Private Equity Growth Capital Council

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Leadership Newsletter Winter 2020 / 2021

T���������, M���� ��� T����������������� Leadership Newsletter Winter 2020 / 2021 GTCR Firm Update Since the firm’s inception in 1980, GTCR has Technology, Media and Tele- partnered with management teams in more communications than 200 investments to build and transform growth businesses. Over the last twenty years alone, GTCR has invested over $16 billion in approximately 100 platform acquisitions, 30+ 95+ PLATFORMS ADD-ONS including more than 65 companies that have been sold for aggregate enterprise value of over $ $50 billion and another 14 companies that have 25B+ been taken public with aggregate enterprise value PURCHASE of more than $34 billion. In November 2020, PRICE we closed GTCR Fund XIII, the firm’s largest fund to date, with $7.5 billion of limited partner capital commitments. This fund follows GTCR Fund Acquisition Activity Since 2000 XII, which we raised in 2017, with $5.25 billion As of January 15, 2021* of limited partner capital commitments. GTCR currently has 25 active portfolio companies; ten of these companies are within the Technology, Media and Telecommunications (“TMT”) industry. Page 1 / Continues on next page Technology, Media and Telecommunications Group Update Since 2000, GTCR has completed over 30 new platform investments and over 95 add-on acquisitions within the TMT industry, for a total of over 125 transactions with a combined purchase price of over $25 billion. During just the past year, we have realized several of these investments, selling three businesses and completing the partial sale of two additional companies, for a combined enterprise value of over $9 billion. Our TMT franchise includes ten active portfolio companies and one management start-up, which together have completed nearly 30 add-on acquisitions under our ownership, representing approximately $3 billion of GTCR invested capital. -

September 5, 2017 GTCR XII $150 Million September 5, 2017 Francisco Partners V $250 Million August 17, 2017 NGP Natural Resource

JOHN D. SKJERVEM PHONE 503-431-7900 CHIEF INVESTMENT OFFICER FAX 503-620-4732 INVESTMENT DIVISION STATE OF OREGON OFFICE OF THE STATE TREASURER 16290 SW UPPER BOONES FERRY ROAD TIGARD, OREGON 97224 OREGON INVESTMENT COUNCIL SEPTEMBER 20, 2017 MEETING MINUTES Members Present: Rukaiyah Adams, Tobias Read, John Russell, Rex Kim, Rick Miller and Steve Rodeman Staff Present: John Skjervem, Perrin Lim, David Randall, Deena Bothello, Karl Cheng, May Fanning, Michael Langdon, Jen Plett, Jen Peet, James Sinks, Michael Viteri, Tony Breault, Amanda Kingsbury, Austin Carmichael, Dana Millican, Ricardo Lopez, Jo Recht, Ben Mahon, Debra Day, Tom Lofton, Angela Schaffers, Priyanka Shukla, Roy Jackson, Garrett Cudahey, Mike Mueller, Steven Chang, Andy Coutu, Cassie Lallack, Dmitri Palamateer, Kim Olson, Aliese Jacobsen, William Hiles, Cassie Lallak, Amy Wojcicki Consultants Present: Tom Martin, Nic DiLoretta, David Fan, (TorreyCove); Allan Emkin, Christy Fields (PCA); Jim Callahan, Uvan Tseng, Janet Becker-Wold (Callan) Legal Counsel Present: Dee Carlson, Oregon Department of Justice The September 20th, 2017 OIC meeting was called to order at 8:59 am by Rukaiyah Adams, OIC Chair. I. 9: 01am Review and Approval of Minutes MOTION: Treasurer Read moved approval of the August 9th, 2017 OIC meeting minutes, and Mr. Kim seconded the motion which then passed by a 5/0 vote. II. 9:06 am Committee Reports and CIO Update Committee Reports: John Skjervem, OST Chief Investment Officer gave an update on the following committee actions taken since the August 9, 2017 OIC meeting: Private Equity Committee September 5, 2017 GTCR XII $150 million September 5, 2017 Francisco Partners V $250 million Alternatives Portfolio Committee August 17, 2017 NGP Natural Resources XII $250 million Opportunity Portfolio Committee None Real Estate Committee None OREGON INVESTMENT COUNCIL September 20, 2017 Meeting Summary Mr. -

Form 3 FORM 3 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

SEC Form 3 FORM 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 OMB APPROVAL INITIAL STATEMENT OF BENEFICIAL OWNERSHIP OF OMB Number: 3235-0104 Estimated average burden SECURITIES hours per response: 0.5 Filed pursuant to Section 16(a) of the Securities Exchange Act of 1934 or Section 30(h) of the Investment Company Act of 1940 1. Name and Address of Reporting Person* 2. Date of Event 3. Issuer Name and Ticker or Trading Symbol Requiring Statement EASTMAN KODAK CO [ EK ] Chen Herald Y (Month/Day/Year) 09/29/2009 (Last) (First) (Middle) 4. Relationship of Reporting Person(s) to Issuer 5. If Amendment, Date of Original Filed C/O KOHLBERG KRAVIS ROBERTS & (Check all applicable) (Month/Day/Year) CO. L.P. X Director 10% Owner Officer (give title Other (specify 2800 SAND HILL ROAD, SUITE 200 below) below) 6. Individual or Joint/Group Filing (Check Applicable Line) X Form filed by One Reporting Person (Street) MENLO Form filed by More than One CA 94025 Reporting Person PARK (City) (State) (Zip) Table I - Non-Derivative Securities Beneficially Owned 1. Title of Security (Instr. 4) 2. Amount of Securities 3. Ownership 4. Nature of Indirect Beneficial Ownership Beneficially Owned (Instr. 4) Form: Direct (D) (Instr. 5) or Indirect (I) (Instr. 5) Table II - Derivative Securities Beneficially Owned (e.g., puts, calls, warrants, options, convertible securities) 1. Title of Derivative Security (Instr. 4) 2. Date Exercisable and 3. Title and Amount of Securities 4. 5. 6. Nature of Indirect Expiration Date Underlying Derivative Security (Instr. 4) Conversion Ownership Beneficial Ownership (Month/Day/Year) or Exercise Form: (Instr. -

Private Equity Spotlight January 2007 / Volume 3 - Issue 1

Private Equity Spotlight January 2007 / Volume 3 - Issue 1 Welcome to the latest edition of Private Equity Spotlight, the monthly newsletter from Private Equity Intelligence, providing insights into private equity performance, investors and fundraising. Private Equity Spotlight combines information from our online products Performance Analyst, Investor Intelligence and Funds in Market. FEATURE ARTICLE page 01 INVESTOR SPOTLIGHT page 10 Overhang, what overhang? The favourable market and difficulty of getting allocations to With 2006’s $404 billion smashing all previous records for top quartile funds has led to increased LP interest in Asian private equity fund raising, some commentators are suggesting focused funds. We look at LPs investing in these funds. that there is now an ‘overhang’ of committed capital that the industry may struggle to invest. The facts suggest otherwise. • How do LPs perceive Asian focused funds? PERFORMANCE SPOTLIGHT page 05 • Who is making the most Growth in distributions to LPs and the rate of call-ups are significant investments? driving the fundraising market. Performance Spotlight looks at the trends. • Which types of investor are the most active? FUND RAISING page 06 After a record breaking year for fundraising in 2006, we • How much is being committed examine the latest news for venture and buyout funds, as well to the region? as examining the market for first-time fund vehicles. No. of Funds on INVESTOR NEWS page 12 US Europe ROW Road All the latest news on investors in private equity: Venture 202 97 83 382 • State of Wisconsin Investment Board posts high returns Buyout 100 48 36 184 boosted by its private equity portfolio Funds of Funds 65 47 12 124 • Somerset County Council Pension Fund seeks new fund of Other 129 31 42 202 funds manager • LACERA looks for new advisor Total 496 223 173 892 • Indiana PERF is set to issue real estate RFPs SUBSCRIPTIONS If you would like to receive Private Equity Spotlight each month • COPERA close to appointing new alternatives chief. -

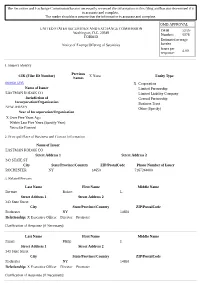

The Securities and Exchange Commission Has Not Necessarily Reviewed the Information in This Filing and Has Not Determined If It Is Accurate and Complete

The Securities and Exchange Commission has not necessarily reviewed the information in this filing and has not determined if it is accurate and complete. The reader should not assume that the information is accurate and complete. OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB 3235- Washington, D.C. 20549 Number: 0076 FORM D Estimated average Notice of Exempt Offering of Securities burden hours per 4.00 response: 1. Issuer's Identity Previous CIK (Filer ID Number) X None Entity Type Names 0000031235 X Corporation Name of Issuer Limited Partnership EASTMAN KODAK CO Limited Liability Company Jurisdiction of General Partnership Incorporation/Organization Business Trust NEW JERSEY Other (Specify) Year of Incorporation/Organization X Over Five Years Ago Within Last Five Years (Specify Year) Yet to Be Formed 2. Principal Place of Business and Contact Information Name of Issuer EASTMAN KODAK CO Street Address 1 Street Address 2 343 STATE ST City State/Province/Country ZIP/PostalCode Phone Number of Issuer ROCHESTER NY 14650 7167244000 3. Related Persons Last Name First Name Middle Name Berman Robert L. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Faraci Philip J. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Haag Joyce P. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Kruchten Brad W. -

TRS Contracted Investment Managers

TRS INVESTMENT RELATIONSHIPS AS OF DECEMBER 2020 Global Public Equity (Global Income continued) Acadian Asset Management NXT Capital Management AQR Capital Management Oaktree Capital Management Arrowstreet Capital Pacific Investment Management Company Axiom International Investors Pemberton Capital Advisors Dimensional Fund Advisors PGIM Emerald Advisers Proterra Investment Partners Grandeur Peak Global Advisors Riverstone Credit Partners JP Morgan Asset Management Solar Capital Partners LSV Asset Management Taplin, Canida & Habacht/BMO Northern Trust Investments Taurus Funds Management RhumbLine Advisers TCW Asset Management Company Strategic Global Advisors TerraCotta T. Rowe Price Associates Varde Partners Wasatch Advisors Real Assets Transition Managers Barings Real Estate Advisers The Blackstone Group Citigroup Global Markets Brookfield Asset Management Loop Capital The Carlyle Group Macquarie Capital CB Richard Ellis Northern Trust Investments Dyal Capital Penserra Exeter Property Group Fortress Investment Group Global Income Gaw Capital Partners AllianceBernstein Heitman Real Estate Investment Management Apollo Global Management INVESCO Real Estate Beach Point Capital Management LaSalle Investment Management Blantyre Capital Ltd. Lion Industrial Trust Cerberus Capital Management Lone Star Dignari Capital Partners LPC Realty Advisors Dolan McEniry Capital Management Macquarie Group Limited DoubleLine Capital Madison International Realty Edelweiss Niam Franklin Advisers Oak Street Real Estate Capital Garcia Hamilton & Associates -

Private Equity 05.23.12

This document is being provided for the exclusive use of SABRINA WILLMER at BLOOMBERG/ NEWSROOM: NEW YORK 05.23.12 Private Equity www.bloombergbriefs.com BRIEF NEWS, ANALYSIS AND COMMENTARY CVC Joins Firms Seeking Boom-Era Size Funds QUOTE OF THE WEEK BY SABRINA WILLMER CVC Capital Partners Ltd. hopes its next European buyout fund will nearly match its predecessor, a 10.75 billion euro ($13.6 billion) fund that closed in 2009, according to two “I think it would be helpful people familiar with the situation. That will make it one of the largest private equity funds if Putin stopped wandering currently seeking capital. One person said that CVC European Equity Partners VI LP will likely aim to raise 10 around bare-chested.” billion euros. The firm hasn’t yet sent out marketing materials. Two people said they expect it to do so — Janusz Heath, managing director of in the second half. Mary Zimmerman, an outside spokeswoman for CVC Capital, declined Capital Dynamics, speaking at the EMPEA to comment. conference on how Russia might help its reputation and attract more private equity The London-based firm would join only a few other firms that have closed or are try- investment. See page 4 ing to raise new funds of similar size to the mega funds raised during the buyout boom. Leonard Green & Partners’s sixth fund is expected to close shortly on more than $6 billion, more than the $5.3 billion its last fund closed on in 2007. Advent International MEETING TO WATCH Corp. is targeting 7 billion euros for its seventh fund, larger than its last fund, and War- burg Pincus LLC has a $12 billion target on Warburg Pincus Private Equity XI LP, the NEW JERSEY STATE INVESTMENT same goal as its predecessor. -

WARSAW, Poland & BUDAPEST, Hungary

WARSAW, Poland & BUDAPEST, Hungary--(BUSINESS WIRE)-- MCI Group, a leading Central European private equity firm with headquarters in Warsaw (Poland), announced today that their Fund MCI.EuroVentures is selling a portion of its shares in Netrisk, the leading online insurance brokerage in Hungary, to global growth private equity firm TA Associates for EUR 55 million (PLN 235 million). As a result of the partial exit, MCI.EuroVentures (buyout fund of MCI Group) has realized a return on investment of 3.0x CoC and 73% IRR. ● MCI Group, one of the leading investors in the Central and Eastern European (EU-CEE) region, remains an important investor in Netrisk and is retaining a 23.7% stake in the company to actively help build value for the insurtech leader on a larger, regional scale. ● TA Associates and Netrisk’s management will hold 75% and 1.3% of the company’s shares, respectively. ● Minority shareholder AMC Capital IV S.c.Sp., advised by Mezzanine Management, is selling all of its shares in Netrisk. ● TA Associates is one of the most experienced global growth private equity firms, having raised USD 33.5 billion in capital since its founding in 1968, and has a long history of investing in companies focused on the digital economy. ● In addition to sustained organic growth, Netrisk will consider acquisition opportunities in CEE, including online, multi-channel and offline companies involved in the distribution of personal- line insurance products. MCI.EuroVentures invested in Netrisk in 2017. The non-life insurance market in Hungary is estimated at USD 1.8 billion, of which the online channel accounts for more than 20%, which is significantly more than other countries in the region, including Poland. -

RRP Sector Assessment

OrbiMed Asia Partners III, LP Fund (RRP REG 51072) OWNERSHIP, MANAGEMENT, AND GOVERNANCE A. The Fund Structure 1. The Asian Development Bank (ADB) proposes to invest in OrbiMed Asia Partners III, LP Fund (OAP III), which is a Cayman Islands exempted limited partnership seeking to raise up to $500 million in capital commitments. It is managed by OrbiMed Asia GP III, LP (the general partner), a Cayman Islands exempted limited partnership. The sole limited partner of the general partner is OrbiMed Advisors III Limited, a Cayman Islands exempted company. OrbiMed Advisors LLC (the investment advisor), a registered investment advisor with the United States (US) Securities and Exchange Commission, will provide investment advisory services to OAP III. This structure is illustrated in the figure below. Table 1 shows the ultimate beneficial owners (UBOs) of the general partner and the investment advisor. Table 1: Ultimate Beneficial Owners of the General Partner and the Investment Advisor (ownership stake, %) Name Investment Advisor General Partner Sven H. Borho (~10–25%) (~8%) Alexander M. Cooper (~8%) Carl L. Gordon (~10–25%) (~8%) (also Director) Geoffrey C. Hsu (<5%) (~8%) Samuel D. Isaly (~50–75%) (~8%) W. Carter Neild (<5%) (~8%) (also Director) Jonathan T. Silverstein (~5–10%) (~8%) (also Director) Sunny Sharma (~8%) (also Officer) Evan D. Sotiriou (~8%) David G. Wang (~8%) (also Officer) Jonathan Wang (~8%) (also Officer) Sam Block III (~8%) Source: OrbiMed Group. 2 2. Investors. The fund held a first closing of approximately $233.5 million on 1 March 2017, and a second closing of approximately $137.6 million on 26 April 2017. -

Stepstone Atlantic Fund, L.P

StepStone Atlantic Fund, L.P. Private Equity and Infrastructure Quarterly Monitoring Report For the period ending December 31, 2020 Report Prepared For: Important Information This document is meant only to provide a broad overview for discussion purposes. All information provided here is subject to change. This document is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security, or as an offer to provide advisory or other services by StepStone Group LP, StepStone Group Real Assets LP, StepStone Group Real Estate LP, StepStone Conversus LLC, Swiss Capital Alternative Investments AG and StepStone Group Europe Alternative Investments Limited or their subsidiaries or affiliates (collectively, “StepStone”) in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this document should not be construed as financial or investment advice on any subject matter. StepStone expressly disclaims all liability in respect to actions taken based on any or all of the information in this document. This document is confidential and solely for the use of StepStone and the existing and potential clients of StepStone to whom it has been delivered, where permitted. By accepting delivery of this presentation, each recipient undertakes not to reproduce or distribute this presentation in whole or in part, nor to disclose any of its contents (except to its professional advisors), without the prior written consent of StepStone. While some information used in the presentation has been obtained from various published and unpublished sources considered to be reliable, StepStone does not guarantee its accuracy or completeness and accepts no liability for any direct or consequential losses arising from its use. -

Understanding Private Equity. What Is Private Equity? EXAMPLES of PRIVATELY HELD COMPANIES

Understanding private equity. What is private equity? EXAMPLES OF PRIVATELY HELD COMPANIES: A private equity investor is an individual or entity that invests capital into a private company (i.e. firms not traded on a public exchange) in exchange for equity interest in that business. In the US, there are approximately 18,000 publicly traded companies, and more than 300,000 privately held companies. WHO MIGHT SEEK A PRIVATE EQUITY INVESTOR AS A SOURCE OF CAPITAL? • Companies looking to fund a capital need that is beyond traditional bank financing • Owners considering a partial or complete sale of their business • Managers looking to buy a business Private equity strategies. EXAMPLES OF PRIVATE EQUITY FIRMS: MOST PRIVATE EQUITY INVESTORS WILL LIMIT THEIR INVESTMENTS TO ONE OR TWO OF THE FOLLOWING STRATEGIES: • Angel investing • Growth capital • Venture capital • Distressed investments • Leveraged buyouts (LBO) • Mezzanine capital Sources of capital for PE funds. THERE ARE TWO TYPES OF PRIVATE EQUITY FIRMS: • Firms with a dedicated fund, with the majority of the capital sourced from institutional investors (i.e. pension funds, banks, endowments, etc.) and accredited investors (i.e. high net worth individual investors) • Firms that raise capital from investors on a per-deal basis (pledge funds) INVESTMENT DURATION AND RETURNS. • Typical investment period is 3−10 years, after which capital is distributed to investors • Rates of return are higher than public market returns, typically 15−30%, depending on the strategy HISTORICAL S&P 500 RETURNS S&P 500 Returns Average Source: Standard & Poor’s LCD Private equity fund structure. PRIVATE EQUITY FIRM LIMITED PARTNERS (Investors) (Public pension funds, corporate pension funds, insurance companies, high net worth individuals, family offices, endowments, banks, foundations, funds-of-funds, etc.) Management Company General Partner Fund Ownership Fund Investment Management PRIVATE EQUITY FUND (Limited Partnership) Fund’s Ownership of Portfolio Investments Etc. -

PEI Investor Relations, Marketing & Communications Forum 2019

June 19-20 | Convene, 730 Third Ave | New York Attendee list A.P. Moller Capital Bain Capital C-Bridge Capital Partners FTV Capital ACME Capital Banner Real Estate Group CCMP Capital Advisors Further Capital Partners Actis Barings Centerbridge Partners GCM Grosvenor Advent International Basis Investment Group Cerberus Capital Management General Atlantic AE Industrial Partners Battery Ventures Charlesbank Capital Partners General Catalyst Partners AEA Investors BBH Capital Partners The Chauncey F. Lufkin III Gennx360 AEW Capital Management BC Partners Foundation Genstar Capital AIMA The Beach Company The City of New York, Finance Global Infrastructure Partners Alcentra Berkshire Partners Civitas Capital Grain Management Alcion Ventures Bernhard Capital Partners Coller Capital Gryphon Investors Allianz Capital Partners Bicknell Family Holding Cornell Capital GTCR Altor Equity Partners Company Court Square Capital Partners Halstatt American Securities Bison Crescent Capital Group Hamilton Lane AMP Capital BKM Capital Partners CRV Hammes Angelo Gordon Blackstone Cypress Real Estate Advisors Hammond, Kennedy, Whitney Antares Capital Blue Heron Asset Managment Denham Capital & Co Apollo Global Management Blue Water Energy Duff & Phelps Hancock Capital Management ARC Financial Corp Bridge Investment Group Dyal Capital Partners Harvard Management Company ArcLight Capital Partners BroadVail Capital Edelman HCI Equity Partners Argosy Capital Brook Venture Partners EnCap Investments HGGC Arroyo Energy Investment Brookfield Asset Management EQT Partners