Part B: Queensland Rail Declaration Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Section 3.7 – Local Area Frameworks

Draft Ipswich Planning Scheme 2019 Statement of Proposals 3.7 Local Area Frameworks 3.7.1 Preliminary (1) The Ipswich Local Government Area has been divided into thirty local area strategic planning units based on geographically identifiable communities of interest (areas with identifiable boundaries and within which there are broad land use and planning commonalities) to which individual Local Area Frameworks apply. (2) The thirty Local Area Frameworks provide a more detailed spatial expression of the policies included in the Whole of City Strategic Framework (refer to sections 3.1 to 3.6) for each of the local area strategic planning units by: (a) including a description of the geographic extent of the strategic planning unit to which the Local Area Framework applies; (b) identifying the Valuable Features in the area that are of significance and are to be protected; (c) identifying the most significant Development Constraints that impact on development in the area and that need to be considered and addressed in allocating precincts and for development assessment; (d) setting out the Growth Management outcomes that are to be delivered in the area; (e) identifying the key Infrastructure that needs to be delivered to support growth and development in the area; (f) showing the preferred use of land in the area by including each property in a land use precinct designation; and (g) where there are different development options (including for example building heights, lot sizes, dwelling densities or different land uses) for an area or individual -

Kuranda Scenic Railway Brochure

Kuranda Scenic Railway 2021 / 22 KURANDA Skyrail Kuranda RAILWAY STATION EXPERIENCE KURANDA SCENIC RAILWAY Terminal Port Douglas and Choose to experience your journey in either Heritage Class or Gold Class – both offering stunning views and old-time charm Koala Gardens Rainforestation Northern Beaches in refurbished wooden heritage carriages. As you reach Kuranda, spend your day strolling through the picturesque village and Australian Butterfly enjoy restaurants, shops, markets, and activities at your own pace, or combine your trip with a Kuranda day tour package. Sanctuary coral sea Birdworld Barron Skyrail Kuranda Markets Falls red Smithfield HERITAGE CLASS EXPERIENCE* GOLD CLASS EXPERIENCE* Stop peak Terminal Travel in the Kuranda Scenic Railway original timber carriages, Enjoy the comfort of Gold Class in carriages adorned in rob’s monument some of which are up to 100 years old, and experience the handcrafted Victorian inspired décor, club lounge style pioneering history as the train winds its way through World seating and personal onboard service. Heritage-listed rainforest. lake Your Gold Class journey includes: placid FRESHWATER Your Heritage Class journey includes: • Souvenir trip guide and gift pack falls lookout RAILWAY STATION Cairns • Souvenir trip guide available in nine languages • Audio commentary Airport • Audio commentary • Brief photographic stop at Barron Falls viewing platform • Brief photographic stop at Barron Falls viewing platform • Welcome drink^ and all-inclusive locally sourced appetisers stoney creek falls • Filtered -

Appendix 20 – Economic Impact Assessment

APPENDIX 20 – ECONOMIC IMPACT ASSESSMENT STANMORE IP SOUTH PTY LTD ISAAC DOWNS PROJECT ISAAC DOWNS PROJECT ECONOMIC IMPACT ASSESSMENT STANMORE IP SOUTH PTY LTD OCTOBER 2019 ISAAC DOWNS PROJECT – ECONOMIC IMPACT ASSESSMENT DOCUMENT CONTROL Job ID: J001178 Job Name: Isaac Downs Project – Economic Impact Assessment Client: Stanmore IP South Pty Ltd Client Contact: Richard Oldham Project Manager: Kieron Lacey Email: [email protected] Telephone: 07 3831 0577 Document Name: Isaac Downs Project EIA Final Last Saved: 3/10/2019 1:18 PM Version Date Reviewed Approved Draft v1 22/07/2019 KL KL Draft v2 13/08/2019 KL KL Draft v3 23/09/2019 KL KL Final 3/10/2019 KL KL Disclaimer: Whilst all care and diligence have been exercised in the preparation of this report, AEC Group Pty Ltd does not warrant the accuracy of the information contained within and accepts no liability for any loss or damage that may be suffered as a result of reliance on this information, whether or not there has been any error, omission or negligence on the part of AEC Group Pty Ltd or their employees. Any forecasts or projections used in the analysis can be affected by a number of unforeseen variables, and as such no warranty is given that a particular set of results will in fact be achieved. i ISAAC DOWNS PROJECT – ECONOMIC IMPACT ASSESSMENT EXECUTIVE SUMMARY BACKGROUND Stanmore Coal (Stanmore) is a mining company with interests in operational and prospective coal projects and mining assets within Queensland’s Bowen and Surat Basins. Stanmore IP South Pty Ltd (IP South), a wholly owned subsidiary of Stanmore Coal Ltd (Stanmore), is the proponent for the Isaac Downs Project (the Project). -

Off-Street Parking Off-Street C

134 the Ipswich City Centre, at schools, parks and sporting schools, at City Centre, the Ipswich do not have spaces The majority of these facilities. within specific parking areas however time restrictions as necessary. time limited are City Centre the Ipswich the by use for available generally are spaces These no charge. public and have and stations railway Hospital, the Ipswich at facilities and offices. facilities government such specific people, by use for dedicated are these others while within a shopping centre, as customers of these in some Parking public use. for available are charge park operators other car while is free, facilities their use. for fees Existing Situation Parking On-Street servicing Ipswich throughout parking is located On-street schools, areas, industrial and residential centres, activity facilities. and other community parks, sports centres or of charge free parking is provided on-street Typically, City Centre. in the Ipswich low-cost at parking car of 2,200 on-street formal is in the order There of which City Centre within the Ipswich marked spaces with time limits parking meters by managed are about 700 many also are one and nine hours. There between ranging are that City Centre within the Ipswich spaces kerbside metered. and/or time restricted marked, not formally parking is usually car on-street City Centre, In the Ipswich Friday, to 8am and 5pm, Monday between time limited 8am and 11:30am on a Saturday. and between time and/or marked spaces on-street also are There facilities the city near across on other roads restricted schools, (e.g. -

The Railway Technical Society of Australasia – the First Ten Years

The Railway Technical Society of Australasia The First Ten Years Philip Laird ENGINEERS AUSTRALIA RTSA The Railway Technical Society of Australasia The First Ten Years Philip Laird What may have been. An image from the 1990s of a future Speedrail Sydney - Canberra train at Sydney’s Central Station. Photo: Railway Digest/ARHSnsw. Three Vlocity trains standing at Southern Cross Station. These trains coupled with track upgrades as part of Victoria’s Regional Fast Rail program have seen a 30 per cent increase in patronage in their first full year of operation. Photo: Scott Martin 2008 Contents Introduction 4 RTSA Executive Chairman Ravi Ravitharan Acknowledgements Foreword 5 Hon Tim Fischer AC Section 1 Railways in Australasia 6 Section 2 The National Committee on Railway Engineering 11 Section 3 The Railway Technical Society of Australasia 17 3.1 The formation and early years 17 The Railway Technical Society of Australasia 3.2 Into the 21st century (2000 - 2004) 22 PO Box 6238, Kingston ACT 2604 3.3 Recent developments (2004 - 2008) 27 ABN 380 582 55 778 Section 4 Engineering and rail sector growth 34 4.1 The iron ore railways 34 © Copyright Philip Laird 4.2 Rail electrification in Queensland 36 and the Railway Technical Society of Australasia 2008 4.3 Queensland ‘s Mainline Upgrade 38 4.4 An East - West success story 40 Design and prepress by Ruby Graphics 4.5 The Australian Rail Track Corporation 42 Printed and bound by BPA Print Group 4.6 Perth’s urban rail renaissance 44 PO Box 110, Burwood VIC 3125 4.7 Rail in other capital cities 46 4.6 Trams and light rail 48 National Library of Australia Cataloguing-in-Publication entry 4.9 New railways in Australia 50 4.10 New Zealand railways 52 Title: The Railway Technical Society of Australasia : the first ten years / Philip Laird. -

Queensland Rail Holidays

QUEENSLAND RAIL HOLIDAYS 2021/22 QUEENSLAND RAIL HOLIDAYS Sunlover Holidays loves Queensland and you will too. Discover the beautiful coastline and marvel at spectacular outback landscapes as you traverse Queensland on an unforgettable rail holiday. We have combined a great range of accommodation and tour options with these iconic rail journeys to create your perfect holiday. Whether you’re planning a short break, a romantic getaway or the ultimate family adventure, Sunlover Holidays can tailor-make your dream holiday. Use this brochure for inspiration, then let our travel experts assist you to experience Queensland your way – happy travelling! Front cover image: Spirit of Queensland Image this page: Tilt Train Enjoy hearty Outback inspired cuisine and unparalleled service on the Spirit of the Outback CONTENTS Planning Your Rail Holiday 5 COASTAL RAIL 6 Tilt Train 7 Tilt Train Holiday Packages 8 Spirit of Queensland 10 Spirit of Queensland Holiday Packages 12 Kuranda Scenic Railway 17 GULF SAVANNAH RAIL 18 Lawn Hill Gorge, Queensland Gulflander 19 Gulf Savannah Holiday Packages 20 OUTBACK RAIL 23 Spirit of the Outback 24 Ultimate Outback Queensland Adventure – Fully Escorted 26 Spirit of the Outback Holiday Packages 28 Westlander 33 Westlander Holiday Packages 33 Inlander 34 Inlander Holiday Packages 34 Booking Conditions 35 Michaelmas Cay, Tropical North Queensland Valid 1 April 2021 – 31 March 2022 3 Take the track less travelled onboard the Inlander Thursday Island Weipa Cooktown Green Island Kuranda Cairns Karumba Normanton Tully -

Tropical North Queensland Tourism Opportunity Plan

Tropical North Queensland Tourism Opportunity Plan 2 0 1 0 - 2 0 2 0 DISCLAIMER – Tourism Tropical North Queensland and Tourism Queensland makes no claim as to the accuracy of the information contained in the Tropical North Queensland Tourism Opportunity Plan. The document is not a prospectus and the information provided is general in nature. The document should not be relied upon as the basis for financial and investment related decision. DISCLAIMER – STATE GOVERNMENT The Queensland Government makes no claim as to the accuracy of the information contained in the Tropical North Queensland Tourism Opportunity Plan. The document is not a prospectus and the information provided is general in nature. The document should not be relied upon as the basis for financial and investment related decisions. This document does not suggest or imply that the Queensland State Government or any other government, agency, organisation or person should be responsible for funding any projects or initiatives identified in this document. Executive Summary Dunk Island Purpose Catalyst Projects The purpose of this Tourism Opportunity Plan (TOP) is to Through the consultation and review process the following provide direction for the sustainable development of tourism in 18 catalyst projects have been identified for the Tropical North the Tropical North Queensland region. Queensland region. These projects are tourism investment or infrastructure projects of regional significance which are The TOP aims to: expected to act as a catalyst to a range of other investment, marketing and product development opportunities. < Identify new and upgraded tourism product that meets future visitor expectations and demands; 1 . Cairns Arts, Cultural and Events Precinct < Identify the need for new investment in infrastructure that 2 . -

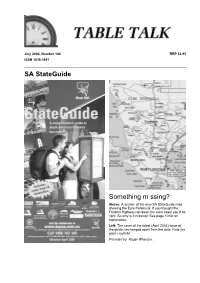

SA Stateguide Something M Ssing?

July 2004, Num ber 144 RRP $2.95 ISSN 1038-3697 SA StateGuide Something m ssing? Above: A section of the new SA StateGuide map showing the Eyre Peninsula. If you thought the Flinders Highway ran down the west coast you‘d be right. So why is it missing? See page 10 for an explanation. Left: The cover of the latest (April 2004) issue of the guide, unchanged apart from the date. Note the giant crayfish! Provided by Roger W heaton. Top Table Talk: • More on the new Sydney Cityrail timetable œ page 4 • Sydney Buses all timetables now TransitGraphics style œ page 7 • New SA StateGuide œ page 10 Table Talk is published monthly by the Australian Association Of Timetable Collectors Inc. [Registration No: A0043673H] as a journal covering recent news items. The AATTC also publishes The Times covering historic and general items. Editor: Duncan MacAuslan, 19 Ellen Street, Rozelle, NSW, 2039 œ (02) 9555 2667, dmacaus1@ bigpond.net.au Editorial Team : Graeme Cleak, Lourie Smit. Production: Geoff Lambert, Chris Noman and friends. Secretary: Steven Haby, PO Box 18049, Collins Street East, Melbourne, Vic, 8003 œ (03) 9898 0159 AATTC on the web: www.aattc.org.au, email: aattc@ ozemail.com.au Original material appearing in Table Talk may be reproduced in other publications, acknowledgement is required. Mem bership of the AATTC includes monthly copies of The Times , Table Talk, the distribution list of TTs and the twice-yearly auction catalogue. The membership fee is $45.00 pa. Membership enquiries should be directed to the Membership Officer: Dennis McLean, 53 Bargo Street, Arana Hills, Qld, 4054, - (07) 3351 6496. -

Public Transport in SEQ Options to Deliver Value and Innovation in Future South East

Council ol Mayors South E<1Rt Queensland Public Transport in SEQ Options to deliver value and innovation in future South East Queensland public transport infrastructure January 2012 5 w -(/) u c ::J u0 GHD was commissioned by the Council This report not only develops a list of of Mayors (SEQ) to provide advice on priority projects, but proposes a new innovative and value for money options for vision for SEQ Public Transport that puts investment in the public transport network the commuter at the heart of the system. in South East Queensland (SEQ). It is being released to encourage public discussion about options for investing in A key challenge for the investment public transport infrastructure across SEQ. program for public transport infrastructure in SEQ is how to meet the needs of The report does not represent an endorsed a growing region within the financially policy position of the Council of Mayors constrained fiscal environment now faced (SEQ). which will not consider the report by all levels of government. and public reactions to it until after the 2012 local government elections. The A key concern is whether the funds exist Council of Mayors (SEQ) will consider to proceed with the State Government's all options in developing its future input iconic $7700M Cross River Rail project. into the next iteration of the Queensland Some SEQ Councils are concerned Infrastructure Plan. that funding the project may delay other important projects in the region, while The Council of Mayors (SEQ) looks forward failure to deliver the project may stymie to further developing a constructive growth of the regional rail network. -

MIW METS Industry Capability and Supply Chain Study

MIW METS Industry Capability and Supply Chain Study Prepared for the MIW METS Export Hub by Lytton Advisory Pty Ltd September 2020 Acknowledgments Lytton Advisory acknowledges the assistance of Dean Kirkwood, MIW METS Export Hub Manager at RIN, and feedback from the Project Advisory Group. Disclaimer This Report has been prepared solely for Lytton Advisory’s client. While every effort has been made to ensure the accuracy of this document and any attachments, the uncertain nature of economic data, forecasting and analysis means that Lytton Advisory is unable to make any warranties concerning the information contained herein. Lytton Advisory, its employees and agents disclaim liability for any loss or damage that may arise as a consequence of any person relying on the information contained in this document and any attachments. © Lytton Advisory. All rights reserved. This work is copyright. The Copyright Act 1968 permits fair dealing for study, research, news reporting, criticism or review. Selected passages, tables or diagrams may be reproduced for such purposes provided acknowledgment of the source is included. Permission for any more extensive reproduction must be obtained from Lytton Advisory through the contact officer listed for this report. Lytton Advisory ABN 61 825 134 215 www.lyttonadvisory.com.au BRISBANE PO Box 5676 Manly Queensland 4179 E: [email protected] For information on this report please contact Craig Lawrence T: 0421 786 486 E: [email protected] Report prepared by (in alphabetical order): Hamish Bain, Nick Behrens, Sue Holz, Craig Lawrence and Gene Tunny, with research assistance provided by Norman Lee and Ben Scott Document Control Version Date Approved Approved By Description 1.0 30/06/2020 Craig Lawrence Draft report 2.0 05/08/2020 Craig Lawrence Draft final report 2.1 01/09/2020 Craig Lawrence Final report 2 Table of Contents Table of Contents ............................................................................................................ -

October 2017 Index

FIFTY-FIFTH PARLIAMENT FEBRUARY— OCTOBER 2017 INDEX Page Nos. Date Vol No. Page Nos. Date Vol No. 1 – 102 …. 14 February 2017 431 1789 – 1922 16 June 2017 432 103 – 170 …. 15 February 2017 431 1923 – 2066 8 August 2017 433 171 – 252 …. 16 February 2017 431 2067 – 2148 9 August 2017 433 253 – 356 …. 28 February 2017 431 2149 – 2230 10 August 2017 433 357 – 442 …. 1 March 2017 431 2231 – 2366 22 August 2017 433 443 – 554 …. 2 March 2017 431 2367 – 2448 23 August 2017 433 555 – 705 21 March 2017 431 2449 – 2572 24 August 2017 433 707 – 830 22 March 2017 431 2573 – 2688 5 September 2017 433 831 – 918 23 March 2017 431 2689 – 2778 6 September 2017 433 919 – 1022 9 May 2017 432 2779 – 2884 7 September 2017 433 1023 – 1122 10 May 2017 432 2885 – 2998 10 October 2017 434 1123 – 1206 11 May 2017 432 2999 – 3078 11 October 2017 434 1207 – 1320 23 May 2017 432 3079 – 3170 12 October 2017 434 1321 – 1412 24 May 2017 432 3171 – 3251 24 October 2017 434 1413 – 1500 25 May 2017 432 3253 – 3328 25 October 2017 434 1501 – 1563 13 June 2017 432 3329 – 3442 26 October 2017 434 1565 – 1636 14 June 2017 432 Index 434 1637 – 1788 15 June 2017 432 Index 14 February 2017 to 26 October 2017 1 A Inquiry into the Hendra virus (HeV) EquiVacc® vaccine— Final government response ................................................................. 927 Aboriginal and Torres Strait Islander Partnerships, Portfolio, Ministerial Interim government response ............................................................. 10 responsibilities .................................................................................... 2158 Report No. -

Temporary Exemptions Report October 2019 – September 2020

TEMPORARY EXEMPTIONS REPORT OCTOBER 2019 – SEPTEMBER 2020 Contents INTRODUCTION ......................................................................................................................... 2 Queensland Rail ............................................................................................................................... 2 Feedback Welcomed ........................................................................................................................ 2 PART A – EXEMPTIONS FROM THE TRANSPORT STANDARDS .......................................... 3 2.1 Access paths – Unhindered passage - rail premises and rail infrastructure .................. 3 2.1 Access paths – Unhindered passage - rail premises and rail infrastructure .................. 3 2.4 Access paths – Minimum unobstructed width - existing rail premises and existing rail infrastructure .............................................................................................................................. 4 2.6 Access paths – conveyances - existing rail conveyances ............................................... 4 2.6 Access paths – conveyances - existing rail conveyances ............................................... 5 2.6 Access paths – conveyances - existing rail conveyances ............................................... 5 4.2 Passing areas – Two-way access paths and aerobridges - existing rail platforms ....... 5 5.1 Resting points – When resting points must be provided - existing rail premises and existing rail infrastructure ........................................................................................................