2018 Coffee Barometer

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1H2018 M&A Update

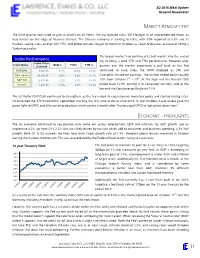

3Q 2018 M&A Update General Newsletter MARKET ATMOSPHERE The third quarter continued to give us drama on all fronts. The EU rejected Italy’s 2019 budget in an unprecedented move, as Italy teeters on the edge of financial distress. The Chinese economy is starting to falter, with GDP reported at 6.5% and its markets seeing a loss of over 20% YTD. And global tensions began to mount in October as Saudi Arabia was accused of killing a Turkish journalist. The broad market had continued its bull market into the end of Index Performance Q3, marking a solid YTD and TTM performance. However after Index Price Index Name QoQ % YTD% TTM % 9/28/2018 quarter end the market experience a pull back as the Fed NASDAQ 8,046.35 7.1% 14.8% 23.9% continued to raise rates, the DOW dropped as 3M, and Dow Jones 26,458.31 9.0% 6.6% 18.1% Caterpillar missed on earnings. The market ended down roughly st th S&P 500 2,913.98 7.2% 8.1% 15.7% 10% from October 1 – 29 . At the high end the Russell 2000 Russell 1,696.57 3.3% 9.5% 13.8% pulled back 12.9%, putting it in correction territory, and at the low end the Dow Jones pulling back 7.6%. The US Dollar (DXY:CUR) continued to strengthen, as the fed ended its expansionary monetary policy and started raising rates. Oil breached the $70 threshold in September marking the first time to do so since 2014. In late October, Saudi Arabia gave the green light to OPEC and allies on oil production, which comes a month after Trump urged OPEC to “get prices down now.” ECONOMIC - HIGHLIGHTS The US economy continued to see positive data come out across employment, GDP and inflation. -

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

Nnn Investment Opportunity Long Term Corporate Lease Krispy Kreme Doughnut Corporation Nnn Investment Opportunity Long Term Corporate Tenant

KRISPY KREME| 810 CASSAT AVENUE, JACKSONVILLE, FL 32205 NNN INVESTMENT OPPORTUNITY LONG TERM CORPORATE LEASE KRISPY KREME DOUGHNUT CORPORATION NNN INVESTMENT OPPORTUNITY LONG TERM CORPORATE TENANT KRISPY KREME| 810 CASSAT AVENUE,£¤301 JACKSONVILLE FL 32205 £¤17 UVA1A JACKSONVILLE INT'L AIRPORT PROPERTY HIGHLIGHTS • Address: 810 Cassat Ave, Jacksonville FL 32205 • Total SF: 19,820 SF • Total AC: 0.455 AC • Building SF: 2,600 SF • Occupancy :100% • Concept: Krispy Kreme JACKSONVILLE • Year Built: 2012 DOWNTOWN ¨¦§295 £¤90 UVA1A TENANT HIGHLIGHTS £¤17 • Over 1,400 Krispy Kreme locations across 30 countries UNIVERSITY OF NORTH FLORIDA • Founded 82 years ago in Winston-Salem, NC UV202 • Acquired by JAB Holdings in 2016 (S&P “A-“ credit rating) NAVAL AIR STATION JACKSONVILLE • World Famous “Glazed Doughnut” icon £¤17 295 ¨¦§ £¤1 UV21 ¨¦§95 ¨¦§95 For more information, please contact: £¤1 PJ BEHR Vice President, CCIM Investment Sales 407.540.7746 420 South Orange Ave. Suite 950 [email protected] Orlando, FL 32801 Although the information contained herein was provided by sources believed to be reliable, CNL Commercial Real Estate makes foundrycommercial.com no representation, expressed or implied, as to its accuracy and said information is subject to errors, omissions or changes. NNN INVESTMENT OPPORTUNITY LONG TERM CORPORATE TENANT MARKET AERIAL CASSAT AVE - 23,500 VPD AVE CASSAT I - 10 - 103,500 VPD PROPERTY FEATURES The Krispy Kreme is located at 810 Cassat Ave, a major north-south artery in the Riverside submarket of Jacksonville, FL. The property is a .45 ac signalized corner lot with great visibility and access at the SWC of the intersection. -

Deal of the Week: JAB to Buy Pret a Manger for $2B

Deal of the Week: JAB to Buy Pret A Manger for $2B Announcement Date May 29, 2018 Acquirer JAB Holding Company Acquirer Description Privately held German conglomerate that includes investments of companies operating in the arenas of consumer goods, forestry, coffee, luxury fashion, and fast food, among others Already owns Panera, Au Bon Pain, Caribou Coffee, Krispy Kreme, and Keurig Headquartered in Luxembourg Target Company Pret A Manger Target Description International sandwich shop chain commonly referred to simply as "Pret” with approximately 530 locations in nine countries Controlled by the investment firm Bridgepoint Advisers Revenue of 879 million pounds last year Founded in 1983 and headquartered in London Acquirer Advisor HSBC Target Advisor JP Morgan Price / Consideration $2 billion Cash Rationale Since 2012, JAB Holdings, backed by Germany’s wealthy and secretive Reimann family, has spent tens of billions of dollars to assemble a huge portfolio of brands, expanding its coffee and beverage empire It began with coffee, as JAB sought to challenge the industry heavyweight Nestlé. JAB made deals for Peet’s Coffee, Caribou Coffee, Stumptown and more. Then came restaurants like Krispy Kreme and the fast‐casual chain Panera. And this year, JAB helped Keurig Green Mountain, which the conglomerate bought and combined with Mondelez’s former coffee arm, move into soft drinks with an $18.7 billion deal for Dr Pepper Snapple "Management's proven track record and commitment to customer service, investment in innovation and -

JAB to Buy Keurig Green Mountain for $13.9B

Deal of the Week: JAB to Buy Keurig Green Mountain for $13.9B Announcement Date December 7, 2015 Acquirer JAB Holding Company Acquirer Description European consumer products conglomerate Target Keurig Green Mountain, Inc. (NASDAQ: GMCR) Target Description Produces and sells coffeemakers and specialty coffee in the United States, Canada, and internationally Founded in 1981 and headquartered in Waterbury, Vermont Target Financial Mkt Cap: $13.4 billion LTM EBITDA: $1.1 billion Statistics EV: $8.1 billion LTM EV / Revenue: 1.8x LTM Revenue: $4.5 billion LTM EV / EBITDA: 7.6x Target Advisors Bank of America and Credit Suisse provided fairness opinions to Keurig Green Mountain Price / Consideration Price: $13.9 billion Consideration: Cash Rationale Acquiring Keurig Green Mountain is JAB’s latest and biggest move yet to capitalize on consumers’ craving for coffee “Keurig Green Mountain represents a major step forward in the creation of our global coffee platform,” Bart Becht, the chairman of JAB, said in the statement. “Keurig Green Mountain will operate as an independent entity to ensure it will further build on its coffee and technology strength and continue to serve all its partners to the best of its abilities.” “This transaction will deliver significant cash value for our shareholders and offers an exciting new chapter for our customers, partners and employees by combining Keurig Green Mountain with JAB’s global coffee platform,” added Brian Kelley, CEO of Keurig Green Mountain Deal Points JAB will acquire Keurig Green Mountain for $92 a share in cash, a 78% premium over its stock price on Dec. 4 To acquire Keurig, JAB joined with several firms that are already investors in Jacobs Douwe Egberts. -

Panera Bread (Houston MSA) 6439 Garth Road Baytown, Texas 77521 Panera Bread | Baytown, TX Table of Contents

Net Lease Investment Offering Panera Bread (Houston MSA) 6439 Garth Road Baytown, Texas 77521 Panera Bread | Baytown, TX Table of Contents TABLE OF CONTENTS Offering Summary Executive Summary ................................................................... 1 Investment Highlights ............................................................. 2 Property Overview ...................................................................... 3 Location Overview Photographs ...................................................................................4 Location Aerial .............................................................................. 5 Site Plan ..............................................................................................6 Location Map ................................................................................. 7 Market Overview Demographics ..............................................................................8 Market Overviews .......................................................................9 Tenant Summary Tenant Profile .................................................................................11 www.bouldergroup.com | Confidential Offering Memorandum Panera Bread | Baytown, TX Executive Summary EXECUTIVE SUMMARY The Boulder Group is pleased to exclusively market for sale a single tenant net leased Panera Bread property located within the Houston MSA in Baytown, Texas. Panera Bread has been in this location since June 2013. There are over 12 years remaining on the primary term of the -

JAB Holding to Buy Krispy Kreme for $1.35B

Deal of the Week: JAB Holding to Buy Krispy Kreme for $1.35B Announcement Date May 9, 2016 Acquirer JAB Holding Company Acquirer Description Billionaire European family Investment arm of the Reimann family, heirs to the German consumer goods conglomerate, Joh. A. Benckiser Target Company Krispy Kreme Doughnuts, Inc. (NYSE: KKD) Target Description Operates as a branded retailer and wholesaler of doughnuts, coffee and other complementary beverages, and treats and packaged sweets Founded in 1937 and headquartered in Winston‐Salem, North Carolina Target Financial Mkt Cap: $1.3 billion LTM EBITDA: $68.9 million Statistics EV: $1.0 billion LTM EV / Revenue: 2.0x LTM Revenue: $513.7 million LTM EV / EBITDA: 15.1x Acquirer Advisors Barclays and BDT & Company Target Advisor Wells Fargo Price / Consideration $1.35 billion Cash Rationale With the deal, the JAB Holding Company will add to its trove of coffee‐ oriented businesses, including Peet’s Coffee & Tea, Stumptown Coffee Roasters and Caribou Coffee In December, JAB acquired Keurig Green Mountain for $13.9 billion, its biggest bet yet in building its coffee empire “We are thrilled to have such an iconic brand as Krispy Kreme joining the JAB portfolio,” said Peter Harf, senior partner at JAB, in the statement. “This is yet another example of our commitment to investing in extraordinary brands with significant growth prospects.” Deal Points JAB plans to acquire Krispy Kreme for $21 a share in cash, a premium of more than 25% from Friday’s closing price BDT Capital Partners, -

Panera Bread 2460 Prince William Parkway Woodbridge, VA 22192 REPRESENTATIVE IMAGE 2 SANDS INVESTMENT GROUP EXCLUSIVELY MARKETED BY

JDS Real Estate Services, Inc. VA Lic. # 02260269591 Panera Bread 2460 Prince William Parkway Woodbridge, VA 22192 REPRESENTATIVE IMAGE 2 SANDS INVESTMENT GROUP EXCLUSIVELY MARKETED BY: MATSON KANE BRIAN ROBINSON ELAN SIEDER MAX FREEDMAN TX Lic. # 695584 CA Lic. # 02092902 TX Lic. # 678407 TX Lic. # 644481 512.861.1889 | DIRECT 310.241.3677 | DIRECT 512.649.5185 | DIRECT 512.766.2711 | DIRECT [email protected] [email protected] [email protected] [email protected] SIG Works With Non-Resident Prospective Buyers In Cooperation With: Stan Stanfield, VA Broker Lic # 0226026959 of JDS Real Estate Services, Inc. VA Broker Lic # 0226026959 JDS Real Estate Services, Inc. Works With Prospective Virginia Resident Buyers SANDS INVESTMENT GROUP 3 TABLE OF CONTENTS 04 06 07 10 12 INVESTMENT OVERVIEW LEASE ABSTRACT PROPERTY OVERVIEW AREA OVERVIEW TENANT OVERVIEW Investment Summary Lease Summary Location, Aerial & Retail Maps City Overview Tenant Profile Investment Highlights Rent Roll Demographics Parent Company © 2019 JDS Real Estate Services, Inc. (JDS) in association with Sands Investment Group (SIG). The information contained in this ‘Offering Memorandum,’ has been obtained from sources believed to be reliable. JDS & SIG does not doubt its accuracy, however, JDS & SIG makes no guarantee, representation or warranty about the accuracy contained herein. It is the responsibility of each individual to conduct thorough due diligence on any and all information that is passed on about the property to determine it’s accuracy and completeness. Any and all projections, market assumptions and cash flow analysis are used to help determine a potential overview on the property, however there is no guarantee or assurance these projections, market assumptions and cash flow analysis are subject to change with property and market conditions. -

JAB Sarl Standalone Financials June 2020

JAB Holding Company S.à r.l. Luxembourg Interim Condensed Financial Statements as at and for the six months period ended 30 June 2020 4, Rue Jean Monnet, L-2180 Luxembourg B 164.586 JAB Holding Company S.à r.l., Luxembourg Index Page Report of the Réviseur d’Enterprises agréé 3 Interim Condensed Financial Statements for the six months period ended 30 June 2020 Interim Condensed Statement of Financial Position as of 30 June 2020 4 Interim Condensed Statement of Profit or Loss and Other Comprehensive Income for the six months period ended 30 June 2020 5 Interim Condensed Statement of Changes in Equity for the six months period ended 30 June 2020 6 Interim Condensed Cash Flow Statement for the six months period ended 30 June 2020 7 Notes to the interim Condensed Financial Statements 8 JAB Holding Company S.à r.l., Luxembourg Interim Condensed Statement of Financial Position as of 30 June 2020 Note 30 June 2020 31 December 2019 in $k in $k in $k in $k Non-current assets Investments in subsidiaries 4 18,708,594 24,681,262 18,708,594 24,681,262 Current assets Other receivables 5 3,465 1,335 Cash and cash equivalents 6 8,994 349 12,459 1,684 18,721,053 24,682,946 Shareholder's equity 8 Issued share capital 8,797 8,797 Share premium 9,490,516 9,637,312 Retained earnings 6,649,340 11,309,899 16,148,653 20,956,008 Non-current liabilities Redeemable shares 9 1,205,681 1,586,782 Other liabilities 10, 11 466,942 741,603 1,672,623 2,328,385 Current liabilities Redeemable shares 9 854,490 1,284,894 Other liabilities 10, 11 45,287 113,659 899,777 1,398,553 18,721,053 24,682,946 The notes on pages 8 to 24 are an integral part of these interim condensed financial statements. -

Panera Bread Sale-Leaseback Corporate Relocation Site – Brand New Construction

EXCLUSIVE NET - LEASE OFFERING PANERA BREAD SALE-LEASEBACK CORPORATE RELOCATION SITE – BRAND NEW CONSTRUCTION Representative Photo OFFERING MEMORANDUM 408 Route 3 – Plattsburgh, New York 12901 Confidentiality and Disclaimer Marcus & Millichap hereby advises all prospective purchasers of properties, including newly-constructed facilities or newly- income or expenses for the subject property, the future projected Net Leased property as follows: acquired locations, may be set based on a tenant’s projected financial performance of the property, the size and square sales with little or no record of actual performance, or footage of the property and improvements, the presence or The information contained in this Marketing Brochure has been comparable rents for the area. Returns are not guaranteed; the absence of contaminating substances, PCB’s or asbestos, the obtained from sources we believe to be reliable. However, tenant and any guarantors may fail to pay the lease rent or compliance with State and Federal regulations, the physical Marcus & Millichap has not and will not verify any of this property taxes, or may fail to comply with other material terms of condition of the improvements thereon, or the financial information, nor has Marcus & Millichap conducted any the lease; cash flow may be interrupted in part or in whole due to condition or business prospects of any tenant, or any tenant’s investigation regarding these matters. Marcus & Millichap makes market, economic, environmental or other conditions. Regardless plans or intentions to continue its occupancy of the subject no guarantee, warranty or representation whatsoever about the of tenant history and lease guarantees, Buyer is responsible for property. -

10 Largest Announced and Pending Deals by U.S. Sponsors, Q1 2018

www.buyoutsnews.com April 2, 2018 | BUYOUTS | 35 1ST QUARTER DEALS the quality of business.” can potentially weather the storm of a While it’s too early to say whether Besides leveraging your platform for downturn. a function of tax-policy change, there add-ons, flexibility in terms of how you “A lot more deals are getting done appears to be a pickup in corporate dives- invest also resonates well, El-Nazer said. outside the bank market,” he said. “In titure opportunities in Q1, Simpson said. About one-third of TA’s deals are minor - a downturn, I think you want to make His team is tracking a dozen or so of ity investments. sure that the people you are putting in these situations across industries: “That’s Deal structure aside, El-Nazer added financing syndicates with are more bank- double what we were seeing a year ago.” that the best companies are those that like and have ridden through [economic] Greenip says PE will continue to out- offer phenomenal visibility into rev - cycles,” he said. perform public equity but the amount enues. In fact, across the various indus - In terms of deal type, Simpson said of work that sponsors are putting into tries in which TA invests, about 80 the market could see the return of con - their portfolio companies to get there is percent of the firm’s 2017 transactions sortium bids for $10 billion- or $20 bil - the greatest he’s ever seen. were in companies that have recurring lion-plus take-private LBOs. The bar is higher once a deal is struck, revenue, he said. -

Moody's JAB Holding Company Credit Opinion Update

CORPORATES CREDIT OPINION JAB Holding Company S.a r.l. 30 April 2021 Update of credit analysis Update Summary JAB's Baa2 rating is supported by the company's strong investment portfolio comprising cash-generative and typically defensive global consumer goods and services. Its investments in JDE Peet's and KDP, which accounted for approximately 56% (including direct shares) of JAB's portfolio value at year-end 2020, should continue to protect the group's credit quality. RATINGS JAB's coffee and beverage business as well as the petcare platform exhibited resilience in JAB Holding Company S.a r.l. 2020 under turbulent market conditions, whereas the valuation of Coty and Pret Panera Domicile Luxembourg declined in 2020. Long Term Rating Baa2 Type LT Issuer Rating - Fgn JAB has started simplifying its corporate structure through the partial repayment of Curr contingent liabilities at Acorn Holdings level from IPO proceeds of JDE Peet's and through Outlook Stable the amendment of the contractual terms of the long term incentive plans that are now Please see the ratings section at the end of this report accounted for as equity in JAB Holding's accounts. However JAB's rating remains held back by for more information. The ratings and outlook shown the company's levered capital structure above its own financial policy target of net MLV of reflect information as of the publication date. 15 to 20%. JAB's net MVL has increased materially during 2020 as a result of the unwinding of the Cottage SPV (that was related to JAB's additional purchase of shares in Coty) and pressure on valuations.