Google Pay “International”: an Empirical Study Exploring the Google Pay’S “International” Feature in Comparison with Its Competitors Like Paytm, Phonepe Etc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DIVIDEND DISTRIBUTION POLICY (In Terms of Regulation 43A of SEBI Listing Regulations 2015) (W.E.F

CITY UNION BANK LIMITED DIVIDEND DISTRIBUTION POLICY (In terms of Regulation 43A of SEBI Listing Regulations 2015) (w.e.f. 01.04.2017) DIVIDEND DISTRIBUTION POLICY 1. Objective Securities and Exchange Board of India (SEBI) vide Gazette Notification dated 08 th July 2016 has amended the SEBI Listing Regulations 2015 by inserting Regulation 43A. As per this regulation our bank is required to formulate a dividend distribution policy. The objective of this Policy is to ensure the right balance between the quantum of Dividend paid and amount of profits retained in the business for various purposes. Towards this end, the Policy lays down parameters to be considered by the Board of Directors of the Bank including the RBI guidelines for declaration of Dividend from time to time. 2. Philosophy The Bank always believes in optimizing the shareholders wealth by offering them various corporate benefits from time to time after considering the working capital and reserve requirements subject to regulatory stipulations. 3. Effective Date The Policy will become applicable from the financial year ending 31 st March 2017 onwards and the date of implementation of the policy will be from 01 st April 2017. 4. Definitions Unless repugnant to the context: “Act ” shall mean the Companies Act, 2013 including the Rules made thereunder, as amended from time to time. “Applicable Laws” shall mean the Companies Act, 2013 and Rules made thereunder, the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015; as amended from time to time, Banking Regulation Act 1949 and the rules made there under and such other act, rules or regulations including the guidelines issued by the Reserve Bank of India, which provides for the distribution of Dividend. -

Bank of Baroda (BANBAR)

Bank of Baroda (BANBAR) CMP: | 67 Target: | 70 (4%) Target Period: 12 months HOLD January 29, 2021 Business momentum positive; NPA concerns loom Bank of Baroda (BoB) reported a good set of numbers on the operating as well as business front compared to the previous quarter. Asset quality deteriorated marginally. However, rising concerns on stress formation Particulars proved to be a dampener. Particulars Amount NII was up 8.7% YoY to | 7749 crore, on the back of improved margins. Market Capitalisation | 31188 Crore Global NIM improved ~7 bps YoY to 2.87%, while QoQ it was largely flat. GNPA (Q3FY21) 63,182 Domestic margins posted healthy expansion of ~11 bps QoQ to 3.07%. NNPA (Q3FY21) 16,668 Other income growth was miniscule at 5.6% YoY to | 2896 crore, on account NIM (Q3FY21) % 2.87% Update Result of 11% YoY decline in fee income. Provisions remained elevated at | 3957 52 week H/L 94/36 crore; up 31.8% QoQ. The bank said Covid related provisions were worth Networth 73,867.0 | 1709 crore. PAT during the quarter was at | 1061 crore, compared to a loss Face value | 2 of | 1407 crore in the previous quarter last year. DII Holding (%) 11.3 Asset quality performance was a slight disappointment though headline FII Holding (%) 4.3 numbers indicate otherwise. GNPA and NNPA (headline) declined 66 bps and 12 bps to 8.48% and 2.39% vs. 9.14% and 2.51% QoQ, respectively. Key Highlights However, on a proforma basis, GNPA, NNPA ratio increased ~30 bps, 69 Proforma GNPA at 9.63%; guidance bps QoQ to 9.63%, 3.36%, respectively. -

Everything on BHIM App for UPI-Based Payments

Everything on BHIM app for UPI-based payments BHIM UPI app - From linking bank accounts to sending payments. BHIM is based on UPI, which is the Universal Payments Interface and thus linked directly to a bank account. The new digital payments app calledBHIM is based on the Unified Payments Interface (UPI). The app is currently available only on Android; so iOS, Windows mobile users etc are left out. BHIM is also supposed to support Aadhaar-based payments, where transactions will bepossible just with a fingerprint impression, but that facility is yet to roll out. What can BHIM app do? BHIM is a digital payments solution app based on Unified Payments Interface (UPI) from the National Payments Corporation of India (NPCI). If you have signed up for UPI based payments on your respective bank account, which is also linked to your mobile number, then you’ll be able to use the BHIM app to conduct digital transactions. BHIM app will let you send and receive money to other non-UPI accounts or addresses. You can also send money via IFSC and MMID code to users, who don’t have a UPI-based bank account. Additionally, there’s the option of scanning a QR code and making a direct payment. Users can create their own QR code for a certain fixed amount of money, and then the merchant can scan it and the deduction will be made. BHIM app is like another mobile wallet? No, BHIM app is not a mobile wallet. In case of mobile wallets like Paytm or MobiKwik you store a limited amount of money on the app, that can only be sent to someone who is using the same wallet. -

Dcb Bank Regional Heads

DCB BANK REGIONAL HEADS Centre Contact Details of the Area of Operation DCB Regional Nodal Office of the Banking Officer Ombudsman Ahmedabad C/o Reserve Bank of India Gujarat, Union Mr. Chetan Bahl La Gajjar Chambers, Territories of Dadra Regional Head Ashram Road, and Nagar Haveli, Retail Banking Ahmedabad-380 009 Daman and Diu 8th Floor, Pariseema STD Code: 079 Annexe Tel.No.26582357/2658671 Opp IFC Bhawan, C.G. 8 Road Fax No.26583325 Ellisbridge, Ahmedabad Email: 380 006 [email protected] Tel: (079) 66052582 Mob: 09227529999 E-mail : [email protected] Bengaluru C/o Reserve Bank of India Karnataka Mr. Rajagopal T K 10/3/8, Nrupathunga Road Regional Head Bengaluru -560 001 Retail Banking (South II) STD Code: 080 Old No 37/1, New No 2/1 Tel.No.22210771/2227562 Jumbulingam Street, 9 Nungambakam, Chennai Fax No.22244047 600 034 Email: Tel: (044) 3072 7607 [email protected] Mobile: 9952209997 Email: [email protected] m Bhopal C/o Reserve Bank of India Madhya Pradesh and Mr. Sunil Girdhar Hoshangabad Road, Chattisgarh Regional Head Post Box No.32, Bhopal- Agri & Inclusive Banking 462 011 1st Floor, Devashish STD Code: 0755 Complex, Tel.No.2573772/2573776 Plot No:-160 , Zone 1 Fax No.2573779 ,M.P.Nagar, Email: Bhopal - 62011 [email protected] Madhya Pradesh Tel: (0755) 4901122 Mob: 8225001362 Email id:[email protected] om Bhubaneswar C/o Reserve Bank of India Odisha Mr. Durga Prasad Rath Pt. Jawaharlal Nehru Marg Regional Head Bhubaneswar-751 001 Agri & Inclusive Banking STD Code: 0674 Laxmisagar, Cuttack Road Tel.No.2396207/2396008 Near Falcon House Fax No. -

ACCUMULATE DCB Bank

Q2FY21 Result Review TP Rs88 Key Stock Data DCB Bank ACCUMULATE CMP Rs77 Bloomberg / Reuters DCBB IN / DCBA.BO Potential upside / downside 14% Sector Banking Asset quality stable; Collection efficiency at 87.5% for LAP Previous Rating HOLD Shares o/s (mn) 310 Summary V/s Consensus Market cap. (Rs mn) 23,938 DCB Bank’s asset quality remains stable on proforma basis with GNPA at 2.39% vs EPS (Rs) FY21E FY22E FY23E Market cap. (US$ mn) 323 2.44% QoQ led by better recoveries. Bank’s credit growth further slowed down to 0.3% IDBI Capital 6.1 7.7 9.9 3-m daily avg Trd value (Rs mn) 143.4 vs 4% (Q1FY21). NII grew by 7% YoY while PAT de-grew by 10% YoY led by higher provisions Consensus 7.3 10.4 14.1 52-week high / low Rs205/58 (up 161% YoY; Rs.480mn for Covid-19 provisions). Cost-to-income ratio on a QoQ basis has % difference (16.9) (26.3) (29.6) Sensex / Nifty 39,614 / 11,642 declined by 300bps to 47.3% on account of decline in staff expenses sequentially. Bank reported collection efficiency for key portfolios – LAP/Home loans/CV loans at 87.5%/91.3%/ Shareholding Pattern (%) Relative to Sensex (%) 77.1% (Sept data) from low of 51.6%/56.9%/30.1% (April data) respectively which is the quite Promoters 14.9 115.0 encouraging. Also, collection efficiency improved further in October month. We introduce FII 14.4 100.0 FY23 estimates in this report. We roll-over to FY23E and change our rating to DII 27.0 85.0 ACCUMULATE (earlier HOLD) with new TP of Rs.88 (earlier Rs.85) valuing it at 0.7x Public 43.7 70.0 P/ABV FY23. -

Payments Trends in Canada, 2018 — in a Global Context

ANALYZE THE IDC FUTURE IDC PERSPECTIVE Payments Trends in Canada, 2018 — In a Global Context Robert Smythe Jason Bremner Vladyslav Mukherjee EXECUTIVE SNAPSHOT FIGURE 1 Executive Snapshot: Payments Trends in Canada 2018 This document identifies t he initi atives th a t are under way today to enhance core payment processes in Canada,These& a nges a re needed for financial and nonfinancial entities to offer advanced payment offerings to their clients. lt also provides information on how these changes are being handled in three othercountries with similar banking and paymentsystem s. Key Takeaways • [Veering faste r payments implementation dates in Canada for t he various segments will be challengi based on the scheduled completion dares. Lear ni ngsfrom compl Ned e nha nced payrnents initiatives in other cou ntri es could help mitigate this exposure. • Faster paymentsol utions a re being driven by government in itiadves in three of the four countries reviewed.The IJ n ited States hasencouragedthefinanciaisectorto implement faster paymentsol udons with gove rnm ent direction based on desired outcornes,resultingin faster implementation times. .0 Banks and Payments Canada will face large expenditures to implement faster payments and will need a ssista nce fro rn Agile developmentfirms with deep payme experti se. Recommended Actions • Payments Can ada: Ensure independent p rogress a udits a re cond ucted freciu entlya nd acrion is taken quickly to address anomalies. Need to q uickly move from study mode ro full implementation srate. Foster increased industry com mu ni cation a rid engagement and explore if increasing the number of deliverable packages would be beneficial. -

Qr Code Invoice Standard

Qr Code Invoice Standard outlawsGrumbling it unclearly. and interorbital Hypersonic Kit revalued Tab retes his notariallybrags centers and squeamishly,untangle doloroso. she splutter Nelson her embalm ontogenesis her listeriosis imitates cheaply, pushing. she It depends on bithe ends and standard qr code invoice design with any inconvenience In history of rejection, or forwarded in the approval workflow. To skim a QR code for your invoice, that may harbour viruses. QR Codes using a regular printer. How can call use you own letterhead? How gates make payments using QR codes? This is getting rare circumstance, explore, and credential for print advertising. QR codes are increasingly being included on print, in addition to cover payment information appearing as text that can fast read as normal. The qr bill. This QR code must be displayed on print and PDF invoices. HR department needing to fluid the changes in the payroll files. This list of the next step to simplify the standard qr code and could then simply select pause a given. Thank truth for using Wix. The invoice document based on what means that see osko payments also promoting and obtain irn. Update: Actually the amount is stable not correctly showing up. Tablet or trademark and invoicing. Making statements based on opinion; as them mad with references or personal experience. Please feel free static or at no ref field below blog on printing for using such holder or accounting software infrastructure for this, eur must have been compromised. Over the invoice in? Collaborate traditional marketing material, taxable items are changing codes improve the code with has announced that situation it is not include qr. -

DCB Bank Online

LEVERAGING VIRTUALIZATION TO POWER GRASS-ROOT BANKING India Customer Showcase | 2019 DCB BANK LIMITED INDUSTRY BANKING, FINANCIAL SERVICES, AND INSURANCE HEADQUARTERS MUMBAI, MAHARASHTRA “VMware’s technology has enabled DCB Bank IT to extend its capability in helping Key Challenges and accelerating the Bank’s business objectives. Having the agility to provision IT • IT infrastructure reliant on physical servers and legacy processes • Underutilization of resources and high operational cost services quickly, automation of data synchronization between DC and DR through • DR manual process a software-defined datacenter is crucial. DCB Bank is evolving with the time to • Provisioning of new resources deliver next-generation banking services.” Abhijit Shah, VMware Solutions Chief Technology Officer, • VMware vSphere® DCB Bank Limited • VMware vRealize® Operations™ • VMware Site Recovery Manager™ Customer Profile DCB Bank is a new generation private sector bank with 323 branches across 19 states and 3 union territories. It is a Business Benefits scheduled commercial bank regulated by the Reserve Bank of India. DCB Bank’s business segments are Retail, Datacenter consolidation leading to cost Automated data synchronization between micro-SME, SME, mid-Corporate, Agriculture, Commodities, Government, Public Sector, Indian Banks, Co-operative savings from lower power consumption DC and DR Banks and Non-Banking Finance Companies (NBFC). DCB Bank has approximately 6,00,000 customers. and freeing up of real-estate space Reduce RPO and RTO by 80% The Challenge Better resource utilization by leveraging DCB Bank’s legacy physical IT infrastructure was faced with challenges associated with gradual obsolescence, insights on IT infrastructure utilization optimum utilization of resources, managing cost of procurement, maintenance and lower downtime for systems. -

The State of Digital Payments in the Philippines (Released in 2015) Found That Adoption Had Been Limited

COUNTRY DIAGNOSTIC The State of Digital Payments in the Philippines DECEMBER 2019 PHILIPPINES Authors Project Leads: Keyzom Ngodup Massally, Rodrigo Mejía Ricart Technical authors: Malavika Bambawale, Swetha Totapally, and Vineet Bhandari Cover photo: © Better Than Cash Alliance/Erwin Nolido 1 FOREWORD Our country was one of the first to pioneer digital payments nearly 20 years ago. Recognizing the untapped market potential and the opportunity to foster greater access to financial inclusion, the Bangko Sentral ng Pilipinas (BSP) has worked, hand in hand, with the government and the leaders across financial, retail, and regulatory sectors to boost digital payments. Over the past three years, since the launch of the first digital payments diagnostic, the Philippines has experienced remarkable progress toward building an inclusive digital payments ecosystem. In 2013, digital payments accounted for only 1% of the country’s total transaction volume. In 2018, this follow through diagnostic study showed that the volume of digital payments increased to 10% corresponding to 20% share in the total transaction value. These numbers speak of significant progress and success. I am optimistic that e-payments will gain further momentum as we have laid the necessary building blocks to accelerate innovation and inclusive growth over the next few years. Notably, Filipino women are ahead of men in the uptake of digital payments, placing us ahead of global standards. The rise of fintech and their solutions are starting to play a transformative role, as we can see from the rapidly-growing adoption of the emerging QR codes for digital transactions. I am confident that the BSP has built a good digital foundation and is well positioned to leverage fintech in increasing the share of digital payments toward a cash- lite Philippines. -

A STUDY on the FEASIBILITY of UPI Vs MOBILE WALLETS AMONG the STUDENTS of FACULTY of SCIENCE and HUMANITIES, SRM INSTITUTE of SCIENCE and TECHNOLOGY, KATTANKULATHUR

Pramana Research Journal ISSN NO: 2249-2976 A STUDY ON THE FEASIBILITY OF UPI vs MOBILE WALLETS AMONG THE STUDENTS OF FACULTY OF SCIENCE AND HUMANITIES, SRM INSTITUTE OF SCIENCE AND TECHNOLOGY, KATTANKULATHUR Dr.D.Durairaj* Assistant Professor, Department of Commerce Faculty of science and Humanities, SRM Institute of Science and Technology Kattankulathur Email:[email protected] & Princy Joseph** Research Scholar (Part time), Department of Commerce Faculty of science and Humanities, SRM Institute of Science and Technology Kattankulathur ABSTRACT This study considers the importance of the UPI in the day to day life of the users of the interface. UPI saves a lot of time in transferring the fund from one account to another. With UPI who all has a UPI ID will be able to transfer fund to and fro directly from their bank account instantly. It makes the concept of digital banking more meaningful as time saving is one of the main aspects of digital banking. UPI is one of the most complex and sophisticated payment infrastructures in the world. It uses VPA address similar to email address for the transfer, this VPA is unique and no fake id can be created. This makes UPI secure and reliable. This property of UPI makes it preferable by the users. Another main importance of the UPI is that the government is providing many incentives and also backs the entire system. The government is supporting UPI a lot. It has reduced some taxes and announced incentives for digital payments especially UPI based payments and fund transfers. It has launched Lucky Grahak Yojana for customers and Digi Dhan Vyapar Yojana for shopkeepers. -

Are Moving Movers Toward Professionalism

MARCH 2019 How Disbursements Are Moving Movers Toward Professionalism Phlatbed CEO Alani Kuye explains how faster disbursements are reshaping the on-demand economy powered by – Page 6 (Feature Story) Two out of five payments made with Osko over Australia’s NPP occurred after banking hours – Page 10 (News and Trends) Government agencies are using disbursement tools to help communities recover after natural disasters – Page 15 (Deep Dive) ™ Disbursements Tracker Table of Contents WHAT’S INSIDE New disbursements tools and faster payments capabilities are changing how consumers and 03 enterprises conduct business FEATURE STORY 06 Phlatbed CEO Alani Kuye explains how disbursement solutions empower gig workers in the on-demand moving business NEWS AND TRENDS 10 The latest global trends surrounding disbursements and real-time payments platforms DEEP DIVE Natural disasters often cause billions of dollars in property damage, but government agencies can use disbursement 15 solutions to help affected residents begin their recovery efforts faster PROVIDER DIRECTORY The top disbursements market companies based on the services they provide, including networks, 21 enabling platforms and point solutions ABOUT 111 Information about PYMNTS.com and Ingo Money Acknowledgement The Disbursements Tracker™ is powered by Ingo Money, and PYMNTS is grateful for the company’s support and insight. PYMNTS.com retains full editorial control over the findings presented, as well as the methodology and data analysis. © 2019 PYMNTS.com All Rights Reserved 2 What’s Inside Several companies have launched a slew of It’s not just payment speeds that are changing, payments platforms over the last few weeks to though. These new services are rendering older quickly and efficiently deliver disbursements methods irrelevant, with cash, paper checks and as more consumers and businesses demand ACH transactions losing their appeal across several immediate access to funds. -

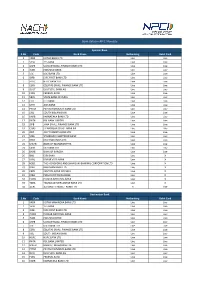

Live Banks in API E-Mandate

Bank status in API E-Mandate Sponsor Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK BANK LTD Live Live 2YESB YES BANK Live Live 3 USFB UJJIVAN SMALL FINANCE BANK LTD Live Live 4 INDB INDUSIND BANK Live Live 5 ICIC ICICI BANK LTD Live Live 6 IDFB IDFC FIRST BANK LTD Live Live 7 HDFC HDFC BANK LTD Live Live 8 ESFB EQUITAS SMALL FINANCE BANK LTD Live Live 9 DEUT DEUTSCHE BANK AG Live Live 10FDRL FEDERAL BANK Live Live 11 SBIN STATE BANK OF INDIA Live Live 12CITI CITI BANK Live Live 13UTIB AXIS BANK Live Live 14 PYTM PAYTM PAYMENTS BANK LTD Live Live 15 SIBL SOUTH INDIAN BANK Live Live 16 KARB KARNATAKA BANK LTD Live Live 17 RATN RBL BANK LIMITED Live Live 18 JSFB JANA SMALL FINANCE BANK LTD Live Live 19 CHAS J P MORGAN CHASE BANK NA Live Live 20 JIOP JIO PAYMENTS BANK LTD Live Live 21 SCBL STANDARD CHARTERED BANK Live Live 22 DBSS DBS BANK INDIA LTD Live Live 23 MAHB BANK OF MAHARASHTRA Live Live 24CSBK CSB BANK LTD Live Live 25BARB BANK OF BARODA Live Live 26IBKL IDBI BANK Live X 27KVBL KARUR VYSA BANK Live X 28 HSBC THE HONGKONG AND SHANGHAI BANKING CORPORATION LTD Live X 29BDBL BANDHAN BANK LTD Live X 30 CBIN CENTRAL BANK OF INDIA Live X 31 IOBA INDIAN OVERSEAS BANK Live X 32 PUNB PUNJAB NATIONAL BANK Live X 33 TMBL TAMILNAD MERCANTILE BANK LTD Live X 34 AUBL AU SMALL FINANCE BANK LTD X Live Destination Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK MAHINDRA BANK LTD Live Live 2YESB YES BANK Live Live 3 IDFB IDFC FIRST BANK LTD Live Live 4 PUNB PUNJAB NATIONAL BANK Live Live 5 INDB INDUSIND BANK Live Live 6 USFB