (HYOSUNG MOTORS & MACHINERY, INC.) MOD CYCLES CORP. MD-1000361 KM4 HYOS (HYOSUNG MOTORS & MACHINERY, INC.) AMERICAN HONDA MOTOR CO., INC. MI-1000437 LAL HOND (HONDA MOTOR CO., LTD) KEEWAY AMERICA, LLC MD-1019578 LBB ZHQM (ZHEJIANG QIANJIANG MOTORCYCLE CO. LTD) Revised on 03/08/2018 Page 1 Motorcycle List - Engine Displacement of 50 cc’s or less, 2 bhp or less or 1492 watts or less FIRST MAKE MANUFACTURER/IMPORTER LICENSE THREE DISTRIBUTOR NAME NUMBER DIGITS (50 cc’s or less) OF VIN (WMI) Please note: A dealer’s license is not required to sell motorcycles 50 cc’s or less. -

Taiwan's Turning Tide

BUSINESS SWEDEN TAIWAN’S TURNING TIDE EXPLORING THE NEXT HORIZON FOR ASIA’S HIDDEN MANUFACTURING POWERHOUSE TAIWAN’S TURNINGFORTSÄTT TIDE SURFA EXPLORING THE NEXT HORIZON FOR ASIA’S PÅHIDDEN TILLVÄXTVÅGEN MANUFACTURING POWERHOUSE MARKNADSINSIKT APRIL 2017 Layout/grafik:Layout/Graphics Business Sweden Communications Foto:Business Sid Sweden 1, www.istockphoto.com. Marcom & Digitalisation Sid 3, Anders Thessing, www.thessing.se Tryck:Photos Åtta45, 2017 Page 1, 5, 8, iStock by Getty Images 2 | BUSINESS SWEDEN | TAIWAN’S TURNING TIDE EXECUTIVE SUMMARY Taiwan’s manufacturing competence and footprint is often underesti- mated. This island off the coast of China is where some of the world’s most high-tech goods are produced, and it is home to global OEMs and ODMs headquartered here. Taiwan is also a very important investor in both China and Southeast Asia. Given new realities on the ground in the APAC region – from trade barriers to shifting labour costs, digitalisation and increased demands on sustainability – Swedish suppliers have a new role to play in helping Tai- wanese manufacturers manage change. Sweden has more global manufacturing companies per capita than any other country in the world. These Swedish companies, and the sub-sup- VLAD MÅNSSON pliers that enabled them to thrive, are experts at providing innovative and Market Manager, Taiwan high-tech equipment, solutions and services where productivity and sus- tainability go hand in hand. The purpose of this report is to reflect on the impact of recent trade war developments on the APAC supply chain in relation to Taiwan’s man- ufacturing base in Asia. In addition, Business Sweden provides strategic recommendations for how Swedish companies can match their offering to the fast-changing needs of Taiwanese manufacturers.