Durham Research Online

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tishman Speyer and Bellco Capital Launch Breakthrough Properties, a First-Of-Its-Kind Global Life Sciences Real Estate Platform

FROM: TISHMAN SPEYER Rubenstein Communications, Inc. – Public Relations Contact: Steven Rubenstein (212) 843-8043 Rick Matthews (212) 843-8267 BELLCO CAPITAL Contact: Leah Couvelier (213) 304-9333 Tishman Speyer and Bellco Capital Launch Breakthrough Properties, a First-of-Its-Kind Global Life Sciences Real Estate Platform Unique Collaboration Combines First-Hand Biotechnology Entrepreneurship and Scientific Research Experience with Unsurpassed Commercial Real Estate Development Capabilities Newly-Formed Joint Venture Acquires its First Development Site, in Boston’s Seaport District New York/Los Angeles/Boston – July 16, 2019 - Tishman Speyer, one of the world’s leading developers, owners, operators and asset managers of first-class real estate, and Bellco Capital (“Bellco”), an investment firm founded by biotechnology entrepreneurs Drs. Rebecka and Arie Belldegrun, have formed Breakthrough Properties (“Breakthrough”). The new company will acquire, develop and operate life science properties in leading technology centers around the world to support scientific innovation across biotechnology, agriculture and nutrition. Board Co-Chairs for Breakthrough are Bellco’s Arie Belldegrun and Tishman Speyer President & CEO Rob Speyer. Dan Belldegrun, a long-term member of Tishman Speyer’s Acquisitions and Development team, has been appointed Chief Executive Officer. The partners also announced today that Breakthrough has acquired its first property, taking advantage of Tishman Speyer’s deep roots and expertise as a commercial real estate developer and operator in the Boston market. The development site is strategically located by the Red Line on a one-acre parcel along the A Street corridor in Boston’s Seaport District and comes with 250,000 square feet of development rights. Completion of the project is anticipated in 2021. -

New York's Iconic Chrysler Building up for Sale 9 January 2019

New York's iconic Chrysler Building up for sale 9 January 2019 intersection of 42nd Street and Lexington Avenue. The announcement comes at a difficult time for the New York real estate market, especially in Manhattan. Development of the Hudson Yards neighborhood, on Manhattan's West Side, will soon be complete, with more than 1.6 million square meters of new office and residential space. That has driven prices down even further for older buildings. Another factor for potential buyers to consider: the The Chrysler Building in midtown Manhattan is one of land on which the Chrysler Building stands is one- the most iconic buildings in the New York skyline third owned by Cooper Union, a private university. In 1997, Tishman Speyer negotiated a long-term lease with the university that ran through 2147. The Chrysler Building, one of the most iconic That deal called for the annual rent to rise from structures in New York, has been put up for sale by $7.8 million in 2017 to $32.5 million from its owners, Emirati investment firm Mubadala and 2019-2027, according to documents seen by AFP. real estate group Tishman Speyer. The value of the land alone was estimated at $679 The owners did not set a selling price, a source million in late 2017. close to the sale told AFP on condition of anonymity, confirming a report that was first The Chrysler Building, which opened in 1930, published in The Wall Street Journal. stands 1,046 feet (319 meters) tall. It was the world's tallest building, but only for 11 months, The building in midtown Manhattan, considered an when it was dethroned by the Empire State Art Deco masterpiece, was acquired in 2008 by Building, also in Manhattan. -

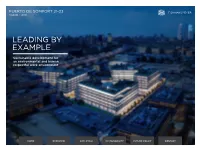

Leading by Example

PUERTO DE SOMPORT 21-23 MADRID / SPAIN LEADING BY EXAMPLE Sustainable development for an environmental and human respectful work environment PUERTO DE SOMPORT 21-23 MADRID / SPAIN OVERVIEW ABOUT PUERTO DE SOMPORT 21-23 Located in the North of Madrid, in the Las Puerto de Somport 21-23 is a 20,000m2 Tablas District, Puerto de Somport 21-23 is building designed to deliver on Tishman the first stage of a three-phase development. Speyer’s ambitious Sustainable Development Once all phases are complete, the complex 2 goals. The project has been developed in will total 60,000m dedicated to office space the framework of a joint venture between and amenities. The development is adjacent Tishman Speyer and Metrovacesa, a partner to Madrid Nuevo Norte, an ambitious urban with great local expertise. Thanks to an all- regeneration scheme intended to help fulfil glass façade and higher-than-usual ceiling the City of Madrid’s contribution to the heights, the six-story construction (ground Sustainable Development Goals of the UN floor plus five) optimizes natural light. 2030 Agenda. There are two impressive lobbies with five- CONTEXT meter ceiling heights and workspaces with three-meter-plus ceiling heights. Puerto To incorporate sustainability holistically de Somport 21-23 offers a unique office throughout the project, Tishman Speyer set environment, with flexible space that can ambitious objectives based on LEED and be adapted according to tenants’ needs. It WELL standards and conducted a life cycle comprises premium serviced offices, retail assessment (LCA) as part of the building and dedicated spaces for wellbeing, such as design process. -

Real Estate Group of the Year: Sullivan & Cromwell by Mccord Pagan

Portfolio Media. Inc. | 111 West 19th Street, 5th Floor | New York, NY 10011 | www.law360.com Phone: +1 646 783 7100 | Fax: +1 646 783 7161 | [email protected] Real Estate Group Of The Year: Sullivan & Cromwell By McCord Pagan Law360 (February 15, 2019, 4:17 PM EST) -- Sullivan & Cromwell LLP last year handled transactions such as GGP Inc.'s $14.8 billion buyout by Brookfield Property Partners and the San Francisco Giants' $1.6 billion redevelopment of the land around its stadium, earning it a spot as one of Law360's Real Estate Groups of the Year. Robert Schlein, managing partner of Sullivan & Cromwell's real estate practice, said one of the strengths of the group is its place within the broader corporate practice area of the firm, allowing attorneys to work with companies on transactions that overlap into other fields, such as private equity or sports. Schlein said that structure gives them a competitive advantage and is more enjoyable for the client. "There's a small team working with them as opposed to different pockets they're not as familiar with," Schlein said. "We really think of ourselves as both real estate lawyers and general corporate lawyers." At the firm of about 900 lawyers, the roughly 27 partners and associates in the real estate group work mostly out of New York, though some are in London, Tokyo and Frankfurt. Partner Anthony Colletta said Sullivan & Cromwell's representation of Goldman Sachs unit Broad Street Principal Investments LLC as it acquired about $750 million worth of residential San Francisco real estate from multiple sellers — about 1,450 apartments across 61 buildings — is an example of the depth of the real estate group. -

DATE: July 11, 2013 TO: Historic Preservation Commissioners FROM: Daniel A

DATE: July 11, 2013 TO: Historic Preservation Commissioners FROM: Daniel A. Sider, Planning Department Staff RE: Market Analysis of the Sale of Publicly Owned TDR In May 2012, Planning Department (“Department”) Staff provided the Historic Preservation Commission (“HPC”) an informational presentation on the City’s Transferable Development Rights (“TDR”) program. In February 2013, the Department retained Seifel Consulting, Inc. and C.H. Elliott & Associates (jointly, “Consultants”) to perform a market analysis informing a possible sale of TDR from City-owned properties. The resulting work product (“Report”) was delivered to the Department in late June. This memo and the attached Report are intended to provide the HPC with relevant follow-up information from the May 2012 hearing. The City’s TDR Program Since the mid-1980’s, the Planning Department has administered a TDR program (“Program”) through which certain historic properties can sell their unused development rights to certain non- historic properties. The program emerged from the 1985 Downtown Plan in response to unprecedented office growth, housing impacts, transportation impacts and the loss of historic buildings. The key goal of the Program is to maintain Downtown’s development potential while protecting historic resources. The metric that underpins the Program is Floor Area Ratio ("FAR"), which is the ratio of a building’s gross square footage to that of the parcel on which it sits. Under the Program, a Landmark, Significant, or Contributory building can sell un-built FAR capacity to a non-historic property which can then use it to supplement its base FAR allowance. TDRs can only be used to increase FAR within applicable height and bulk controls. -

Operational Excellence

OVERVIEW Nike’s Greater China headquarters campus LEED® GOLD HIGHLIGHTS / STATS consists of a nine-story, Class A office Li Na office building: The Li Na and Liu Xiang buildings have both 379,140 sq. ft. building, Li Na, and a five-story conference been certified LEED® (Leadership in Energy (35,220 sq. m.) center, Liu Xiang, which houses conference and Environmental Design) Gold Core & Shell Liu Xiang conference facilities, media rooms and exhibition spaces. v2009, which emphasizes occupant comfort center: 218,600 sq. ft. Nike’s 600,000 sq. ft. (55,740 sq. m.) campus and well-being. (20,310 sq. m.) is part of The Springs, Tishman Speyer’s 20% savings on largest development project in China, CONNECTING TO THE COMMUNITY annual energy The Yangpu District is one of four urban costs, compared to situated in Shanghai’s Yangpu District, less ASHRAE 90.1-2007 than eight miles from the central business submarkets in Shanghai, centrally located baseline district. between the city’s two major airports. The 29% of site dedicated OPERATIONALUpon completion, The Springs will encompass Springs is conveniently situated along a to green space 9.7 million sq. ft. (900,230 sq. m.) spread over major transit hub and important education Adjacent to a 33-acre a 66-acre site. The full-service community corridor, with three of China’s most wetland ecological reserve EXCELLENCEoffers an eco-friendly lifestyle and will provide distinguished universities nearby. A number approximately 900 serviced apartment units of sports centers, shopping, and mixed- and nearly 8 million sq. ft. (740,000 sq. -

400 Montgomery Street

400 Montgomery Street For Lease | Retail Space | North Financial District - San Francisco, CA This exceptionally well-located Downtown retail availability sits at the base of the historic 400 Montgomery Street - a 75,000 SF office building at the cross streets of Montgomery and California. Don’t miss this rare opportunity to front one of the Financial District’s busiest streets. Premises 1,951 Rentable Square Feet 20,253 Cars Per Day on Montgomery Ideal for Fitness, Non-Cooking Food, Estimated 22 Million Pedestrians or Service Per Year Pass the Intersection of Montgomery and California 101 PEIR 39 1 AQUATIC PARK JEFFERSON ST TAYLOR ST POWELL ST JONES ST MARINA GREEN NORTH POINT ST M BEACH ST A MASON ST Y R CASA WAY A IN W A KEARNY ST O B R L I V MARINA BLVD RICO WAY T JEFFERSON ST D STOCKTON ST BRODERICK ST E R GOLDEN GATE NATIONAL WEBSTER ST FORT BAY ST RECREATION AREA MASON NORTH POINT ST BUCHANAN ST GRANT AVE C PRADO ST CERVANTES BLVD R JEFFERSON ST BEACH ST HYDE ST IS S Y BAKER ST FI POLK ST BAY ST FRANCISCO ST CHESTNUT ST ELD A BEACH ST V BEACH ST MONTGOMERY ST E AVILA ST NORTH POINT ST GOUGH ST LARKIN ST T DIVISADERO ST BAY ST CHESTNUT ST H 101 E SCOTT ST E FILLMORE ST LOMBARD ST M CAPRA WAY FRANKLIN ST BAY ST B NORTH POINT ST A T SANSOME ST T E R S M FRANCISCO ST L C E A A G A D R L LOMBARD ST R D V B L A O GREENWICH ST E L M A LEAVENWORTH ST P R R B BAY ST H COLUMBUS AVE H L C O A A OCTAVIA ST CHESTNUT ST H PIERCE ST AY L N W W IL D O L BLV LIN S O A D Y LOMBARD ST C H TAYLOR ST CO TOLE GREENWICH ST K N L E E I N FILBERT ST L -

Tclf.Org What’S

The Cultural Landscape Foundation connecting people to places™ tclf.org What’s Out There® San Francisco Bay Area Photo courtesy Golden Gate National Parks Conservancy The Cultural Landscape Foundation (TCLF) TCLF is a 501(c)(3) non-profit founded in 1998 to connect people to places. TCLF educates and engages the public to make our shared landscape heritage more visible, identify its value, and empower its stewards. Through its website, publishing, lectures and other events, TCLF broadens support and understanding for cultural landscapes. tclf.org 2 The Cultural Landscape Foundation San Francisco Bay Area Welcome to What’s Out There® San Francisco The guidebook is a complement to TCLF’s digital What’s Out Bay Area, organized by The Cultural Landscape There San Francisco Bay Area Guide (tclf.org/san-francisco), Foundation (TCLF) and a committee of local experts. an interactive online platform that includes the enclosed site profiles plus many others, as well as overarching narratives, This guidebook provides photographs and details of 35 maps, historic photographs, and designers’ biographical examples of the region’s rich cultural landscape legacy. Its profiles. The guide is the sixteenth such online compendium publication is timed to coincide with the launch of What’s of urban landscapes, dovetailing with TCLF’s web-based Out There Weekend San Francisco Bay Area, September What’s Out There, the nation’s most comprehensive searchable 14-15, 2019, a weekend of free, expert-led tours. database of historic designed landscapes. Profusely illustrated First settled by indigenous peoples and later by Spanish and carefully vetted, the searchable database currently features colonists, the Bay Area saw relatively modest growth until the more than 2,000 sites, 12,000 images, and 1,100 designer 1848 California Gold Rush and railroad connections irrevocably profiles. -

Seeing Green in San Francisco: City As Resource Frontier,” Antipode 48.3

Knuth, Sarah (Forthcoming 2016) “Seeing Green in San Francisco: City as Resource Frontier,” Antipode 48.3. Expected Publication June 2016 Seeing Green in San Francisco: City as Resource Frontier Dr. Sarah E. Knuth, University of Michigan Abstract The early 21st century witnessed a boom in green building in San Francisco and similar cities. Major downtown property owners and investors retrofitted office towers, commissioned green certifications, and, critically, explored how greening might pay. Greening initiatives transcend corporate social responsibility: they represent a new attempt to enclose and speculate upon “green” value within the second nature of cities. However, this unconventional resource discovery requires a highly partial view of buildings’ socio-natural entanglements in and beyond the city. I illuminate these efforts and their obscurities by exploring the experience of an exemplary green building in San Francisco, an office tower that has successively served as a headquarters organizing a vast resource periphery in the American West, a symbol and driver in the transformation of the city’s own second nature, a financial “resource” in its own right, and, most recently, an asset in an emerging global market for green property. Keywords: green building, green value, urban political economy/ecology, resource geography, financialization, San Francisco Amid the economic turmoil of the late 2000s, the city of San Francisco saw a major building boom, of an unusual kind. Even as foreclosures continued across the metropolitan region and state and local agencies rolled out drastic austerity programs, a fresh flood of capital poured into downtown real estate. This inrush of investment did not only build new buildings; nor did it simply transfer office towers from one owner to another. -

Glass from Glass

VERDE SW1 LONDON / UK GLASSOVERVIEW FROM Nike’s Greater China headquarters campus LEED® GOLD consists of a nine-story, Class A office The Li Na and Liu Xiang buildings have both GLASSbuilding, Li Na, and a five-story conference been certified LEED® (Leadership in Energy center, Liu Xiang, which houses conference and Environmental Design) Gold Core & Shell facilities, media rooms and exhibition spaces. v2009, which emphasizes occupant comfort LeadingNike’s 600,000 by sq. example: ft. (55,740 sq. Setting m.) campus a and well-being. is part of The Springs, Tishman Speyer’s precedentlargest development in the project construction in China, industryCONNECTING TO THE COMMUNITY situated in Shanghai’s Yangpu District, less The Yangpu District is one of four urban than eight miles from the central business submarkets in Shanghai, centrally located district. between the city’s two major airports. The Upon completion, The Springs will encompass Springs is conveniently situated along a 9.7 million sq. ft. (900,230 sq. m.) spread over major transit hub and important education a 66-acre site. The full-service community corridor, with three of China’s most offers an eco-friendly lifestyle and will provide distinguished universities nearby. A number approximately 900 serviced apartment units of sports centers, shopping, and mixed- and nearly 8 million sq. ft. (740,000 sq. m.) use and residential areas also enhance the of Class A office, retail, hotel, cultural and location. amenity space. CONNECTING TO THE ENVIRONMENT VISION As part of The Springs development, Nike’s Sustainability, flexibility and customization campus benefits from strong ties to the local were key goals from the outset. -

Baseline Budget for Phase 1 of the Transbay Transit Center Program (Program) in the Amount of $1,189,000,000 in Year of Expenditure (YOE) Dollars

THIS STAFF REPORT COVERS CALENDAR ITEM NO.: 7 FOR THE MEETING OF: November 16, 2007 TRANSBAY JOINT POWERS AUTHORITY BRIEF DESCRIPTION: Recommendation of a Baseline Budget for Phase 1 of the Transbay Transit Center Program (Program) in the amount of $1,189,000,000 in year of expenditure (YOE) dollars. SUMMARY: A preliminary Phase 1 cost estimate totaling $983 million was developed in January 2006 and presented to the Board in March 2006. This preliminary estimate was prepared using conceptual designs and FTA-mandated minimum levels of contingencies, as well as initial estimates of escalation and program-wide costs such as design and construction management. Since the Phase 1 preliminary cost estimate was presented to the Board in March 2006, considerable work has been completed to identify the most probable final cost of Phase 1 as the basis for the recommended Baseline Budget. The estimate was recalculated to account for the escalation that occurred during 2006, and an industry review was conducted to assess the most probable ongoing annual levels of escalation to the end of construction. In addition, adjustments were made to the Phase 1 preliminary cost estimate to account for further scope development, development of intended contracting strategies, and reallocation of some costs from Phase 2. Accordingly, this report provides an update to the components included in the prior estimate and recommends the adoption of a Baseline Budget for Phase 1 of $1,189,000,000 (YOE). Once adopted, this Baseline Budget will be the benchmark against which cost performance will be measured. Staff and consultants have developed a draft funding plan for the Baseline Budget. -

![[A Model for Small Public Places]](https://docslib.b-cdn.net/cover/0432/a-model-for-small-public-places-2550432.webp)

[A Model for Small Public Places]

[a model for small public places] FOR THE CITY OF SACRAMENTO BY TAMARA MALMSTROM [a model for small public places] FOR THE CITY OF SACRAMENTO A SENIOR PROJECT PREPARED TO THE FACULTY OF THE LANDSCAPE ARCHITECTURE DEPARTMENT UNIVERISITY OF CALIFORNIA, DAVIS IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF BACHELORS OF SCIENCE OF LANDSCAPE ARCHITECTURE ACCEPTED AND APPROVED BY: ___________________________________________________________________ FACULTY MEMBER - MARK FRANCIS, FASLA ___________________________________________________________________ FACULTY MEMBER - PATSY OWENS, ASLA ___________________________________________________________________ COMMITTEE MEMBER - MARY DE BEAUVIERES, PRINCIPAL PLANNER ___________________________________________________________________ COMMITTEE MEMBER - JEFF NITTKA, LANDSCAPE ARCHITECT ___________________________________________________________________ COMMITTEE MEMBER - STEVEN GIGUIERE, LANDSCAPE ARCHITECT ___________________________________________________________________ COMMITTEE MEMBER - GREG TAYLOR, SENIOR URBAN DESIGNER TAMARA MALMSTROM SPRING 2008 “The image of a great city stems largely from the quality of it’s public realm - its streets, boulevards, parks, squares, plazas, and waterfronts.” Cyril B. Paumier 19th & Q Site [abstract] [abstract] The City of Sacramento’s Department of Parks & Recreation is currently developing a vision, purpose, policies, and implementation strategies for the creation of small parks and urban plazas (Small Public Places) in higher density areas of the