Securities and Exchange Commission Form 8-K

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prom 2018 Event Store List 1.17.18

State City Mall/Shopping Center Name Address AK Anchorage 5th Avenue Mall-Sur 406 W 5th Ave AL Birmingham Tutwiler Farm 5060 Pinnacle Sq AL Dothan Wiregrass Commons 900 Commons Dr Ste 900 AL Hoover Riverchase Galleria 2300 Riverchase Galleria AL Mobile Bel Air Mall 3400 Bell Air Mall AL Montgomery Eastdale Mall 1236 Eastdale Mall AL Prattville High Point Town Ctr 550 Pinnacle Pl AL Spanish Fort Spanish Fort Twn Ctr 22500 Town Center Ave AL Tuscaloosa University Mall 1701 Macfarland Blvd E AR Fayetteville Nw Arkansas Mall 4201 N Shiloh Dr AR Fort Smith Central Mall 5111 Rogers Ave AR Jonesboro Mall @ Turtle Creek 3000 E Highland Dr Ste 516 AR North Little Rock Mc Cain Shopg Cntr 3929 Mccain Blvd Ste 500 AR Rogers Pinnacle Hlls Promde 2202 Bellview Rd AR Russellville Valley Park Center 3057 E Main AZ Casa Grande Promnde@ Casa Grande 1041 N Promenade Pkwy AZ Flagstaff Flagstaff Mall 4600 N Us Hwy 89 AZ Glendale Arrowhead Towne Center 7750 W Arrowhead Towne Center AZ Goodyear Palm Valley Cornerst 13333 W Mcdowell Rd AZ Lake Havasu City Shops @ Lake Havasu 5651 Hwy 95 N AZ Mesa Superst'N Springs Ml 6525 E Southern Ave AZ Phoenix Paradise Valley Mall 4510 E Cactus Rd AZ Tucson Tucson Mall 4530 N Oracle Rd AZ Tucson El Con Shpg Cntr 3501 E Broadway AZ Tucson Tucson Spectrum 5265 S Calle Santa Cruz AZ Yuma Yuma Palms S/C 1375 S Yuma Palms Pkwy CA Antioch Orchard @Slatten Rch 4951 Slatten Ranch Rd CA Arcadia Westfld Santa Anita 400 S Baldwin Ave CA Bakersfield Valley Plaza 2501 Ming Ave CA Brea Brea Mall 400 Brea Mall CA Carlsbad Shoppes At Carlsbad -

Copy of Chipotle Restuarant List

Restaurant Name Restaurant City State Zipcode Restaurant Phone Address Addison - Lake 53 - 1819 1078 N. Rohlwing Rd Addison IL 60101 630-282-7220 Algonquin - 399 412 N. Randall Road Algonquin IL 60102 847-458-1030 Arlington Heights - 131 338 E. Rand Road Arlington Heights IL 60004 847-392-8328 Fox Valley - 624 848 N. Route 59, Suite 106 Aurora IL 60504 630-851-3271 Aurora Orchard - 1462 1480 N Orchard Road, Suite 114-116 Aurora IL 60506 630-723-5004 Aurora Kirk & Butterfield - 1888 2902 Kirk Road, Unit 100 Aurora IL 60504 630-429-9437 Berwyn - 1753 7140 West Cermak Road Berwyn IL 60402 708-303-5049 Bloomingdale - 858 396 West Army Trail Rd. Bloomingdale IL 60108 630-893-2108 Fairfield and Lake Street - 2884 170 E Lake Street Suite C Bloomingdale IL 60108 630-529-5128 Bloomington Veterans Prkwy - 305 N. Veterans Pkwy., Suite 101 Bloomington IL 61704 309-661-7850 1035 Bolingbrook - 529 274 S. Weber Road Bolingbrook IL 60490 630-759-9359 Bradley - 2609 1601 Illinois State Route 50 Bradley IL 60914 815-932-3225 Bridgeview 87th & Harlem - 3047 8813 S. Harlem Ave Bridgeview IL 60455 708-598-1555 Champaign - 771 528 East Green Street, STE 101 Champaign IL 61820 217-344-0466 Champaign Prospect - 1837 903 West Anthony Drive #A Champaign IL 61820 217-398-0997 Broadway & Belmont - 36 3181 N. Broadway Chicago IL 60657 773-525-5250 Clybourn Commons - 42 2000 N. Clybourn Ave. Chicago IL 60614 773-935-5710 Orchard - 52 2256-58 N. Orchard Ave. Chicago IL 60614 773-935-6744 Jackson - 88 10 E. -

Complete Annual Report

2 Comprehensive Annual Financial Report For the Year Ended June 30, 2007 County of San Diego CONTENTS Introductory Section Letter of Transmittal ................................................................................... 7 GFOA Certificate of Achievement ........................................................ 21 Board of Supervisors................................................................................ 22 Organizational Chart .............................................................................. 23 Other Elected and Appointed Officials................................................. 25 Financial Section Independent Auditor’s Report................................................................ 27 Management’s Discussion and Analysis ........................................29 Basic Financial Statements: .............................................................47 Government-wide Financial Statements: Statement of Net Assets ...........................................................................................48 Statement of Activities .............................................................................................49 Fund Financial Statements: Balance Sheet Governmental Funds .....................................................................51 Reconciliation of the Governmental Funds Balance Sheet to the Government-wide Statement of Net Assets .....................................................52 Statement of Revenues, Expenditures, and Changes in Fund Balances - Governmental Funds...........................................................................................53 -

Simon Property Group, Inc

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2007 SIMON PROPERTY GROUP, INC. (Exact name of registrant as specified in its charter) Delaware 001-14469 04-6268599 (State or other jurisdiction of (Commission File No.) (I.R.S. Employer incorporation or organization) Identification No.) 225 West Washington Street Indianapolis, Indiana 46204 (Address of principal executive offices) (ZIP Code) (317) 636-1600 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12 (b) of the Act: Name of each exchange Title of each class on which registered Common stock, $0.0001 par value New York Stock Exchange 6% Series I Convertible Perpetual Preferred Stock, $0.0001 par value New York Stock Exchange 83⁄8% Series J Cumulative Redeemable Preferred Stock, $0.0001 par value New York Stock Exchange Securities registered pursuant to Section 12 (g) of the Act: None Indicate by check mark if the Registrant is a well-known seasoned issuer (as defined in Rule 405 of the Securities Act). Yes ፤ No អ Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes អ No ፤ Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

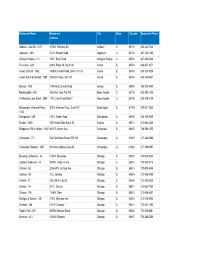

State Storeno Mall Name Store Type 2015 Sales 2014 Sales Variance

Variance State StoreNo Mall Name Store Type 2015 Sales 2014 Sales Inc/(Dec) % Inc/(Dec) TX 83 NorthPark Center In-Line 1,472,766.00 1,363,984.00 108,782.00 7.98% SC 135 Coastal Grand Mall In-Line 1,151,631.67 1,113,877.31 37,754.36 3.39% TX 20 Barton Creek Square Shopping Center In-Line 1,096,658.41 1,083,499.33 13,159.08 1.21% CA 8 Westfield Valencia Town Center In-Line 1,071,022.26 1,087,795.83 (16,773.57) -1.54% TX 19 Baybrook Mall In-Line 1,025,120.43 1,055,953.79 (30,833.36) -2.92% AZ 125 Park Place Mall In-Line 950,664.23 946,527.12 4,137.11 0.44% TN 48 Wolfchase Galleria In-Line 923,588.32 867,012.22 56,576.10 6.53% TX 55 Stonebriar Centre In-Line 876,800.55 815,558.37 61,242.18 7.51% CA 126 Westfield Galleria at Roseville In-Line 869,168.30 754,757.11 114,411.19 15.16% CO 167 Cherry Creek Shopping Center In-Line 868,959.85 835,887.13 33,072.72 3.96% CO 61 Park Meadows Center In-Line 831,157.07 800,397.91 30,759.16 3.84% AZ 28 Arrowhead Towne Center In-Line 771,406.64 656,746.72 114,659.92 17.46% CA 39 Westfield University Towne Center In-Line 738,949.33 573,464.00 165,485.33 28.86% CA 35 The Promenade at Temecula In-Line 733,268.27 666,557.65 66,710.62 10.01% KY 78 Mall St. -

Stay Play Shop

PALM BEACH WEST PALM PALM JUPITER LAKE WELLINGTON BOYNTON DELRAY BOCA GARDENS BEACH BEACH SHOPPING WORTH SHOPPING BEACH BEACH RATON The Gardens Mall PGA Commons Clematis District Palm Beach Outlets Worth Avenue Harbourside Place Downtown Lake Worth The Mall at Renaissance Commons, Atlantic Avenue Mizner Park Town Center at Boca Raton This experience starts with an exquisite two- Peruse and shop in a setting reminiscent Delicate historic buildings stand side- A tremendous mix of brand favorites sure This open-air waterside location with Colorful, artistic, and bohemian to say the Wellington Green Boynton Beach Boulevard The charming ambience of this café-style An enchanting destination with a Stroll a wonderful plaza, tour a fne art An outstanding mix of trendy, elite shops story venue flled with fountains, sculptured of a European village, as outdoor artwork, by-side modern ones, overlooking the to excite bargain hunters and shopaholics sophisticated, inimitable style and grace. This a laid-back, tropical feel is just right for least. The landscape along its two main Wellington is an international destination The welcoming design, stunning streetscape is enhanced by brick-paved exhibit at the Boca Museum of Art, or enjoy along with favorite mall stores. A place artwork, and natural brightness from the iron staircases, fountains, fowers, and high-energy atmosphere produced by alike. Additionally, Marketplace at the is one of the most beautiful shopping venues shopping its national and local stores, streets, Lake and Lucerne Avenues, is for equestrian sports, with a matchless architecture, and inviting scenery make sidewalks lined with oak and palm trees. a concert at the Amphitheater – and shop. -

Community Guide & Business Directory

2019-2020 Community Guide & Business Directory DISCOVER LINCOLNWOOD! LIVE • PLAY • SHOP • DINE Proud Mercedes-Benz Dealer for Six Decades Pictured Left to Right: George Loeber, Executive Vice-President; Michael Loeber, President. PROUDL Y SER experience MA VING THE C TTERS! OMMUNITY F OR O VER 25 YEARS Proud Mercedes-Benz Dealer for Six Decades DISCOVER a senior living community you’ll love today and all your tomorrows. Pictured Left to Right: George Loeber, Executive Vice-President; Michael Loeber, President. Open the door to luxury senior living. 847-686-2888 Independent Living | Assisted Living | Skillied Nursing & Rehabilitation | Memory Care AL License #52605 | 7000 North McCormick Boulevard | Lincolnwood, IL 60712 WWW.SENIORLIFESTYLE.COM Welcome Dear Lincolnwood Chamber 4433 W. TOUHY AVE. LINCOLNWOOD, ILLINOIS 60712 Partners & Friends: We are pleased to present the new edition of the Lincolnwood WHAT’S INSIDE THE GUIDE Chamber of Commerce 2019-2020 Community Resource Guide. This complimentary, hand-delivered publication connects you to WELCOME 4 the center of the Village of Lincolnwood. FROM THE OFFICE OF THE 6 MAYOR At your fingertips is contact information for various business ABOUT THE CHAMBER & CHAMBER BOARD members of the Chamber, as well as easy access to useful OF DIRECTORS 8 information assembled from numerous community HELPFUL NUMBERS 10 stakeholders including the Chamber of Commerce, the Village of Lincolnwood, the Lincolnwood Public Library, Oakton LINCOLNWOOD IS ABOUT LOCATION 12 Community College, School District 74 and Niles Township High HISTORY 14 School District 219. PARKS & RECREATION 16 More than 5,000 copies are delivered door-to-door with an additional 1,000 copies distributed throughout the year via LINCOLNWOOD SCHOOL DISTRICT 74 18–19 Village Hall new resident packages, at member businesses LINCOLNWOOD MAP 20–21 and at numerous Chamber-sponsored events. -

271 Filed 01/06/21 Page 1 of 5

Case 20-13076-BLS Doc 271 Filed 01/06/21 Page 1 of 5 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE ------------------------------------------------------------ x : In re: : Chapter 11 : FRANCESCA’S HOLDINGS CORPORATION, Case No. 20-13076 (BLS) 1 : et al., : : Debtors. Jointly Administered : : Re: D.I. 45, 266 ------------------------------------------------------------ x NOTICE OF POTENTIAL ASSUMPTION AND ASSIGNMENT OF EXECUTORY CONTRACTS OR UNEXPIRED LEASES AND CURE AMOUNTS PLEASE TAKE NOTICE THAT: 1. The above-captioned debtors (collectively, the “Debtors”) each filed a voluntary petition for relief under chapter 11 of title 11 of the United States Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the District of Delaware (the “Court”) on December 3, 2020. 2. On December 4, 2020, the Debtors filed the Motion of Debtors for Entry of Orders (I)(A) Approving Bidding Procedures for Sale of Substantially All of the Debtors’ Assets, (B) Approving Process for Designation of Stalking Horse Bidder and Provision of Bid Protections, (C) Scheduling Auction for, and Hearing to Approve, Sale of Substantially All of the Debtors’ Assets, (D) Approving Form and Manner of Notices of Sale, Auction and Sale Hearing, (E) Approving Assumption and Assignment Procedures and (F) Granting Related Relief and (II)(A) Approving Sale of Substantially All of the Debtors’ Assets Free and Clear of All Liens, Claims, Interests and Encumbrances, (B) Approving Assumption and Assignment of Executory Contracts and Unexpired Leases -

In the United States Bankruptcy Court for the District of Delaware

Case 20-13076-BLS Doc 961 Filed 07/15/21 Page 1 of 27 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE ------------------------------------------------------------ x In re: : Chapter 11 : 1 FHC HOLDINGS CORPORATION, et al., : Case No. 20-13076 (BLS) : Debtors. : Jointly Administered ------------------------------------------------------------ x CERTIFICATION OF STRETTO REGARDING TABULATION OF VOTES IN CONNECTION WITH THE DEBTORS’ FIRST AMENDED COMBINED DISCLOSURE STATEMENT AND CHAPTER 11 PLAN OF LIQUIDATION I, Alexa T. Westmoreland, depose and say under the penalty of perjury: 1. I am a Director at Stretto, which has offices located at 410 Exchange, Suite 100, Irvine, CA 92602. I am over the age of eighteen years and neither I nor Stretto is a party to these proceedings. I am duly authorized to submit this certification on behalf of Stretto (this “Certification”). Except as otherwise indicated, all matters set forth herein are based upon my personal knowledge, and, if called as a witness, I could and would testify competently thereto. 2. I submit this Certification in connection with the tabulation of votes to accept or reject the Debtors’ First Amended Combined Disclosure Statement and Chapter 11 Plan of Liquidation filed in the above-captioned cases [D.I. 737] (as amended, supplemented, or modified from time to time, the “Plan”).2 1 The Debtors in these cases, along with the last four digits of each Debtor’s federal tax identification number, are FHC Holdings Corporation (f/k/a Francesca’s Holdings Corporation) (4704), FHC LLC (f/k/a Francesca’s LLC) (2500), FHC Collections, Inc. (f/k/a Francesca’s Collections, Inc.) (4665), and FHC Services Corporation (f/k/a Francesca’s Services Corporation) (5988). -

2019 Property Portfolio Simon Malls®

The Shops at Clearfork Denver Premium Outlets® The Colonnade Outlets at Sawgrass Mills® 2019 PROPERTY PORTFOLIO SIMON MALLS® LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME 2 THE SIMON EXPERIENCE WHERE BRANDS & COMMUNITIES COME TOGETHER SIMON MALLS® LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME 2 ABOUT SIMON Simon® is a global leader in retail real estate ownership, management, and development and an S&P 100 company (Simon Property Group, NYSE:SPG). Our industry-leading retail properties and investments across North America, Europe, and Asia provide shopping experiences for millions of consumers every day and generate billions in annual sales. For more information, visit simon.com. · Information as of 12/16/2019 3 SIMON MALLS® LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME More than real estate, we are a company of experiences. For our guests, we provide distinctive shopping, dining, and entertainment. For our retailers, we offer the unique opportunity to thrive in the best retail real estate in the best markets. From new projects and redevelopments to acquisitions and mergers, we are continuously evaluating our portfolio to enhance the Simon experience—places where people choose to shop and retailers want to be. 4 LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME WE DELIVER: SCALE A global leader in the ownership of premier shopping, dining, entertainment, and mixed-use destinations, including Simon Malls®, Simon Premium Outlets®, and The Mills® QUALITY Iconic, irreplaceable properties in great locations INVESTMENT Active portfolio management increases productivity and returns GROWTH Core business and strategic acquisitions drive performance EXPERIENCE Decades of expertise in development, ownership, and management That’s the advantage of leasing with Simon. -

Citadel Vs Clemson (9/16/1978)

Clemson University TigerPrints Football Programs Programs 1978 Citadel vs Clemson (9/16/1978) Clemson University Follow this and additional works at: https://tigerprints.clemson.edu/fball_prgms Materials in this collection may be protected by copyright law (Title 17, U.S. code). Use of these materials beyond the exceptions provided for in the Fair Use and Educational Use clauses of the U.S. Copyright Law may violate federal law. For additional rights information, please contact Kirstin O'Keefe (kokeefe [at] clemson [dot] edu) For additional information about the collections, please contact the Special Collections and Archives by phone at 864.656.3031 or via email at cuscl [at] clemson [dot] edu Recommended Citation University, Clemson, "Citadel vs Clemson (9/16/1978)" (1978). Football Programs. 131. https://tigerprints.clemson.edu/fball_prgms/131 This Book is brought to you for free and open access by the Programs at TigerPrints. It has been accepted for inclusion in Football Programs by an authorized administrator of TigerPrints. For more information, please contact [email protected]. OFFICIAL PROGRAM • MEMORIAL STADIUM • SEPTEMBER 16, 1978 vs THE CITADEL Eastern Distribution is people who know how to handle things People who can get anything at all from one place to another on the right timetable, and in perfect condition. Murphy MacLean, Vice President/Florida, and Sherry Herren, Vice President/S. C. Eastern Distribution Office Manager Dianne Moore, Sales Representative Sherry Turner, and Controller Carrol Garrett Yes, the Eastern people on Harold Segars' Greenville, S. C, and Jacksonville, Fla., distribution team get things done, whether they're arranging the same-day movement of something you want out in a hurry, or consolidating loads to save you money through lower rates. -

Discover the Palm Beaches' VIP Media Pass Allows Qualified

Discover The Palm Beaches’ VIP Media Pass allows qualified journalists and digital influencers the opportunity to visit the following attractions and activities at a reduced or complimentary rate. In order to receive a VIP Media Pass, media and influencers are required to complete the Media Visit Request Form with their request. VIP Media Passes are provided in exchange for confirmed editorial and/or social media coverage. These offers are subject to change based upon availability and at the discretion of the hosting party. You are also encouraged to visit the destination’s not-for-profit attractions, shopping locations, parks and of course, the 47 miles of pristine beaches. **Please note, out of fairness to Discover The Palm Beaches’ hosting partners, the Pass may not be used more than once, per attraction, during the requested time frame. All activities must be coordinated in advance of your visit to The Palm Beaches. Should you have any questions, the Discover The Palm Beaches Public Relations department can be reached at [email protected]. While in The Palm Beaches, we encourage you to engage with us by using the hashtag #ThePalmBeaches and connecting with us on the following handles, as you explore the destination’s offerings. Facebook: facebook.com/PalmBeachesFL Facebook (Brazil): facebook.com/DescubraPalmBeaches/ Facebook (UK): facebook.com/DTPB.UK/ Twitter and Instagram: @PalmBeachesFL Instagram (Brazil): @PalmBeachesBR YouTube: youtube.com/PalmBeachCountyFL Pinterest: pinterest.com/ThePalmBeaches VIP Media Pass Participating Locations Ann Norton Sculpture Gardens Complimentary admission for the Media Passholder and one guest at Ann Norton Sculpture Gardens. **Note, Ann Norton Sculpture Gardens will be available by appointment only from July 3 through October 2, 2019.