General Mills More Than Before

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Perfect Parfait Recipes

the perfect mix Everything you want in the perfect parfait! of ease and versatility! Quick & Easy Preparation - Versatility – Kid Appeal – Great Nutrition perfect parfait recipes Nature Valley® Peach Parfait – 2 Sassy Carrot dip with Vegetables – 7 New England Fruit Parfait – 3 Crazy Blue Crunch Parfait – 8 Grape Escape Parfait – 4 Pilgrim Parfait – 9 Fruit Rainbow Parfait – 5 Berry Berry Parfait – 10 American All-Star Parfait – 6 Cocoa PuffS® Parfait – 11 Meal Component Key M/MA = Meat/Meat Alternate G= Grain V =Veggie F = Fruit Foodservice Logo File: 10GM158 Date: 5/17/10 Temp: 76° Orbit: 1.16, 1.17, 1.18 le released 1.19 Nature Valley® Peach parfait INGREDIENTS INSTRUCTIONS 1 MA Yoplait® ParfaitPro™ 1. Place peaches in the bottom of a plastic tumbler. Lowfat Vanilla Yogurt 2. Place blueberries on top of the peaches. 1 G Nature Valley® 3. Pipe Yoplait® yogurt over the fruit. Parfait Granola 4. Serve topped with Nature Valley® Parfait Granola. .5 F Diced Peaches TIPS .5 F Blueberries • Substitute other on-hand USDA fruits to make this classic parfait. • Substitute a variety of General Mills bowlpak cereals for the Nature Valley® Parfait Granola. • Make this classic parfait a signature item in your cafeteria by offering it daily for breakfast or lunch. • Use fresh or frozen fruit. 2 Foodservice Logo File: 10GM158 Date: 5/17/10 Temp: 76° Orbit: 1.16, 1.17, 1.18 le released 1.19 New England Fruit parfait INGREDIENTS INSTRUCTIONS 1 MA Yoplait® ParfaitPro™ 1. Pipe Yoplait® yogurt in the bottom of a plastic tumbler. Lowfat Vanilla Yogurt 2. -

Clip Box Tops–Earn Cash for Our School!

Clip Box Tops–earn cash for our school! Earn cash for our school every time you shop for groceries. Clip Box Tops from hundreds of your favorite products.* Each Box Top is worth 10¢ to our school—and that adds up fast! CEREAL Disney’s® Mickey Mouse Clubhouse Berry Crunch Caribou Coee® Bars Ziploc® Brand Twist ‘n Loc® Containers Cheerios ® Disney’s® Princess Fairytale Flakes Chex Mix® Snack Mix Ziploc® Brand Big Bags Apple Cinnamon Cheerios ® Curves™ Cereal & Bars Chex Mix® for Kids Ziploc® Brand Expandable Bottom Bags Honey Nut Cheerios ® Pop•Secret® Microwave Popcorn Ziploc® Brand Treat Bags Frosted Cheerios ® REFRIGERATED/DAIRY Nature Valley® Crunchy Granola Bars Saran™ Premium Wrap MultiGrain Cheerios ® Pillsbury® Grands! ® Biscuits Nature Valley® Chewy Trail Mix Bars Saran™ Cling Plus® Wrap Team Cheerios ® Pillsbury® Grands! ® Sweet Rolls Nature Valley® Chewy Granola Bars with Yogurt Berry Burst Cheerios ® Pillsbury® Crescent Rolls Nature Valley® Sweet & Salty Nut Granola Bars PAPER PRODUCTS Fruity Cheerios ® Pillsbury® Cookie Dough Nature Valley® Healthy Heart Chewy Granola Bars COTTONELLE® Bath Tissue Yogurt Burst Cheerios® Pillsbury® Flaky Cinnamon Twists Cascadian Farm® Granola Bars COTTONELLE® Bath Tissue with Aloe & E Cheerios Crunch™ Pillsbury® Ready To Bake! ™ Cookies Curves® Snack Bars COTTONELLE® Bath Tissue Ultra Wheaties ® Pillsbury® Sweet Rolls Mini Fruit Roll-Ups® Fruit Flavored Snacks COTTONELLE FRESH® Flushable Moist Wipes Rice Chex ® Pillsbury® Simply Bake® Bars Fruit Roll-Ups® Crazy Pix™ Fruit Flavored Snacks COTTONELLE® -

Pop-Up Grocery Stores Hospital Implementation Guide Concept Overview

Pop-Up Grocery Stores Hospital Implementation Guide Concept Overview Context: • Many hospitals are limiting or closing their communal cafeteria offerings as protocol to face coronavirus • Doctors, nurses and other hospital staff may find their supermarkets are out of basic necessities when they are able to shop for their families after their hospital shifts • Hospitals still have access to a wide range of items from their foodservice distributors Solution: • Hospitals can convert their unused cafeteria space into temporary, pop-up grocery stores for staff • Stock the shelves with the products you already buy and make simple adjustments to tailor the offering to a grocery setting • See our General Mills category management recommendation in the following slides to bring this concept to life in your hospital, using the products you have on hand to serve the caregivers throughout your hospital Category Management Best Practices • Prioritize “Everyday Essentials” • Milk, Eggs, Cheese, Produce, Paper Products, Meat, Cereal, Bread/Baked Goods Category Reach (Based on Household Penetration & Purchase Frequency) • Consider “Family Entertainment” Options: Targeted Essentials Occasional Essentials Everyday Essentials Diapers Butter/Margarine Milk RTE Cereal • Microwave popcorn, baking mixes, frosting/icing Wine/Beer Coffee Eggs Bread Baby Food Flour Cheese Sugar/Sweeteners Paper Products Laundry Supplies Fresh Produce HH Cleaners Fresh Meat • As shelf/cooler space allows, bring in additional individually saleable foodservice Targeted Staples Occasional -

General Mills General Mills

Annual Report 2008 General Mills Continuing Growth Welcome to General Mills Net Sales by U.S. Retail Division U.S. Retail $9.1 billion in total Our U.S. Retail business segment includes the major marketing divisions 22% Big G Cereals listed to the left. We market our products in a variety of domestic retail 22% Meals outlets including traditional grocery stores, natural food chains, mass 19% Pillsbury USA merchandisers and membership stores. This segment accounts for 14% Yoplait 66 percent of total company sales. 13% Snacks 8% Baking Products 2% Small Planet Foods/Other Net Sales by International Region international $2.6 billion in total We market our products in more than 100 countries outside of the 35% Europe United States. Our largest international brands are Häagen-Dazs ice 27% Canada cream, Old El Paso Mexican foods and Nature Valley granola bars. This 23% Asia/Pacifi c business segment accounts for 19 percent of total company sales. 15% Latin America and South Africa Net Sales by Foodservice Bakeries And Foodservice Customer Segment We customize packaging of our retail products and market them to $2.0 billion in total convenience stores and foodservice outlets such as schools, restaurants 46% Bakery Channels and hotels. We sell baking mixes and frozen dough-based products to 45% Distributors/Restaurants supermarket, retail and wholesale bakeries. We also sell branded food 9% Convenience Stores/Vending products to foodservice operators, wholesale distributors and bakeries. This segment accounts for 15 percent of total company sales. Net Sales by Joint Venture Ongoing Joint Ventures (not consolidated) We are partners in several joint ventures. -

The Brands They Love for Cacfp

the brands they love for cacfp More than 70 eligible products for the Child and Adult Care Food Program all with no artificial flavors, no colors from artificial sources, and no high fructose corn syrup! UPC PRODUCT DESCRIPTION UPC PRODUCT DESCRIPTION ON-THE-GO POUCH CEREAL GOLD MEDALTM MIX 100-16000-31529-4 Whole Grain Variety Mun Mix 100-16000-14401-6 25% Less Sugar Cinnamon Toast Crunch™ Cereal On-The-Go Pouch NEW! 100-16000-31527-0 Whole Grain Complete Pancake Mix BOWLPAK CEREAL YOPLAIT PORTABLE YOGURT 100-16000-32262-9 Cheerios™ 100-70470-49295-4 Simply Go-Gurt Strawberry 2 oz 100-16000-38387-3 Cinnamon Chex™ 100-70470-14914-8 Go Big™ Blueberry 4 oz NEW! 100-16000-29444-5 25% Less Sugar Cinnamon Toast Crunch™ 100-70470-47402-8 Go Big™ Strawberry 4 oz 100-16000-33213-0 Corn Chex™ YOPLAIT YOGURT 4OZ 100-16000-11942-7 Kix™ 000-70470-17725-0 Trix™ Raspberry Rainbow 100-16000-32263-6 Multi Grain Cheerios™ 000-70470-17726-7 Trix™ Strawberry Banana Bash 100-16000-31921-6 Rice Chex™ 100-70470-31077-7 Trix™ Triple Cherry CUP CEREAL 000-70470-17729-8 Yoplait Original Strawberry/Strawberry Banana 25% Less Sugar Cinnamon Toast Crunch™ 000-70470-17728-1 Yoplait Original Red Raspberry/Harvest Peach 100-16000-14886-1 2oz Eq. Grain Cereal NEW! YOPLAIT ORIGINAL YOGURT 6OZ 100-16000-14883-0 Cinnamon Chex™ 2oz Eq. Grain Cereal NEW! 100-70470-00302-0 Original Mountain Blueberry BULK CEREAL 100-70470-00303-7 Original Cherry Orchard 100-16000-11977-9 Cheerios™ 100-70470-00323-5 Original French Vanilla 100-16000-13326-3 Corn Chex™ 100-70470-00306-8 Original -

Participating Products ™

powered by For My School PARTICIPATING PRODUCTS ™ ANNIE’S® Minions Cereal Vanilla Vibe REFRIGERATED & DAIRY Nature Valley™ Oatmeal Baking Mix Nature Valley™ Baked Oat LAND O’LAKES® Butter Squares Cereal Bites Oui® by Yoplait® (4-6oz) Nature Valley™ Biscuits Cheesy Rice Nature Valley™ Granola Pillsbury™ Crescents Nature Valley™ Granola Cups Cookies Crunch Pillsbury™ Grands Protein One™ Bars Crackers Nature Valley™ Oat Clusters Pillsbury™ Cookies Nature Valley™ Snack Mix Fruit Snacks Nature Valley™ Protein Pillsbury™ Pizza and Nature Valley™ Wafers Granola Bars Crunchy Granola Pie Crust Nature Valley™ Packed Bars Graham Snacks Nature Valley™ Protein Yoplait® Go-GURT® and Pillsbury™ Soft Baked Bars Soft Baked ® Mac & Cheese Simply Go-GURT Yogurt Nature Valley™ Toasted ® Pasta Quinoa Rice Yoplait Go-gurt Dunkers WHOLESOME PANTRY Oats Muesli ® Pizza Bagels Yoplait Light & Original Wholesome Pantry Organic Oatmeal Crisp™ Pizza Poppers Fridge Packs (8ct) Peanut Butter Peanut Butter Chocolate ® Popcorn Yoplait Kids Yogurt Wholesome Pantry Organic Blasted Shreds™ Multipack Refrigerated Baked Goods Frozen Fruit Raisin Nut Bran Yoplait® Trix™ Yogurt Wholesome Pantry Organic Rice Pasta Chowder ® Reese’s Puffs Multipack Maple Syrup Rice Shell Pasta Rice Chex™ Yoplait® (4-6oz) Wholesome Pantry Almond Snack Mix Strawberry Toast Crunch™ Yoplait® Smoothie Milk Soup Total™ YQ® by Yoplait® Yogurt Trix™ Wheaties™ SHOPRITE BRAND BAKING ShopRite Frozen Appetizers Betty Crocker™ Baking Mixes FROZEN ShopRite Flexible Straws Betty Crocker™ Frosting Green Giant™ -

99¢ 99¢ $1499

A-Z12S DIGITAL SAVINGS SO BIG THEY’RE BUSTING THROUGH THE DOOR! OFFERS VALID: SUNDAY, MARCH 7 THRU SATURDAY, MARCH 13, 2021 Sale $ 88 Sale $ 59 Price: 2 Price: 2 DIGITAL $ 89 DIGITAL ¢ Turkey Hill COUPON - 1OFF Bowl & Basket COUPON-71OFF Ice Cream FINAL PRICE Butter FINAL PRICE 48-oz. cont., Any Variety Sherbet, with Digital Coupon 1-lb. pkg., Quarters, with Digital Coupon Dairy Dessert, Light or Regular Salted or Unsalted (Excluding All Natural) ¢ $ 88 FOLLOW THESE LIMIT 4 PER VARIETY 99ea. 1ea. SIMPLE STEPS With an additional purchase of $10.00 or more Limit 1 With an additional purchase of $10.00 or more LIMIT 4 (excluding fuel and items prohibited by law). (excluding fuel and items prohibited by law). TO BIG SAVINGS! SIGN IN Visit shoprite.com or the ShopRite App to sign in or create an account to get started! 2-lb. Bag Sale $ 98 Sale $ 99 Price: 11 Price: 3 Cape Gourmet DIGITAL $ 00 DIGITAL $ 00 LOAD Jumbo EZ Peel COUPON- 2OFF COUPON- 2OFF FINAL PRICE Jimmy Dean FINAL PRICE Tap the Load to Card Shrimp with Digital Coupon with Digital Coupon button on each digital 21 to 25-ct./lb., Frozen, Bacon Responsibly Raised $ 98 12-oz. pkg., Any Variety $ 99 coupon you’re interested in. LIMIT 4 PER VARIETY 9ea. 1ea. With an additional purchase of $10.00 or more With an additional purchase of $10.00 or more (excluding fuel and items prohibited by law). LIMIT 4 (excluding fuel and items prohibited by law). LIMIT 4 REDEEM Scan your Price Plus® Club Card or enter your phone number at checkout. -

Fiscal 2018 Annual Report

FISCAL 2018 ANNUAL REPORT Fiscal 2018 Financial Highlights Change In millions, except per share and 52 weeks ended 52 weeks ended on a constant- profit margin data May 27, 2018 May 28, 2017 Change currency basis* Net Sales $ 15,740 $ 15,620 1% Organic Net Sales* Flat Operating Profit $ 2,509 $ 2,566 (2%) Total Segment Operating Profit* $ 2,792 $ 2,953 (5%) (6%) Operating Profit Margin 15.9% 16.4% -50 basis points Adjusted Operating Profit Margin* 17.2% 18.1% -90 basis points Net Earnings Attributable to General Mills $ 2,131 $ 1,658 29% Diluted Earnings per Share (EPS) $ 3.64 $ 2.77 31% Adjusted Diluted EPS, Excluding Certain $ 3.11 $ 3.08 1% Flat Items Affecting Comparability* Average Diluted Shares Outstanding 586 598 (2%) Dividends per Share $ 1.96 $ 1.92 2% Net Sales Total Segment Adjusted Diluted Free Cash Flow* Dollars in millions Operating Profit* Earnings per Share* Dollars in millions Dollars in millions Dollars $3.11 $3,154 $17,910 $2,218 $17,630 $3,035 $3,000 $3.08 $2,953 $16,563 $2,035 $2,792 $1,959 $15,740 $15,620 $1,936 $1,731 $2.92 $2.86 $2.82 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018 *See page 45 of form 10-K herein for discussion of non-GAAP measures. Fiscal 2018 Net Sales $15.7 Billion Total Company Net Sales by Product Platform Total Company Net Sales by Reporting Segment Our portfolio is focused on five global growth In fiscal 2018, we reported net sales in four platforms. -

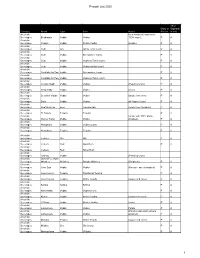

Pesach List 2020 1

Pesach List 2020 All or Dairy or Sephardi Category Brand Type Item Notes Pareve m only Alcoholic from Australia (made from Beverages Bushman's Vodka Vodka 100% cane). P A Alcoholic Beverages Chopin Vodka Potato Vodka (potato). P A Alcoholic Beverages Club Gin Gin & Tonic (corn). P A Alcoholic Beverages Club Vodka Screwdriver (corn). P A Alcoholic Beverages Club Vodka Vodka & Tonic (corn). P A Alcoholic Beverages Club Vodka Vodka Gimlet (corn). P A Alcoholic Beverages Cocktails for Two Vodka Screwdriver (corn). P A Alcoholic Beverages Cocktails for Two Vodka Vodka & Tonic (corn). P A Alcoholic Beverages Crystal Head Vodka Vodka (Peach & Corn) P A Alcoholic Beverages Deep Eddy Vodka Vodka (corn) P A Alcoholic Beverages Devotion Vodka Vodka Vodka (made from corn) P A Alcoholic Beverages Dixie Vodka Vodka all 4 types (corn) P A Alcoholic Beverages Dogfish Head Beer Tweason'ale (made from Sorghum) P A Alcoholic Beverages El Tosoro. Tequila Tequila P A Alcoholic (made with 100% Idaho Beverages Glacier Teton Vodka Vodka potatoes). P A Alcoholic Beverages Hampton's Vodka Vodka (Corn) P A Alcoholic Beverages Herradura. Tequila Tequila P A Alcoholic Beverages Iceberg Gin Gin P A Alcoholic Beverages Iceberg Rum Gold Rum P A Alcoholic Beverages Iceberg Rum Silver Rum Alcoholic Beverages Iceberg Vodka (Peach & Corn) Alcoholic James F.C. Hyde Beverages Whiskey Whiskey Sorgho Whiskey (Sorghum) P A Alcoholic Beverages Jinro Soju Vodka Vodka (Korean - sweet potatoes) P A Alcoholic Beverages Jose Cuervo Tequila Traditional Tequila P A Alcoholic Beverages Jose Cuervo Tequila White Tequila (agave and cane). P A Alcoholic Beverages Kahlua Kahlua Kahlua P A Alcoholic Beverages Kamchatka Vodka Vodka (corn). -

Earn 10 Box Tops on These Specially Marked Items at Costco

EARN 10 BOX TOPS ON THESE SPECIALLY MARKED ITEMS AT COSTCO CEREALS SNACKS ¨ Cheerios™ ¨ Nature Valley™ Almond Butter Biscuits ¨ Honey Nut Cheerios™ ¨ Nature Valley™ Oats & Honey Crunchy Granola Bars ¨ Multigrain Cheerios™ ¨ Nature Valley™ Fruit & Nut Chewy Granola Bars ¨ Cinnamon Toast Crunch™ ¨ Nature Valley™ Sweet & Salty Peanut Granola Bars ¨ Lucky Charms™ ¨ Mott’s® Fruit Snacks, 90 ct ¨ Annie’s® Friends Bunnies Organic Cereal ¨ Fruit by The Foot® Fruit Rolls MEALS YOGURT ¨ Annie’s® Mac & Cheese (Variety Pack) ¨ Go-GURT® Simple Yogurt DOWNLOAD BUY & SCAN EARN $ FOR BOX TOPS APP RECEIPT YOUR SCHOOL Offer available at COSTCO NO MORE CLIPPING *For each Box Tops For Education (BTFE) product purchased at Costco between 7/15/19-9/30/19, you can earn 10 Bonus Box Tops for your BTFE-eligible enrolled school. Multi-pack BTFE products purchased at Costco count as 1 participating product for purposes of this offer. To receive your Box Tops, your eligible receipt must be scanned in the App within 14 DAYS of your BTFE product purchase at Costco. Standard data rates may apply. Each product featuring the Box Tops logo is worth 10 cents (unless otherwise specified) to your participating school when you scan your receipt containing the participating product in the free Box Tops App. To join, download the App and support an eligible, enrolled school. Limit $20,000 per school per year for redemptions through the clip and receipt scanning programs. Limit $10,000 per App user per year for redemptions through receipt scanning. See www.BTFE.com for App Terms of Service, Official Program Rules, and Privacy Policy. -

An Eight-Hour Day Or a Big Strike,” the 1903 Operative Millers’, Nailers’, Packers’

UNIVERSITY OF CALGARY “An Eight-Hour Day or a Big Strike,” The 1903 Operative Millers’, Nailers’, Packers’, and Loaders’ Strike in the Minneapolis Flour Mills by Shannon Elizabeth Murray A THESIS SUBMITTED TO THE FACULTY OF GRADUATE STUDIES IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ARTS DEPARTMENT OF HISTORY CALGARY, ALBERTA SEPTEMBER, 2008 © Shannon Elizabeth Murray 2008 ISBN: 978-0-494-44650-8 ABSTRACT On September 21, 1903, men in the operative millers’, nailers’ and packers’, and loaders’ unions left the Minneapolis flour mills where they worked. On the 22nd, they returned as strikers walking a picket line, to support the eight-hour workday for the loaders. The three unions united under the International Union of Flour and Cereal Mill Employees (IUFCME) in 1902, and this was the first test of their solidarity. Throughout the strike divisions like age, birthplace, marital status, wage, and skill among the men were clear. The millwrights’ union, also IUFCME members, did not strike. The men who were married and had ties to the area were the most militant during the strike. The mill owners, members of the Citizens’ Alliance (CA), fought to undermine worker solidarity and establish the open shop. The strike failed, resulting in a strengthened CA and an open shop principle in Minneapolis. ii ACKNOWLEDGEMENTS I would first like to thank my advisor, Dr. Elizabeth Jameson, for her guidance and aid during my research and writing period. Also thanks to Dr. Kurt Hackemer, whose guidance and supervision during my undergraduate career has led me to where I am today. -

General Mills' 2005 Annual Report

General Mills 2005 Annual Report General Mills at a Glance Selected Brands Cheerios, Betty Crocker, Wheaties, Pillsbury, Gold Medal, Hamburger Helper, Old El Paso, Totino’s, Yoplait, Green Giant, Progresso, Bisquick, Nature Valley, Cascadian Farm, Grands!, Chex Mix, Lucky Charms, Pop.Secret, Bugles, Total, Häagen-Dazs, Chex, Muir Glen, Fruit Roll-Ups, Gardetto’s, Kix, Colombo, Wanchai Ferry, Latina, La Salteña, Forno de Minas, Frescarini, Nouriche, Cinnamon Toast Crunch U.S. Retail Bakeries and International Joint Ventures Foodservice Our U.S. Retail business This segment of our We market our products in We are partners in several segment includes the business generates over $1.7 more than 100 countries out- joint ventures around the six major marketing divisions billion in sales. We customize side the United States.Our world. Cereal Partners listed below. We market our packaging of our retail prod- largest international brands Worldwide is our joint venture products in a variety of ucts and market them to are Häagen-Dazs ice cream, with Nestlé. We participate domestic retail outlets includ- convenience stores and food- Old El Paso Mexican foods, in four Häagen-Dazs joint ing traditional grocery stores, service outlets such as Green Giant vegetables and ventures, the largest of which natural food chains, mass schools, restaurants and hotels. Pillsbury dough products. is in Japan. And we are merchandisers and member- We sell baking mixes and This business segment partners with DuPont in ship stores. This segment frozen dough-based products accounts for 15 percent of 8th Continent, which produces accounts for 69 percent of to supermarket, retail and total company sales.